- Kick-off into gridlock. As the World Cup kicks off, markets face their own pressure game – energy risks had kept inflation in play and hawks on the pitch, though tentative US‑Iran deal signals now offer a potential route out of the stalemate.

- Fatigue-driven resilience. After weeks of flare‑ups, markets snap back into risk‑on mode – Trump’s claimed Iran breakthrough sends equities and bonds higher and oil lower, as investors once again price de‑escalation despite a history of false starts.

- Inflation shoots higher. US CPI tops 4% with little market reaction because energy is a large part of the problem. But a hotter‑than‑expected PPI, led by ‘supercore’, tempered dovish hopes.

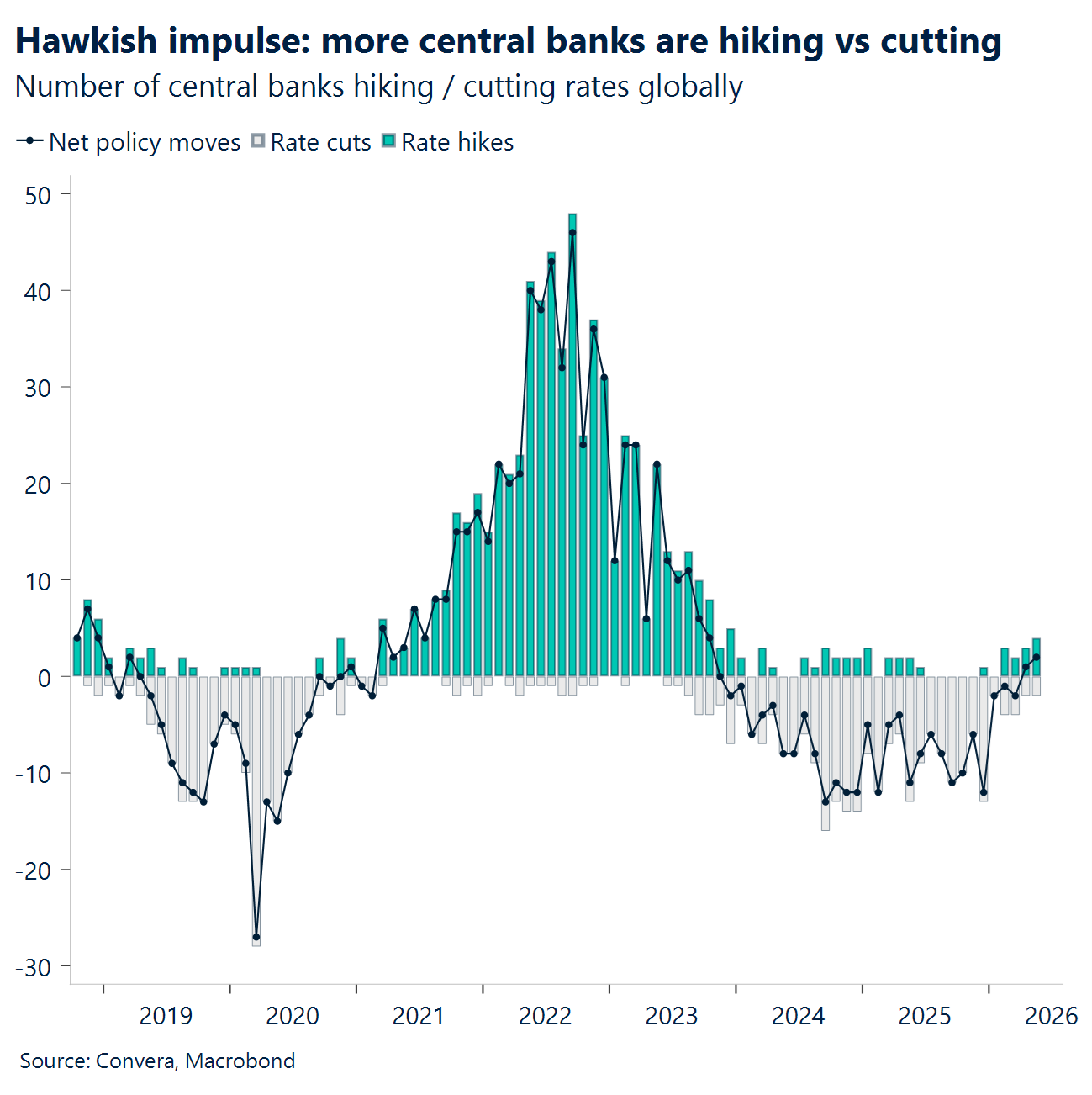

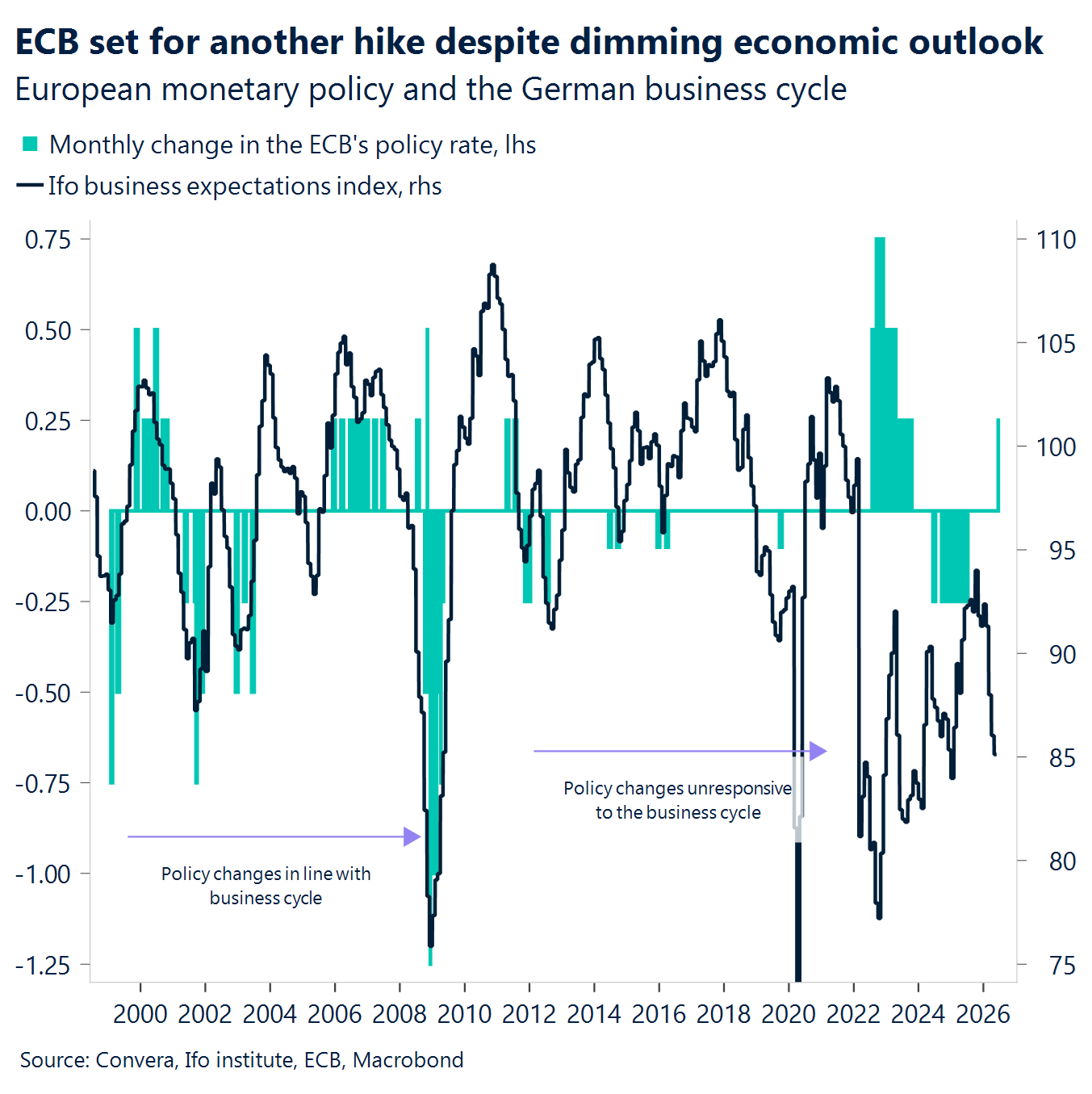

- Hold vs. hike. While the Bank of Canada stays on the sidelines, the European Central Bank grabs the armband – ending a three‑year hike drought to lead the G7’s hawkish attack.

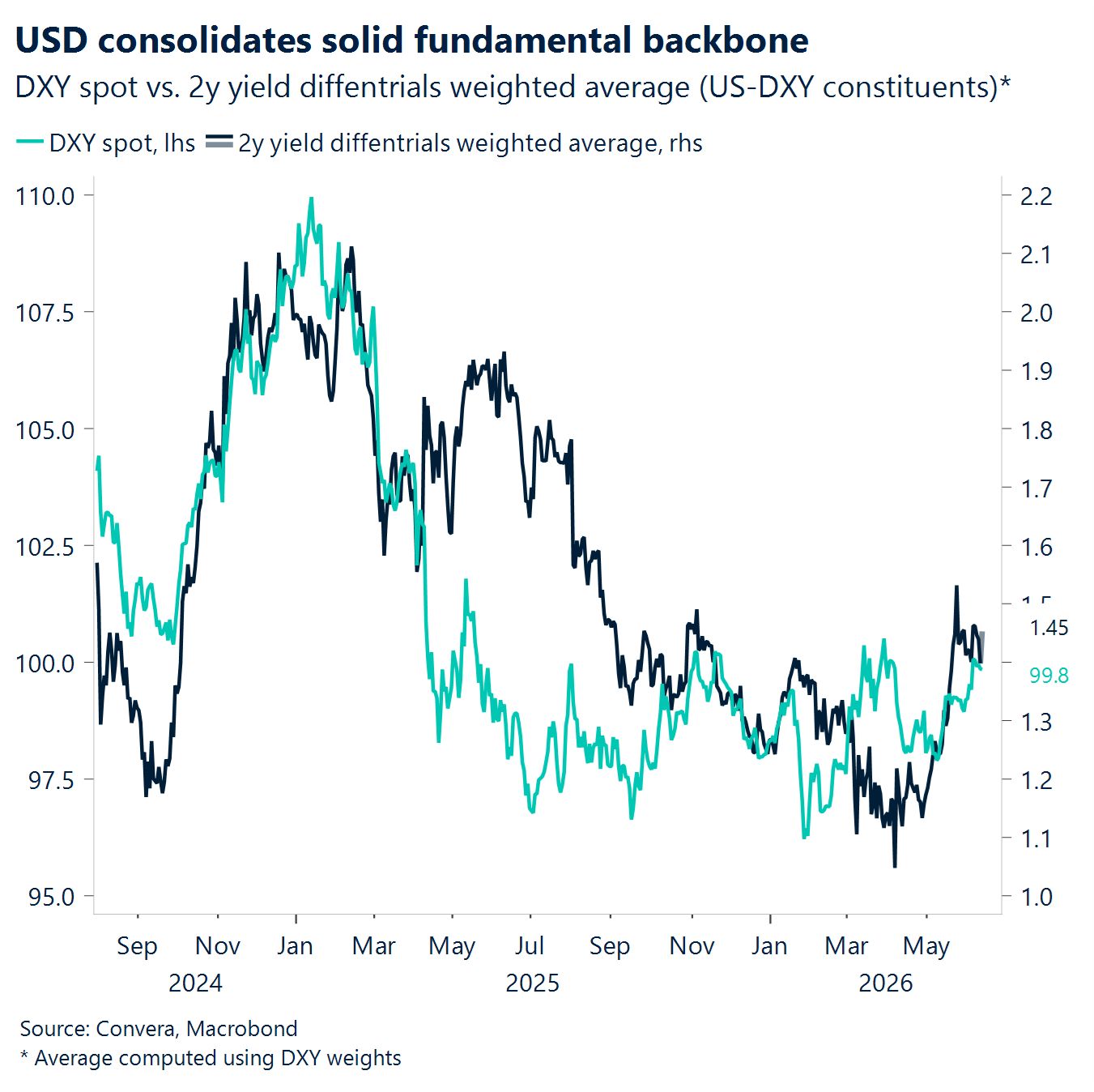

- Sideways play in FX. Limited conviction keeps currencies pinned, with no side willing to shoot decisively. The USD is down modestly on the week, but EUR and GBP are struggling to convincingly recapture 1.16 and 1.34, respectively.

- Big fixtures loom. The Fed headlines a run of central bank meetings next week, while a UK by‑election poses a wildcard risk for sterling.

Global Macro

ECB hikes as inflation keeps policy tight

ECB hikes. The ECB lifted the deposit facility rate to 2.25%, as expected, even as euro area growth remains weak. The hike is aimed at preventing higher energy prices from becoming embedded in broader inflation. Lagarde also kept the door open to another move, with end-2026 inflation expectations rising to 3.0% y/y from 2.6% y/y and the Governing Council still flagging upside inflation risks amid a highly uncertain outlook.

US inflation mix: US headline CPI came in as expected at +0.5% m/m and +4.2% y/y, but core CPI was softer at +0.2% m/m vs +0.3% expected and +2.9% y/y vs 3.0% expected. The softer core read was offset by hotter producer prices, with PPI final demand at 6.5% y/y vs 6.4% expected and core PPI at 5.4% y/y, in line with forecast, so pipeline pressure stayed very much alive. Add in initial claims at 229k vs 220k expected and continuing claims at 1.795m vs 1.780m expected, and the US mix still reads as softer core inflation, but no clean easing in broader price pressure or labor slack.

North America split. Mexico’s May CPI cooled to 3.94% y/y vs 4.03% expected, with core CPI at +0.22% m/m vs +0.24% expected, reinforcing the disinflation trend. In Canada, the Bank of Canada held at 2.25%, as expected, and leaned on weak domestic activity and elevated external uncertainty.

Asia divergence. Japan’s Q1 GDP final held at +0.5% q/q vs +0.3% expected, confirming that the first-quarter growth pulse was firmer than markets had penciled in. China’s May CPI printed +1.2% y/y vs +1.3% expected, while monthly CPI fell-0.1% m/m, which points to softer underlying demand even as producer-side inflation stays elevated.

Week ahead

Central banks take centre stage

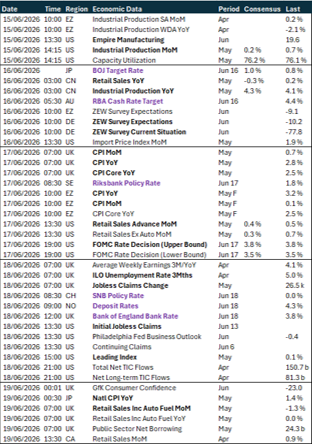

- Policy in focus. Next week brings a busy central bank calendar. For EMEA, focus will be on the Federal Reserve (Fed) and the Bank of England (BoE). Both are expected to hold, with markets pricing in one additional hike for the Fed and close to two for the BoE by year‑end. At the Fed, attention will centre on Kevin Warsh, the newly appointed Chair replacing Jerome Powell. Given ongoing concerns around potential sensitivity to political pressure for lower rates, markets will closely scrutinise his communication and tone at the press conference.

- Softening backdrop. In the UK, April’s labour market report is due. May’s release provided further evidence of a softening backdrop, with geopolitical tensions weighing on the macro outlook and complicating the BoE’s policy path.

- Sentiment under test. In the euro area, June’s ZEW survey for both Germany and the wider bloc will be in focus. Against a backdrop of higher energy costs and tighter financial conditions, the downward trend in sentiment since the February peak is expected to extend.

- Makerfield vote to test Starmer. Beyond macro data, attention will also turn to the Makerfield by‑election. A victory for Andy Burnham, currently mayor of Manchester, would mark a return to Westminster and reopen questions around UK political leadership as pressure builds on Keir Starmer.

FX views

Action escalates, rhetoric softens

USD Dollar held in check amid conflicting geopolitics. The dollar index, or DXY, remains broadly unchanged relative to the start of the week, despite renewed flare-ups between the US and Iran. Episodes of escalation have met more conciliatory rhetoric from the US administration, which has helped contain gains in oil prices and, in turn, limited upside for the dollar. On the macro front, this week’s CPI release came in broadly in line with expectations but showed signs of building inflationary pressure. Combined with the recent run of firm labour market data, this reinforces the case for a more hawkish Fed stance through the remainder of the year, keeping the dollar supported. Markets are currently pricing in roughly one rate hike by year‑end. On renewed de-escalation optimism, we expect the DXY to remain below the 100 level into week-end. A move back above that threshold appears more likely next week if the weekend brings little tangible peace progress and markets are faced with a hawkish Warsh at the upcoming policy meeting.

EUR ECB fails to excite. The euro drew limited support from a hawkish‑leaning ECB at its June meeting, with EUR/USD failing to reclaim the 1.1550 area after slipping below 1.16 last week on the back of firm US data. It took renewed optimism around Hormuz to drive a more meaningful push higher toward 1.16. While Lagarde acknowledged that inflation pressures are building beyond energy, the overall tone toward further hikes remained non‑committal. Markets are currently pricing one further hike by September and two by year‑end, while inflation expectations over the next 12 months sit around 3% in the 1‑year swap. The ECB’s upward revision to its inflation projections broadly aligns with this view, suggesting a higher bar for further hawkish repricing and additional euro gains. For now, EUR/USD remains driven by geopolitical developments and the Fed policy outlook into next week, with a test of 1.15 likely barring tangible peace progress over Hormuz.

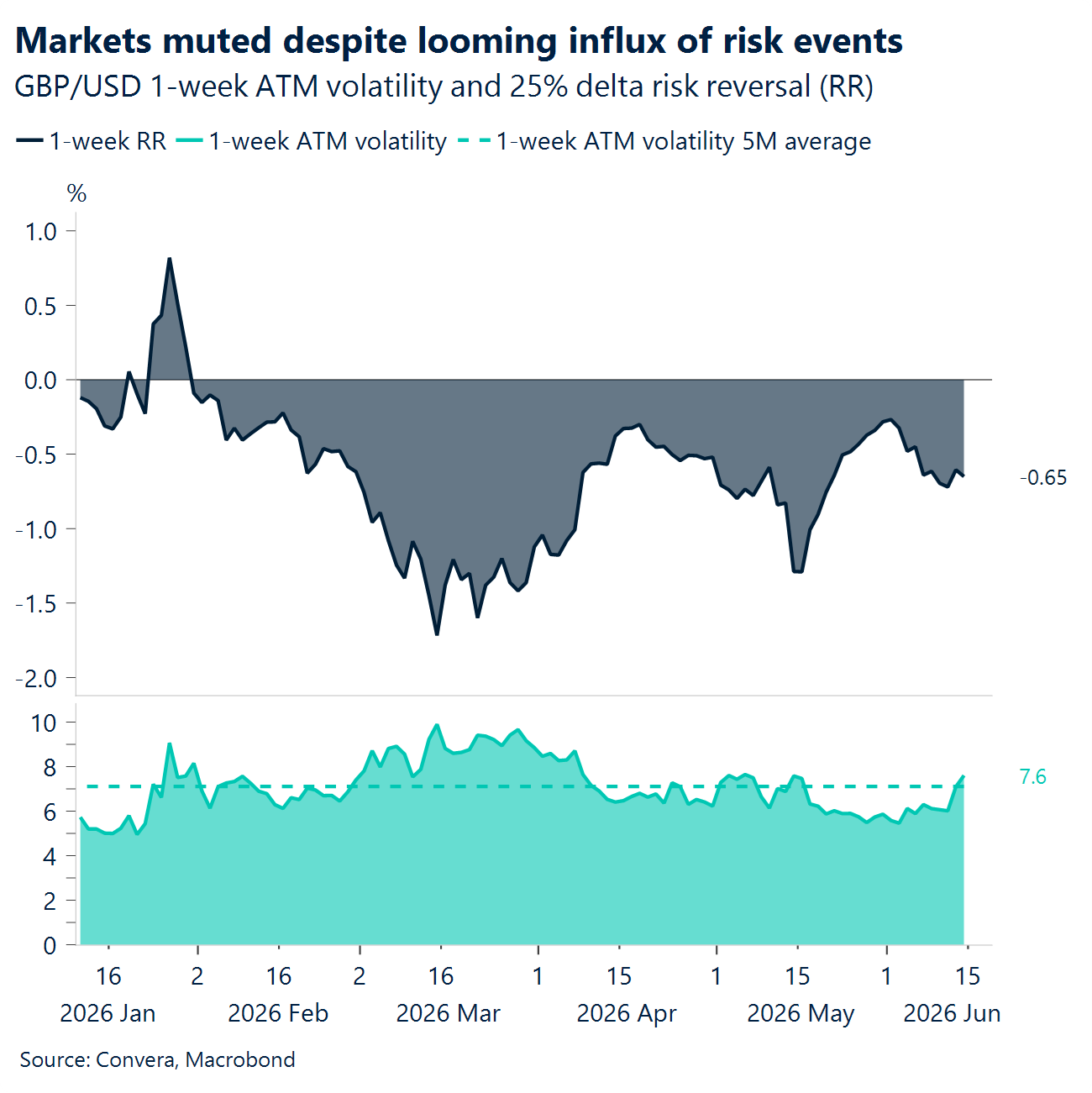

GBP Stalls at the gate. Sterling has been resilient this week, recovering from the 1.33 area against the USD as risk appetite stabilised, but it remains constrained below key resistance near the 200‑day moving average around 1.3420. While GBP/USD has edged higher, gains have been limited by a still-supportive USD backdrop driven by stronger US growth and real yield differentials. Against the EUR, GBP has held firm, again testing the 1.16 ceiling, supported by constructive momentum, carry appeal, and positioning dynamics, though a sustained breakout remains elusive. Importantly, sterling’s stability has been driven more by external factors than domestic strength. UK economic data has softened, while domestic political uncertainty is beginning to re-enter the equation. Looking ahead, a plethora of risk events loom – from the Fed and BoE meetings, to the Makerfield by-election. As a result, we see risks skewed mildly lower for sterling, even if global risk appetite stays firm, but surprisingly options markets aren’t signaling much volatility.

CHF Rates and referendum risk. Despite persistent geopolitical uncertainty in the Gulf, the franc has come under increased selling pressure. EUR/CHF has climbed back toward the 0.92 area, reinforcing the notion that CHF is currently more sensitive to rate differentials than safe‑haven flows. The move has been driven largely by the global sell-off at the front end of the curve, where Swiss rates remain anchored and lag external moves, allowing EUR short-end dynamics to dominate. The long-standing EUR/CHF downtrend from 2021 is now under pressure – an important inflection point for broader sentiment. At the same time, USD/CHF continues to act as a key expression of the ongoing unwind of dollar debasement trades. Adding to franc woes – the SNB has reiterated its increased willingness to intervene, with upcoming Q1 FX data likely to show a pickup in activity. Meanwhile, the June 14 population referendum introduces a new marginal risk, with potential implications for Switzerland’s growth model and EU relations, leaving CHF vulnerable.

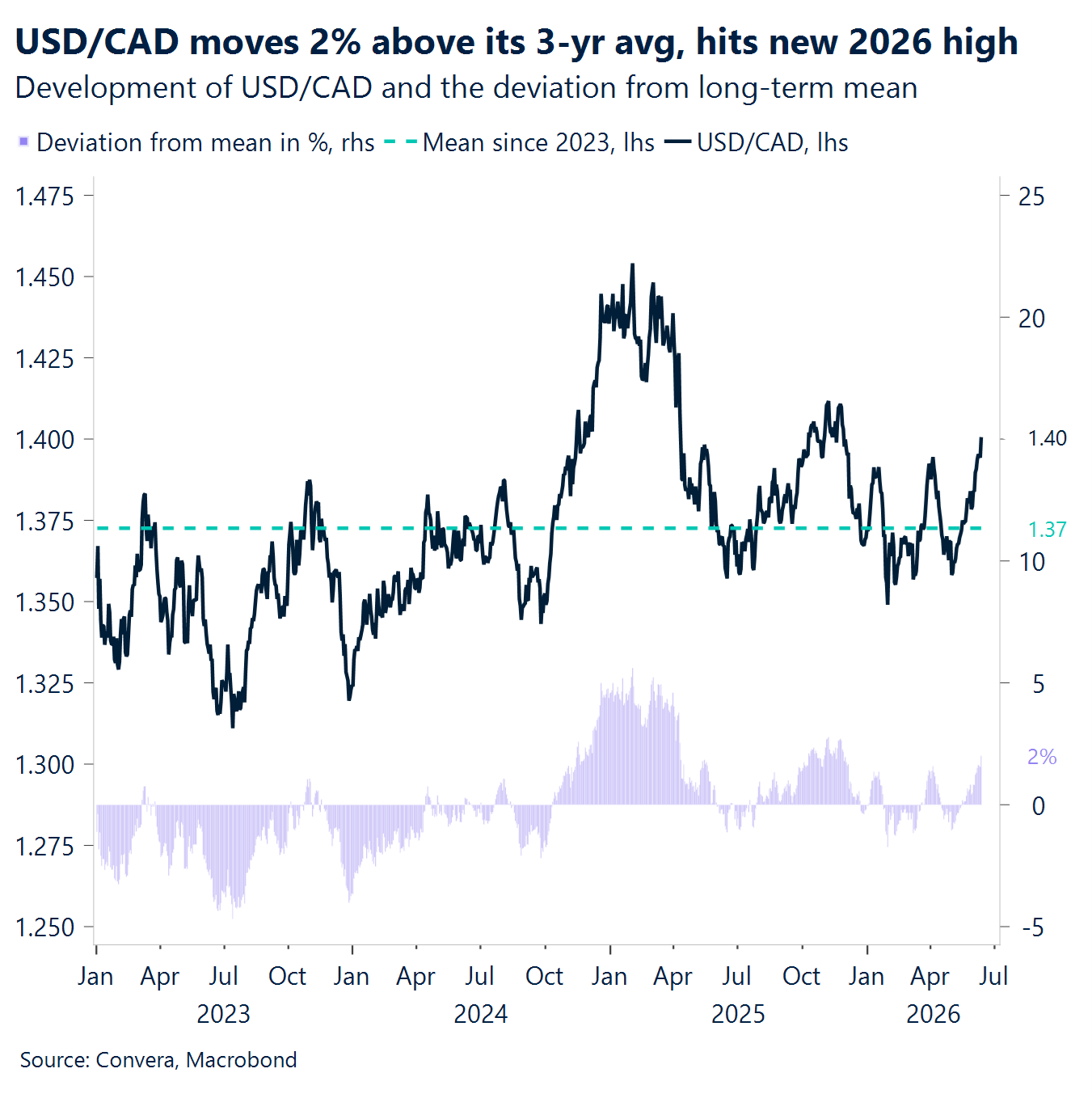

CAD 1.40 back in play. Over the last two weeks, the USD/CAD has priced a tougher mix for Canada. The Bank of Canada kept rates at 2.25% for a fifth straight meeting, but the message turned more hawkish and more uncertain than in April. The Bank now says policy could move either way: cuts if new US trade restrictions hit growth, or hikes if energy costs start feeding into persistent inflation. That leaves the BoC with a less comfortable reaction function, especially with the July 1 CUSMA review approaching and trade tensions still in play. On top of that, a firmer US dollar and renewed US-Iran rhetoric have added pressure, while speculative positioning turned more bearish on the Loonie, with net shorts widening to 94.1k contracts from 68.9k. US-CA short-term yield differential has also widened to the highest since June 2025. After spending most of the week trapped in the 1.3900–1.3950 range, USD/CAD broke higher and printed 1.4024, but reversed and trades around 1.398 after President Trump cancelled air strikes against Iran. The 1.402 is the strongest level in 2026. The pair now sits above the 20-day (1.3844), 50-day (1.3767), 100-day (1.3726), and 200-day (1.3817) moving averages, which confirms that upside momentum has broadened. The immediate hurdle is the 1.4025–1.4100 zone, where the March and November highs come back into view. On the downside, the first support sits at 1.3950, followed by 1.3900.

AUD Aussie dollar sags as the mood sours. A US–Iran deal reopening the Strait of Hormuz toll-free would cap oil prices and ease the energy-cost drag, but softer commodities also trim support for the Aussie. Australian households turned gloomier in June. Westpac’s confidence gauge fell 2.9% m/m to 80.6, one of the weakest prints in the half-century history of the survey, as budget strain, sticky living costs, rising loan repayments and energy bills all weighed. A separate survey showed business sentiment still fragile, edging up only slightly to -14 in May from a revised -23. The market is currently pricing in no rate hike at the upcoming RBA meeting. AUD/USD trades above its 100-day EMA at 0.7038. We watch the 21-day EMA at 0.7106 as the next ceiling to clear, followed closely by the 50-day EMA at 0.7108. A break above both would signal a firmer footing, while failure keeps the bias soft. We turn next to the RBA rate call and its accompanying statement.

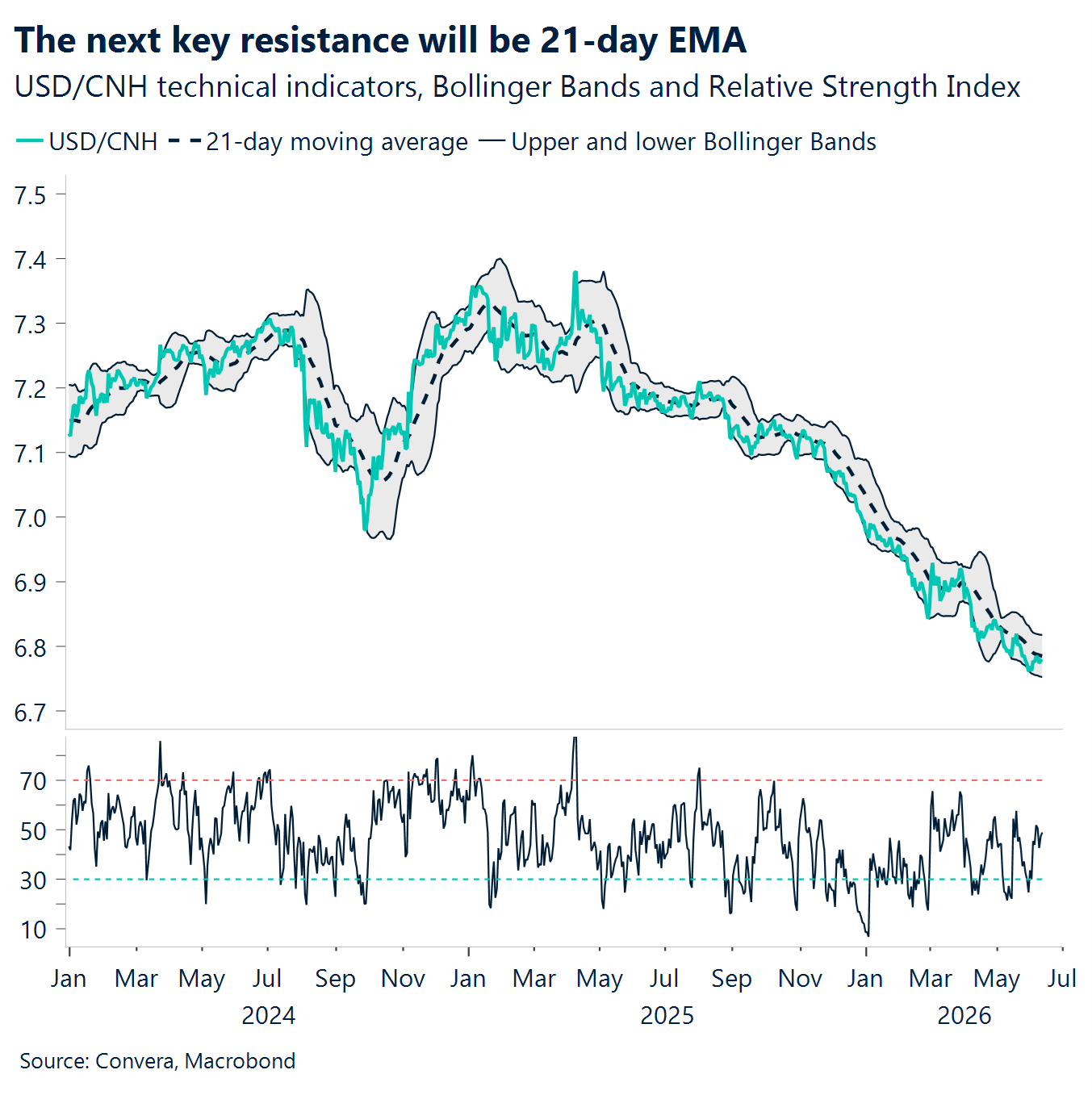

CNH Yuan steadies as prices stay tame. China’s May consumer prices held at 1.2% y/y, just below the 1.3% expected. Factory-gate prices matched forecasts at 3.9% y/y, building on the prior 2.8% and extending further into positive territory. We still expect Beijing to achieve its growth target, with consumer inflation drifting lower through the back half. USD/CNH trades roughly 0.1% above its recent floor of 6.7581 (2 June). The pair must clear the 21-day EMA at 6.7837 to build upward momentum. A move higher would expose the 50-day EMA at 6.8103, then the 100-day EMA at 6.8587, while the 6.7581 low caps the downside. We turn next to industrial output, the jobless rate, fixed-asset investment and the NBS briefing.

JPY Yen slides as growth cools. A US–Iran deal that calms oil would ease Japan’s energy bill and support the case for further rate hikes, lending the yen some backing against a softer dollar. Japan’s Q1 real GDP growth eased to an annualised 1.8%, revised down from 2.1%, as firms cut business investment by 0.7% q/q versus an initial 0.3% gain. Household spending and external demand held firm. Even at this slower pace, the economy still looks resilient, and we expect the BoJ to lift rates at the upcoming June meeting. The market has priced in a 97% probability of a hike at that meeting. USD/JPY has now pierced the pivotal 160.00 level, trading around 0.3% below its 30 April high of 160.72. The 21-day EMA near 159.62 and the 50-day EMA at 159.00 should provide support on dips, while 160.72 marks the level to clear for further upside. A close back below 160.00 would cool the move. We turn next to the BoJ rate decision, the trade balance and inflation data.

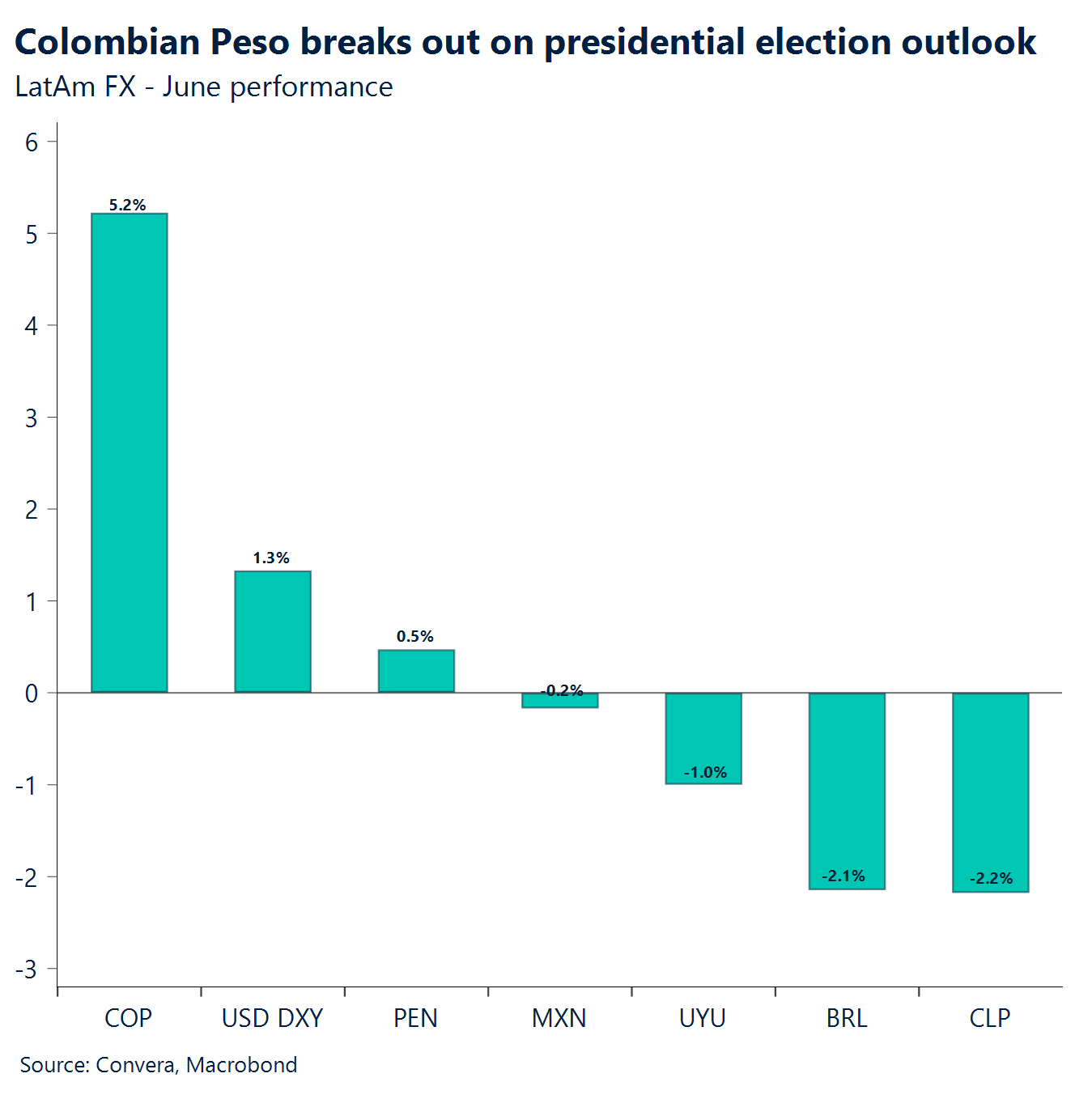

MXN Range still holds. The Mexican peso is no longer the standout performer in LatAm this month, but it is still one of the cleanest currencies in the region. While the Colombian peso has surged on election optimism, MXN has stayed broadly flat month to date, which says a lot about how differently the market is pricing regional risk. USD/MXN again pushed toward the 17.5 ceiling that has capped the pair since April, but the level held. That stability reflects a familiar mix: high carry, low volatility, and much less political noise than in Brazil, Colombia, or Peru. In short, the peso is not leading the region outright, but it is still behaving like the region’s lower-beta carry currency. The technical picture fits that story. USD/MXN is trading near 17.38, above the 20-day (17.35) and 50-day (17.37) averages, but still below the 100-day (17.43) and far below the 200-day (17.84). That leaves the pair in a short-term recovery, but not in a broader bullish trend. The first resistance is 17.43–17.45, and then the market goes straight back to the key 17.56 cap. On the downside, 17.35 is the first support, followed by 17.20. As long as USD/MXN stays below 17.5, the peso still holds up well, but a clean break would likely trigger a fast repricing given how cheap volatility still looks.

BRL Risk repriced . USD/BRL has moved back up toward 5.15, keeping the pair near its weakest level in two months as broad dollar strength continues to dominate. The latest leg higher has come renewed tension around the Strait of Hormuz which has lifted demand for safe havens, while firm US inflation and a still-tight labor market have kept the Fed’s path skewed hawkish. Brazil-specific risk has also started to matter more, with investors watching fresh polling that showed President Lula widening the lead over Senator Flávio Bolsonaro. That domestic layer has offset otherwise solid macro data, including 1.1% Q1 GDP growth, which beat expectations, and 4.39% April inflation, which keeps the policy backdrop uncomfortable. Markets now lean toward a pause in next week’s central bank meeting. The technical picture has turned firmer for USD/BRL, even if the broader trend is not fully reversed. While the real still ranks among the better-performing EM currencies this year, the near-term bias remains fragile as long as USD/BRL holds above the 5.1 support zone.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.