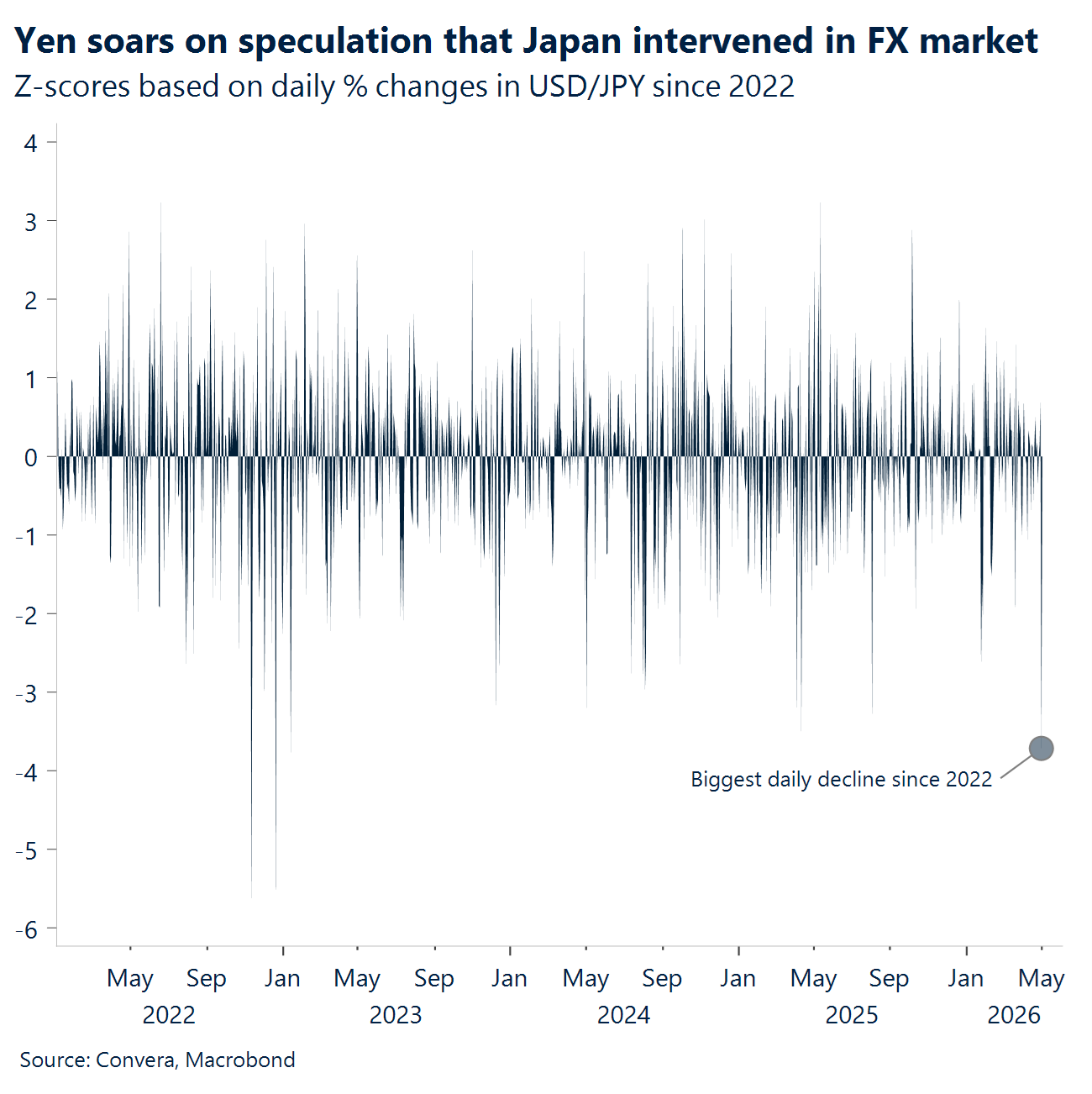

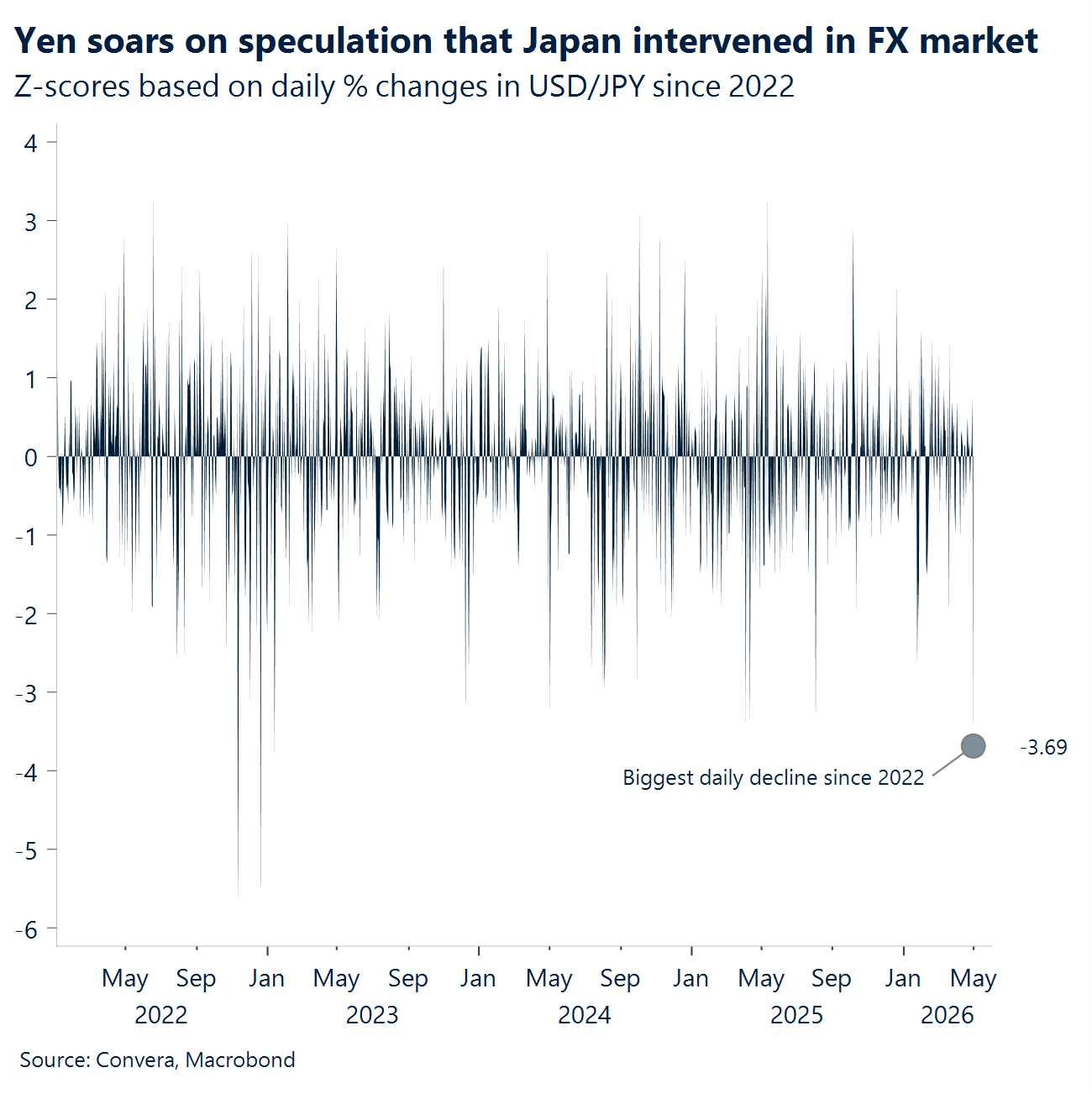

- Yen crashes the party. Markets have had more than enough to chew on this year already, and this week added to it with a yen surge stealing the show. Suspected Japanese intervention after USD/JPY traded up to 160.725 yanked the pair sharply lower, destabilizing the dollar more broadly.

- Peace without piece. US-Iran talks remain stuck, the Strait of Hormuz is still effectively impaired, and the market is still carrying a chunky geopolitical risk premium in the way of oil prices reaching their highest since 2022 this week.

- Abu Dhabi unplugged. The UAE’s decision to leave OPEC added a second oil twist: near-term scarcity from Hormuz, but longer-term supply flexibility from a major producer no longer tied to cartel quotas.

- Equities barely blinked. The S&P 500 rose 10.4% in April while the Nasdaq jumped 15.3% – best months since 2020 – with fresh record highs underpinned by sturdy earnings and the market’s still-insatiable appetite for AI capex.

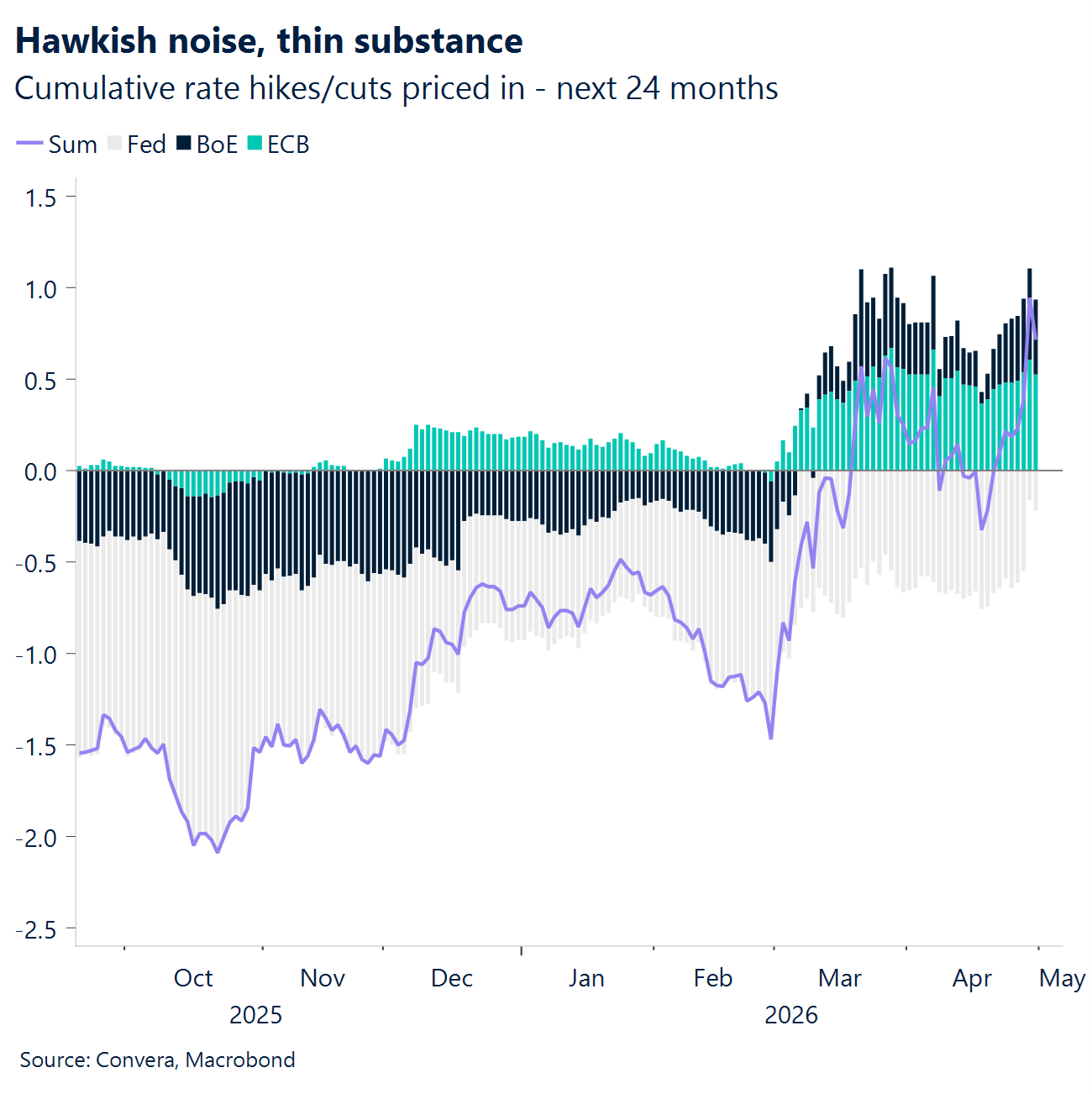

- Hold me hawkish. It was a week of central-bank non-moves that still felt meaningfully hawkish: the Fed, ECB, BoE and BoJ all held rates, but the message across the board was that higher energy prices are muddying the inflation outlook and pulling the next move closer to a hike than a cut.

- Powell’s last dance. Powell’s final meeting as Fed chair ended with an 8-4 split, the most divided Fed decision since 1992, and a distinctly theatrical sign-off after he said he intends to remain on the Board as a governor while the Fed renovation saga plays out.

Global Macro

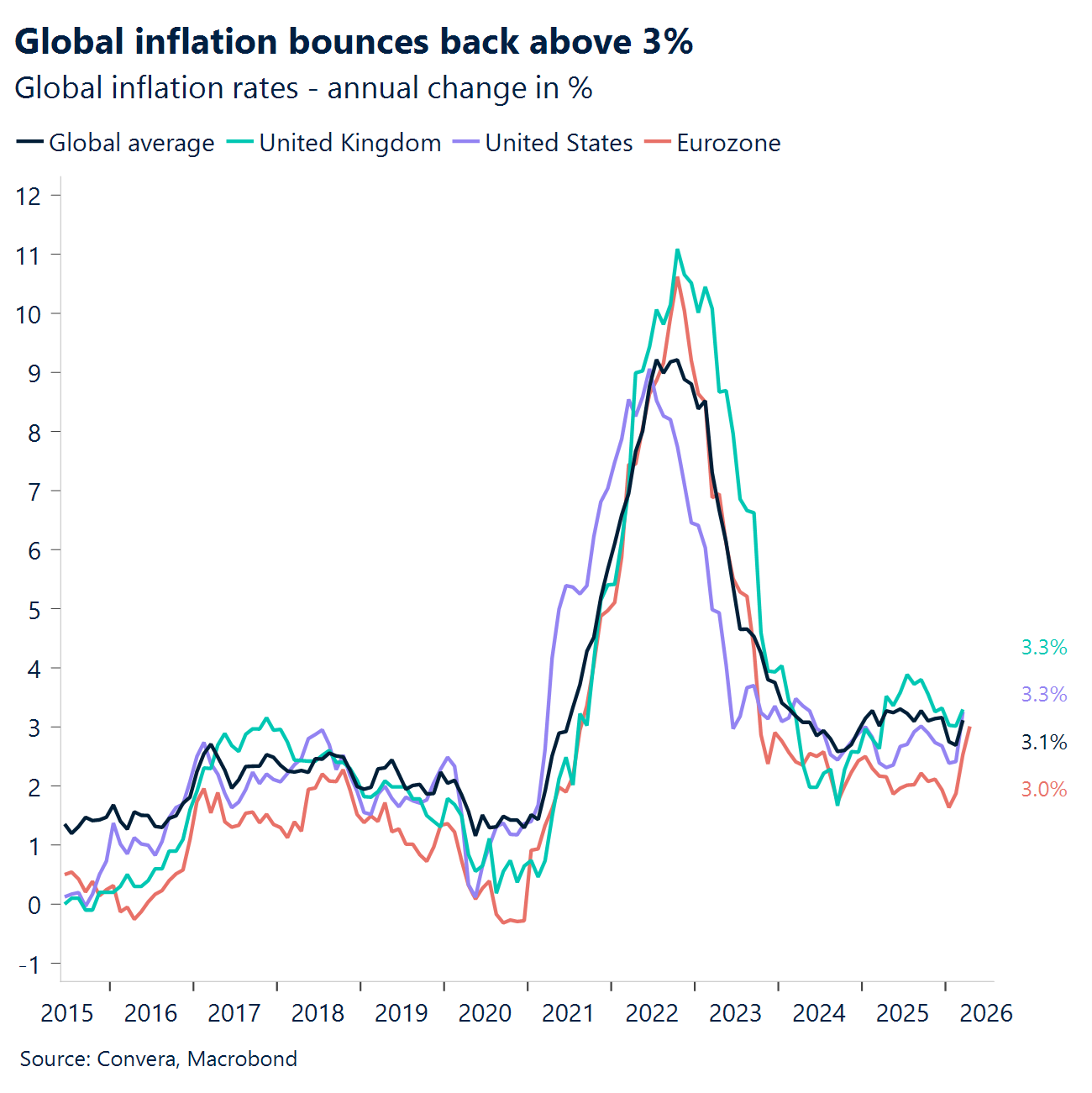

A hold wave as global inflation reaccelerates

Hold wave. The Fed held the funds target range at 3.50–3.75% (as expected), but the 8–4 split (and debate over keeping an “easing bias”) was the real headline, underscoring a more contested policy path. BoC held at 2.25% (expected), leaning heavily on geopolitical/energy uncertainty and two‑sided risks. In Europe, ECB held the deposit rate at 2.00% and BoE held Bank Rate at 3.75% (both expected), while the BoJ held at 0.75% with a notably hawkish internal split.

US repricing. Q1 GDP (advance) printed +2.0% SAAR vs +2.2% expected, a rebound from Q4’s +0.5%, but still a mild downside surprise on the headline. March PCE landed in line on the key inflation marks (headline +0.7% m/m, +3.5% y/y; core +0.3% m/m, +3.2% y/y), keeping the inflation conversation “sticky” even without a beat. The demand details were firmer: personal income +0.6% vs +0.3% expected and spending +0.9% vs +0.9% expected, while initial jobless claims fell to 189k vs 212k expected, reinforcing the “growth still grinding forward” narrative despite higher inflation prints.

Euro squeeze. The euro area flashed GDP +0.1% q/q vs +0.2% expected (still positive, but softer momentum), while the labor backdrop stayed stable with unemployment at 6.2% (in line). The bigger market impulse was inflation: April HICP flash +3.0% y/y vs 2.9% expected (up from 2.6%), driven by energy inflation surging to 10.9%. That mix (soft growth + energy‑led inflation) boxed the ECB into “wait‑and‑see”, not because the trend disinflation story is dead, but because the near‑term shock raises upside inflation risk while growth is already fragile.

China. China’s composite PMI held just above the 50 threshold, pointing to stabilization rather than re‑acceleration. The data suggested policy support is preventing further deterioration, but private‑sector momentum remains fragile. Markets continued to treat China as a drag reducer, not a growth engine.

Week ahead

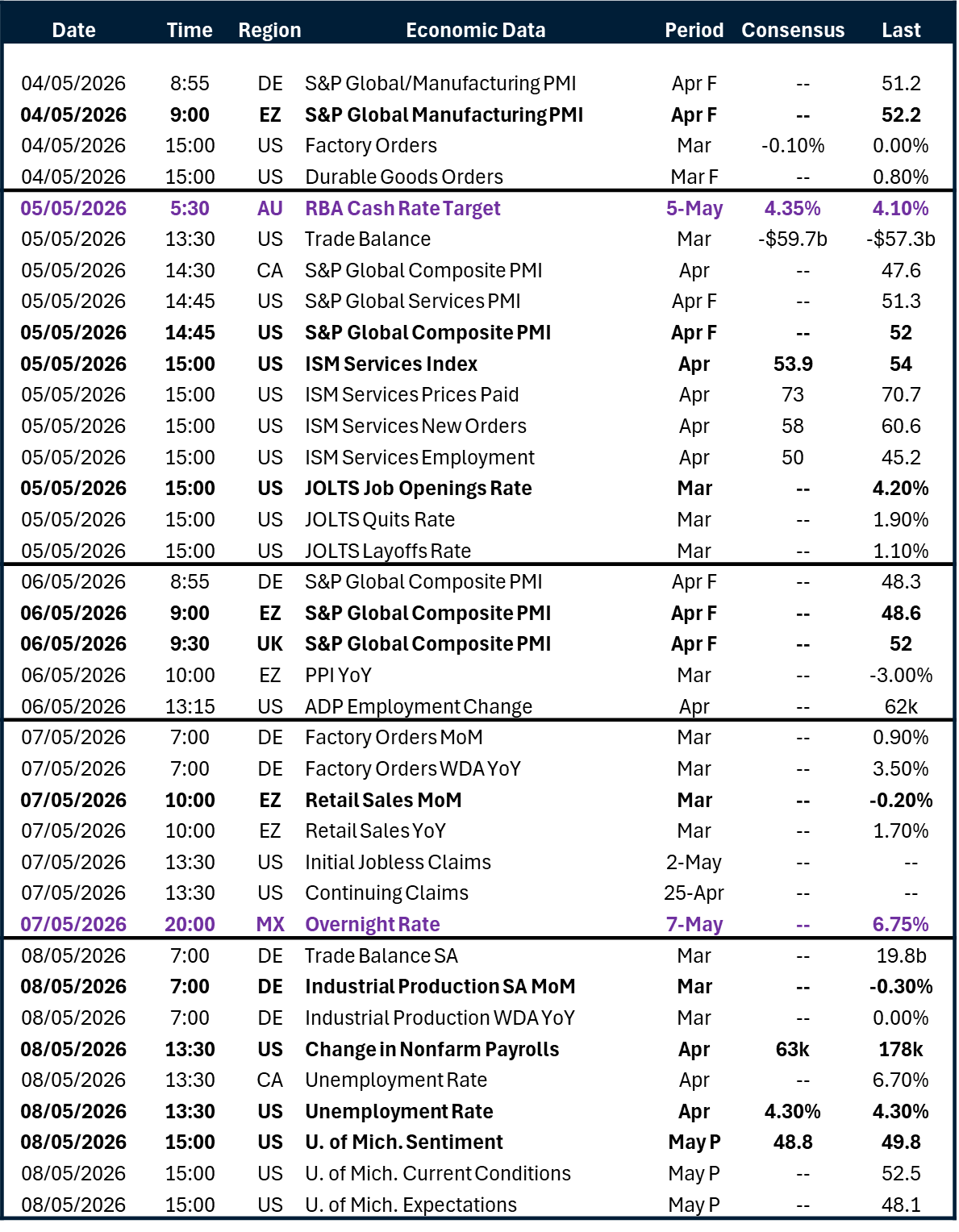

US jobs in focus

- The US economy will dominate the narrative over the upcoming week with a focus on the employment market. These numbers will be in particular focus after US weekly unemployment claims fell to the lowest level since 1969. On Tuesday, we have JOLTS (job openings and labor turnover), ADP on Wednesday and the all-important non-farm payrolls on Friday. For NFPs, the market is looking for 60k new jobs (after 178k in the previous month) with the unemployment rate forecast to remain steady at 4.3%.

- There’s less activity in Europe and the UK. In Europe, we have final manufacturing PMIs on Monday, final services PMIs on Wednesday and retail sales on Thursday. The UK sees construction PMI on Thursday and a key speech from Bank of England governor Andrew Bailey.

- In Canada, Bank of Canada governor Tiff Macklem speaks to the House of Commons on Monday while monthly labor market data is due on Friday.

- The Reserve Bank of Australia decision will also be closely watched. Most recently, headline annual inflation came in slightly below expectations at 4.6 percent, compared with 4.8 percent expected. The closely watched trimmed mean inflation measure, which strips out volatile items, was unchanged at 3.3 percent, broadly in line with forecasts. As a result, market pricing for an interest rate hike at Tuesday’s Reserve Bank of Australia meeting edged lower. The implied probability of a hike fell from around 80 percent on to roughly 74 percent after the data.

FX views

BoJ rocks markets

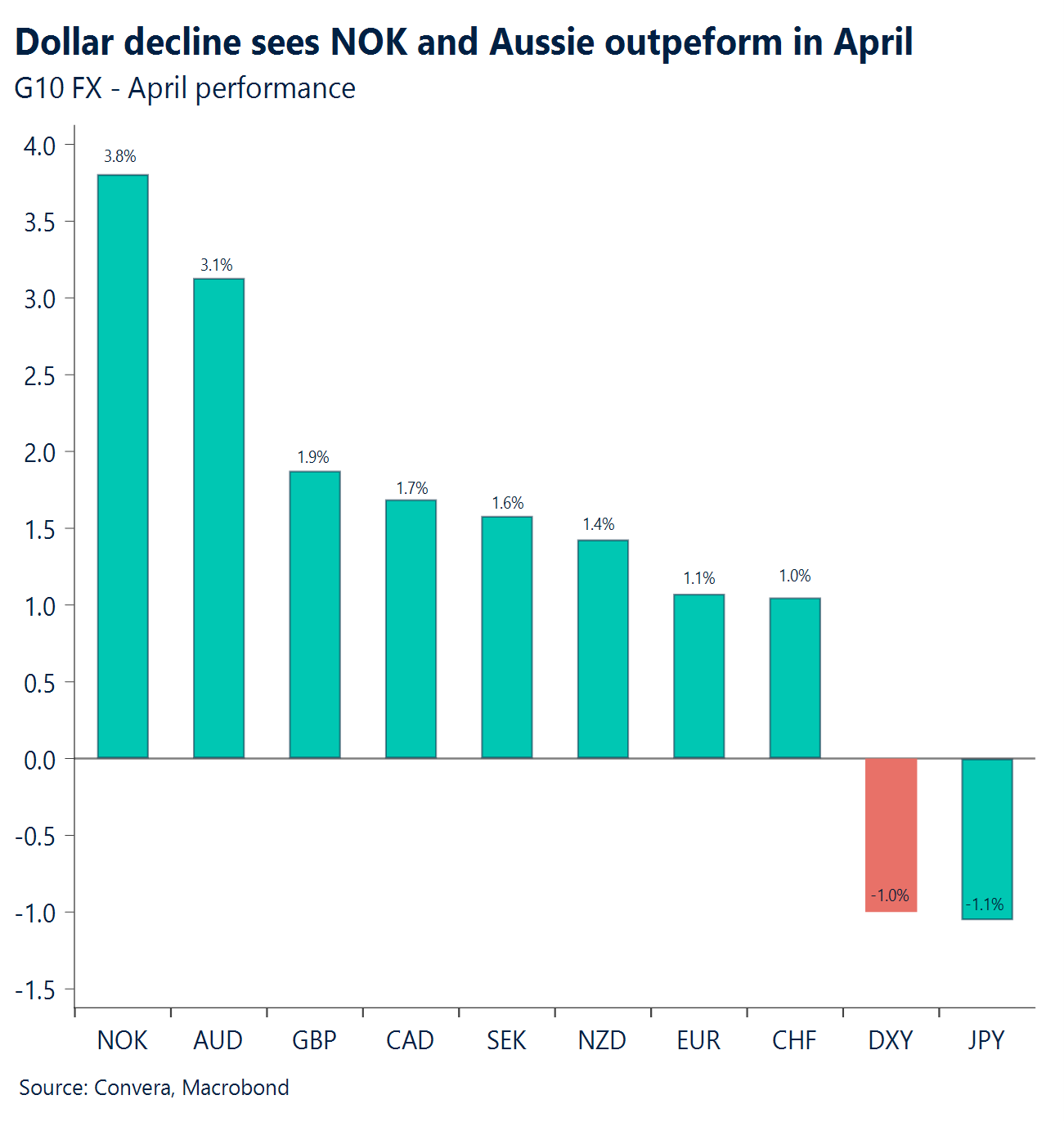

USD BoJ move hits greenback. The US dollar ended the week broadly lower, with losses mostly driven by the impact of suspected Bank of Japan intervention in the USD/JPY pair on Thursday. Earlier in the week, the US dollar strengthened after the Federal Reserve held interest rates steady, but the vote included four dissents, making it the most divided Fed decision since the early 1990s. Three voting members argued against signalling future rate cuts, citing inflation risks and resilient economic conditions. In contrast, Trump‑appointed board member Stephen Miran dissented in favour of an immediate 25‑basis‑point rate cut, arguing policy had become unnecessarily restrictive. More broadly, the USD index remains in a clear downtrend, with the DXY below key short‑ and long‑term moving averages. Coming up, the focus is on jobs, with JOLTS (job openings and labor turnover) on Tuesday, ADP on Wednesday and non‑farm payrolls on Friday.

EUR Struggles to capitalize. The EUR/USD edged back towards ten-day highs in a relatively muted week of trading for the single currency, helped by late week USD losses, with worries about the impact of high oil prices on European growth dampening any positive support from potentially tighter policy. The euro was weaker in other markets, with EUR/GBP nearing eight-month lows. The euro struggled even as the European Central Bank kept the door open to tighter policy at Thursday’s rate decision. While holding rates steady, the ECB said it would consider hikes at its next meeting in June if energy prices remained elevated. Technically, EUR/USD remains in a moderate uptrend, with support seen at 1.1600 and resistance at 1.1850. A quieter week lies ahead, with final manufacturing PMIs on Monday, final services PMIs on Wednesday and retail sales on Thursday.

GBP Breaching 1.36 resistance. Sterling proved remarkably resilient through late April, tracking buoyant global risk appetite even as higher oil prices capped outright upside. GBP/USD bounced cleanly off its 100‑day moving average early in the week and went on to pierce 1.36, printing a new post‑conflict high, underscoring that the broader April uptrend remained intact. Rising energy prices — with oil rebounding sharply — acted more as a ceiling than a reversal trigger, tempering rallies rather than derailing them. The Bank of England’s hold at 3.75% briefly weighed on the pound as the messaging leaned marginally dovish, but the impact proved short‑lived. Instead, global FX dynamics took centre stage, with a sharp surge in the Japanese yen dominating price action late in the week and driving volatility across USD crosses, including GBP. Relative performance remained constructive. GBP/EUR continued to grind higher, with 1.16 now in sight, supported by widening UK–Eurozone growth, yield and policy differentials. Overall, sterling ended the period supported by risk sentiment and technical momentum, with external shocks — not domestic weakness — setting the pace.

CHF Riding yen’s coattails. The Swiss franc remains locked in a regime of resilience rather than outright haven leadership, but this week it benefited from a sharp rally in the Japanese yen. EUR/CHF and USD/CHF both fell abruptly, with EUR/CHF erasing all of its April gains in a single session, highlighting how quickly CHF moves can unfold when positioning is crowded and volatility spikes. The move appears driven less by a shift in Swiss fundamentals and more by cross‑haven spillovers, as broader market jitters and renewed intervention risk in Japan triggered defensive demand across low‑yielding currencies. In that context, CHF functioned as a secondary beneficiary alongside JPY, despite remaining constrained by domestic policy considerations. Those constraints remain intact. Switzerland’s real effective exchange rate sits near a 15‑year high, reinforcing the SNB’s heightened sensitivity to further strength and its explicit signal that intervention tolerance has increased. As a result, CHF gains are likely to remain episodic and spillover‑driven, rather than marking a shift toward sustained, independent haven outperformance.

CAD A USD story. CAD’s April gains look a lot more like a USD story than a fresh Loonie renaissance. USD/CAD sliding toward the mid‑1.36s has lined up neatly with a broader unwind in safe‑haven demand as markets price a less binary Middle East outcome, and the US dollar slowly sheds the conflict premium it built when escalation risk felt open‑ended, even as oil prices remain triple-digit. Without a durable domestic growth turn, without a rates impulse that forces a repricing of the BoC path, and with trade policy uncertainty still acting like an overhead premium as CUSMA/USMCA conversations remain sluggish, there just isn’t a second engine to pull USD/CAD meaningfully closer to “fair value.” So yes, the loonie has looked better on the tape recently, but strip out the USD’s de‑escalation unwind. February GDP met expectations, and a hawkish MPR and BoC press conference successfully repriced the year’s outlook toward a September hike. Consequently, the CAD has anchored near 1.36, though it remains vulnerable to US headline risk. While 1.356 stands as the immediate support floor, the pair likely maintains a choppy bias around 1.36 leading into next Friday’s employment report.

AUD All eyes on RBA. The AUD was stronger over the week boosted by USD weakness. Despite rising headline inflation, the closely watched trimmed mean measure cooled to 0.8% last quarter, dodging a feared price spike and easing the need for urgent rate hikes. While monthly prices hit 4.6% in annual terms, they stayed below the 4.8% danger zone. The pair is now eyeing the 0.7200 psychological barrier and the recent peak of 0.7222. On the downside, the 21-day EMA at 0.7108 and the 50-day EMA at 0.7048 provide immediate support. With the worst-case inflation scenario avoided, the AUD/USD will likely move in sync with global trends. Investors are now shifting focus toward upcoming building approvals and the next RBA interest rate decision, due Tuesday, for further direction.

CNH Yuan weakens despite steady outlook. China’s leadership reported a robust start to 2026, yet the Yuan remains under pressure. Even with Moody’s upgrading China’s outlook to “stable” due to manufacturing resilience, the USD/CNH recently climbed to a two-week high. USD/CNH has risen 0.5% from its recent floor of 6.8059, now pushing toward technical hurdles. Resistance sits at the 21-day EMA of 6.8430, with the 50-day EMA further up at 6.8701. Traders are balancing the government’s focus on self-sufficiency against a strengthening U.S. Dollar. All eyes now turn to the upcoming RatingDog Services PMI and official foreign exchange reserves data to gauge further momentum.

JPY Jumps as suspected FX intervention. The yen staged a sharp rebound after Japanese officials stepped in to counter its depreciation, with markets reacting to suspected FX intervention aimed at arresting the yen’s slide beyond the critical 160.00 level against the dollar. The move triggered aggressive short‑covering in USD/JPY, reinforcing the idea that authorities remain unwilling to tolerate sustained weakness above intervention-sensitive levels, even as yield differentials continue to favor the dollar. On that note, the Bank of Japan left rates unchanged at 0.75%, though the decision was marked by a split vote and a higher inflation outlook, strengthening the case that policy normalization is approaching. Markets now price roughly a 65% chance of a rate hike at the June meeting. Even so, structural headwinds continue to undermine the yen’s medium‑term outlook. High energy prices and persistent labour shortages are weighing on growth and worsening Japan’s external balance, factors that have left USD/JPY resilient despite rising intervention risks. Prior to today’s reversal, the pair had been hovering near its recent 160.47 peak, underscoring how stretched positioning had become. Market participants are now bracing for the S&P Global Services PMI, wage income reports, and updates on the monetary base to see if the Yen can recover.

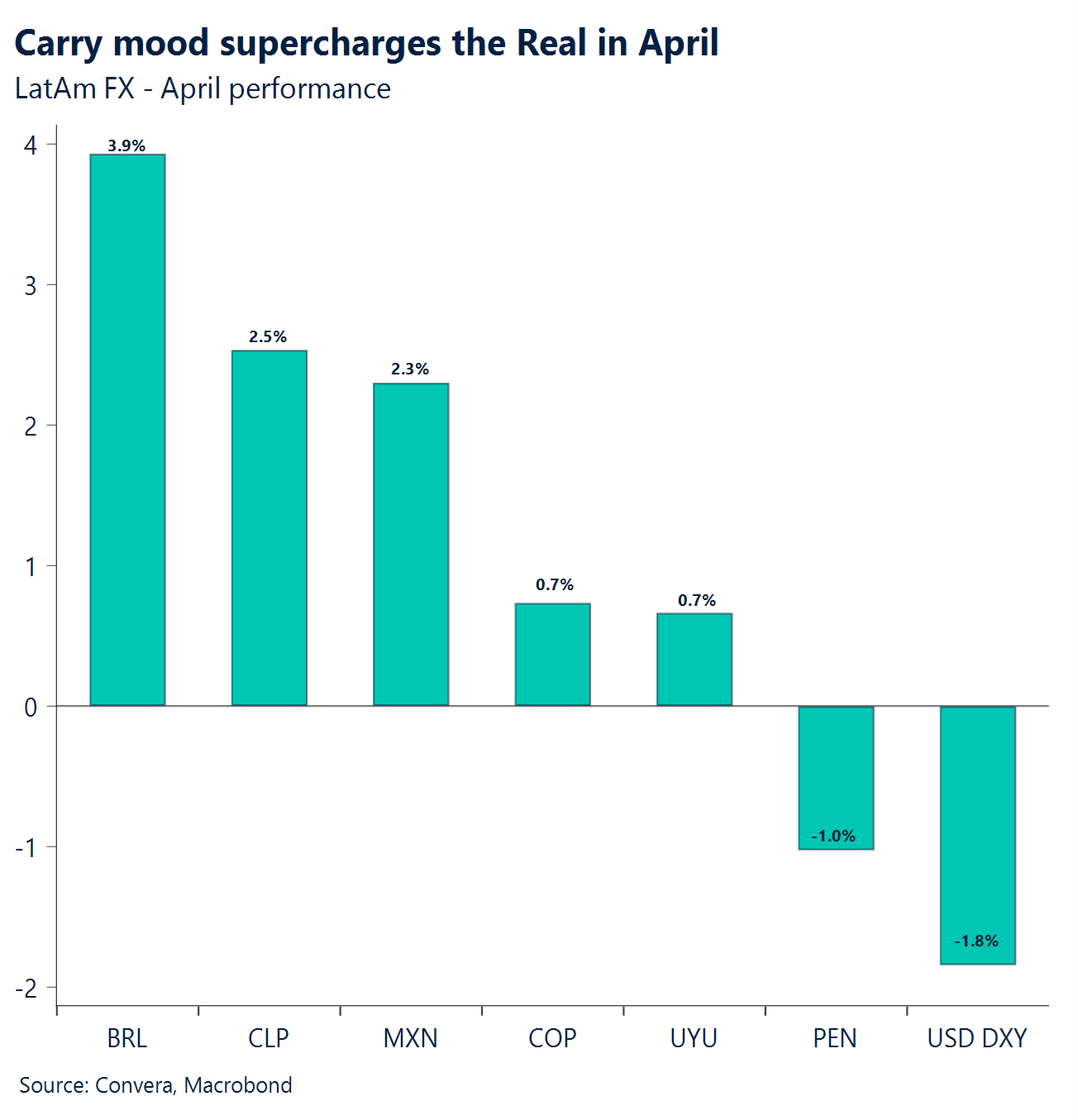

MXN Left behind. The Mexican peso was a notable carry beneficiary through April, up ~2.3% in April, trailing the BRL (~3.5%) and CLP (~2.5%) among LatAm peers, an environment where “carry mood” broadly outperformed. That strength, however, faded late in the month, with USD/MXN pushing up toward ~17.5, due to geopolitical tensions boosting oil prices higher. Importantly, Mexico inflation easing (headline 4.53% in early April vs 4.63% in March; core down to 4.27%, a five‑month low) has pulled forward expectations of a more dovish Banxico, reinforcing the lack of impulse versus USD. Also, Mexico’s 1Q GDP print underscores an economy operating below potential and suggests the negative output gap is widening more than policymakers anticipated. Technically, the USD/MXN around ~17.52, sits above the 20‑day (~17.42) but below the 50‑ and 100‑day (~17.57–17.60) and well below the 200‑day (~18.05), a setup consistent with near‑term consolidation/mean reversion within a broader MXN‑positive (lower USD/MXN) trend. Net: MXN’s late‑April wobble looks more like a risk‑off + policy‑repricing pause than a full trend break, but the balance of risks near term hinges on Banxico’s easing signal, Fed rhetoric, and whether trade uncertainty continues to cap Mexico’s cyclical rebound. Next Thursday, Banxico is expected to cut its overnight rate by 25 bps.

BRL Carry darling. Brazil’s central bank delivered the expected 25 bp cut, taking the Selic to 14.5%, but the message was more hawkish than in March. Policymakers avoided guidance to keep flexibility as they cited firmer inflation and uncertainty around war and oil prices. Even after the cut, policy is still very tight, with the ex ante real rate near 10%, about double neutral, so more easing is possible but not guaranteed. The bank lifted its inflation forecast for the policy horizon, now end 2027, to 3.5% from 3.3%, and stressed elevated risks. Markets still expect another 25 bp cut on June 17 and a year end Selic closer to 13.25%, but risks tilt upward if expectations worsen or oil stays high. Labor remains tight, with unemployment at 6.1% from 5.8%, still low historically. The Real held near 4.98 per dollar, a two year high, supported by carry and the bank’s caution on further cuts. Spot sits below moving averages, consistent with BRL strength. The next leg depends on inflation and activity data to let June easing proceed or force a pause.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.