- Strait stakes. The Strait of Hormuz remains in focus as escalating US action against Iran raises the risk of renewed disruption to global energy flows, adding another layer of uncertainty to an already fragile geopolitical backdrop.

- Crude awakening. Brent crude oil is heading for its biggest weekly gain (>10%) since April, with the benchmark trading just below $85 a barrel.

- Headline relief, underlying heat. While softer US CPI data offered some relief, rising energy prices and upside risks within core PCE-linked PPI components suggest investors may be premature in pricing a benign inflation backdrop.

- No peace for bonds. Global yields are likely to stay elevated as the impact of war-driven supply disruptions boosts the risk of increased inflation pressures and pushes major central banks to maintain or enhance their hawkish stances

- Bellwether to bear-wether. The plunge in South Korea’s equity index is testing confidence in the AI-led rally, as persistent weakness in semiconductor stocks threatens to undermine one of the market’s most important bullish narratives.

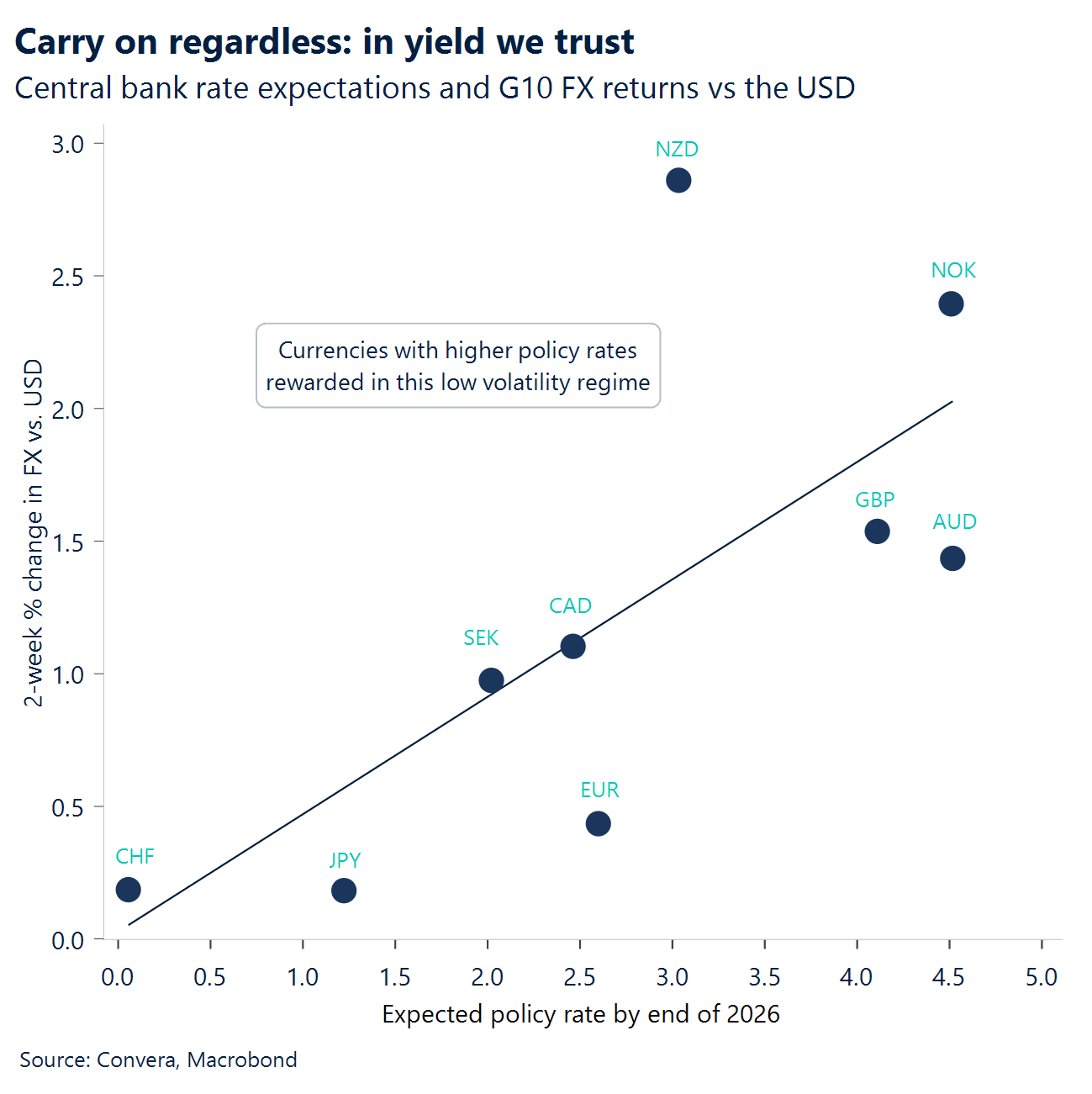

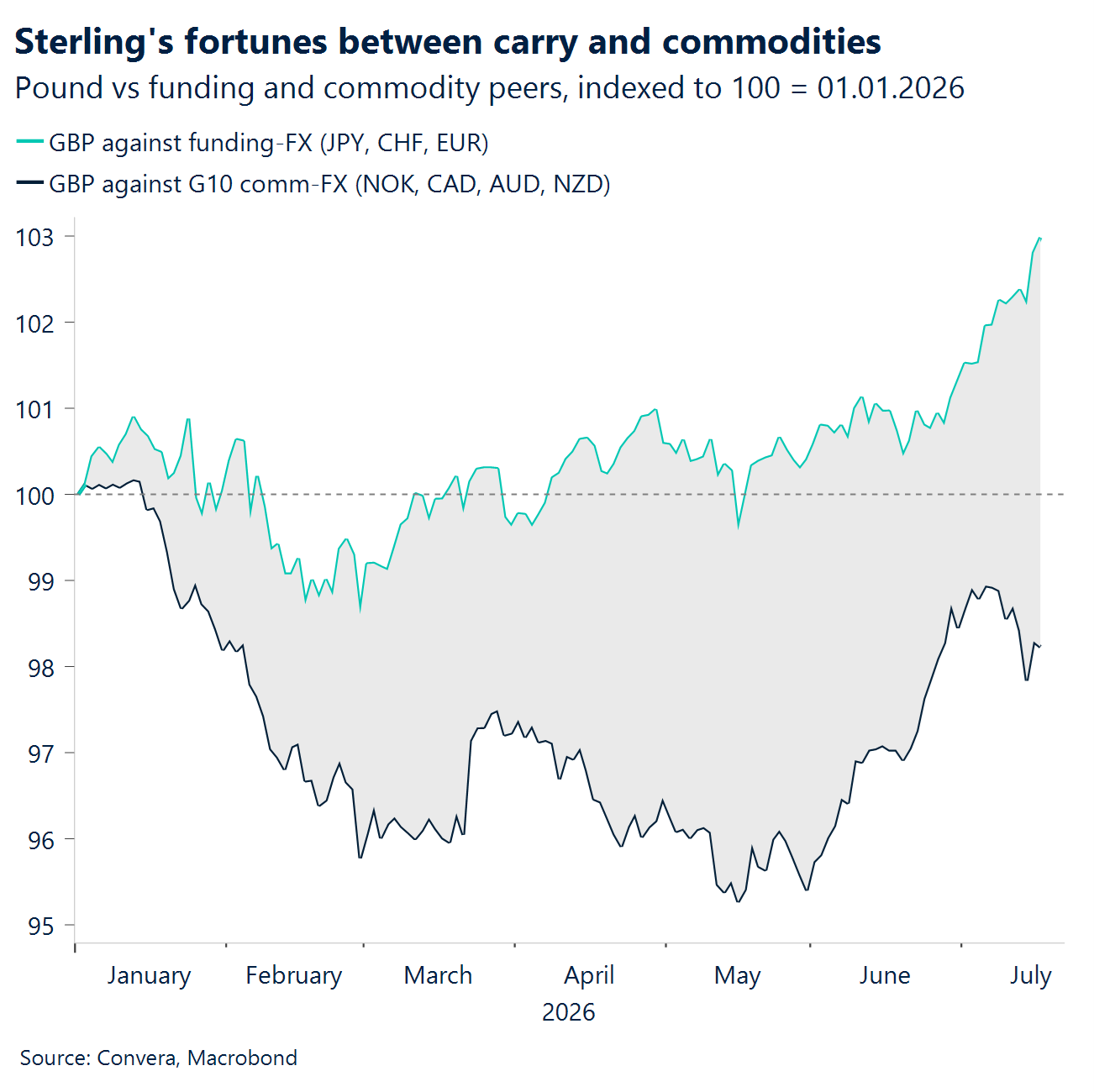

- Carry is King. Despite risk off conditions limiting gains, low FX volatility and persistent policy divergence remain fertile ground for carry, supporting high-yielders like GBP, AUD, NOK and NZD in the near term.

- Low conviction. Overall, beneath the headlines, markets remain stuck in a higher-for-longer equilibrium, with low volatility reflecting indecision rather than confidence.

Global Macro

Inflation cools, growth refuses to crack

US CPI relief. US CPI cooled more than expected, with headline CPI at -0.4% m/m vs roughly -0.2% expected and 3.5% y/y vs 3.8% expected, helped by a sharp drop in energy prices. Core CPI was also softer, coming in flat m/m vs +0.2% expected and 2.6% y/y vs 2.9% expected, giving markets the cleanest disinflation signal in weeks.

PPI confirms. Producer prices reinforced the softer inflation message, with PPI final demand at -0.3% m/m vs -0.1% expected and 5.5% y/y vs 6.2% expected. The downside was led by goods and energy, but the core ex-food, energy and trade-services gauge still rose 0.1% m/m and 5.1% y/y, so pipeline pressure eased but did not disappear.

US activity holds. US retail sales rose only 0.2% m/m, in line with expectations, but lower gasoline receipts held down the headline and underlying momentum looked better. Jobless claims fell to 208k vs 217k expected, the lowest in over two months, while the Philadelphia Fed index jumped to 41.4 vs 13 expected, its strongest reading since late 2021.

China disappoints. China’s Q2 GDP slowed to 4.3% y/y vs 4.5% expected, missing forecasts and highlighting weak domestic demand. June retail sales improved to +1.0% y/y vs -0.1% expected and industrial production rose 5.3% vs 4.7% expected, but the overall message stayed uneven: factories and exports are holding up better than households and investment.

Canada improves. The Bank of Canada held rates at 2.25%, as expected, and its tone improved as officials said growth is picking up and inflation should ease from its recent spike. Canada also delivered stronger factory data, with manufacturing sales rising 1.3% m/m vs 1.1% expected, reaching a record C$78.1bn in May.

Week ahead

ECB to kick off summer policy decisions

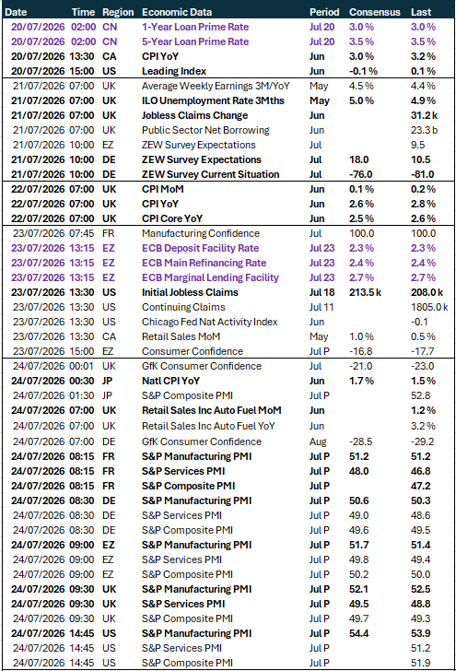

•Sterling faces a key test. Next week brings the UK’s labour market and inflation reports, providing a major test for both the Bank of England’s policy outlook and sterling’s recent resilience. A relatively quiet data calendar so far this month has shielded the pound from the dovish repricing seen in Fed and ECB expectations after both delivered softer-than-expected inflation readings. Investors will now be watching closely to see whether UK inflation also surprises to the downside, particularly following the sharp decline in oil prices.

•ECB’s active hold. The ECB meets on 23 July, with markets widely expecting rates to remain unchanged. However, the decision is likely to be framed as an “active hold” rather than a signal that the tightening cycle is over. Given ongoing geopolitical uncertainty and the recent escalation between the US and Iran, policymakers are likely to preserve a tightening bias and maintain maximum flexibility. That stance, combined with limited progress toward de-escalation in the Middle East, should help consolidate expectations for a September rate hike in the coming weeks.

•PMIs in focus. Next week will also provide an important test of global sentiment through the release of July PMI surveys across several major economies. The year started on a relatively solid footing before geopolitical tensions intensified in March, weighing on growth expectations while fuelling concerns about inflation. Particular attention will be paid to the prices-paid components, which may offer an early indication of whether this month’s renewed escalation is already beginning to reverse the more benign inflation trend that had emerged following the drop in oil prices.

FX views

Directionless ahead a busy policy slate

USD Losing momentum, not support. The dollar index has lost some bullish momentum after slipping below its 21-day moving average near 101.00, with softer-than-expected inflation prints driving the move. Even so, the near-term outlook remains broadly supportive for the greenback. While the latest geopolitical re-escalation has yet to trigger meaningful safe-haven demand, it is likely to reinforce the Fed’s tightening bias. Moreover, even in a synchronised hawkish cycle, the dollar tends to attract disproportionate support owing to its role as the world’s primary funding currency, with tighter liquidity conditions typically boosting demand for USD funding. Further out, downside risks remain should de-escalation regain momentum, paving the way for another dovish recalibration of the Fed’s policy outlook. In the meantime, with Fed officials in their blackout period ahead of the 29 July policy meeting, the dollar is likely to consolidate within the 100.00-101.00 range, though risks remain skewed to the upside should the US-Iran conflict escalate further.

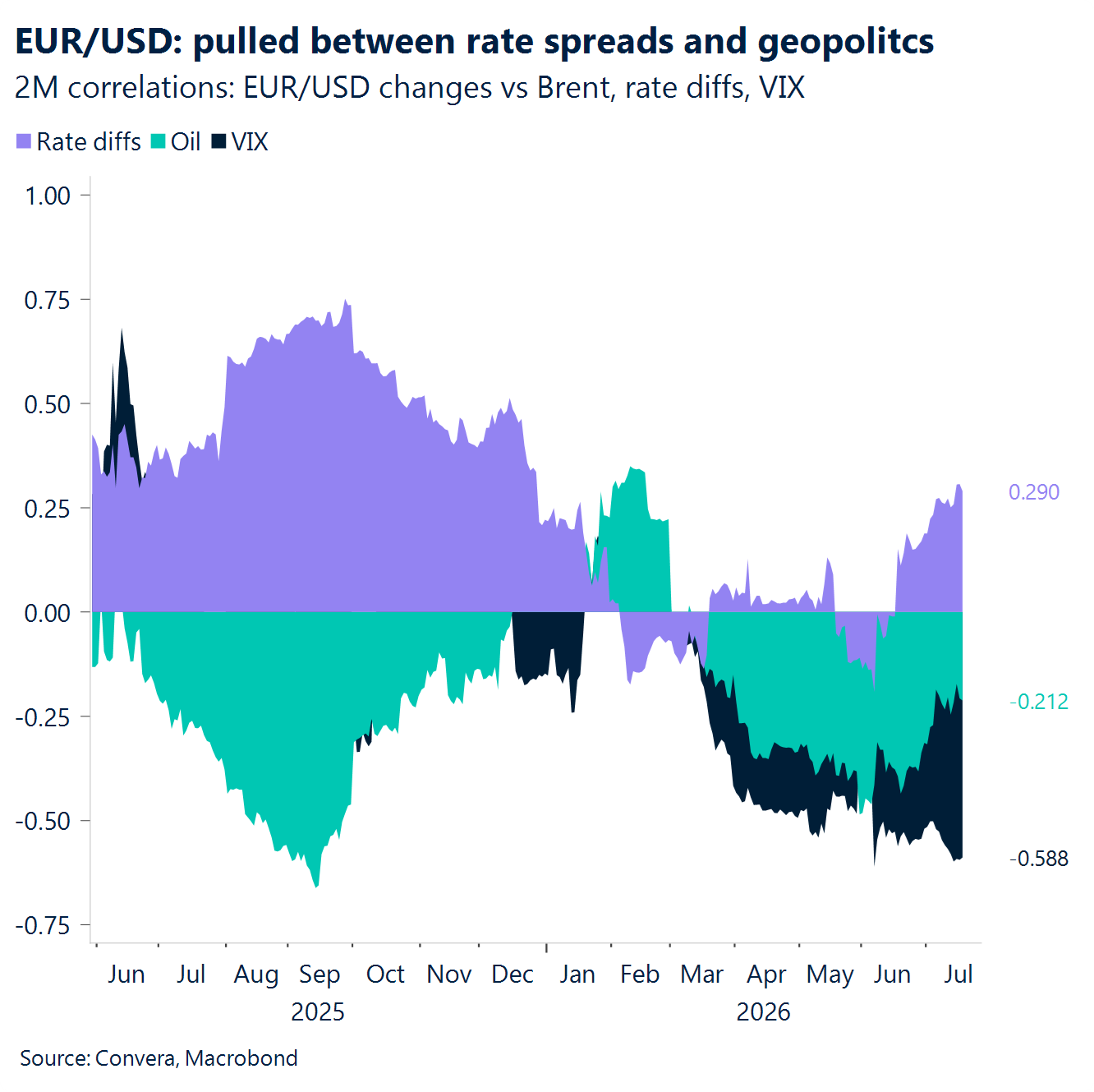

EUR Stuck around 1.14. EUR/USD has traded with little directional conviction through most of July. The pair has drifted higher from the one-year low of 1.1325 reached on 24 June, although that move has been driven more by a lack of strength in its two main bearish catalysts than by any intrinsic bullish momentum behind the euro. A hawkish Fed and geopolitical risks remain the clearest downside forces for the single currency. The former is being pulled between softer-than-expected inflation prints and renewed geopolitical tensions that cloud the disinflation outlook. The latter gained traction this week but has so far failed to trigger full-blown risk aversion across markets. The dollar, therefore, has struggled to draw meaningful safe-haven support. Absent a more prolonged geopolitical escalation, EUR/USD should continue to hover around the 1.14 handle heading into the month-end slate of central bank meetings.

GBP Alive and carrying. Sterling enjoyed another broadly constructive week, supported by carry demand, easing political risk premia and a benign volatility backdrop. GBP/USD rallied to its highest level since mid-May, recording its third-strongest daily gain of 2026, as softer US labour market data weighed on the dollar and optimism around the composition of a future Burnham-led government supported UK assets. GBP/EUR also extended its recent rally, breaching 1.18 to reach a fresh one-year high before easing back. Momentum indicators pushed into overbought territory and front-end rate spreads no longer fully justify current levels, suggesting the rally versus the euro has become stretched. Even so, carry dynamics remain supportive in a low-volatility environment, with the euro, yen and franc increasingly being used as funding currencies against higher-yielding sterling. Reflecting this, GBP/JPY touched its highest level since 2008, while GBP/CHF reached a one-year high. Looking ahead, attention shifts to UK labour market data, inflation, retail sales and flash PMIs. These releases will help determine whether current BoE pricing remains justified and whether sterling can maintain the rate advantage that has underpinned much of its recent outperformance. Markets will also closely monitor Andy Burnham’s first days as prime minister, with cabinet appointments likely to shape investor confidence in the UK’s fiscal trajectory.

CHF Favored funder. A common theme of 2026 persists – despite lingering geopolitical uncertainty and periodic haven demand, CHF has struggled to attract sustained inflows as exceptionally low FX volatility continues to support carry strategies. With volatility subdued across major currency pairs, investors have become increasingly comfortable borrowing in low-yielding currencies to fund higher-yielding positions elsewhere. In that environment, the franc has emerged as an attractive funding currency alongside the yen, creating a persistent source of selling pressure. This dynamic reinforces the broader CHF narrative. Domestic fundamentals remain supportive, with resilient growth, firmer inflation and fading expectations of negative rates providing an underlying floor. However, the SNB’s repeated emphasis on its willingness to intervene continues to deter aggressive CHF buying, even during risk-off episodes.

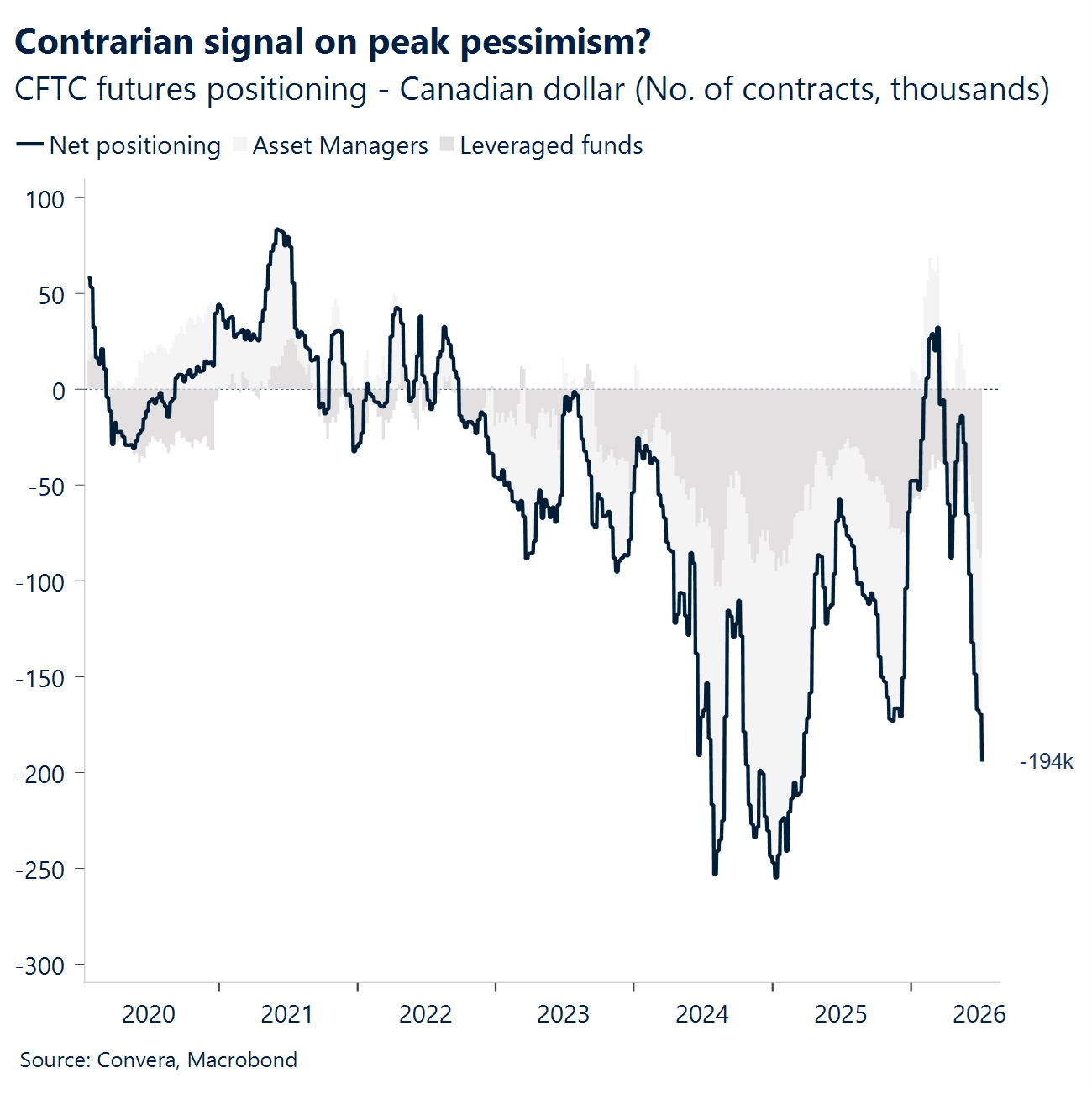

CAD Negative sentiment, CAD recovers. USD/CAD has slipped back toward 1.4050 after softer US CPI and PPI cooled the dollar’s rate-support story and pulled the pair further below 1.41. Lower US inflation reduces near-term Fed hike risk and eases pressure from yield spreads that had worked against the Loonie, while firmer oil adds some secondary support for CAD. Canada’s backdrop has also improved at the margin: the Bank of Canada held at 2.25%, said growth is picking up, and manufacturing sales rose 1.3% m/m to a record C$78.1bn in May. From a technical perspective, the USD/CAD sits below the 20-day moving average near 1.416, but still above the 50-day at 1.397, 100-day and 200-day at 1.385, so the rally has cooled and consolidated. Positioning remains a headwind for CAD, with net Canadian-dollar exposure near-194k contracts, the weakest sentiment backdrop since end of 2025. The next test is 1.4000–1.3978; a break below that relies on the US disinflation story gaining more momentum. Next week, focus is on CPI (Mon) for the month of June, where markets are expecting a YoY print of 3.1%, coming down slightly from 3.2%. Retail sales (Thu) will be also a key datapoint to monitor.

AUD Aussie loses momentum. Australia’s inflation expectations eased to 4.7% in July, the lowest level since January, reducing pressure for further interest rate hikes. At the same time, the escalating US-Iran conflict and growing uncertainty in global energy markets have kept investors cautious, limiting gains for the currency. Markets are pricing in only a 20% chance of a rate hike at the August RBA meeting. We are monitoring AUD/USD at 0.6950, followed by 0.6900, as the next key psychological support levels. On the upside, resistance is located at the 50-day EMA of 0.7011. AUD/USD has staged a modest rebound, although a sustained move above the 50-day EMA is needed to confirm stronger upside momentum.

CNH US-China trade concerns linger. Trade tensions between the US and China remain in focus as Washington believes Beijing is falling short of previous commitments. However, US officials are avoiding a public dispute for now to preserve upcoming diplomatic engagements. Rare earth exports remain a key sticking point ahead of future negotiations. Investor sentiment was also dampened after Chinese President Xi Jinping’s keynote address at the World AI Conference in Shanghai (July 17–20) focused on AI safety, governance and risk management rather than fresh stimulus or investment measures, disappointing those hoping for stronger policy support. Meanwhile, rising regional security tensions and the threat of supply chain disruptions continue to weigh on sentiment. USD/CNH remains close to its three-year lows. The pair is trading just 0.4% above its June 17th trough of 6.7539. A break above the 21-day EMA at 6.7851 could pave the way toward the 50-day EMA at 6.7953, while support is seen at 6.7700.

JPY USD/JPY nears 40-year high. The Japanese yen remains under pressure, with USD/JPY trading just below the 162.84 peak, a level not seen in around 40 years. Comments supporting greater investment through Japan’s Government Pension Investment Fund (GPIF) briefly lifted the yen, but the effect faded as many viewed the proposal as difficult to implement in the near term. The yen showed little reaction to official warnings, highlighting the limited effectiveness of verbal intervention alone. Higher oil prices, concerns over Japan’s fiscal outlook, and renewed Middle East tensions have continued to support demand for the US dollar. Uncertainty surrounding the government’s policy direction has also weighed on sentiment, while expectations for further yen weakness remain widespread. USD/JPY is trading just below the 162.84 high on July 1st . We see support at the 21-day EMA of 161.83, followed by the 50-day EMA at 160.84 and the 100-day EMA at 159.53. Resistance stands at 162.84, with the next hurdle at the key psychological level of 163.00. Meanwhile, NZD/JPY has climbed to its highest level in more than a month.

MXN Peso supported. USD/MXN remains biased lower after softer US CPI and PPI reduced Fed-hike anxiety, pulled US yields down and gave Mexico’s carry trade fresh support. The pair is trading near 17.42, after failing to sustain a move toward the 200-day moving average at 17.7, while spot now sits around the 20-day at 17.47, the 50-day at 17.37 and the 100-day at 17.48, leaving the pair in a narrow consolidation band. Banxico’s hold at 6.50% keeps the peso’s rate cushion intact, and the latest minutes support an extended pause: most board members saw the current rate as adequate to guide inflation back toward target, with economic slack, peso strength and fading cost shocks helping the disinflation story, even as sticky services inflation keeps policy cautious. That aligns with the broader setup for MXN: lower US inflation gives investors more room to lean into carry, while Banxico avoids sounding dovish enough to undermine the currency. The next local tests are retail sales on July 21, bi-weekly CPI and core CPI on July 23, IGAE activity on July 23, and unemployment on July 24; However, near term momentum keeps pegged to global sentiment and US dollar volatility.

COP Reversion risk. USD/COP remains under heavy downside pressure, with spot near 3,230 after touching levels that sit roughly 12.5%–12.7% below the 200-day moving average, a stretch that has been seen only a handful of times over the past two decades. The pairis well below the 20-day average at 3,362, the 50-day at 3,537, the 100-day at 3,604, and the 200-day at 3,693, confirming a deeply extended Colombian peso rally. The political catalyst remains supportive for COP, as markets continue to price a lower policy-risk path after Abelardo de la Espriella’s stronger-than-expected election showing, but the technical setup now looks statistically stretched. Historical episodes of similar deviations below the 200-day average have often been followed by a normalization rebound toward the trend line, with timing ranging from a few weeks to several months. That does not mean the peso rally has to end immediately, but it does raise the risk that USD/COP is entering a zone where further peso gains become harder to sustain and mean-reversion pressure starts to build.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.