- The regional rupture. The US-Israel war on Iran has escalated into a full regional shock with global costs. Markets are now trading the fallout more than the headlines as the crisis enters its seventh day with no sign of resolution.

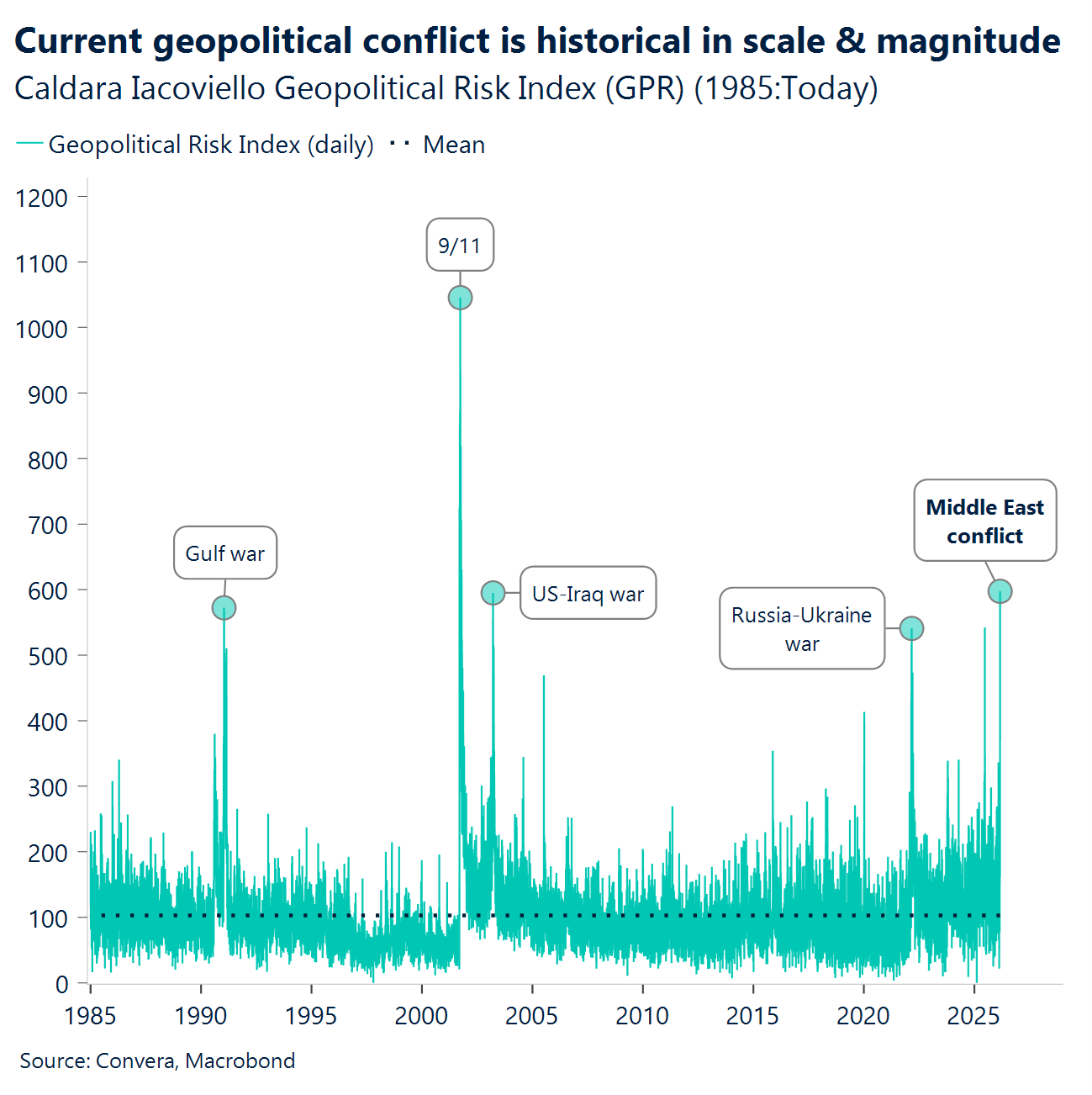

- Risk gauges on red alert. The global geopolitical risk index has hit its highest level since 2001, oil prices are up around 30%, gas prices have doubled, freight rates surging, equities sliding and rate‑cut expectations being priced out as inflation fears rebuild.

- Longer it lasts, harder it hits. For markets, the branching point is stark: does this end in days, weeks, or does it evolve into a drawn‑out regional conflict with no definable endpoint? A prolonged conflict would be a major drag on global trade just as the world was still digesting the tariff‑driven inflation and growth hit.

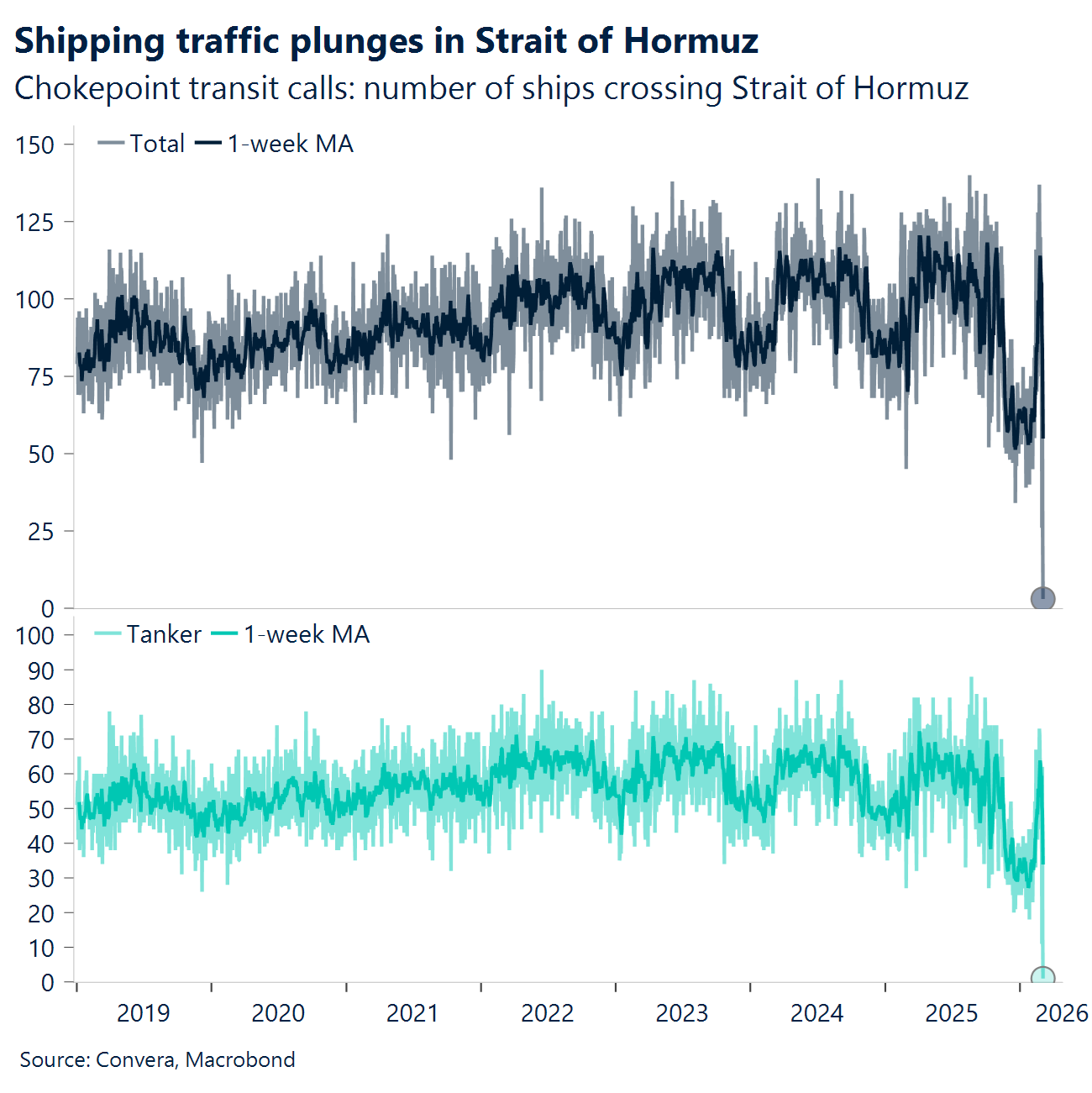

- Chokepoint that chokes markets. Shipping remains at a standstill in the Strait of Hormuz and puts 15–20% of global oil supply at risk, but the larger risk might stem from LNG logistics, drawing uncomfortable parallels with the 2022 energy shock.

- Two levers that matter. Near‑term risk hinges on whether energy prices can retreat if Hormuz reopens, and whether central banks retain the space to cut rates or at least avoid tightening to support the global economic outlook.

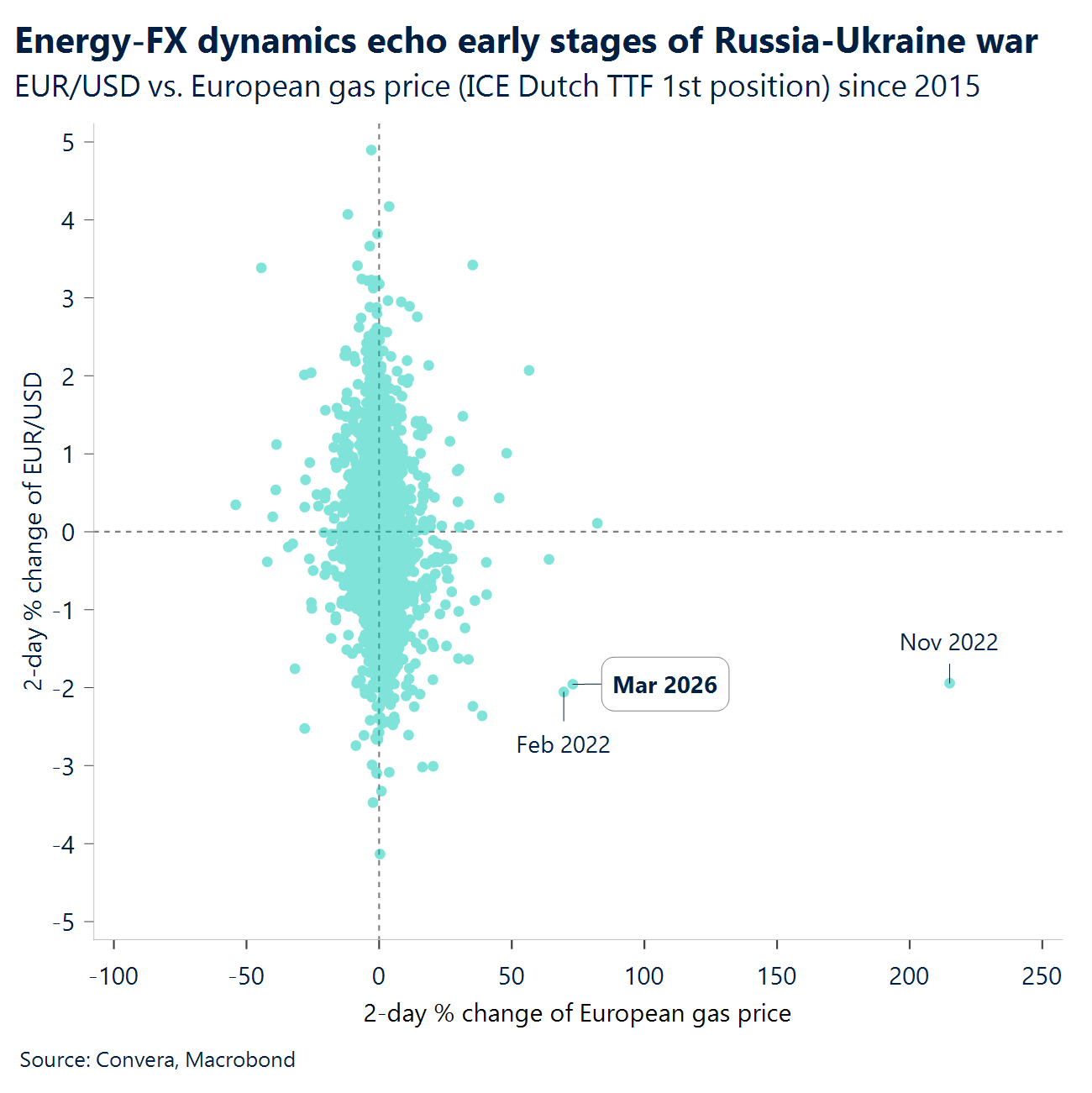

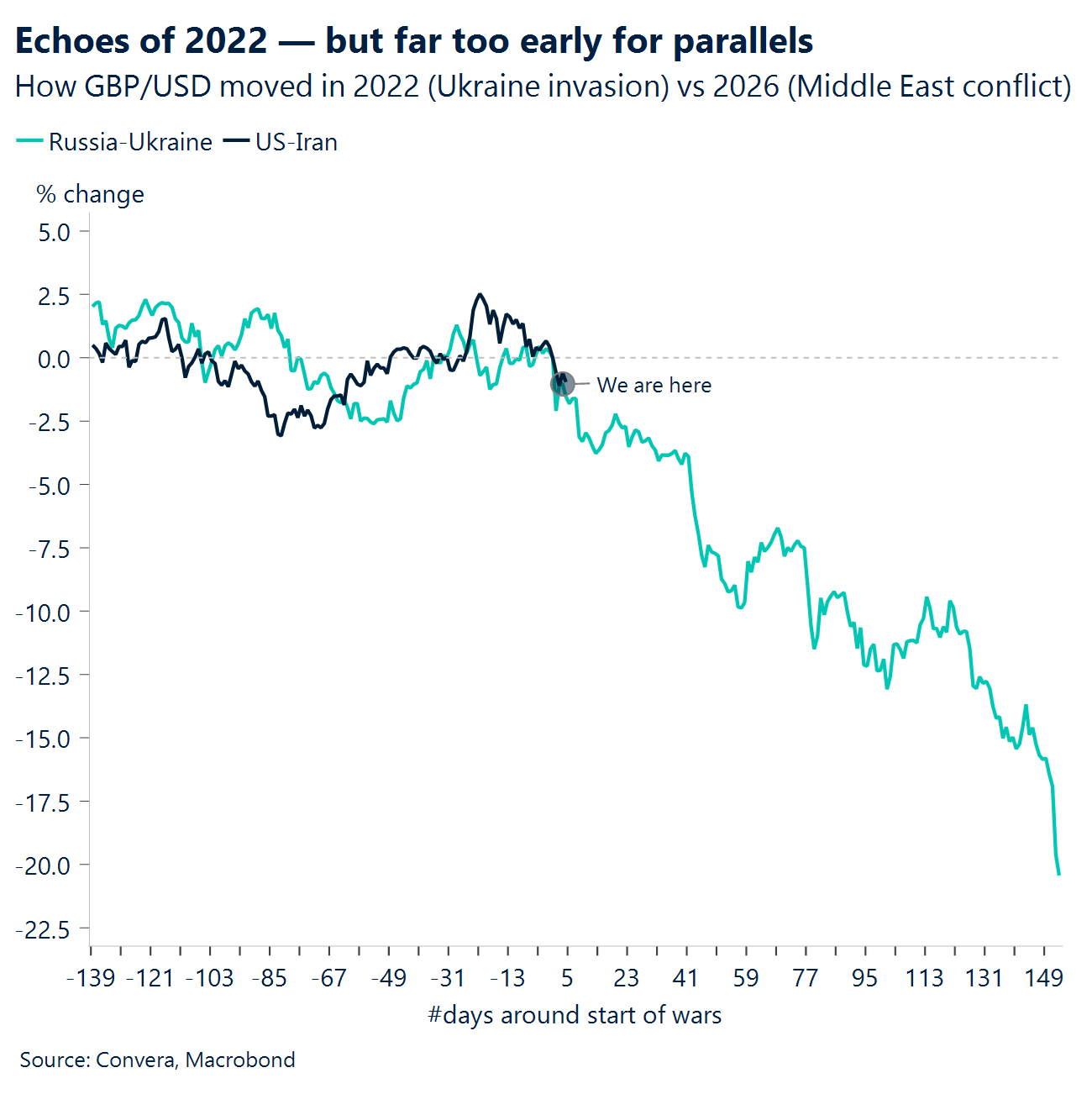

- FX déjà vu. It might be wise to revisit the March 2022 playbook: commodity FX resilience and US energy independence favoring USD strength vs. energy‑importing currencies in Europe and Asia. We’re already seeing early echoes of that pattern.

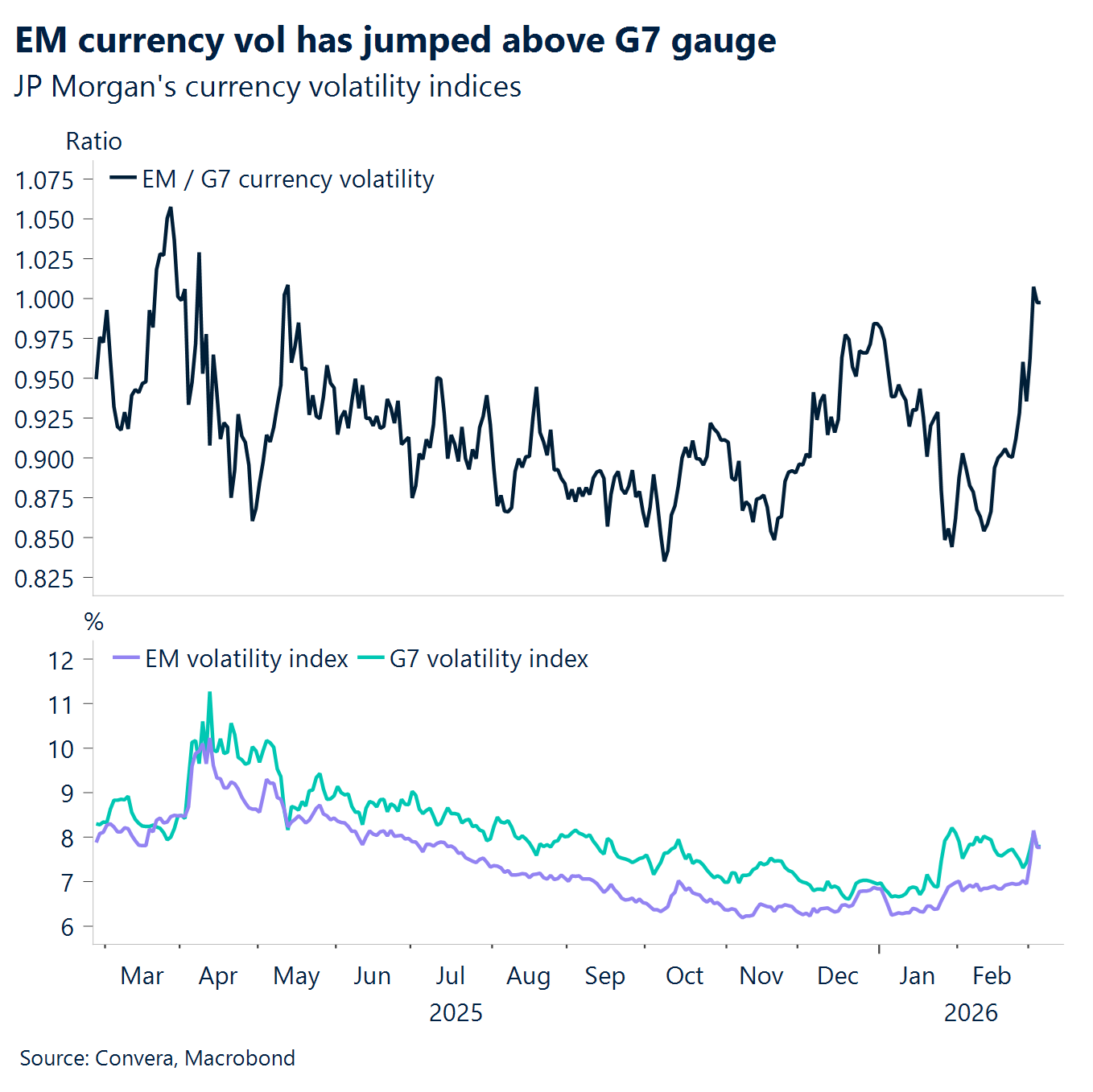

- EM turbulence returns. Emerging‑market FX volatility has jumped above G7 FX levels for the first time since May 2025, fueled by Middle East tensions and spillovers from sharp swings in Asian equities such as the 12% plunge in Korea’s Kospi.

Global Macro

When geopolitics becomes the macro

Game of attrition? Markets remain hypersensitive to headline risk as Brent crude hovers near $84. On the US side, after the confirmed killing of Khomeini, policy calculus still revolves around containing energy‑driven inflation while sustaining operational tempo. On the Iranian side, their response has deteriorated sharply, turning what began as an offensive push that involved neighboring countries into a grind of attrition and interdiction.

Strait of Hormuz. The central uncertainty is whether investors have fully baked in the potential for a stalled diplomatic ‘ramp-off, and continued bottlenecks in the Strait of Hormuz. While the initial shock usually carries the most weight, the trajectory from here relies on three pivotal factors: the steady decline of Tehran’s offensive reach, the resolve of neighboring states to keep Iran sidelined, and the effectiveness of US and its allies’ efforts to shield cargo and prevent a spike in pump prices.

Macro largely ignored. Plenty of global macro data has been released this week, all has been largely ignored, as markets fate is tied to headline risk coming from the Middle-East. Worth noting US manufacturing sector outperforming expectations at 52.6, Service ISM print which smashed expectations, the stagflation narrative was crushed, as the ISM’s Prices Paid index tumbled to an 11-month low. Meanwhile, China’s economy showed signs of seasonal slowing with its Manufacturing PMI dipping to 49.0, and Europe’s inflation edged up slightly to 1.9%.

Surprisingly weak NFP. The underlying employment numbers paint a weak picture of the labor market and make the positive January data look like a total outlier. Total nonfarm payrolls contracted by 92,000 in February, and the gloomy outlook was compounded by downward revisions that subtracted another 69,000 jobs from the prior two months. This combination of a contracting labor market and stubborn inflation pressures from higher energy prices leaves the Federal Reserve in a very tough spot.

Week ahead

Geopolitics to steal the spotlight

Middle East tensions keep markets on edge. The conflict in the Middle East will continue to dominate headlines, with no meaningful signs of de‑escalation as both sides keep exchanging fire. While still early in the conflict, economic risks are multiplying as the Strait of Hormuz remains close to a standstill, injecting more bullish fuel into energy prices.

US inflation double-header. Both CPI and the Personal Consumption Expenditures deflator are out next week, offering a fuller picture of US price dynamics for the first months of 2026, February and January respectively. The latter is the Fed’s preferred gauge as it feeds directly into the personal consumption expenditure component of GDP. After the behemoth surge in PPI in December, we will keep monitoring the consumer price landscape to gauge pass‑through in the months ahead.

JOLTS adds another data point. January’s JOLTS report is also due. After upbeat ADP and NFP February prints last week, the one‑month lag makes this release less market‑moving, but at a time when the Fed stresses stabilisation in the labour market, it remains important to validate the trend across time and across sources to ensure a healthier stabilisation pattern.

UK growth pulse. In the UK, we will start to see how growth has fared so far this year, with monthly GDP and industrial production figures. Late‑2025 data showed a pick‑up in activity, and next week’s releases will indicate whether that momentum is continuing as businesses begin to breathe as the effects from the Autumn 2024 tax hikes have been largely absorbed.

All times are in GMT.

FX views

Energy shock triggers FX reset

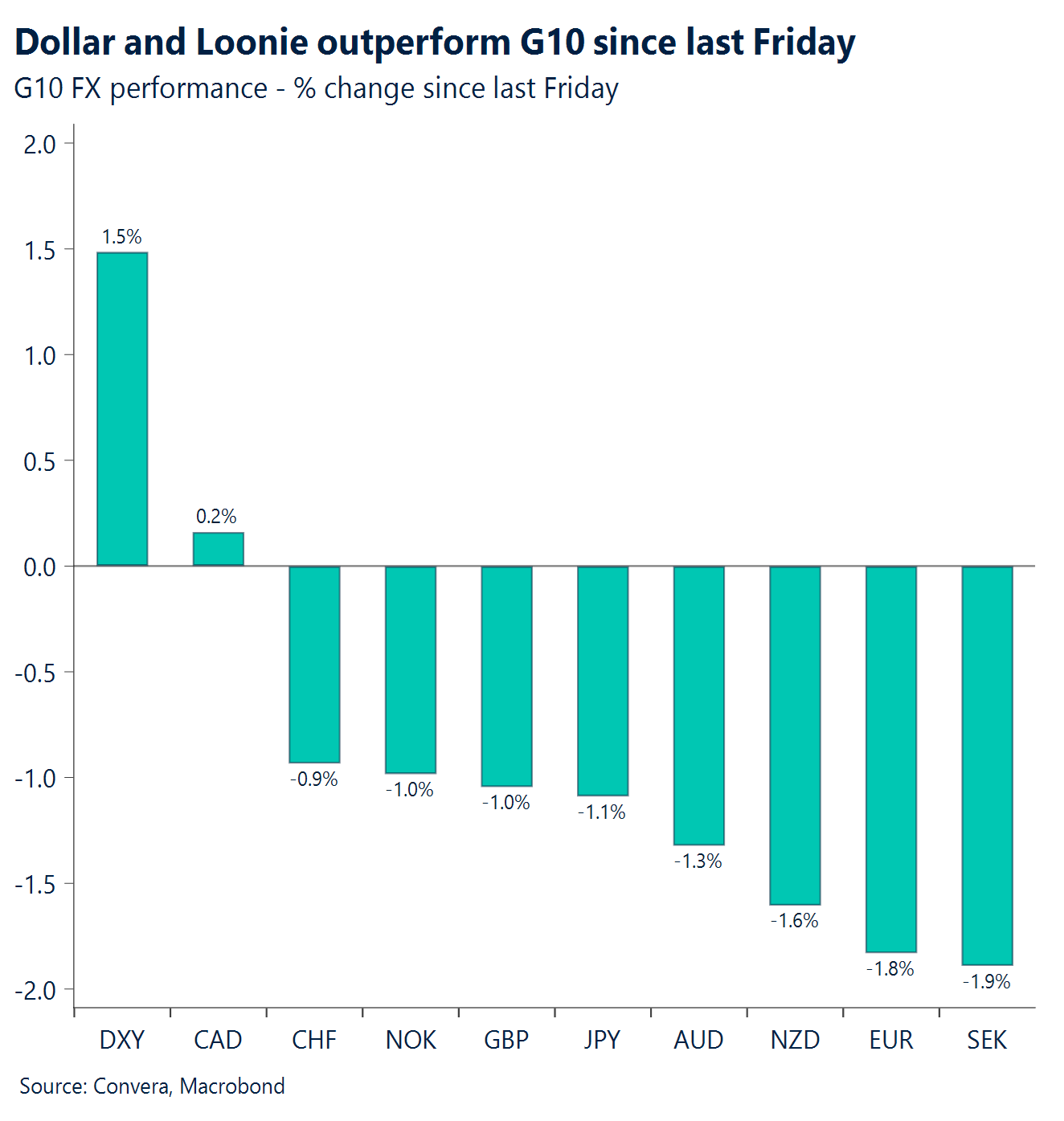

USD War dollar. The US dollar index has surged to its highest level since November as geopolitical escalation collides with a renewed energy shock, overshadowing the recent dent to USD sentiment caused by Trump’s erratic policy agenda. Oil’s jump toward $90 per barrel is dollar‑positive: the US is now a net oil exporter, and with most global crude priced in USD, higher prices mechanically lift the dollar. That strength then amplifies the global supply shock rather than cushioning it. A firmer USD raises local‑currency energy costs abroad, tightens global financial conditions and deepens stagflation risks for importers. Improving US terms of trade, haven flows, macro divergence and risk‑off tightening all reinforce the cycle, keeping the dollar well supported. Without a genuine political breakthrough, the dollar is unlikely to relinquish its strength anytime soon. True, the shock US jobs report knocked yields and USD lower, but the geopolitical story continues to overshadow.

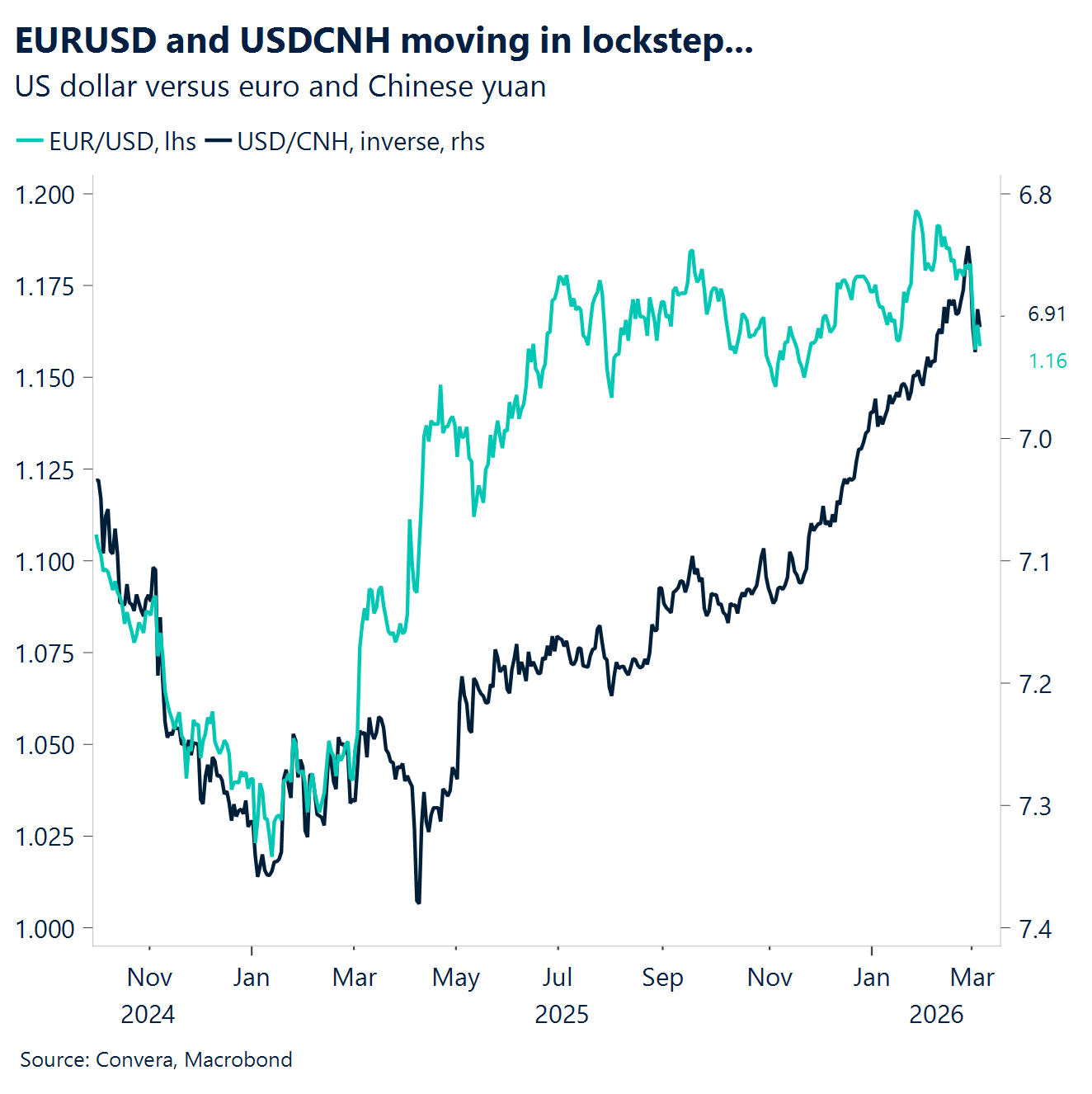

EUR Hit by worsening terms of trade. Traders are the most bearish about the euro’s near-term prospects since 2022 as the Middle East conflict triggers an energy‑market shock that looks uncomfortably reminiscent of the early days of Russia’s invasion of Ukraine. As a net oil importer, the eurozone’s terms of trade weaken – the region pays more for energy while export prices do not rise in tandem, stoking stagflation fears. ECB officials have urged caution against drawing hasty conclusions about the conflict’s material impact on economic performance, arguing it is too early to revise inflation forecasts higher on the back of rising oil and natural gas prices. EUR/USD has slipped below all key moving averages and now hovers around the psychologically important 1.16 level. It has been breached for three consecutive sessions but ultimately closed above it each time, suggesting sellers remain hesitant to push more aggressively below 1.16 while markets await clarity on the duration and scale of the conflict. A decisive close beneath that level would put 1.15 in focus.

GBP Caught in the cross-currents. The renewed surge in oil and gas prices has revived classic petro‑dollar dynamics, dragging GBP/USD back to 1.33, and hitting its weakest level since December. There are early hints that downside momentum is slowing on the charts, but nothing yet that resembles a durable base. The medium‑term risk is clear: a sustained energy shock that erodes the UK’s terms of trade — the same channel that drove the 20% GBP/USD slide in 2022. We’re not drawing a direct parallel, but the vulnerability is back on the radar. Against the euro, however, sterling is showing relative resilience. GBP/EUR has pushed above 1.15, up more than 0.8% on the week and trading near a one‑month high. Momentum has improved: the pair has cleared its 50‑day moving average and the daily RSI is rising through 55, signalling building upside pressure. The driver is the rates channel. UK gilt yields have risen more sharply than their European counterparts as markets pare back expectations for Bank of England easing due to renewed inflation fears. This provides GBP/EUR a short‑term yield advantage even as both economies face similar energy‑related headwinds.

CHF Less compelling in current crisis. The SNB sharpened its warnings on currency strength, signalling it is increasingly prepared to intervene to prevent further appreciation. That shift matters because it effectively places a policy ceiling on CHF at a time when geopolitical tensions would normally boost haven demand. EUR/CHF reflected this dynamic clearly – rising even as global risk sentiment would typically favour the franc. The SNB’s comments come after a period of exceptional franc resilience. CHF has gained nearly 3% against the euro this year, with the cross hovering near levels last seen outside the brief 2015 spike. The currency has been the preferred haven over the past year as investors questioned US policy consistency and worried about Japan’s debt dynamics. But the franc carries its own vulnerabilities. Heavy reliance on imported energy exposes Switzerland to external price shocks, and the SNB’s explicit intervention stance limits the upside investors can expect in periods of stress.

CAD Energy trade. Since the first strikes on Iran, a significant split has emerged in the currency markets driven largely by energy. While the US dollar is outperforming even traditional safe havens, commodity-linked currencies like the Canadian dollar have remained resilient. This has essentially divided the market into oil exporters versus oil importers, with exporters showing clear strength even as the US dollar dominates. Because of this shift, the Loonie is beating the European majors, pushing both EUR/CAD and GBP/CAD to their lowest levels since July of last year. This market behavior is also hitting historical extremes. Before the last week, there have been only a few days in the last 25 years (2008) where gold fell more than 5%, the S&P 500 dropped more than 2%, and the US dollar index rose more than 1% simultaneously. When these three moves happen at once, it indicates a massive, rare scramble for cash and a total flight from risk. The fact that the Canadian dollar is holding its ground in this environment highlights just how much the market is currently valuing energy independence.

AUD RBA Bullock signals hawkish tilt. The AUD has been mainly supported in in the post-Iran sell-off with its energy exposure providing some support. The Aussie has gained solidly versus European and Asian FX, while AUD/USD remained broadly in its 0.7000 to 0.7150 range. RBA governor Bullock struck a firmer tone, warning that demand in the economy is running hotter than supply and that labour markets remain tight. She added that it’s unclear whether current financial conditions are restrictive enough to bring inflation back to target in time. The key question now is timing: will the RBA wait until May to act, or move sooner as oil-driven price pressures risk pushing inflation higher? Current market pricing suggests only minimal odds of a March move. Markets are leaning toward a May rate hike. AUDUSD is trading about 1.5% below its recent high of 0.7147 (Feb 12). Next support sits at the 50‑day EMA of 0.6938, followed by the 100‑day EMA at 0.6811. Market participants will keep an eye on upcoming NAB business confidence and building approvals.

CNH China PMIs split as private survey shines. China’s official manufacturing PMI slipped to 49 in February, weaker than the expected 49.2 and down from 49.3 previously. New orders fell to 48.6, while export orders dropped further to 45. Non‑manufacturing PMI covering construction and services came in at 49.5, missing forecasts of 49.7. By contrast, the private RatingDog survey painted a brighter picture. Manufacturing PMI surged to 52.1, well above expectations of 50.1, while services PMI jumped to 56.7 versus a steady 52.3 forecast. RatingDog noted that manufacturing is likely to maintain moderate expansion in the short term. The gap between the official and private surveys underscores uneven momentum across China’s economy. Meanwhile, the USDCNH has rebounded 1.1% from its recent low of 6.8267 on February 26, boosted by the safe-haven rebound in the US dollar. The next resistance level is at 6.9373, near the 50‑day moving average, followed by 100-day EMA of 6.9916. Traders will keep an eye on the upcoming CPI, PPI and trade balance..

JPY BoJ downplays impact of past hikes. The Japanese yen was mostly weaker, with USD/JPY higher, as financial markets favoured safe havens like the US dollar. By contract, the JPY has underperformed due to worries about its status as a massive oil importer. Bank of Japan Deputy Governor Ryozo Himino said recent rate hikes have had only limited impact so far. He noted that underlying inflation is rising steadily, though he cannot confirm the price trend has reached 2%. USD/JPY sits 1.2% below its Jan 14 high of 159.45. Support levels are at the 50-day EMA of 155.77 and the 100-day EMA of 154.77. With the pair pulling back, dollar buyers may see room to step in. Traders are still pricing in a rate hike in July 2026. Market participants will keep an eye on the upcoming household spending, GDP, current account.

MXN Hurt by flight-to-quality. Emerging market currencies initially kicked off the year with significant strength, driven by aggressive portfolio diversification and improved terms of trade for commodity exporters. Latin America, in particular, attracted a massive surge of inflows in January that sparked outsized moves in the Brazilian and Mexican equity markets. While these high-yield destinations were once solidified as compelling targets for global capital due to their commodity exposure and proximity to the U.S. market, the narrative has shifted as geopolitical volatility triggers a move away from risk.

The Mexican peso has hit a six-week low, weakening toward 17.7 per dollar as global investors shift toward safer assets. This dip follows a record $6.48 billion trade deficit in January, largely driven by a sharp 33.5% drop in oil exports and a 9% decline in auto shipments to the US market. Essentially, the energy and industrial sectors, traditionally Mexico’s biggest economic engines, are currently facing a bit of a perfect storm, turning previous strengths into temporary hurdles.

BRL Vulnerable in sentiment shift. The rising dollar creates one of the most challenging backdrops for emerging market assets seen in the past year, as the greenback’s safe-haven status is now compounded by its tendency to amplify energy shocks. A stronger dollar inherently tightens global financial conditions, pressuring balance sheets burdened with dollar-denominated debt and weighing on cross-border lending and trade.

The Brazilian real is taking a hit again, sliding past 5.26 per dollar and wiping out its recent gains. Between the Middle East conflict driving up oil prices and a global rush toward the “safety” of the US dollar, the Real is feeling the squeeze. At home, things are a bit of a balancing act because inflation hit 4.44% annually, which is uncomfortably close to the 4.5% limit. Despite that heat, the Central Bank is still expected to trim the 15% Selic rate by 0.25% to 0.50% at the March 18th meeting, a move that combined with fresh polls showing a dead heat for the upcoming election has investors feeling pretty jumpy.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.