- Bumpy peace. The US and Iran have reportedly agreed to a tentative 60-day extension of the ceasefire, which is awaiting President Trump’s approval, taking the steam out of oil and supporting bonds and equities.

- Headline market. Still, mixed signals and fresh military strikes have created a choppy, low-conviction “peace trade” with markets once again in a headline-driven regime.

- Strait up. Focus remains on whether this leads to a reopening of the Strait of Hormuz or simply prolongs the current stalemate, keeping geopolitical risk elevated and risk sentiment restrained.

- Data digest. Sub-consensus core PCE data had limited impact on Fed pricing, with markets holding off on dialing back rate hike expectations ahead of the next CPI print.

- Hawk migration. Central banks are increasingly leaning pre-emptively against inflation, with even previously dovish institutions (like the RBNZ) showing hawkish intent.

- Fed backstop. The Fed’s shift toward a more hawkish stance has become the key anchor for markets, supporting the US dollar even during risk-on moves.

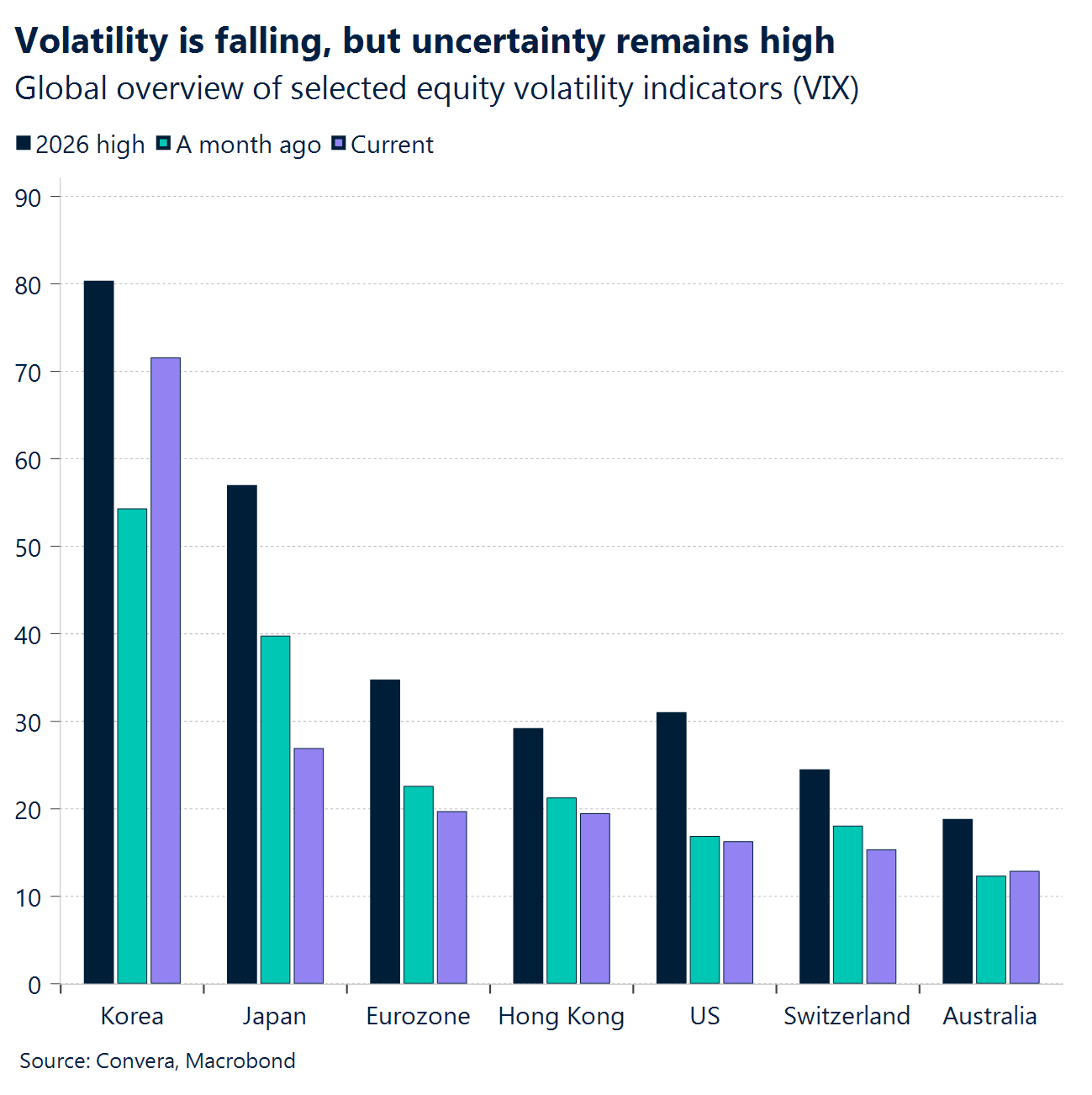

- FX paralysis. FX volatility remains low as the market slips into a low-conviction, rangebound phase amid conflicting macro narratives. The US dollar has outperformed in May but is down on the week.

Global Macro

Stagflation back on the radar

RBNZ holds. The RBNZ left the OCR at 2.25%, in line with expectations, but the commentary suggested the central bank is nearing a hike. The RBNZ said the Middle East conflict will keep inflation above target this year, slow the recovery, and that the OCR will most likely need to increase sooner and by more than it had projected in February, in other words, a hawkish hold.

Confidence firms. US Conference Board consumer confidence printed 93.1, beating the 92.5 consensus and showing households are holding up a bit better than feared despite higher prices. The details were mixed rather than outright strong, the present situation index fell, while expectations improved, so the signal was resilience, not reacceleration.

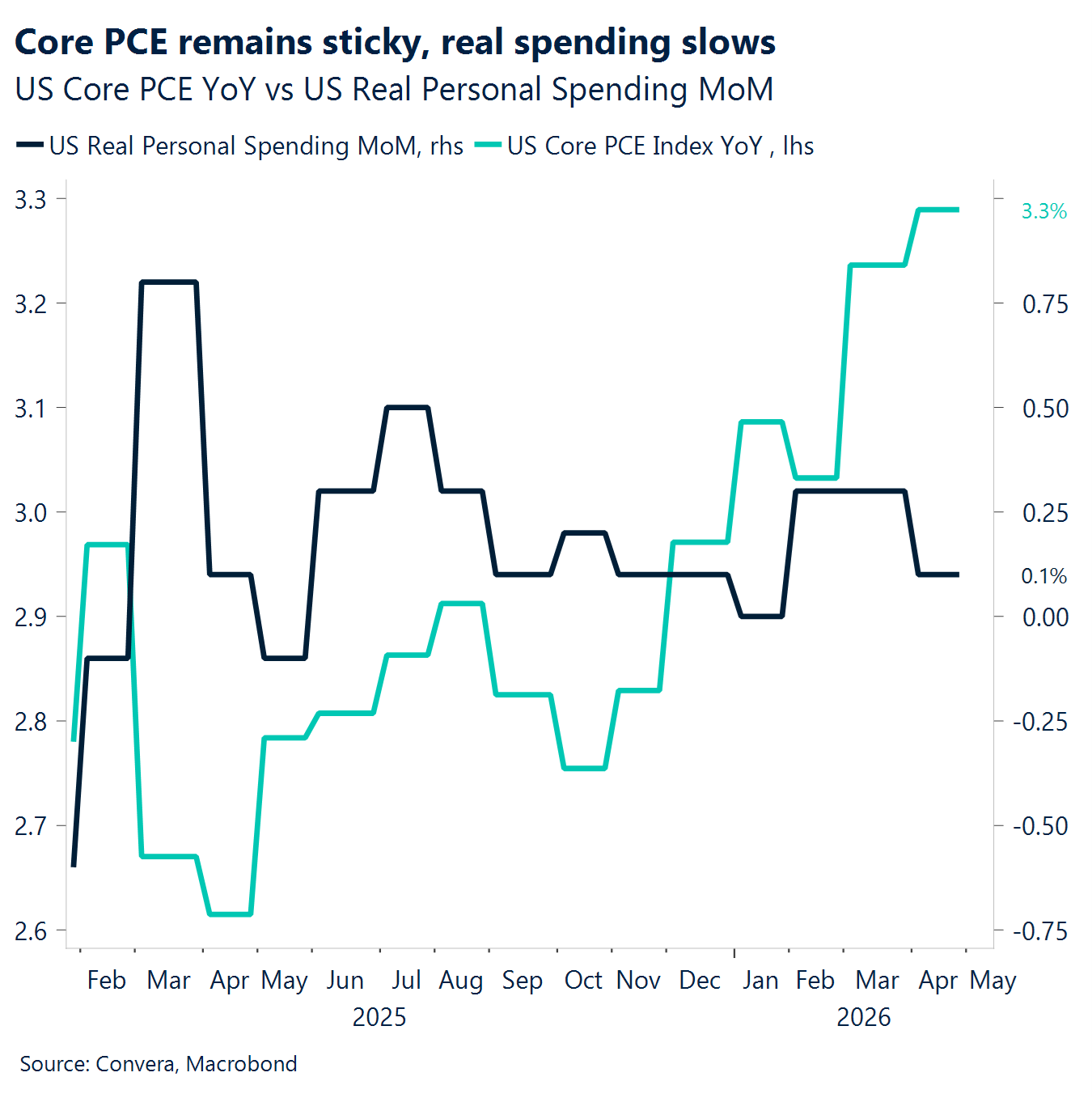

Growth revised. The big growth surprise this week was the downward revision to Q1 US GDP, with the second estimate coming in at 1.6% SAAR vs 2.05%. BEA explicitly said the downgrade from the advance 2.0% estimate mainly reflected weaker consumer spending and investment, which is important because it shifts the mix from “solid but inflationary” toward “softer growth with still-elevated prices.”

PCE cools. The inflation pulse was softer than feared. Headline PCE rose 0.4% m/m, below the 0.5% expectation, while core PCE came in at 0.2% m/m vs 0.3% expected; on the year, headline PCE was 3.8% and core PCE 3.3%, still high but not as hot as markets had worried after CPI/PPI earlier in the month.

Demand splits. Beneath the PCE print, the demand story was mixed. Personal income was basically flat at 0.0% m/m vs 0.4% expected, but personal spending still rose 0.5% m/m, in line with expectations, even though real personal spending increased only 0.1%. Meanwhile, goods demand looked much stronger on the surface: durable goods orders surged 7.9% m/m, far above the consensus.

Week ahead

Busy week for macro signals

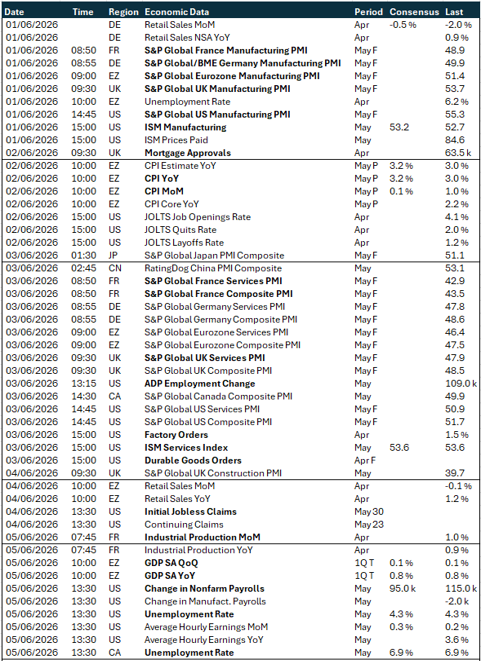

- Jobs report in focus. The highlight of the week will be the US May jobs report. The previous two releases were solid, with April adding 105k new jobs to the economy. It will be instructive to see whether this robust streak holds up despite ongoing conflict-related tensions. However, it may be premature to call a sustained rebound away from the softer tone seen in 2025 if the impasse over Hormuz persists.

- Prices set the tone for ECB. The Eurozone’s preliminary CPI print for May is also due. Country-level releases this week should remove much of the suspense ahead of next week’s aggregate release. That said, with inflation on an accelerating trajectory due to the conflict – and this being the final inflation snapshot before the ECB’s 11 June policy meeting – the data will be subject to close scrutiny.

- Activity data under the microscope. In the US, May’s ISM Manufacturing and Services PMI releases are due. Both indices have had a solid start to the year despite geopolitical tensions. Tax cuts from the “Big Beautiful Bill” and strong momentum in the AI sector have supported activity, although softer employment and higher prices-paid sub-indices point to a more fragile underlying backdrop. This is particularly evident in manufacturing, where expansion may partly reflect front-loading activity to avoid anticipated price pressures rather than expectations of sustained demand.

FX views

Conflicting narratives paralyze FX

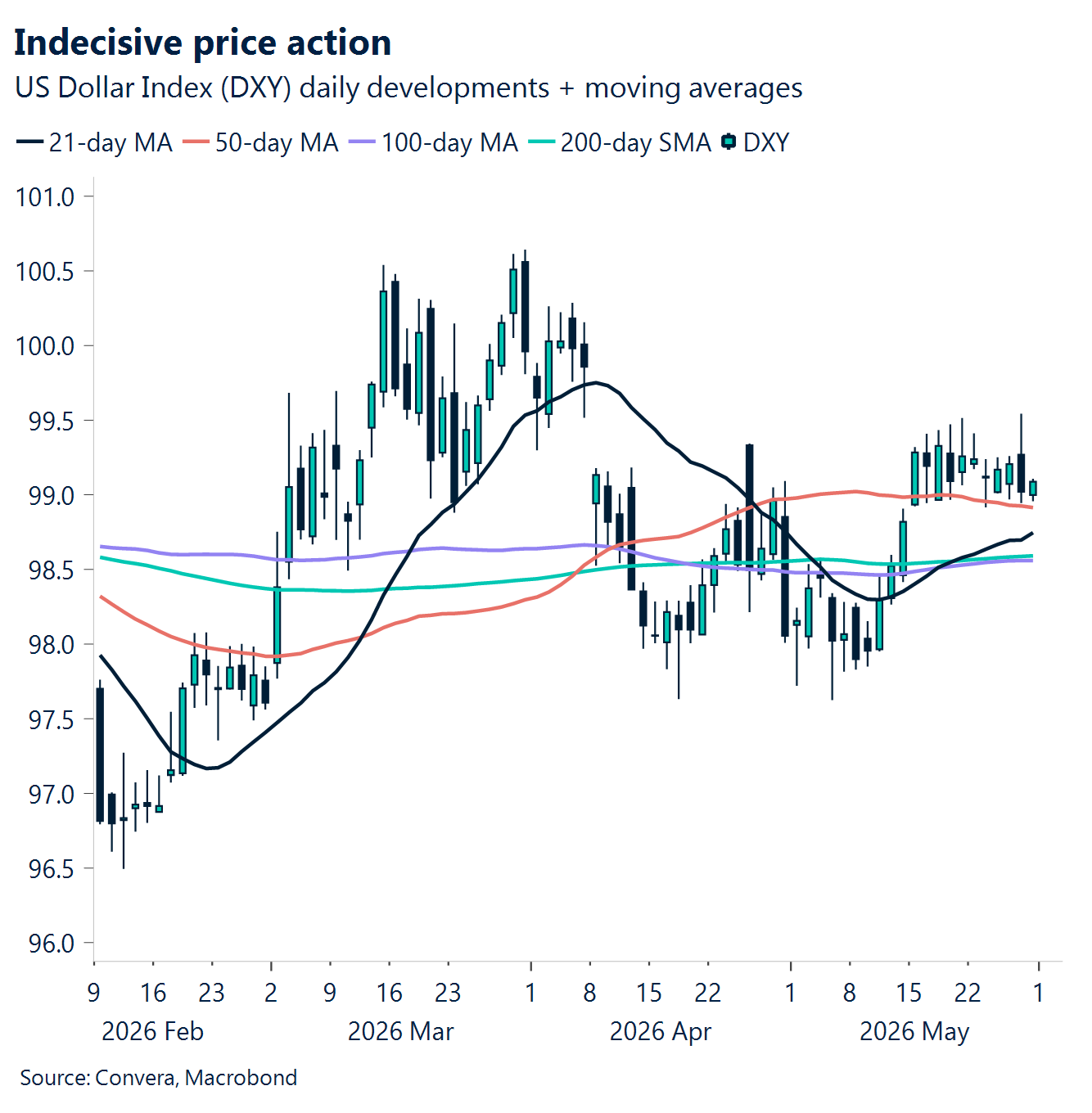

USD Dollar holds ground amid noise. The US Dollar Index (DXY) has traded range-bound since mid-May (99.0–99.5), as investors have failed to take a stronger directional view amid a flux of conflicting geopolitical headlines clouding the outlook. Hopes of a deal resurfaced as consensus grew that both sides may be working toward an interim agreement, prioritising the reopening of Hormuz while delaying more complex negotiations, such as nuclear issues. This type of arrangement appears more workable and achievable in the near term, helping to explain investors’ reluctance to abandon the de-escalation narrative, despite recent bouts of re-escalation. Meanwhile, May’s hawkish repricing of Fed policy expectations has strengthened the fundamental support for the dollar. The outlook into mid-June (the Fed’s policy meeting) appears mildly bullish for the greenback, under the base case that no meaningful progress emerges on Hormuz and incoming data continue to point to no urgency for easing from the Fed.

EUR EUR/USD drifts as conviction fades. EUR/USD continues to drift along the 1.16 level, appearing reluctant to push higher as buyers lack conviction that a US–Iran peace deal is imminent. At the same time, sentiment remains cautiously optimistic, helping the pair hold above the 1.16 handle. EUR/USD is currently around 1% lower month-to-date, having declined from the 1.18 area in early May, as hawkish Fed repricing has coincided with a partial unwind of the market’s previously more entrenched hawkish bias toward the ECB. Markets now price around 15bp of tightening for the Fed and 60bp for the ECB by year-end – the relative adjustment appears more balanced, and EUR/USD price action has correspondingly slowed. That said, a move below 1.16 appears increasingly likely should there be no meaningful progress on Hormuz, while incoming data continue to tilt the relative rates backdrop in a more hawkish direction for the US ahead of next month’s slate of central bank policy meetings.

GBP Supported but not strong. Sterling has traded in a narrow but fragile range this week, with GBP/USD holding above 1.34 but capped at 1.35, while GBP/EUR has slipped back toward 1.15 after once again failing to convincingly breach the 1.16 resistance ceiling. The absence of meaningful domestic data and a fading UK political risk premium has left the pound largely at the mercy of external forces. Resilient but restrained global risk sentiment, shaped by conflicting Middle East headlines, has resulted in a lack of conviction in either direction. The pound is broadly flat on the week versus the dollar but has underperformed higher‑beta peers, reflecting limited participation in risk‑on rallies. Importantly, GBP/USD remains down over 1% month‑to‑date, highlighting a more challenging underlying backdrop. USD strength continues to be supported by haven demand, hawkish Fed repricing, and relative US growth resilience, reinforcing “dollar exceptionalism.” Domestically, political risks have been priced but not resolved, with the timing of any leadership challenge still unclear. Combined with softer macro data and fading rate support, sterling remains “supported but not strong”, with upside capped and downside risks building.

CHF Intervention signals. The dominant CHF theme this week is the SNB’s explicit intervention posture, which is tempering franc strength despite elevated geopolitical risk. EUR/CHF weakness and USD/CHF range-trading reflect this tug-of-war between safe-haven demand and central bank pushback. SNB President Martin Schlegel reiterated the central bank’s increased willingness to intervene in the FX market, citing the situation in the Middle East. Schlegel noted that inflation “remains within the range of price stability,” with medium-term inflationary pressures largely unchanged, though inflation has risen recently. The SNB’s intervention stance is offsetting the franc’s traditional safe-haven appeal, as EUR/CHF bounced off a 9-week low.

CAD On the defensive. This week’s backdrop still leaned against the Canadian dollar. Renewed Middle East tensions kept broader risk sentiment uneasy, but the more durable driver remained rates, with the US–Canada 2-year spread still sitting near 120bp in favor of the US, continuing to tilt carry demand toward the dollar. That said, the relative-rate story was challenged somewhat by the end of the week, as the latest US data pointed to slower real spending and a downward revision to GDP, even though core inflation remained sticky. In other words, the US macro pulse was mixed and marginally narrowed the yield advantage, giving the Loonie some respite after USD/CAD touched a weekly high near 1.387. Technically, the pair has moved back above the 20-day (~1.372), 50-day (~1.375), and 100-day (~1.3723) moving averages and is now testing the 200-day near 1.3811, which remains the key hurdle preventing this from becoming a cleaner bullish breakout in USD/CAD. A sustained move above that level would strengthen the case for a retest of 1.3870 and potentially the 1.39 region, while failure there would suggest this latest move is still just a rebound within the broader range. On the downside, 1.3755 is the first support to watch, followed by the 1.3720/25 zone.

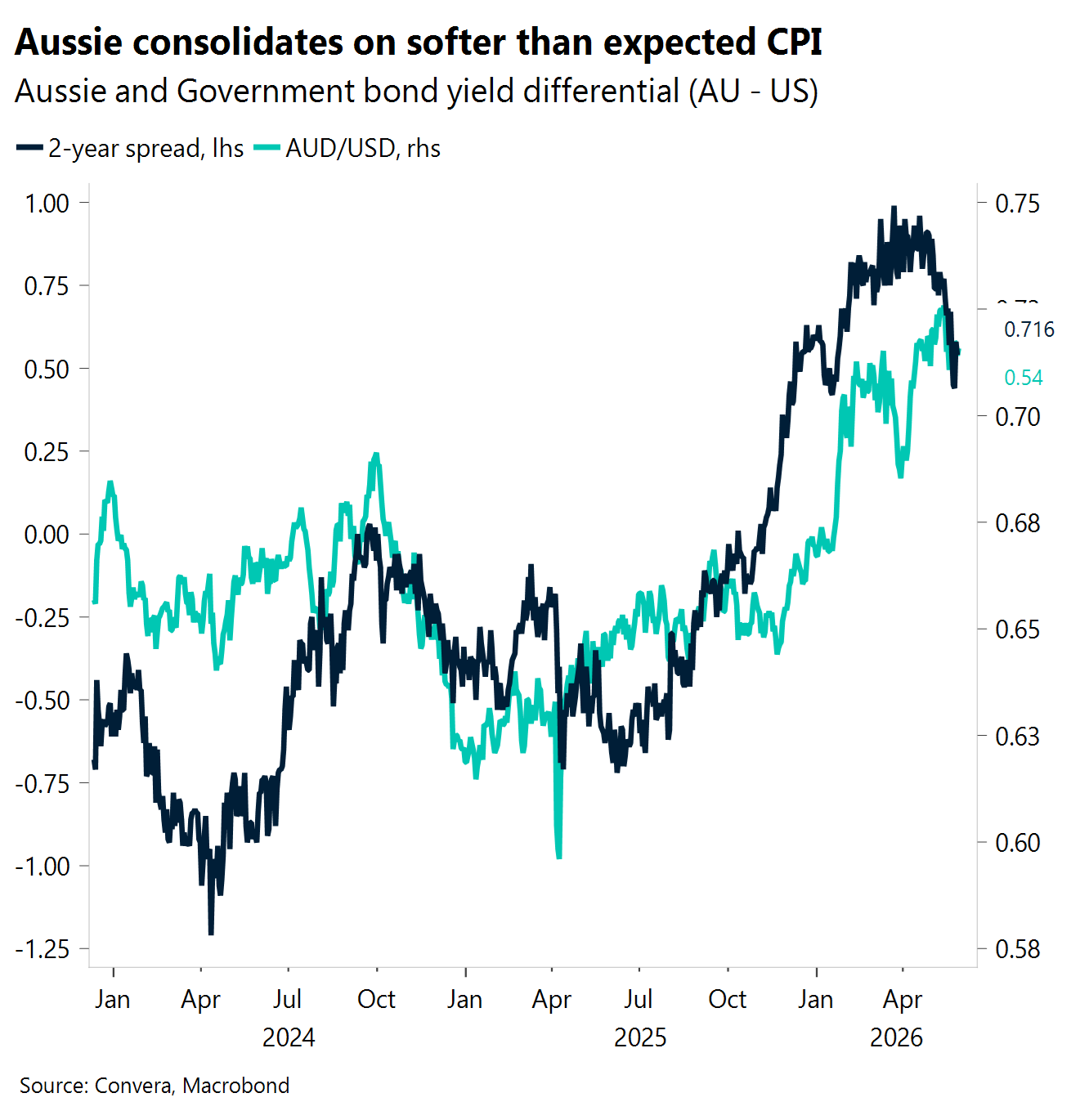

AUD Aussie slips on soft inflation read. Easing Middle East tensions and the sharp pullback in oil prices provided a modest tailwind to risk sentiment, which tempered some of the downside pressure on AUD. Earlier, AUD/USD pulled back after headline inflation came in below expectations, with the miss largely attributable to the reversal of the fuel excise rather than any genuine softening in underlying price pressures — the trimmed mean held steady. The softer print collided with stretched long positioning, prompting some holders to trim, but we see the market reaction as overdone given that core inflation remains reasonably firm. Positioning dynamics mean the pair remains highly sensitive to headline data in the near term. AUD/USD is sitting just 1.7% below its 6 May peak of 0.7278. Near-term support lies at the 21-day EMA around 0.7163, with the 50-day EMA near 0.7123 as the next floor if selling pressure extends. Initial resistance comes in at the key psychological handle of 0.7200. Upcoming current account, building approvals, GDP, and trade balance data will keep markets on watch.

CNH Xi’s Japan remarks catch Washington off guard. With oil prices down on ceasefire hopes, China’s status as one of the world’s largest crude importers makes a sustained Hormuz reopening providing modest tailwind to the Yuan via improved terms of trade. Reports that President Xi voiced unusually sharp criticism of Japan’s military build-up during his meeting with President Trump — catching US officials off guard — lent support to the yuan. Trump reportedly defended Japan’s stepped-up defence posture as a response to North Korean threats, but the episode laid bare simmering China–Japan tensions and Tokyo’s rising military spending as a live friction point. USD/CNH is at a three-year low and remains just above its recent trough of 6.7674 from 29 May. For the pair to build upward traction, it first needs to clear the 21-day EMA at 6.7987, with the 50-day EMA at 6.8279 as the next hurdle. Upcoming manufacturing and non-manufacturing PMI prints will be in focus.

JPY BoJ hike still in play. Tokyo’s inflation data came in below expectations across all measures in May. Headline CPI rose 1.4% y/y against a 1.6% consensus, core CPI excluding fresh food printed 1.3% versus a 1.5% forecast, and the core-core reading — stripping out both fresh food and energy — came in at 1.6%, undershooting the 1.8% expected. Despite the miss, OIS markets still have nearly 20bp of BoJ tightening priced for June, suggesting the rate hike narrative remains intact. USD/JPY is holding above 159.00, down roughly 1% from its 30 April peak of 160.72. Support sits at the 21-day EMA near 158.76, followed by the 50-day at 158.45 and the 100-day EMA at 157.56. Upcoming capital spending figures, the S&P Global Services PMI, and household spending data will be in focus.

MXN Consolidation move. This week, the peso story was still a tug-of-war between softer domestic growth and supportive external flows. Mexico’s Q1 GDP contraction of 0.6% q/q confirmed the economy lost momentum, especially in industry as manufacturers adjusted to US tariffs, but that weakness was partly offset by a much stronger April trade surplus of $4.52bn and a still-firm labor market with unemployment at 2.5%. At the same time, softer inflation helped keep the easing narrative alive, even as Moody’s downgrade to Baa3 and S&P’s negative outlook kept fiscal concerns in the background. The USD/MXN near 17.33 still looks like consolidation as the pair is hovering around the 20-day average (~17.31) but remains below the 50-day and 100-day (~17.47) and well below the 200-day (~17.90), so the medium-term bias still favors MXN unless USD/MXN can break meaningfully above the 17.45–17.50 area. For now, the range looks fairly well defined, with 17.20 as near-term support and 17.45 as the first meaningful resistance, which fits the macro picture of a peso that is no longer surging, but also not yet giving up its broader strength.

BRL Facing headwinds. This week’s backdrop turned a bit less friendly for the real, on renewed Middle East tensions along with fiscal concerns intensifying amid election-driven measures in Congress and investors reassessing the odds of another Lula term. At the same time, the central bank is clearly pushing back against any dovish interpretation: Nilton David flagged rising 2028 inflation expectations as a growing concern, warned that a global energy shock could worsen the longer-term outlook, and reiterated that rates will stay restrictive for long enough to bring inflation back toward target, with policy remaining firmly data-dependent and without forward guidance. Technically, the USD/BRL is trading around 5.04, having bounced from its late-April lows but still sitting within a broader medium-term downtrend; the pair is back above the 20-day average (~4.981) and now hovering just below the 50-day (~5.05), while the 100-day (~5.15) and 200-day (~5.27) remain well above and continue to frame the larger bearish structure in USD/BRL.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.