- Truce extended. As expected, the U.S. and China extended their tariff truce by 90 days, averting triple-digit duties on each other’s goods through November. This helped keep risk appetite firm, with US equities notching record highs.

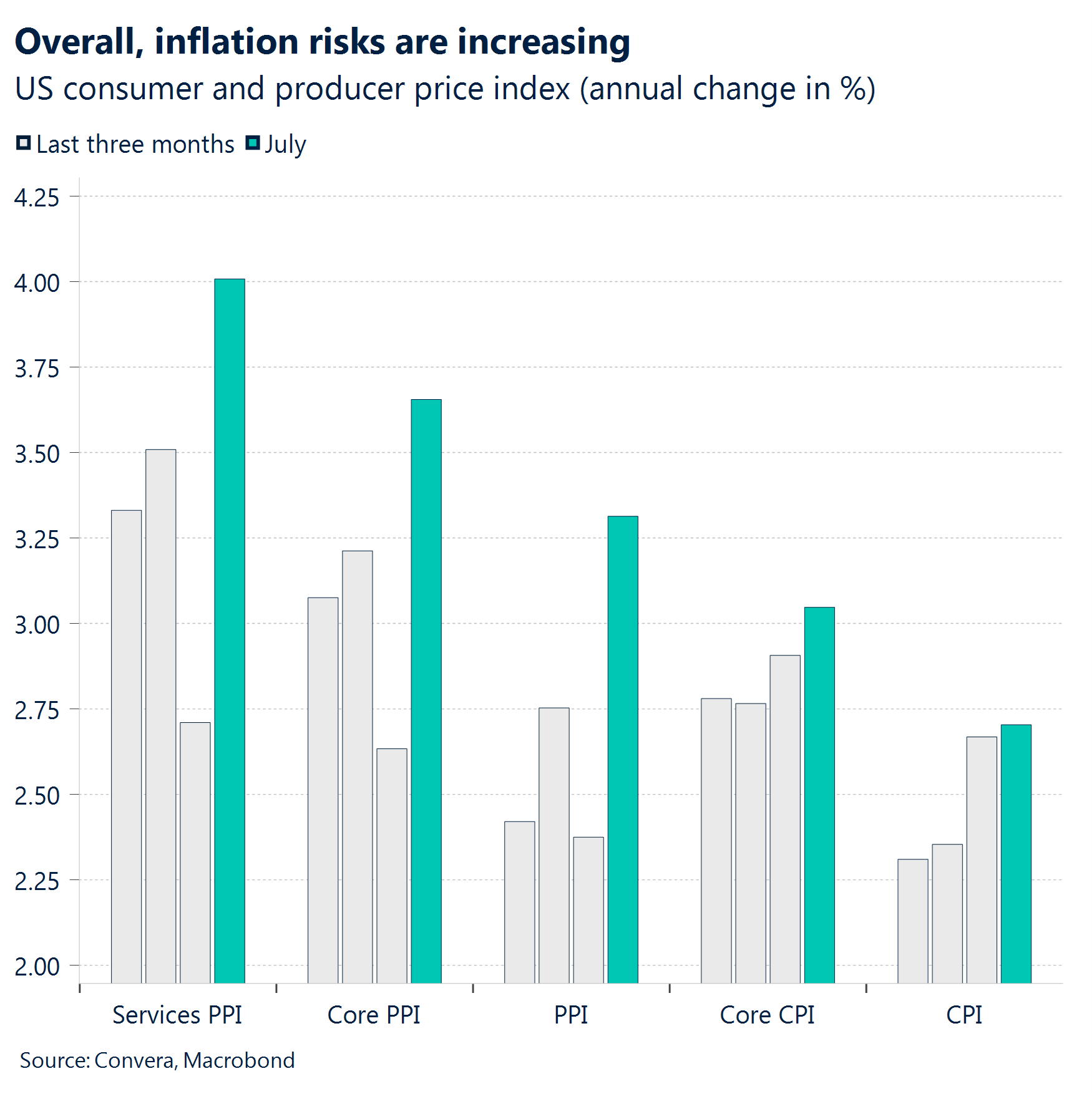

- CPI calm, PPI storm. U.S. CPI met expectations, but PPI surged past forecasts, revealing divergence. Either companies are absorbing higher costs and facing margin pressure, or consumer inflation may soon rise as producer prices trickle through.

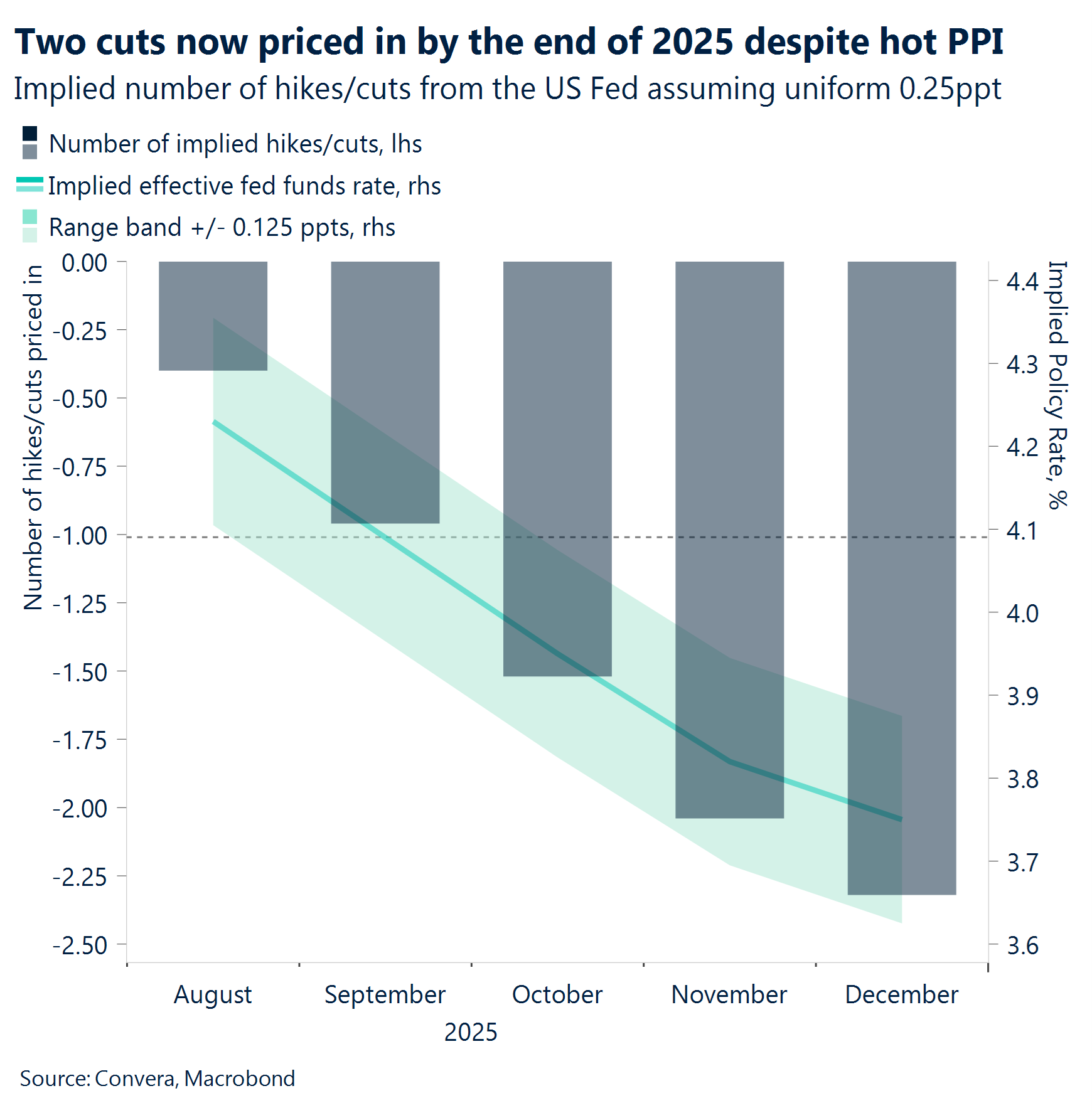

- Volatile policy pricing. Talks of a jumbo 50bps Fed cut faded fast after the PPI data, but markets are still pricing two 25bps cuts out of the next three Fed meetings before year-end. Again, this has helped fuel risk appetite of late.

- Old anchor, new risks. Traditional forces are reasserting themselves in the US dollar story. Just as stability returns, mounting Fed rate-cut pressure risks unsettling the balance as renewed sensitivity to yields could fuel fresh weakness.

- Aussie drops on dovish RBA. As expected, the Reserve Bank of Australia cut its official cash rate, but signaled further easing may be needed, which dragged AUD lower.

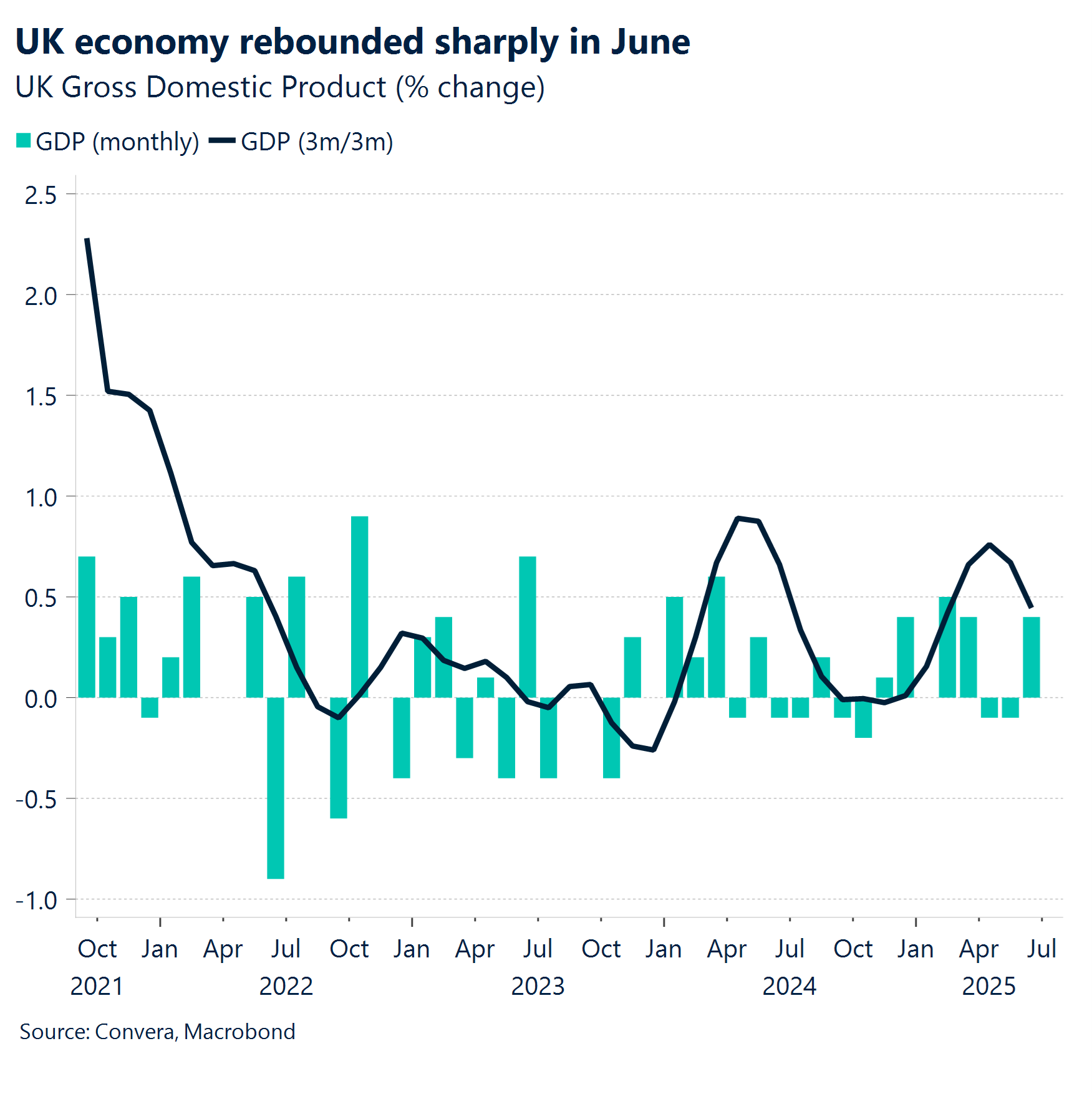

- Sterling pops on UK data. UK labor market data showed private wage growth still hovering around 5%, whilst GDP figures beat forecasts – supporting hawks at the Bank of England and boosting the pound to 1-month highs.

- Charm offensive. Russian President Vladimir Putin sought to strengthen his rapport with Donald Trump ahead of their summit in Alaska later today, but Trump held firm.

Global Macro

Markets eye September cut despite hot PPI

US Inflation Data. CPI and PPI were released this week, but the market’s reaction was driven more by the bigger picture. While the Producer Price Index (PPI) came in surprisingly high, the Consumer Price Index (CPI) was more moderate than feared, rising 0.2% month-over-month. This data, coupled with a series of weaker labor market reports, has solidified the market’s belief that the Federal Reserve will cut interest rates at its September meeting. Markets are pricing in with a 90% probability of a 25 basis point cut despite the hotter than expected PPI. This conviction is so strong that some market participants, including Treasury Secretary Scott Bessent, are even suggesting the possibility of a more aggressive 50 basis point cut, though this remains a less likely outcome. The market is effectively betting that the Fed will prioritize supporting a slowing economy over its lingering inflation concerns, viewing the PPI surge as a temporary effect of tariffs rather than a long-term inflationary trend.

Australia. The RBA cut rates by 25 basis points in a unanimous decision, with all nine board members backing the move. The central bank flagged rising uncertainty, warning that households and businesses may hold off on spending. While wages have climbed, the RBA noted that job market conditions remain slightly tight.

Global Macro. The UK’s Q2 GDP surprised to the upside, growing by a stronger-than-expected 1.2% YoY and 0.3% QoQ. This positive data, driven by growth in the services and construction sectors, initially boosted the Pound. It also complicates the Bank of England’s path toward further rate cuts, as the economy appeared more resilient than previously thought. The Eurozone’s Q2 GDP met expectations, with a modest 0.1% QoQ and 1.4% YoY increase. A key concern was the contraction of Germany’s economy, the bloc’s largest. The data reinforced a cautious outlook for the region and supported the European Central Bank’s current neutral policy stance, as there was no strong evidence of a significant rebound. China’s July data presented a mixed picture, with robust industrial production but weak retail sales. This suggested that while China’s export-oriented manufacturing sector was holding up, domestic consumer demand remained a key area of concern.

Regional outlook: UK

BoE easing bets pushed back further

Mixed labour market signals. Wage growth slowed more than forecast, with total earnings rising 4.6% versus 4.7% expected, down from 5% previously. Unemployment held steady at 4.7%. Regular pay (excluding bonuses) remained at 5%, while private sector earnings eased to 4.8%. Payrolled employees declined for a sixth straight month – the worst stretch since the pandemic. Job vacancies fell for the 37th consecutive period, and the vacancy-to-unemployment ratio dropped, signaling a looser labour market. Despite signs of cooling, wage growth remains above levels consistent with the Bank of England’s inflation target. The data supports the BoE’s hawkish hold last week, reinforcing rate expectations and offering some support to the pound via the yield channel.

GDP expands more than expected. The UK economy grew more than expected in Q2, expanding by 0.3% and beating the 0.1% forecast. Meanwhile, industrial production (0.7%) and manufacturing output (0.5%) also exceeded expectations for June, rebounding from contraction in the previous month. These figures contribute to a picture of a resilient economy that has held up despite tax hikes and President Trump’s tariffs. It’s worth noting that the higher Q1 growth of 0.7% was artificially inflated, as exporters rushed to secure deals ahead of the tariffs – boosting the monthly export figure by 3.3%, compared to 1.6% this quarter. Factory output also performed better than estimated.

Inflation is key. July’s inflation print will be pivotal. While growth remains subdued, the bigger question for markets is how long UK inflation will stay elevated above the Bank’s 2% target. With wage pressures still strong, a meaningful drop in realized inflation will be needed to shift the stance of more hawkish MPC members who opposed a cut earlier this month.

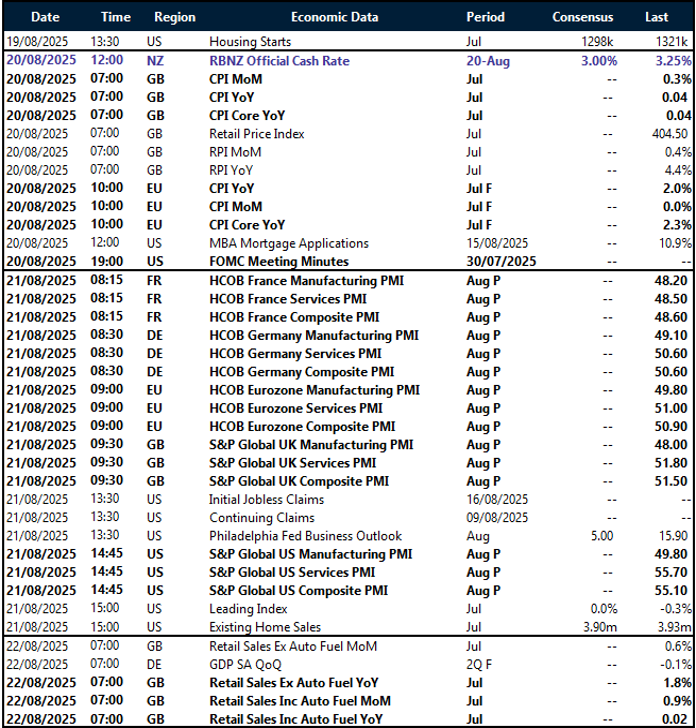

Week ahead

Global pulse monitor: PMIs in the spotlight

- A raft of PMIs. With a focus on the EU, UK, and US, these leading indicators will offer insight into how these economies are adjusting to the new, tariff-laden modus operandi. For the EU in particular, any signs of deterioration would compound the already disappointing ZEW survey expectations, which plunged following poorly negotiated terms with the US on the tariff front.

- UK inflation sticks. The Bank of England revised its inflation forecast upward during its last policy meeting, now projecting a peak of 4% in September, up from 3.7%. Inflation remains stubbornly high, complicating the BoE’s ability to commit to a more overtly dovish rate-cutting cycle. All eyes are on July’s report on Wednesday.

- Fed signals soon. The Jackson Hole Economic Policy Symposium, scheduled for 21–23 August, along with the FOMC meeting minutes due on 20 August, will be closely watched. These events may offer the first cohesive glimpse into the Fed’s evolving stance in light of recent data developments.

- UK retail sales in focus. Following stronger-than-expected GDP and resilient labour market data, retail sales will offer a crucial piece of the puzzle as the Bank of England scans for any signs of economic softening to justify further rate cuts amid persistently sticky inflation.

FX Views

Unclear signals, unsteady path

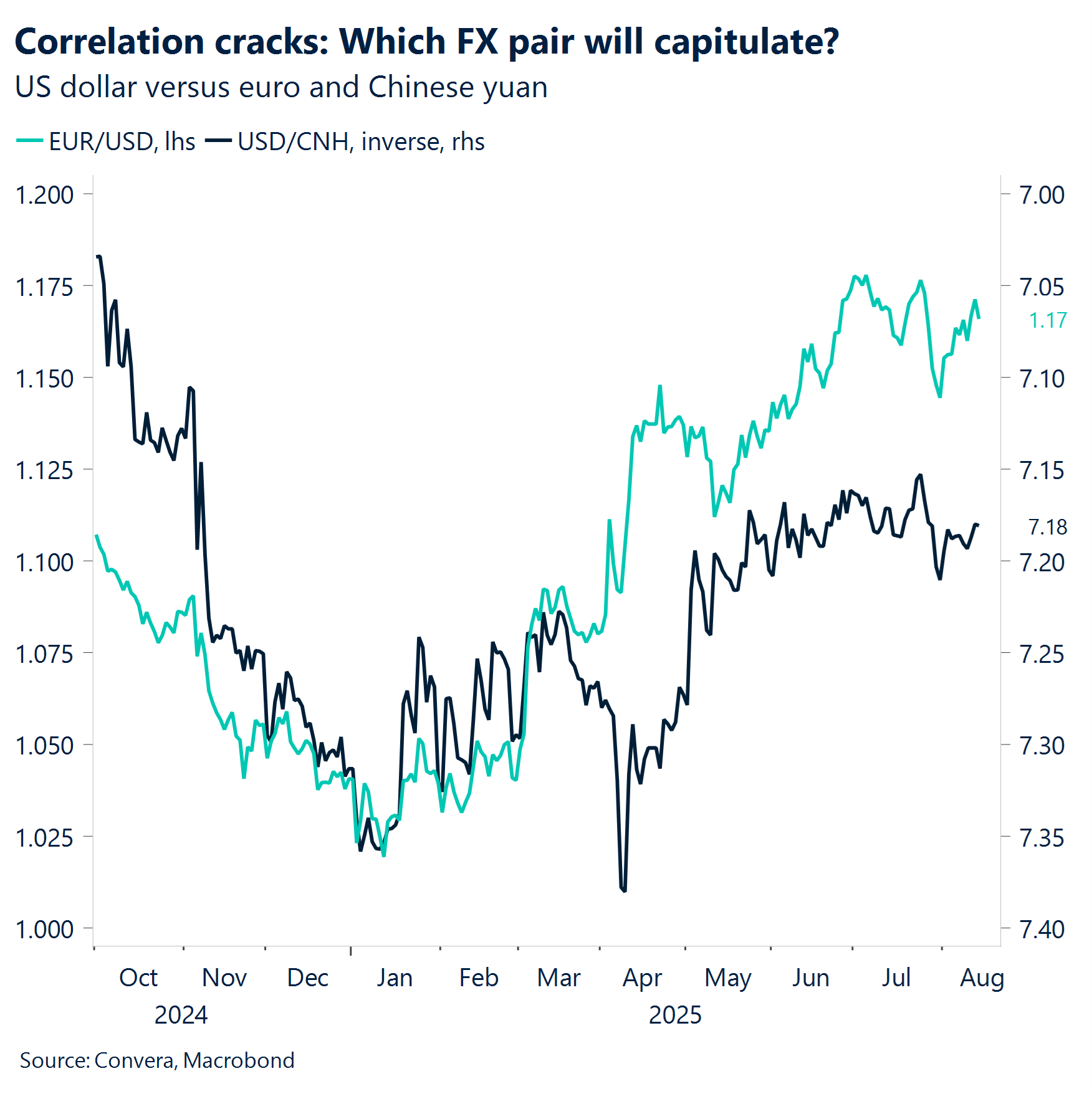

USD Dollar doubts deepen Bearish forces have consolidated against the dollar, primarily through the rate expectations channel, causing the dollar index – DXY – to fall ~2% this month. Recent weak labor data and mild inflation have raised expectations of a dovish Fed stance. However, Thursday’s spike in wholesale inflation – likely driven by tariff-related import costs – adds complexity to the Fed’s next move. A 25 basis-point cut is almost fully priced in for September, with some speculating about a 50 basis-point move. The predictions remain speculative amid a lack of Fed guidance and conflicting data. Dollar bearishness driven by lower rate expectations is being amplified by lingering skepticism toward the greenback. As investors continue to hedge USD amid renewed concerns following disappointing US macroeconomic data, lower interest rates would serve as an incentive for hedging by reducing its cost, further weighing on the dollar. Looking ahead, dollar price action continues to hinge on macroeconomic indicators as they continue to assess the impact of tariffs on the US economy.

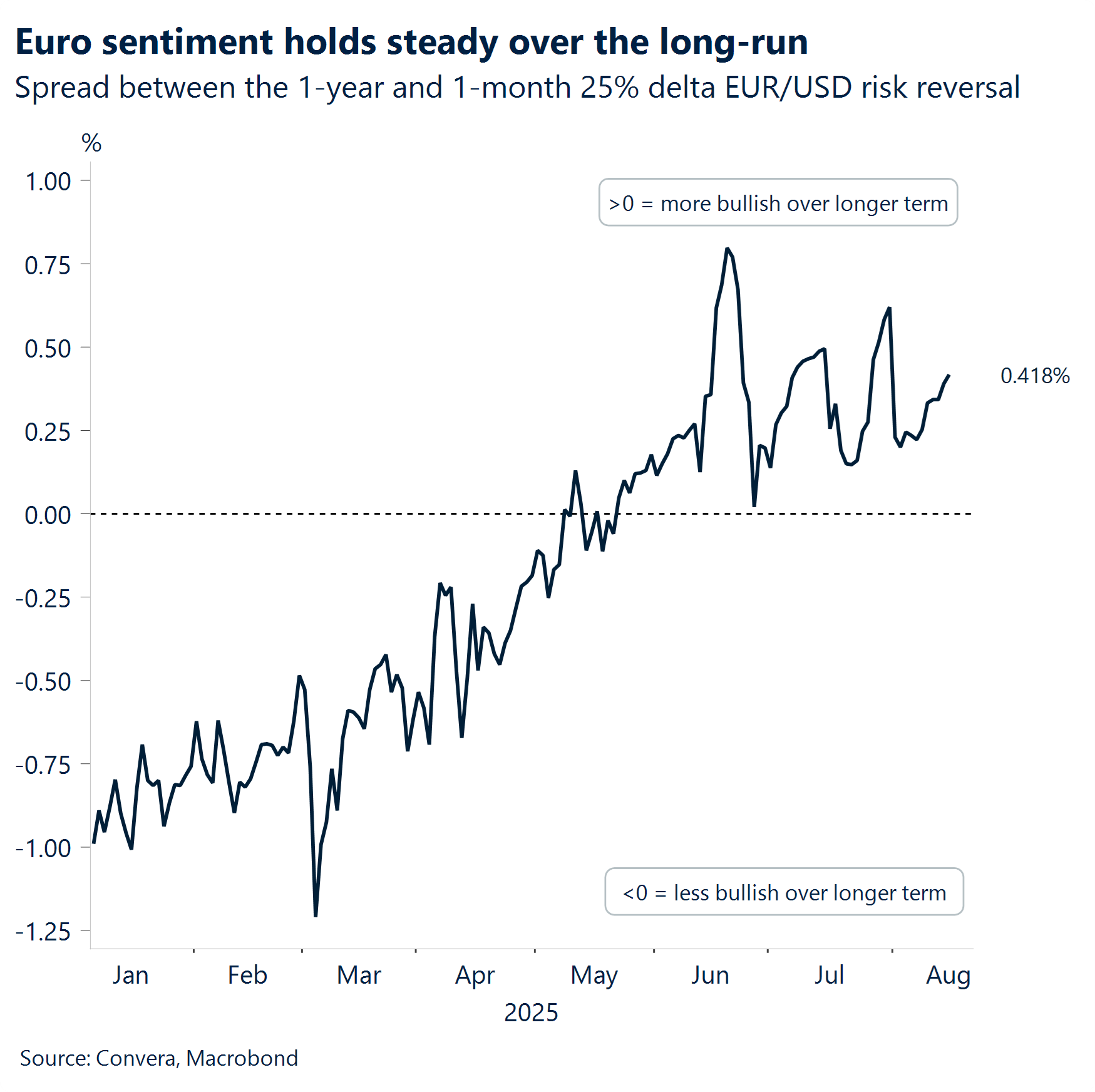

Euro eyes the highs The euro has secured, so far, favorable rate differentials against the dollar. The ECB appears comfortable maintaining its current stance, while the Fed may soon signal a dovish tilt following signs of a weakening labor market. Earlier this summer, a notable dovish shift from the Fed in late June pushed an already stretched EUR/USD pair into the 1.18 range, hitting a one-year high of 1.1829 on July 1st. Today, the prospect of further Fed dovishness positions the euro to potentially reclaim those highs. However, conflicting US data continues to challenge the case for a more decisively dovish shift. Also, since early July, trade-related noise out of Washington has lost some of its momentum in driving the euro higher. Meanwhile, the investor community has had time to digest the reality that tariffs – now past their deadlines – have become the new status quo. This leaves the euro’s bullish momentum needing to transition from headline-driven sentiment to more concrete validation – namely, U.S. macro data – to justify further decoupling from the dollar and renewed refuge in the common currency.

GBP Pound for pound. Sterling has held its own of late, hitting one-month highs against major peers – including USD, EUR, CAD, and AUD. This has been driven by upbeat UK data and a hawkish shift in BoE rate expectations. GBP/EUR broke back above €1.16 and is testing its 50-day moving average for the first time since mid-June. The pair is on track for a third straight weekly gain, up roughly 2% cumulatively. Macro signals point to further upside – real rate differentials and subdued volatility suggest GBP/EUR could be trading closer to €1.18–1.19. But options traders still favor euro strength over the long run. GBP/USD, however, is now trading above all key long-term daily moving averages, reinforcing bullish momentum. With the 14-day RSI neutral and price action strong, the pair could be gearing up for a fresh leg higher. The $1.38 region could be next if yield support holds and sentiment stays firm. The real bout begins with next week’s inflation and retail sales data though – potential knockouts for GBP direction, although dollar dynamics continue driving the overall FX narrative.

CHF Cracks in the haven. From safe haven to short candidate, the Swiss franc is losing ground. Despite being the G10’s second-best performer this year, up around 11% against the dollar, momentum may be fading. US tariffs and the threat of negative rates are chipping away at its appeal. The US has slapped a hefty 39% tariff on Swiss imports, raising concerns over economic growth. Regardless of how the trade dispute unfolds, though, the franc’s status as a safe haven has been marginally compromised. More concerning is the increased likelihood that the Swiss National Bank may take proactive steps to weaken the currency – be it through deeper negative interest rates or direct market intervention. If volatility stays low, CHF looks increasingly vulnerable to shorts against USD, GBP, and EUR. A break above the 0.8151 USD/CHF peak from last month could trigger further upside, especially with a yield advantage of over 400 basis points drawing in carry traders chasing rate differentials.

CAD Fed speculation buoys CAD. The USD/CAD has been remarkably stable over the past two weeks, holding a tight range between 1.382 and 1.372. This period of relative calm, with the pair trading between its 20-day and 100-day moving averages, is a deceptive indicator of the underlying economic reality in Canada. The primary force preventing the Canadian dollar from weakening further is not its own strength, but rather a broad-based softness in the U.S. dollar, which is masking persistent domestic and external pressures on the Loonie. In fact, the CAD is the worst-performing currency against all majors in the last 7 days. Ending the week, the CAD pushed to its highest level of the last two weeks at 1.381, after yields and the dollar reacted on a hotter-than-expected US PPI. The direction of the pair in the coming months will hinge on whether the narrative of a dovish Fed continues to dominate or if Canada’s underlying economic and trade weaknesses begin to assert themselves more forcefully in the market. Next week, Canadian CPI on Tuesday will be the most important macro report.

AUD Jobs surprise gives Aussie a lift, eyes now on sentiment. Australian employment data for July delivered a positive surprise, with the headline number matching expectations at 24.5k and a robust gain in full-time jobs (+60.5k), offsetting a drop in part-time positions. The unemployment rate dipped to 4.2%, suggesting underlying labor market strength, while the participation rate edged down to 67%. This upbeat data lent support to the AUD, but later fell as the USD jumped overnight after hot US PPI numbers. Technically, AUD/USD remains above the 100-day moving average (0.6471) and the key 0.6340-0.6486 support zone, keeping the broader uptrend intact unless a decisive breakdown occurs. Resistance is clustered at 0.6683-0.6722. Focus now shifts to manufacturing and services PMIs as well as Westpac consumer sentiment for further direction.

CNH Weak China data stirs stimulus talk. China’s July activity data fell short across the board, highlighting ongoing economic headwinds. Retail sales growth slowed to 3.7% year-on-year, well below expectations, while industrial production and fixed asset investment also disappointed. The persistent drag from a slumping property sector—property investment contracted 12% year-to-date—underscores fragile domestic demand and mounting pressure on policymakers to deliver further support. In FX, USD/CNH is hovering above key support level of 21-day EMA of 7.1841. The next key resistance lies at 50-day EMA of 7.1879 and 100-day EMA of 7.2023. We expect range bound price action for this pair in the near term. USD/CNH was flat for the week of Aug 11th. Upcoming PBoC loan prime rate announcements will be closely watched for policy signals.

JPY Yen rallies as Japan beats growth forecasts. Japan’s Q2 GDP data outperformed, posting 1% annualized growth driven by strong business investment, despite headwinds from US tariffs. The resilient economy bolsters the case for the Bank of Japan to consider further policy normalization, especially as inflation stays above target. The yen led currency gains for the week of August 11, rising over 0.6% against the dollar. USD/JPY had broke the 21-day EMA of 147.55. For a sustained yen rally, USD/JPY would need to break below 147.21-147.45, with further support at 145.75-145.86. Conversely, the next key resistance for the pair will be 148.52. Market participants are awaiting upcoming trade balance, CPI, and PMI data, which could provide the next catalyst for direction, particularly if inflation surprises to the upside.

MXN Technical bottoming? Since July, the USD/MXN pair has been unable to break below its 2025 low of 18.51, a key technical level. This has signaled a potential bottoming formation and suggests the pair could be consolidating, likely trading within a range between 18.55 and 18.90. The momentum for the Mexican Peso, along with other high-yielding emerging market currencies, appears to be losing steam. The extended “risk-on” sentiment, supported by subdued volatility and a soft dollar, has pushed valuations for many emerging market and Latin American assets to very high levels. After four months of strong performance, investors may now be looking to lock in profits and explore opportunities outside of high-yield currencies, as the carry-appeal weakens. This shift in sentiment is supported by growing concerns about global growth and a recent drop in commodity prices. These factors create a challenging environment for the Mexican Peso to continue appreciating against the U.S. dollar, increasing the likelihood of a sustained period of range-bound trading.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.