- Shock, but no awe. A naval blockade on maritime traffic in the Strait of Hormuz reignited oil and briefly lifted the USD at the start of the week. The market reaction, however, was notably restrained, highlighting rising geopolitical fatigue.

- From threat to tactic. The blockade was quickly reframed as negotiating leverage rather than escalation. Risk sentiment flipped decisively, with markets shifting to cautious optimism around a more durable peace outcome.

- Cooling volatility. Measures of risk rapidly compressed, with the VIX falling to its lowest level since late February. Oil reversed sharply, equities rebounded alongside precious metals, and the USD slid to six‑week lows.

- Record highs. Ceasefire confirmation cemented the de‑escalation trade, pushing multiple equity indices to record highs. Renewed demand for AI-related stocks added momentum, helping drive the Nasdaq >4% higher.

- Too much too soon? However, Gulf Arab and European officials suggest a permanent ceasefire deal may still be months away, tempering enthusiasm and reinforcing the idea that markets may have moved faster than diplomacy.

- Background risks linger. IEA warnings on jet fuel shortages in Europe and renewed IMF caution underscore that conflict‑related economic damage may still be underpriced.

- Rates hold the line. Though yields have fallen broadly, rates markets remain reluctant to fully fade inflation risks, with hikes still priced for many central banks this year.

Global Macro

Growth cycle meets war premium

China Q1 GDP + March activity. China’s Q1 print beat consensus on headline growth but the underlying mix was uneven: GDP +5.0% y/y (Q1) and +1.3% q/q, industrial output +5.7% y/y (Mar) beat expectations, while retail sales slowed to +1.7% y/y (Mar) and fixed‑asset investment +1.7% y/y (Q1) undershot. Market read‑through was “resilience, but demand still soft”. :Hang Seng extended gains, while the offshore yuan was largely flat and bonds steady, consistent with a “growth pulse intact, policy support still needed” setup. China is stabilizing the cycle, but war‑driven energy tightness is capping upside.

US PPI (Mar), inflation pipeline under an energy shock. The wholesale inflation print was hot on energy, cooler underneath: headline PPI +0.5% m/m and +4.0% y/y, with final demand goods +1.6% driven by energy +8.5% (gasoline +15.7%), while final demand services were unchanged and “core” (ex food/energy/trade) rose +0.2% m/m. Markets treated it as modest relief rather than an all‑clear. Treasuries rose and yields edged lower by a few bps as oil retreated, but some components relevant to the Fed’s preferred inflation measures remain firm, keeping the cautious tone on inflation.

IMF WEO, the regime shift gets official. The IMF’s baseline now embeds the war shock as a growth drag with inflation risk: it projects global growth at 3.1% in 2026 and 3.2% in 2027, explicitly warning that the conflict can tighten financial conditions via commodities and inflation expectations.

Euro area CPI (Mar) + ECB reaction function. Euro area inflation re‑accelerated with headline CPI at 2.6% y/y (Mar) and core at 2.3% y/y, keeping the “energy shock → inflation persistence” debate front‑and‑center for European rates. But ECB communication poured cold water on “imminent hikes”: Lagarde said the economy is “between the baseline and the adverse” scenarios and stressed it’s too early to commit to a rate path; though some officials are leaning toward an April hold as they assess war fallout.

Week ahead

Sentiment pulse on the economy

- Sentiment check. The eurozone will see the release of several key sentiment indicators, including the IFO and ZEW surveys as well as the PMIs. The conflict has inflicted lasting damage on the outlook for the energy‑dependent euro area, and these indicators tend to be quick in capturing such a drag, as already signalled by the March readings. A further validation of a stagflationary environment – characterised by subdued activity and elevated prices – therefore appears likely.

- Jobs print to sharpen BoE trade-off. In the UK, the focus turns to the jobs report. While the data relate to February, and therefore pre‑conflict conditions, evidence of a softening labour market has been a persistent constraint for the Bank of England, strengthening the case for further easing amid still‑elevated inflation. As such, the release may serve as a reminder of the Bank’s increasingly stark two‑sided risk profile.

- Inflation test for BoE. UK inflation will be a key focal point next week. Earlier forecasts had pointed to inflation returning to target by April, but the conflict has materially altered that trajectory. Headline CPI for March is now expected to rise to around 3.3% from 3.0% in February. Confirmation of renewed inflationary pressure would reinforce the BoE’s policy paralysis as it navigates an increasingly stagflationary backdrop.

FX views

De-escalation trade awaits confirmation

USD Waiting for proof. The US dollar index – the DXY – has edged about 0.4% lower this week and is down roughly 1.7% on a month‑to‑date basis. Sentiment has improved markedly since the US and Iran agreed to a two‑week ceasefire earlier last week. Despite the failed talks in Islamabad, both sides remain committed to avoiding a return to strikes, while negotiations toward something more durable than a ceasefire appear to be ongoing. That said, more concrete evidence of a lasting peace deal is likely required to justify further dollar downside. So far, President Trump has unilaterally hailed progress in the talks, something markets have increasingly learned to discount. The Strait of Hormuz remains effectively closed and, unless the weekend brings news of a more durable peace agreement with Hormuz reopening explicitly attached as a condition, the dollar index is likely to remain comfortably anchored in the lower 98s, with Brent crude holding just south of USD 100 per barrel.

EUR Risk-on helps, fundamentals now needed. EUR/USD has markedly retraced March’s bearish trend and now hovers just south of the 1.18 handle, broadly in line with levels last seen on 27 February, while sitting above all key moving averages. The pair is up around 2% so far this month. It is therefore understandable that, in the absence of a credible peace plan, a sustained move above 1.18 appears unwarranted. The fundamental backdrop helps reinforce this caution. Our short‑term fair‑value model for EUR/USD points to levels in the low‑1.17s, reinforcing the view that any push toward January 1.19/1.20 highs is likely to prove short‑lived for now. In a macro environment marked by still‑elevated oil prices, unconvincing ECB hiking propensity, and an uncertain growth outlook, the pair lacks sufficient fundamental support to break north of the 1.18 area on a more sustainable basis.

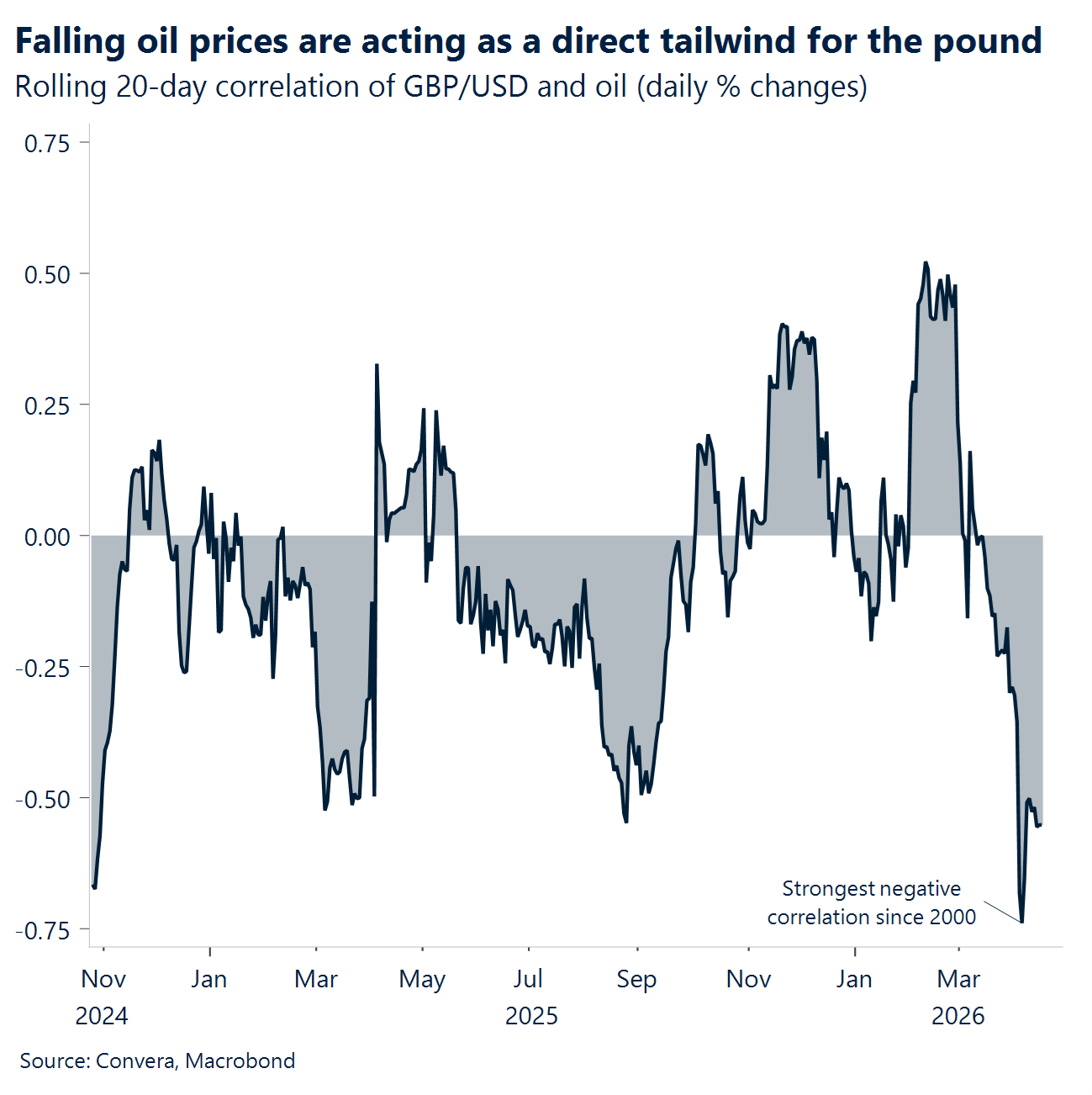

GBP Powers to pre-war levels. Sterling extended its April rally this week, with GBP/USD rising to pre-war levels near 1.36, driven primarily by improving global risk sentiment and a sharp pullback in energy prices. Crucially, the pair held and then decisively broke above its 200‑day moving average near 1.3410. This break has flipped medium‑term momentum bullish, with GBP/USD also now trading above all major daily moving averages. Price action has been tightly linked to energy markets. The 20‑day rolling correlation between GBP/USD and oil turned sharply negative at the onset of the war and remains near its most extreme inverse reading since 2000, highlighting sterling’s heightened sensitivity to energy‑driven risk dynamics. Domestically, stronger‑than‑expected GDP (+0.5% m/m) provided some marginal support, though the data reflects pre‑war conditions and does little to shift the forward‑looking outlook. Consistent with that, BoE rate pricing has been scaled back rather than reinforced, confirming that recent GBP strength is not yield‑led. Overall, this week’s gains have been technically driven, oil‑sensitive, and closely tied to global risk‑on conditions, leaving the rally vulnerable to renewed energy or geopolitical shocks, whilst domestic conditions remain a headwind.

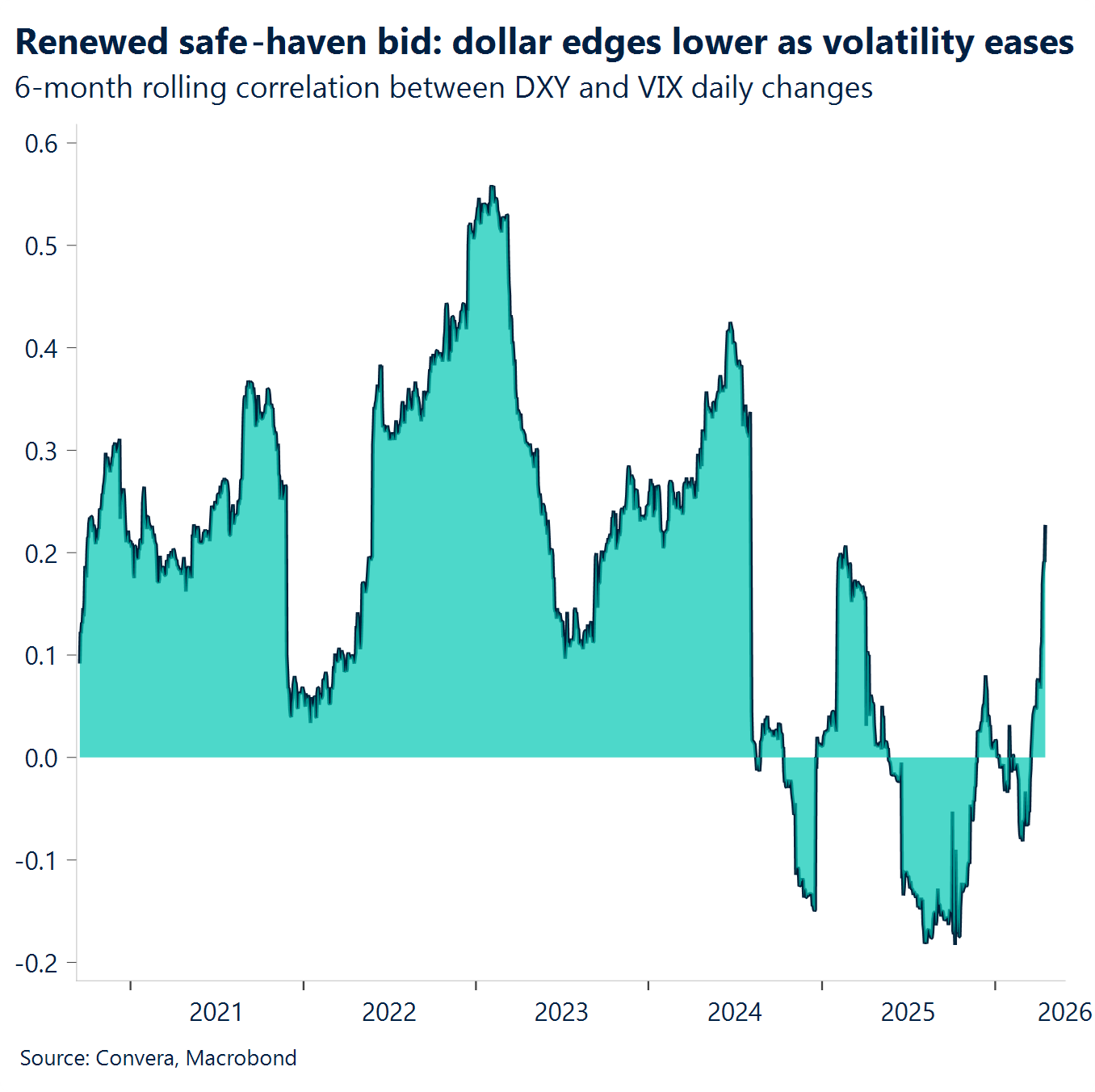

CHF A constrained stabiliser. As peace talks unwind conflict trades, the Swiss franc is up over 2% versus the USD MTD. The franc has not been the preferred safe haven since the Iran conflict escalated. It had failed to attract meaningful marginal haven inflows, with the USD instead emerging as the dominant defensive asset. A key constraint has been SNB rhetoric. At its March meeting, the SNB hardened its exchange‑rate language, stating its willingness to intervene had increased due to Middle East tensions. Evidence of actual intervention remains limited though. Sight deposits have risen just a touch, while the increase in FX reserves in March likely reflects valuation effects amid volatile currency and gold markets. Even so, rhetoric alone has been sufficient to cap CHF upside. Combined with higher energy prices weakening Swiss terms of trade and already stretched valuations, this has produced a regime in which the USD has captured haven inflows, while CHF has mainly stayed defensive but capped, only benefiting opportunistically when conflict trades unwind rather than during the escalation phase.

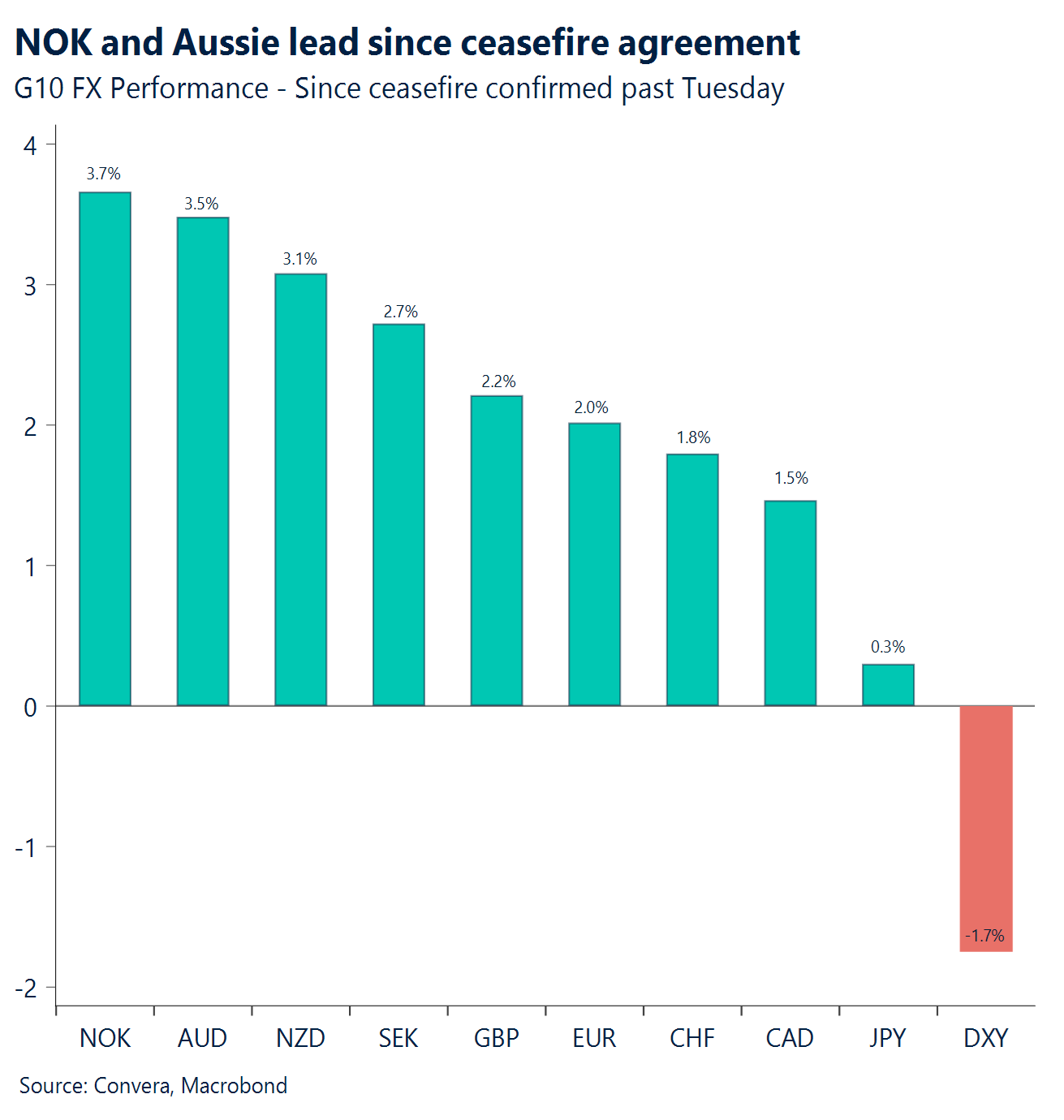

CAD Needed relief. The Loonie found some much-needed relief this week as the USD/CAD pair dropped from 1.3878 toward 1.37. This shift comes as de-escalation hopes and improving risk sentiment take hold across broader markets. Since the recent ceasefire agreement was confirmed, the Canadian Dollar has gained roughly 1.5% against the Greenback. This trend clearly shows that when geopolitical fears cool, the US Dollar loses its “risk premium,” allowing the CAD to return toward its medium-term fair value. Extension of the current move will depend on whether US Dollar softness can gain traction as the “oil war premium” unwinds. Additionally, the pair’s direction will hinge on any upside surprises in the upcoming macro data releases. Looking ahead to next week, the most significant macro data point arrives on Monday. March CPI is expected to show a sharp 1.0% monthly jump, which would bring the yearly inflation reading to 2.5%. Friday’s retail sales will also be essential to watch. These figures will provide a clearer picture of how Q1 GDP was shaping up just before the economic impact of the US-Iran conflict began to register.

AUD Aussie jobs hold firm. Australia’s job market proved resilient in March. Overall, the figures point to a still-tight labour market. RBA deputy governor Andrew Hauser reinforced a cautious message. He said policymakers are no longer convinced current interest rate settings are tight enough to contain inflation risks. A broader risk-friendly backdrop lifted the Australian dollar, pushing AUD/USD to a fresh multi‑year high near 0.7197 on 16 April. AUD/USD was the strongest performer in the G10 space over the week of 13 April, gaining about 1%. Markets now price a 73% chance of another RBA rate increase in May. That said, momentum looks stretched. The 14‑day RSI is close to overbought territory, leaving AUD/USD vulnerable to a pullback after its recent run. The next psychological hurdle sits near 0.7200. On the downside, initial support comes in at the 21‑day EMA around 0.7048, followed by the 50‑day EMA near 0.7002. Markets will watch upcoming S&P Global Manufacturing and Services PMIs, along with the unemployment rate.

CNH Strong China growth. China’s economy picked up speed in the first quarter. GDP grew 5% year-on-year, beating the 4.8% consensus and improving from 4.5% in the previous quarter. The headline strength should reassure policymakers and reduces the urgency for any policy shift at the upcoming Politburo meeting. In Asia, AUD/CNH hovered near a one‑month high, while SGD/CNH traded close to a one‑week high. Meanwhile, USD/CNH has rebounded about 0.2% from its recent low of 6.8059, last seen on 14 April. The next resistance for USD/CNH sits at the 21‑day EMA near 6.8539, followed by the 50‑day EMA around 6.8858, levels that may attract renewed USD buying interest. Markets will focus on upcoming Loan Prime Rate announcements.

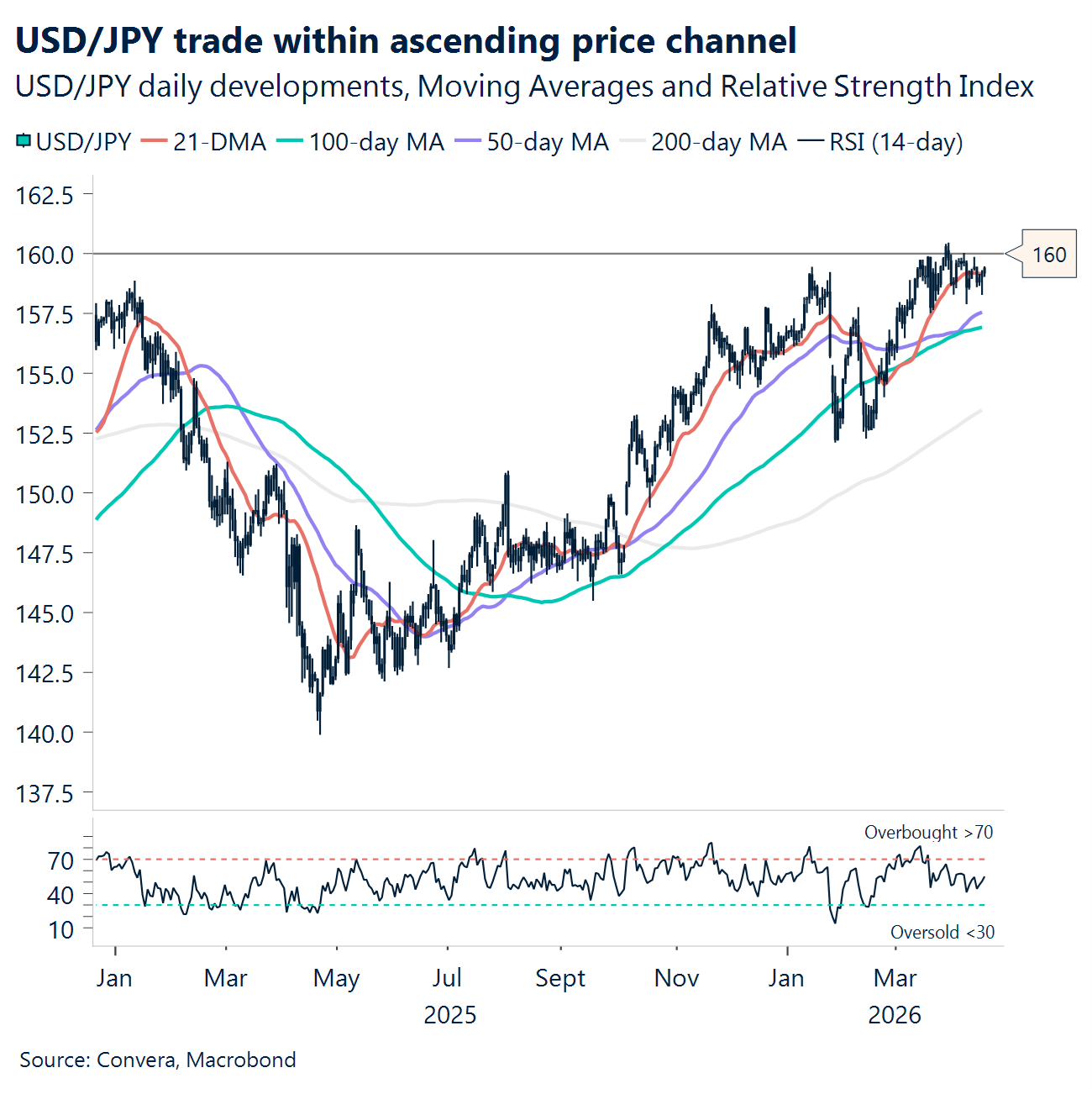

JPY Japan talks caution. Bank of Japan governor Kazuo Ueda highlighted Japan’s balancing act between rising prices and a slowing economy. He also pointed to Middle East tensions as a major source of uncertainty. His comments signal that the central bank remains cautious and reluctant to raise interest rates in the near term. Japan’s top currency diplomat, Atsushi Mimura, confirmed coordination with the United States on currency matters. In FX, USD/JPY has slipped about 0.7% from its late‑March peak near 160.46 and is now hovering around the 159.00 area. Initial support lies at the 21‑day EMA near 159.02, followed by the 50‑day EMA around 158.15. Elsewhere, Yen weakness remains striking. AUD/JPY sits just 0.1% below its strongest level in 36 years. Markets will watch upcoming trade balance data, S&P Global Services PMI, and national CPI releases.

MXN Revisiting 2026 lows. Rising risk sentiment has stalled the dollar rally for now. The US dollar index has stayed soft this week as investors lean into the classic de-escalation trade after the ceasefire was confirmed. Since last Tuesday, the greenback has given back nearly all its March gains, suggesting the conflict premium is fading fast. Positioning is shifting out of safe havens and back into growth-heavy sectors and emerging markets. Against this backdrop, the Mexican peso has staged an impressive comeback as a relief rally sweeps through the currency markets. The USD/MXN pair has moved sharply from its February peaks, moving back toward the 17.25 area, close to its year-to-date lows. Essentially, the recent spike in volatility has faded, which allows the peso to reclaim its standing among high-yielding emerging market peers. The sustainability of this move will be tested by a very busy economic calendar next week. Thursday will be particularly important, as we receive fresh updates on bi-weekly inflation and retail sales performance. Investors will also be watching Friday’s unemployment and economic activity data to assess Mexico’s underlying growth momentum.

BRL Hitting the $5. Current market conditions have turned noticeably calmer as FX volatility eases across both emerging markets and the G10. This shift has allowed EM currencies to regain traction, supported by optimism surrounding potential US–Iran peace talks and a softer US Dollar. With crude prices cooling, investors finally have some breathing room, creating a steadier backdrop for regional currencies to reprice without the constant threat of headline-driven volatility. In this environment, the Brazilian real has emerged as a clear leader. The BRL/MXN cross has pushed higher toward the 3.46 level, while the Real has also strengthened against the Dollar, breaking below R$5 for the first time since early 2024. This momentum is fueled by elevated local rates, a rotation of capital away from the US, and favorable trade dynamics. Ultimately, a stronger Real is improving Brazil’s inflation outlook, providing much-needed domestic relief even as the global macro picture remains in transition. Further gains from here will rely mostly on a sustained risk on environment and a softer USD.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.