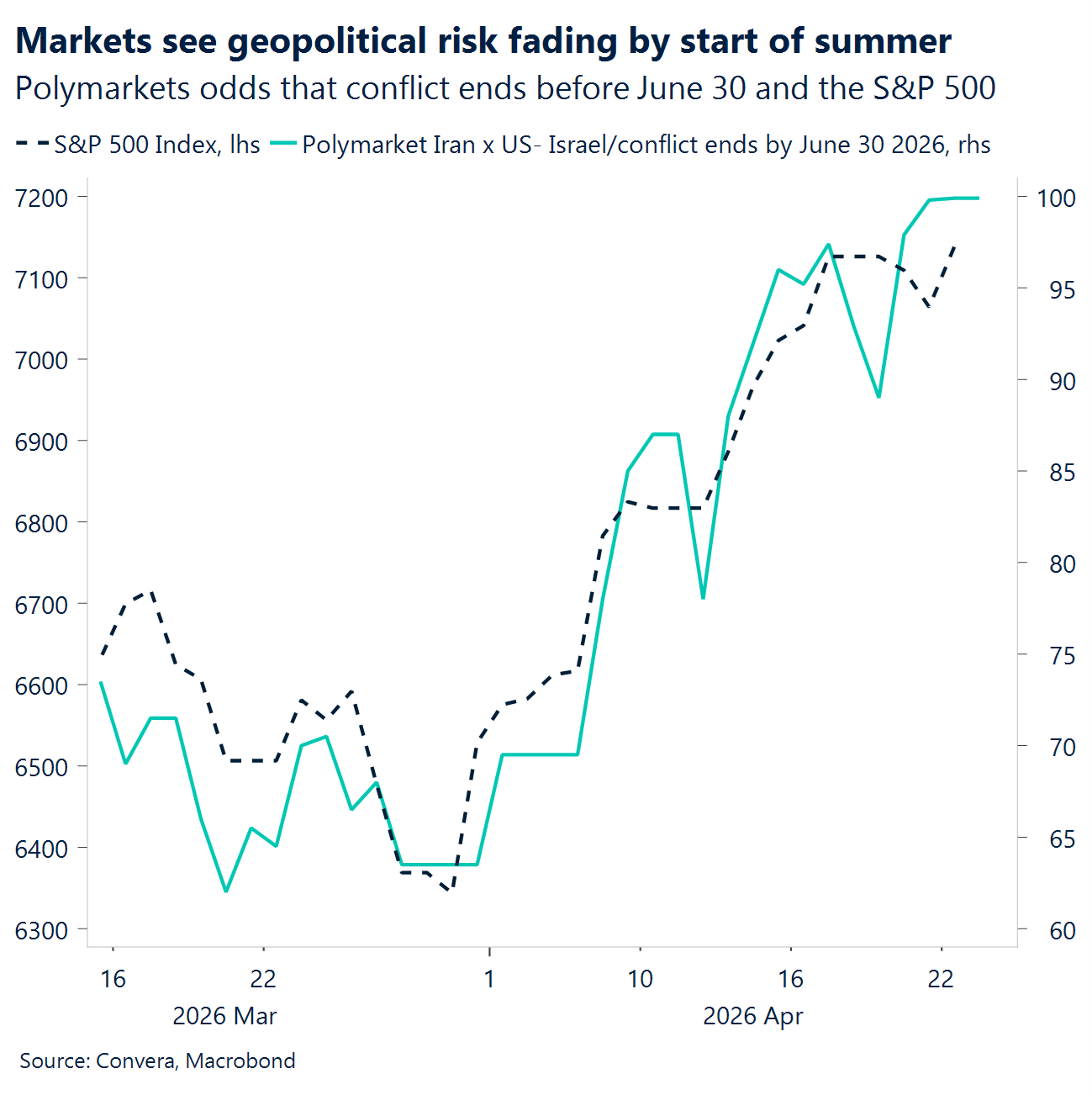

- Strait stuck. The US and Iran remain locked in a stalemate over the Strait of Hormuz, with both sides effectively blocking traffic with little sign of movement on the diplomatic front.

- Risk rally slows. With negotiations at an impasse, the record US equity rally lost momentum, while Brent crude oil pushed back above $100 as energy risks were repriced. Still, markets remain optimistic about the conflict ending by summer.

- Warsh walks the line. Kevin Warsh’s Senate hearing reassured investors on Fed independence without signalling a clear policy shift. His rejection of forward guidance and call for a “new framework” landed softly. Markets were unfazed.

- Calm before the headline. FX volatility has slid back toward late‑2025 lows as war-related tail risks are priced out, but the calm looks more like complacency. Current vol levels imply a durability of peace that is far from assured.

- Data dump digest. UK wage growth slowed to a four‑year low in February, while the unemployment rate ticked lower to 4.9%. PMIs outperformed the Eurozone yet input price pressures surged to their highest since late 2022.

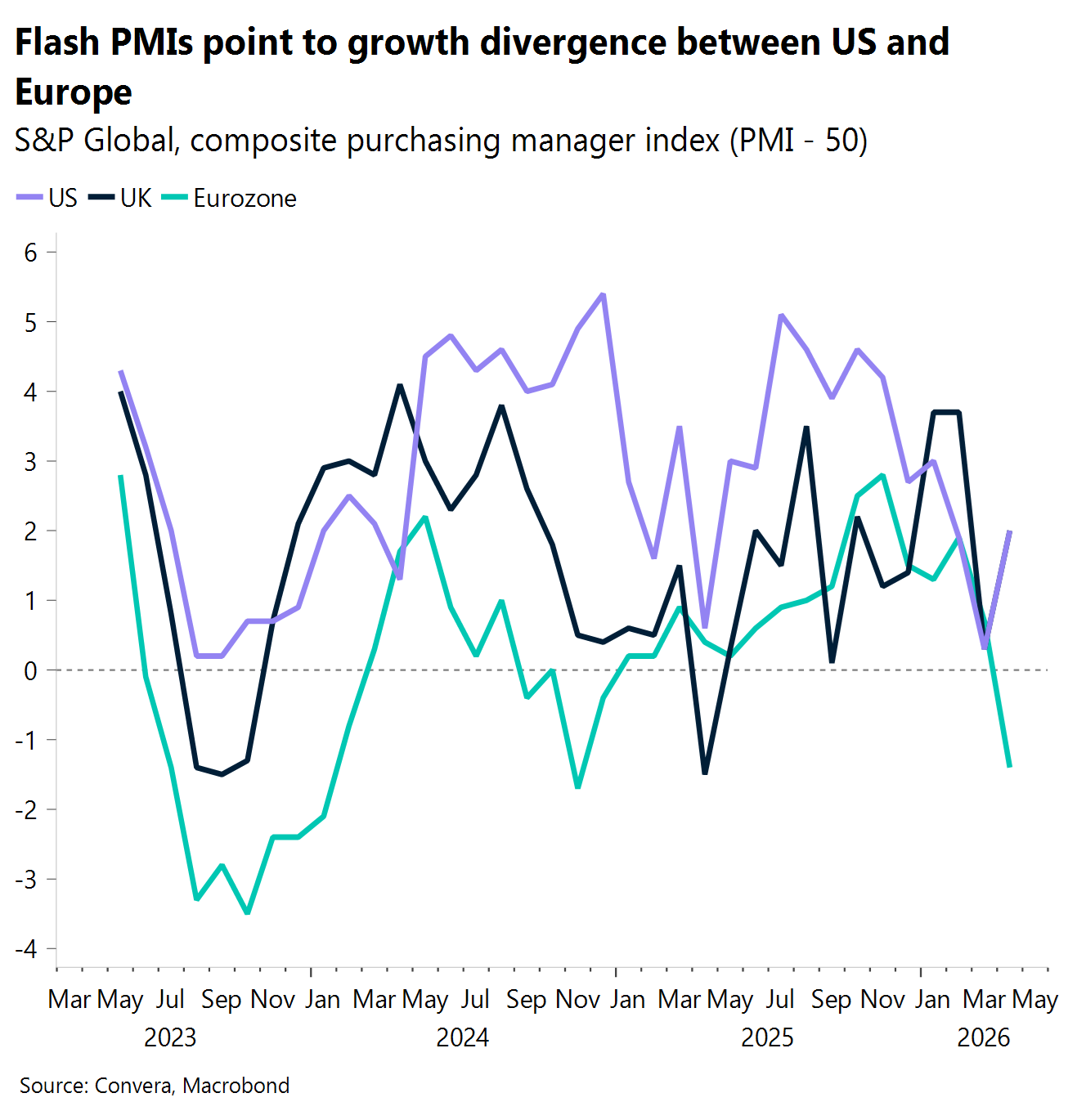

- Europe hits a wall. Eurozone PMIs disappointed sharply, led by steep contractions in German and French services. The data point to mounting growth damage as the Iran conflict hits confidence and costs.

- Central banks back in focus. As geopolitical risk oscillates, attention is turning back to monetary policy, with a dense run of central bank decisions looming before month‑end.

Global Macro

Global growth momentum fragments

PMI Divergence. Flash PMIs sharpened the split, US composite rebounded to 52.0 while the Eurozone composite slid to 48.6, turning “divergence” from a theme into a print. European markets tied that directly to the war/energy channel, with stocks softer as oil pushed higher and PMI weakness feeds the growth scare, even as US risk assets remained comparatively supported.

China Steady. China left benchmark lending rates unchanged again, keeping the 1‑year LPR at 3.00% and the 5‑year LPR at 3.50%, signaling policy patience rather than fresh cyclical support. The market backdrop made that “no new impulse” feel louder, as crude re‑tested $100+ while Asia largely tracked the global risk tape.

UK CPI Reheats. UK inflation accelerated to 3.3% y/y in March (from 3.0%), keeping the UK squarely in the “energy‑linked inflation risk” bucket this week. Higher energy costs and war uncertainty lead market narrative and the pressure point for households and risk sentiment, which makes the CPI re‑acceleration feel more persistent than “one‑off.”

Canada CPI Pops. Canada’s March CPI re‑accelerated to 2.4% y/y with a 0.9% m/m jump, keeping the week’s inflation story tightly linked to the energy shock rather than a clean core re‑run. The crude strength is the “tax” markets can’t ignore, oil stayed elevated as Hormuz frictions persisted, keeping inflation fears in play even when equities tried to stay upbeat.

US Demand Holds. US retail sales surged 1.7% m/m in March and the GDP‑relevant control group printed +0.7% m/m, pointing to underlying spending resilience beyond the gasoline lift. This “good growth, awkward inflation” narrative didn’t matter for stocks, which were buoyed by ceasefire‑relief/earnings momentum, but rising crude and firmer yields are still near‑term headwinds.

Week ahead

Caught between war talk and rate talk

Geopolitics will continue to dominate as a closed Strait of Hormuz keeps Brent above $100, with markets watching US–Iran talks for a reopening signal.

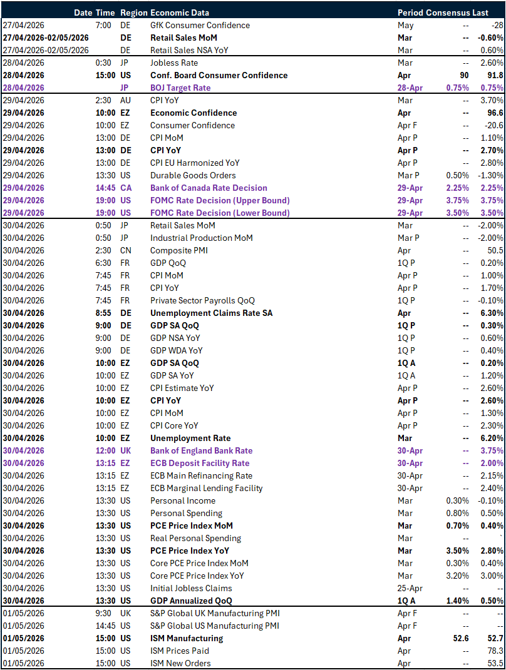

Central Banks: cautious, not committed. The week is packed with central bank policy meetings. We expect all banks to strike a cautious, hawkish‑leaning tone that nonetheless falls short of signalling a firm tightening bias. A preference for full optionality remains the baseline. With economies facing asymmetric risks across activity and labour‑market conditions, policymakers are likely to stress the need for incoming data to assess how the two‑pronged risk profile – high prices versus weakening activity – ultimately evolves.

Macro reality check. A heavy slate of hard macro data is due this week, particularly in the eurozone, including preliminary Q1 GDP growth, inflation, and unemployment figures for both Germany and the wider region. The macro backdrop had already been disappointing in 2026, with the conflict expected to exacerbate the weakness. However, given lagging effects and the low frequency of some indicators (notably GDP), we are unlikely to see meaningful conflict‑related distortions in the data this early. Monitoring remains crucial to establish a clean baseline as conflict effects propagate through the economy in the months ahead.

Inflation in the spotlight. In the US, attention turns to the Private Consumption Expenditures (PCE) price index due next week – the Fed’s preferred inflation gauge. On headline prices, conflict‑related pass‑through is expected to be more pronounced, with consensus pointing to a jump to 3.5% year‑on‑year in March from 2.8% in February. The core measure, which strips out volatile food and energy prices, is expected to remain more subdued.

FX views

The dollar’s oil backed rebound

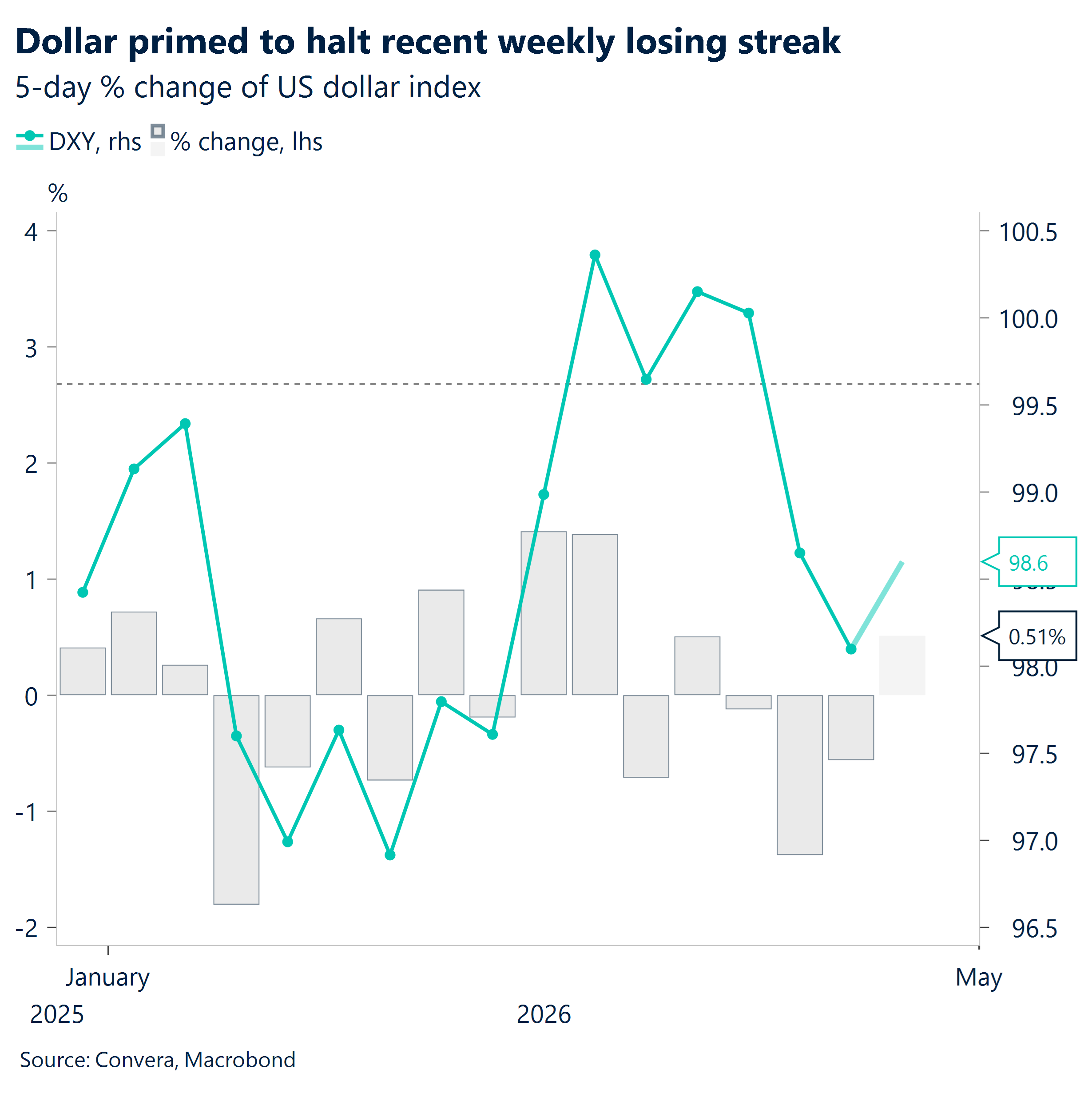

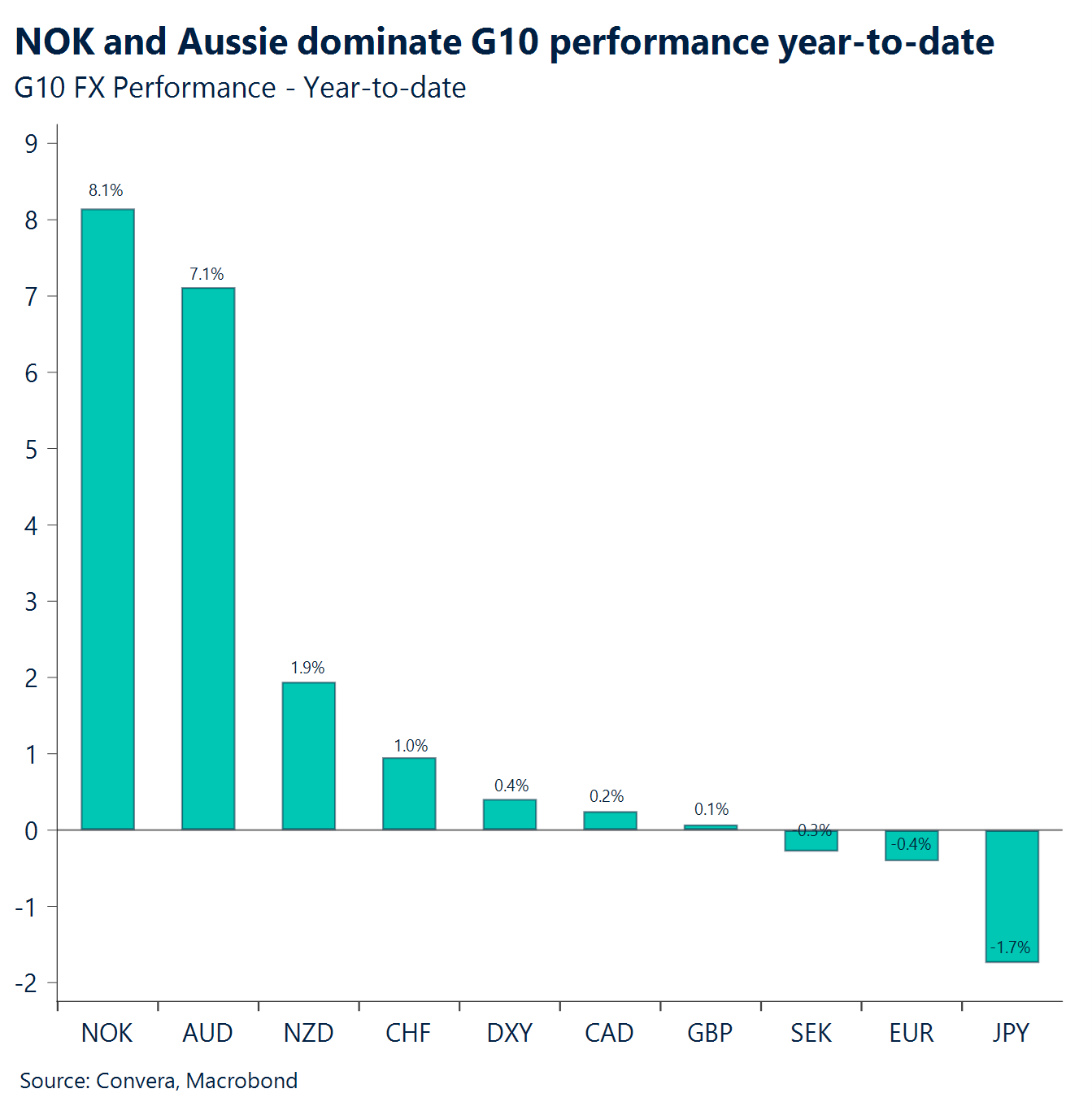

USD. Oil tensions fuel dollar bounce. The US dollar’s key bullish driver – rising oil prices – remains in place. While a resumption of March’s military pressure appears unlikely, the Strait of Hormuz remains shut, deadlocked by both sides. The stalemate has helped DXY recover around 0.8% this week, with the shift away from full de‑escalation likely to keep the dollar bid as oil prices stay elevated. In this context, a move back above 99 – below which the index only traded at peak de‑escalation optimism – appears justified. Beyond geopolitics, the dollar largely shrugged off Kevin Warsh’s Senate testimony following Trump’s Fed chair nomination. Still, concerns that a more politically accommodating chair could favour lower rates may build over time. As such, downside risks for the dollar remain should geopolitical tensions ease and unwind the oil‑linked support currently underpinning the dollar.

EUR. Euro rolls over as risk calm weakens. EUR/USD briefly built sufficient momentum to complete a reversal of March’s bearish trend, hovering just below the 1.18 handle (end‑February levels). The move subsequently stalled after a less clear‑cut de‑escalation development re‑introduced a milder – but still firm – bearish directional impulse into the pair, which is now trading around 0.7% lower heading into the end of the week. Iran’s and the US’s apparent intentions not to resume strikes on the scale seen in March have, for now, contained a sharper deterioration in risk sentiment, despite the Strait remaining blocked and energy prices elevated. Since the conflict began, EUR/USD has tracked swings in risk sentiment more aggressively than oil, reinforcing the view that a more gradual move lower could give way to an accelerated decline should the Strait not be reopened in the near term. We therefore see a test of the 1.16 mark as a plausible downside target in the coming days, with scope for acceleration if posturing on either side intensifies further.

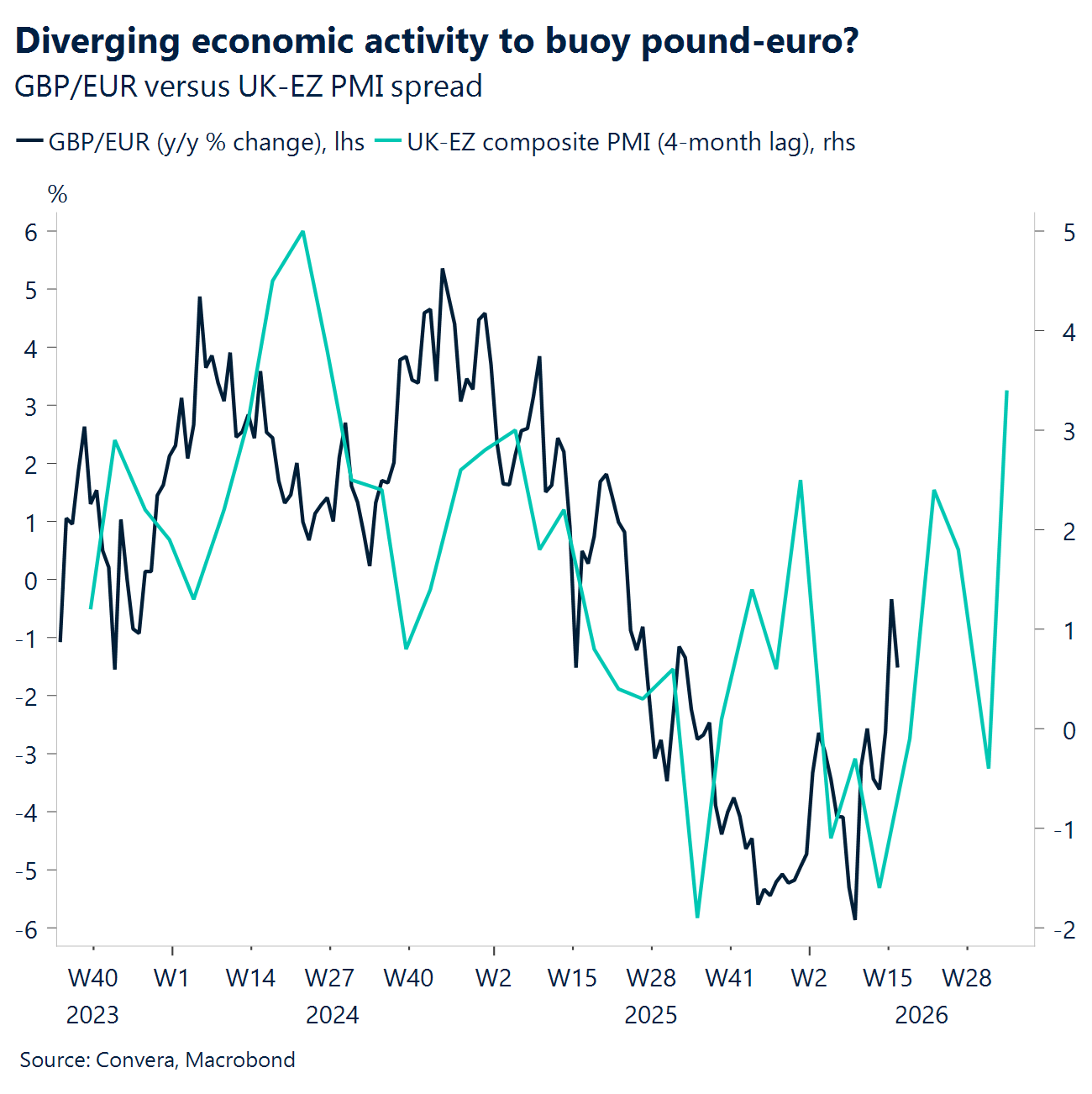

GBP Diverging trends. Sterling has traded on a two‑track dynamic over the past week, with geopolitics dominating GBP/USD tactically, while domestic and relative fundamentals have asserted themselves more clearly in GBP/EUR. Early in the period, the pound was whipsawed by ceasefire reversals, leaving GBP/USD tightly tethered to the de‑escalation trade and capped near 1.36, even as GBP/EUR proved more insulated, holding a narrow 1.145–1.15 range. As the week progressed, risk momentum faded, with equities losing traction and oil rebounding sharply. That shift naturally weighed on the energy‑sensitive, high‑beta pound, driving GBP/USD back toward sub‑1.35, and losing out to commodity FX such as CAD and NOK. Even so, the broader April uptrend in GBP/USD remains intact, with pullbacks thus far corrective rather than trend‑breaking. Tactically, 1.3461 and 1.3415 are key downside levels to watch in GBP/USD, with 1.36 still a meaningful upside barrier. As for GBP/EUR, it pushed above 1.15, reflecting relative UK resilience versus a weakening euro growth backdrop. Political risk has eased near‑term, offering some relief, but remains a latent downside catalyst ahead of May elections.

CHF Testing SNB’s resolve. The Swiss franc continues to trade near cycle‑high levels, but recent price action reinforces the idea that CHF is acting as a constrained stabiliser rather than the market’s primary haven. Despite being up around 1–1.5% YTD versus the euro and dollar, CHF failed to attract strong marginal inflows during the Iran conflict, with the USD instead capturing most defensive demand. This dynamic is increasingly underpinned by valuation and policy constraints. Switzerland’s real effective exchange rate has climbed to its highest level in almost 15 years, now well above past peaks that historically prompted SNB unease over competitiveness. While geopolitics may have increased tolerance for currency strength at the margin, the SNB has clearly hardened its tone, explicitly stating that its willingness to intervene has increased. Actual intervention remains limited, but rhetoric alone has been sufficient to cap CHF upside. Absent physical action, low inflation and haven characteristics should still enable gradual gains, leaving the franc probing the upper bounds of SNB tolerance rather than breaking decisively higher.

CAD Flat year-to-date. The USD/CAD has once again bounced at 1.37, with the pair’s near-term outlook remaining tightly tethered to Middle East developments, fluctuating oil prices, and broader global risk sentiment. While recent domestic inflation data did little to alter policy expectations, the currency pair is likely to stay rangebound between 1.365 and 1.375 as markets navigate geopolitical headline swings and wait for tangible diplomatic progress. Adding to this domestic complexity is the looming shadow of CUSMA trade negotiations; the lack of clear progress in preliminary treaty discussions and the potential for friction surrounding the upcoming mid-year review serve as an additional layer of overhead for the Canadian Dollar. Looking ahead to next week, focus will shift to a major central bank double-header on Wednesday, where both the Bank of Canada and the Federal Reserve are widely expected to hold rates steady, followed by a close watch on Canada’s advance GDP data for February on Thursday.

AUD Australia stabilises, Aussie hesitates. Australia’s S&P Global April flash composite PMI rose to 50.1 from 46.6 in March, returning to marginal expansion. Services rebounded sharply to 50.3 from 46.3, while manufacturing edged higher to 51.0 from 49.8. However, the improvement remained uneven as manufacturing output stayed in contraction at 48.2, down from 49.4, limiting the overall recovery. In FX, AUD/USD fell 0.8% in the week of April 20 as a stronger US Dollar weighed on risk‑sensitive currencies. The pair is now trading about 1.4% below its recent high near 0.7222 seen on 17 April, though it remains near the top of its six‑month trading range. AUD/USD is holding just above the 21‑day EMA at 0.7087, which offers near‑term support, while a further dip would bring the 50‑day EMA near 0.7029 into view. On the upside, moves continue to struggle near 0.7200, suggesting the pair is pausing after recent gains rather than starting a fresh move. Market participants will watch upcoming CPI, PPI and manufacturing PMI releases.

CNH Xi speaks, Yuan loses ground. Chinese President Xi Jinping called for an immediate ceasefire in the Middle East and urged the conflict to be resolved through political and diplomatic channels following talks with Saudi Crown Prince Mohammed bin Salman. Xi stressed that the Strait of Hormuz should remain open to normal shipping, framing this as a shared interest for the region and the global economy. In FX, USD/CNH traded near a two‑week high in Asian hours as the pair extended its rebound. USD/CNH has risen roughly 0.5% from its 14 April low of 6.8059, reflecting firmer short‑term momentum. The next upside test sits at the 21‑day EMA near 6.8448, while a sustained break above that level would bring the 50‑day EMA around 6.8756 into view. Markets will focus on upcoming Chinese industrial profit data, official manufacturing and non‑manufacturing PMIs, the RatingDog Manufacturing PMI and the Chinese Composite PMI

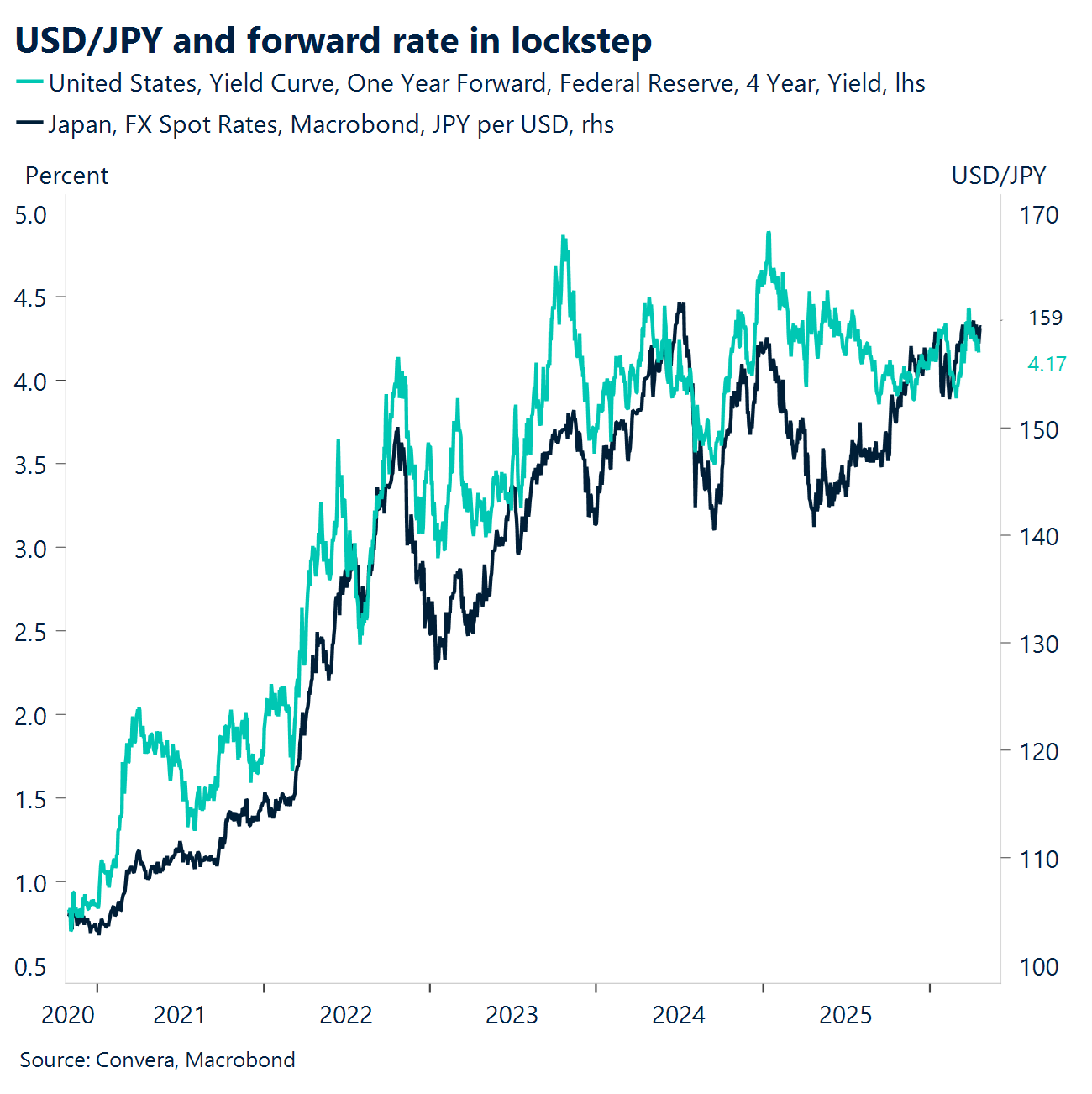

JPY Yen hovers near 160.00. Japan’s S&P Global flash April composite PMI eased to 52.4 from 53.0 in March, but stayed above the 50 expansion threshold for a thirteenth straight month. Manufacturing drove the strength, jumping to 54.9 from 51.6, the strongest reading since January 2022. In contrast, services slowed to 51.2 from 53.4, marking the weakest pace of growth in nearly a year. In FX, USD/JPY gained 0.6% in the week of April 20, as broader US Dollar strength persisted amid geopolitical tensions. The pair is now about 0.4% below its late‑March high near 160.46 and is hovering close to the 160.00 level. Initial support sits near the 21‑day EMA around 159.15, with a deeper pullback pointing toward the 50‑day EMA near 158.36. Despite the recent dip, the broader upward trend remains intact, keeping the door open for another test of 160.00 and potentially 162.00 if upward momentum returns. Market participants will watch the BoJ rate decision, the Monetary Policy Statement, industrial production, retail sales, manufacturing PMI data and upcoming CPI releases.

MXN Underperforming peers. The USD/MXN is consolidating in the 17.3 to 17.5 range, as a firmer Dollar, propped up by geopolitical friction and stalled diplomatic efforts, keeps the peso on the back foot. . Domestic data has provided no relief; February Retail Sales significantly underperformed expectations, printing at 3.1% YoY against a 4.5% forecast, signaling a sharp cooling in consumer activity. Furthermore, today’s bi-weekly inflation data showed Core CPI stuck at 4.27%, a figure that came in higher than the 4.26% expected, complicating the outlook for monetary policy as Banxico balances a stalling economy against sticky core prices. This combination of weak growth indicators and stubborn inflation has seen the peso underperform its regional peers, the COP and BRL, in the LatAm space. While markets appear “immune” to the latest round of USMCA tariff rhetoric, the currency remains highly sensitive to the macro backdrop ahead of a pivotal week featuring the Fed’s Wednesday meeting and Mexico’s Q1 GDP release on Thursday, which will serve as the next major litmus test for the peso’s resilience.

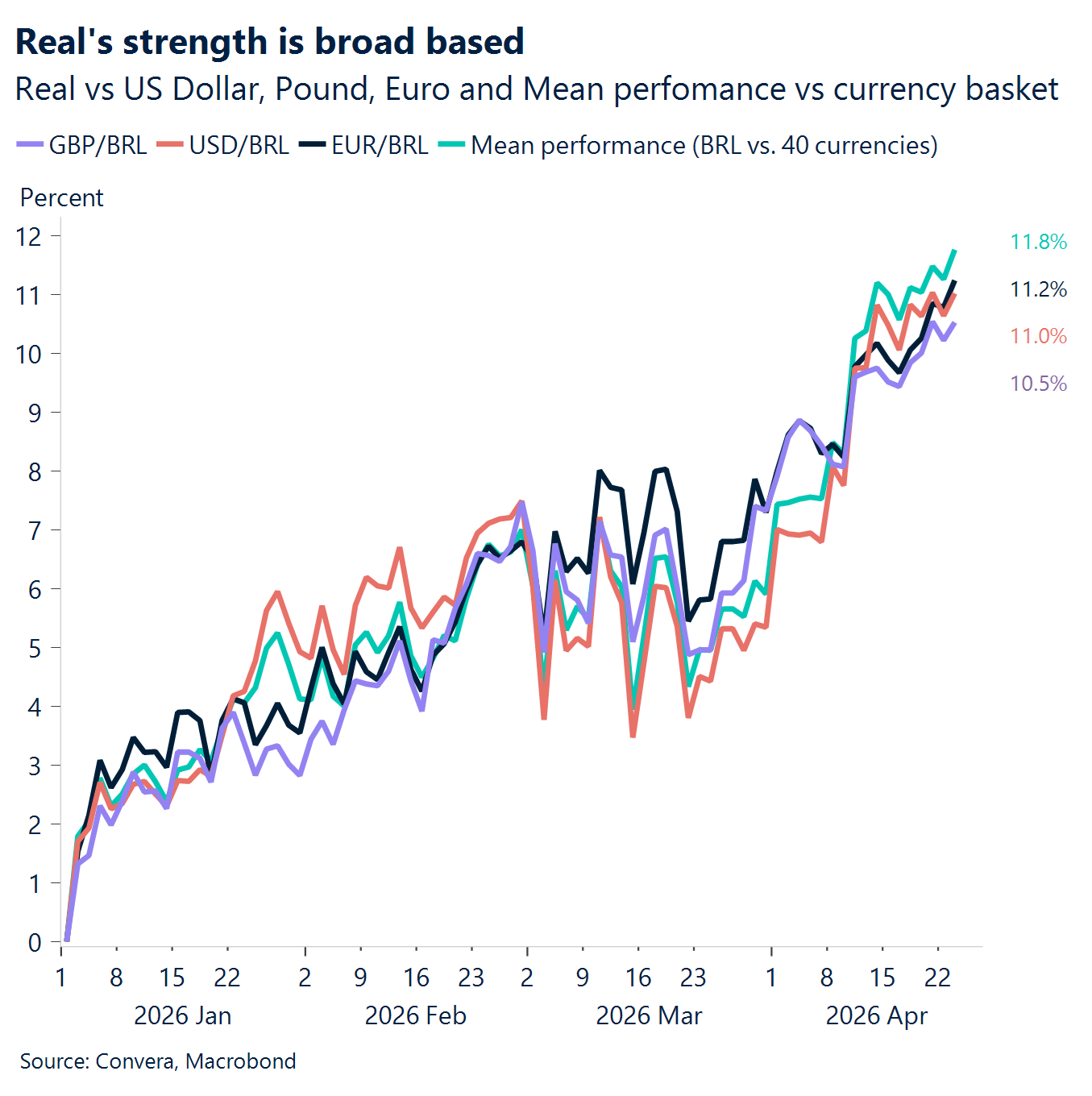

BRL Broad based strength. As market sentiment recovered this week, the Brazilian real has reclaimed its status as a carry trade leader, with the USD/BRL recently touching 4.95, its strongest level since March 2024. This resurgence is fueled by a sharp decline in implied volatility and a surge in global oil prices , a combination that has pushed the real’s carry-to-vol ratio above that of the Colombian peso. With the Central Bank of Brazil (BCB) effectively shelving its rate-cut agenda to counter inflationary energy risks, the currency is finding strong support from foreign inflows into fixed-income assets, looking to consolidate its recent gains around the $5.00 mark. Investors are now bracing for a high-impact week that will test this momentum, starting with Tuesday’s inflation print and followed by Thursday’s labor market data, all centered around Wednesday’s BCB decision where the bank is expected to hold the Selic rate steady at 14.75%.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.