- Global equity markets moved higher and oil tumbled, but FX was more muted as markets reacted to the US–Iran peace deal.

- The deal was announced on Sunday 14 June, President Trump’s 80th birthday, with most of the move captured early in the week. The memorandum of understanding was signed electronically mid-week. A proposed signing ceremony on Friday in Geneva was cancelled.

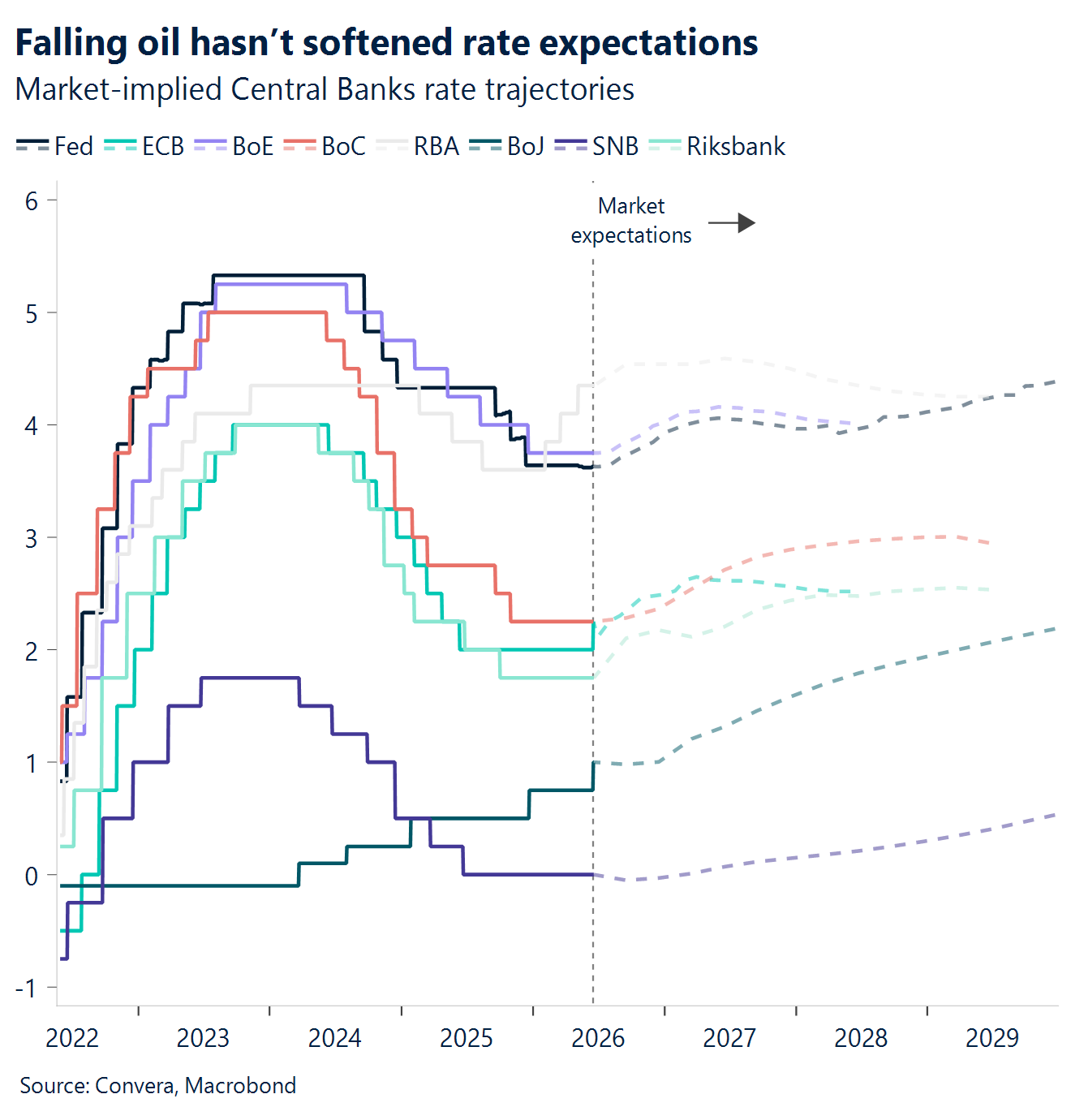

- In his highly anticipated debut, Federal Chair Kevin Warsh kept rates unchanged at 3.5%–3.75%. But the bigger story was the statement — it was materially shorter than previous releases. That likely reflects Warsh’s long-standing scepticism toward heavy forward guidance. Markets are already bracing for a broader shift in how the Fed communicates.

- The Bank of Japan raised its policy rate by 0.25% to 1%, the highest since 1995, in a 7–1 vote. The move signals a clear shift away from ultra-loose policy as price pressures persist and energy costs remain elevated following recent Middle East tensions. The Japanese yen weakened with the USD/JPY climbing further above 160.00

- The Bank of England left rates unchanged at 3.75% yesterday. The vote split was 7–2, with Megan Greene and Huw Pill voting for a hike, in line with expectations. The GBP fell.

- The RBA held the cash rate at 4.35% in a unanimous decision. The statement carried a slightly firm tone, signalling policymakers could still lift rates if needed.

Global Macro

BoJ hikes while hawkish holds dominate

Hawkish holds. A central-bank heavy week. The Fed held rates at 3.50%–3.75%, as expected, but removed the earlier easing bias and shifted the tone in a more hawkish direction. At the same time, the RBA held at 4.35%, the Riksbank held at 1.75%, the SNB held at 0.00%, Norges Bank held at 4.25%, and the BoE held at 3.75%—all in line with expectations. The difference is in the tone: the Fed, RBA, Riksbank, Norges, and BoE all left the door open to further tightening if inflation persists, while the SNB remained the clear outlier on the dovish side.

BoJ hikes. The Bank of Japan raised rates to 1.00% from 0.75%, exactly in line with expectations, taking policy to its highest level since 1995. The BoJ flagged the risk of inflation overshooting target and signalled that further tightening remains possible, making it the sole outright hiker among the major central banks this week.

US beats. US retail sales rose 0.9% m/m vs 0.4% expected, while ex-auto sales climbed 0.8% vs 0.3% expected, a strong upside surprise that reinforced the idea that the US consumer is holding up. Industrial production was softer at 0.1% m/m vs 0.2% expected, but capacity utilization printed 76.2% vs 76.2% expected, so the growth signal was softer at the margin. Elsewhere in the US data flow, the Empire State index fell to 5.7 vs 13.2 expected, which is a reminder that regional manufacturing still looks more uneven than consumer demand.

China weakens. China’s May retail sales fell 0.6% y/y vs 0.0% expected, a clear consumption miss and the first annual decline since December 2022. Industrial production was the only offset, rising 4.5% y/y vs 4.3% expected, so the broad message stayed the same: China remains a two-speed economy with soft domestic demand and firmer factory output.

Week ahead

Sentiment check

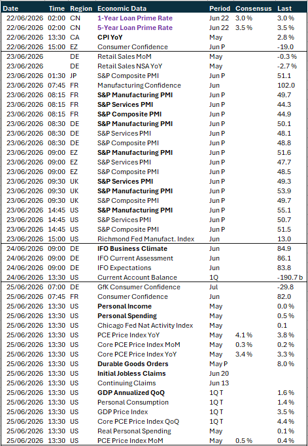

- PMIs testing the stagflation narrative. Preliminary releases of June’s S&P Global PMIs are due next week across major economies, including the eurozone, UK and US. Recent prints have pointed to rising stagflation risks, with activity momentum weakening as price pressures continue to build. The recently announced peace deal should help ease some of this divergence, and upcoming releases may begin to reflect that shift, particularly given the pullback in oil prices that had already started ahead of the announcement.

- Policy gauge in focus. The May PCE price index is also due. While it remains the Fed’s preferred gauge, Kevin Warsh’s leadership and his stated intention to reshape the policy framework have introduced discussion around alternative measures. He has frequently referenced trimmed mean inflation as a potential complement, though any transition would likely unfold gradually. In the meantime, PCE retains strong market relevance given the breadth of its price coverage.

- Resilient but tested. Markets will also turn to May personal spending. Following a modest 0.1% inflation-adjusted increase in April, real consumption moderated as rising prices continue to erode purchasing power. The US consumer remains altogether resilient, however. And with the geopolitical backdrop improving, upcoming releases may point to consumer demand beginning to regain momentum.

All times in BST

FX views

Hawkish tilt defines Warsh’s Fed debut

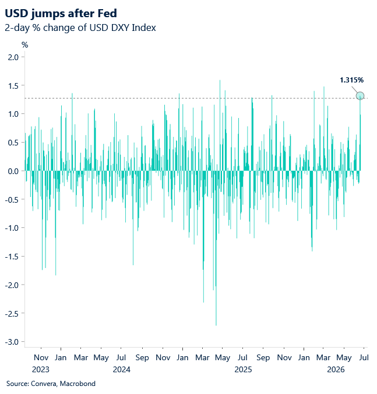

USD Dollar firms as Fed hawkishness offsets de-escalation. The dollar gained strongly into the end of the week as the US and Iran finalised an agreement to end the war and reopen the Strait of Hormuz. The move higher was driven primarily by a hawkish Fed, with half of the FOMC now seeing at least one rate hike at some point this year. The dollar index reclaimed the 100 handle and has pushed past resistance at 100.70. Lower oil prices, now close to their lowest levels since March, failed to weigh on the dollar more meaningfully. The broader risk balance remains asymmetric given the time investors have already had to price in a peace outcome between the US and Iran. On the Fed, solid macro momentum points toward a more hawkish bias. Even so, markets had been looking for confirmation from new chair Kevin Warsh amid lingering concerns over his sensitivity to political pressure for lower rates under President Trump. From here, the scope for further meaningful dollar upside appears limited. Continued de-escalation should extend the decline in oil prices and, in turn, act as a constraint on further dollar strength.

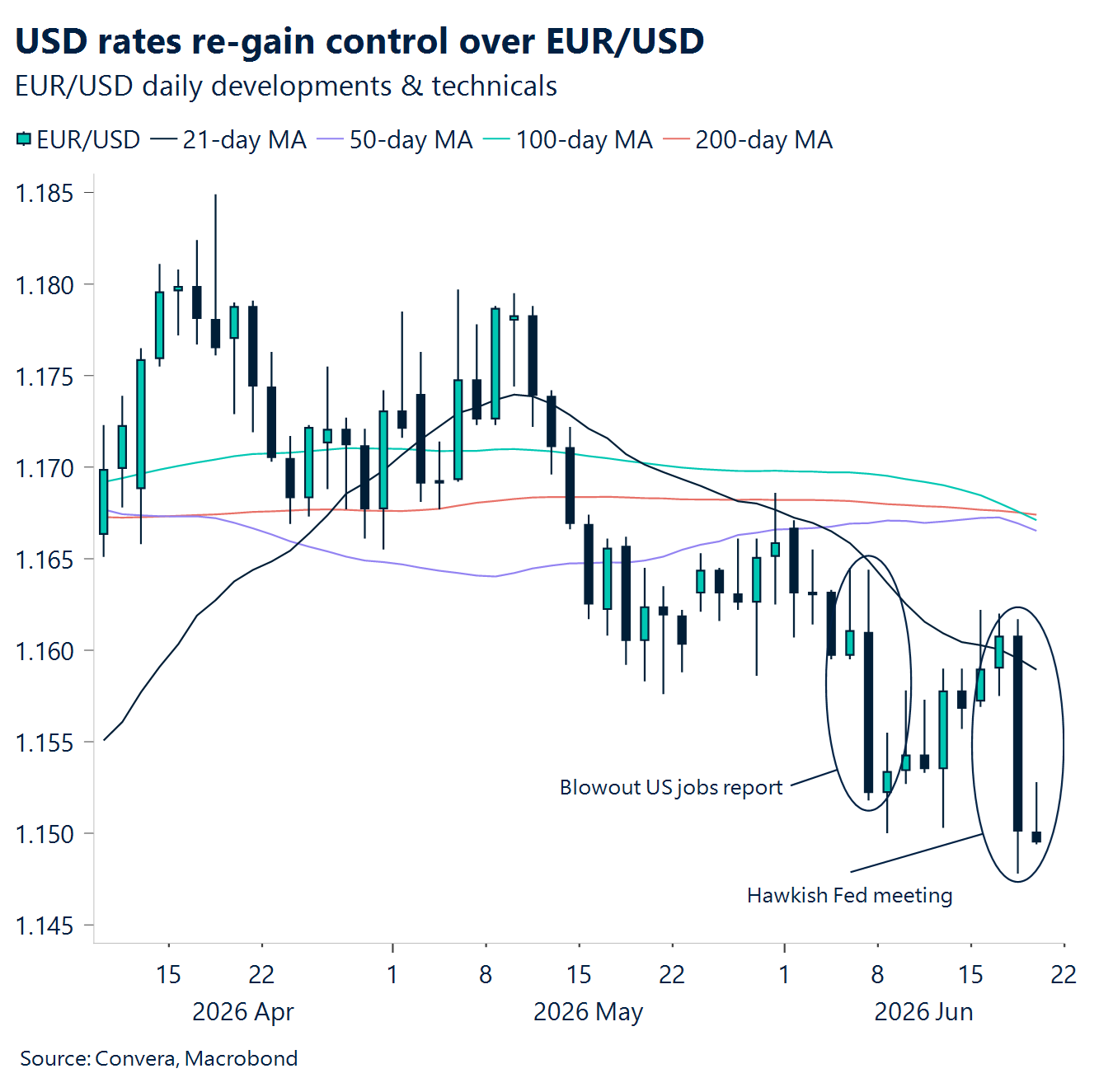

EUR Nearing one-year lows. EUR/USD came under pressure this week following a hawkish Fed. The pair had been recovering toward 1.16 after dropping to the 1.15 area on the back of a strong jobs report a couple of weeks ago, but the latest policy meeting reinforced the Fed’s hawkish bias and pushed the pair back toward recent lows. These moves highlight the renewed influence of rate differentials on FX, after a period in which geopolitics had been the dominant driver. We see scope for a partial retracement of this week’s losses as de-escalation momentum weighs on the dollar. However, with markets having largely absorbed recent geopolitical developments and now turning their focus to the reopening of the Strait of Hormuz, alongside a more convincing, data-backed hawkish stance from the Fed, we are not yet calling for a sustained move back above 1.16.

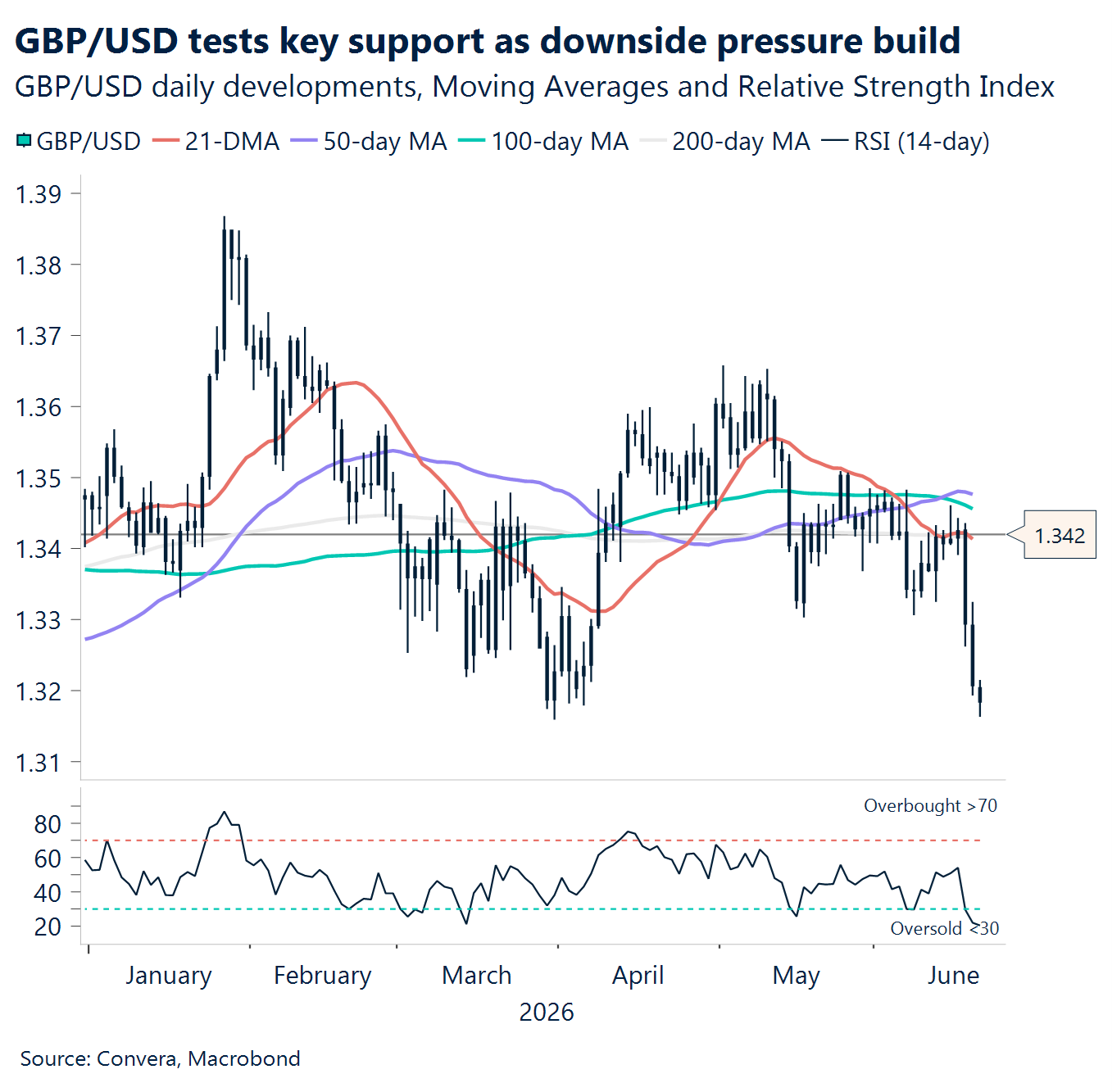

GBP BOE still sees inflation upside. The BoE kept policy rates on hold at its June meeting and acknowledged May inflation slowed to 2.8% but still expects a pickup later this year, softening its tone slightly on persistent price pressure while keeping concerns alive. It isn’t reading the May miss as a decisive dovish turn, though its tone on expectations eased a touch. Inflation is now seen a little under 3% in Q3 and just over 3.25% in Q4 — above target, but lower than April’s fears. In politics, sterling now has a fresh domestic risk to watch after Andy Burnham won the Makerfield by-election, sending him to parliament and setting up a potential Labour leadership challenge to PM Starmer. GBP/USD dropped about 1.7% over the week, weighed by broad dollar strength. Risk sentiment weakened further after US–Iran talks were postponed, adding to downside pressure on GBP/USD via a firmer dollar. The pair needs a break above the 21-day EMA (1.3372) to regain traction, with the 50-day EMA (1.3416) the next hurdle. Without that, rallies may fade quickly. On the downside, 1.3100 remains key support and a break would expose deeper losses. Upcoming PMIs will be key for near-term direction.

CHF USD/CHF climbs to seven-month highs as SNB stays soft. The SNB maintained a cautious stance — rates on hold with inflation still subdued, contrasting with firmer signals elsewhere. This policy gap continues to weigh on the franc. The franc stays an attractive funding currency, keeping a bid under USD/CHF. USD/CHF rose about 1.6% in the week of June 15 and now trades at 7-month highs. Momentum remains positive while the pair holds above the 21-day EMA (0.7947). A move through 0.8100 would extend gains further. On pullbacks, support sits at the 21-day EMA (0.7947), followed by 50-day EMA (0.7902) and 100-day EMA (0.7891). With conditions still favouring the dollar, USD/CHF may stay bid into upcoming ZEW data and SNB updates.

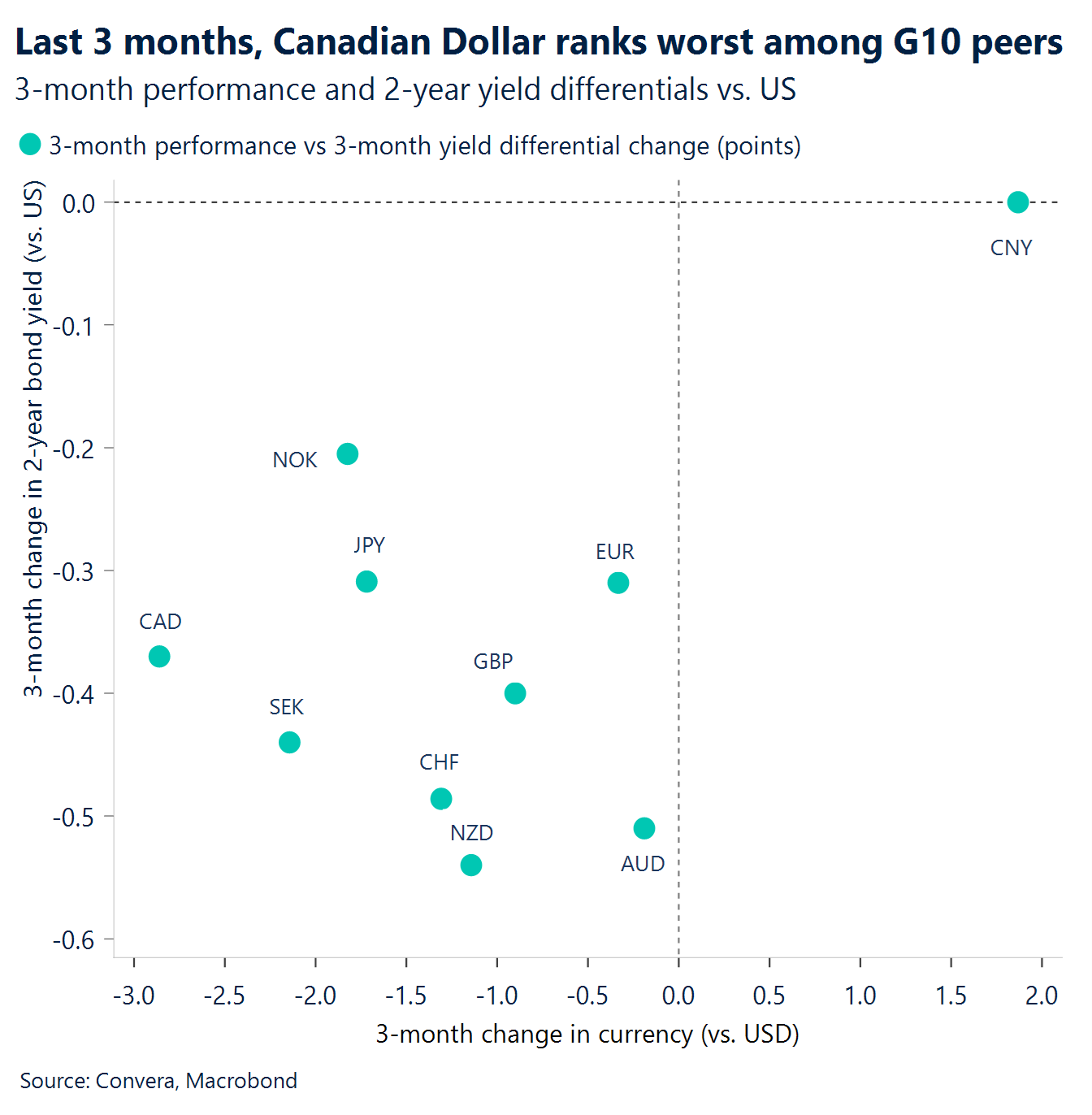

CAD Pressure continues. USD/CAD is being pushed higher by a broad mix of forces, with widening rate spreads, softer Canadian fundamentals, bearish Loonie positioning and renewed trade noise all leaning the same way. The Fed’s June decision removed the earlier cutting bias and pushed markets to price a more hawkish path, while the US-Canada 2-year spread widened to 137 basis points, the widest since May 2025, which keeps the rate advantage firmly with the greenback. At the same time, traders have largely looked past the drop in oil, as markets focus on yield differentials and renewed trade noise, including Trump’s fresh skepticism toward a new CUSMA deal. Futures positioning has also turned largely bearish for the Loonie. Canada’s own backdrop is not helping much either: the economy still looks soft despite the stronger May jobs print, and the BoC’s hold at 2.25%, which feels like old news reasserts the divergence with Fed pricing. Technicals show a clean upside breakout that looks overstretched. USD/CAD is trading around 1.414, above the 20-day moving average at 1.391, the 50-day at 1.378, the 100-day at 1.374, and the 200-day at 1.382, which confirms the broad bullish alignment. The pair cleared the 1.40 handle with speed and is now pressing into the 1.4140–1.4200 area, which leaves little resistance before the highs from spring 2025. On the downside, first support now comes in at 1.40, followed by the 20-day average near 1.3915.

AUD RBA keeps hike option alive. The RBA held the cash rate at 4.35% in a unanimous decision and kept a clear willingness to act if data demands. It said growth is cooling as expected and policy is well placed to adjust, while sticking to its goals of price stability and full employment. AUD/USD fell about 1% in the week of June 15 as a firmer dollar capped gains. Fresh delays in US–Iran talks and renewed Middle East tensions added to risk aversion, reinforcing downside pressure on AUD/USD. The pair trades near 1-week lows and sits ~4% below its 6 May high (0.7278). Resistance stands at the 100-day EMA (0.7038) ahead of the 21-day EMA (0.7077). Failure to reclaim these keeps pressure on 0.6900 support. AUD/EUR, AUD/GBP and AUD/NZD sit at 1-, 2- and 3-week highs respectively, showing mixed cross strength. We’re watching the upcoming employment change and unemployment rate prints.

CNH USD/CNH pushes to more than three-week highs. The PBoC signalled it will refine how it manages short-term rates, hinting at a shift from the seven-day reverse repo toward an overnight anchor. It also flagged heavier use of short-term repo tools set around the 7-day rate. USD/CNH trades around 0.6% above its 17 June low (6.7539) and has climbed to more than three-week highs, driven by broader dollar strength. The pair needs to clear the 50-day EMA (6.8037) to sustain upward momentum. A break higher would open the 100-day EMA (6.8506), reinforcing the bid. On dips, support near 6.7539 remains firm. With policy differences still in play, USD/CNH bias stays tilted higher into upcoming loan prime rate fixes.

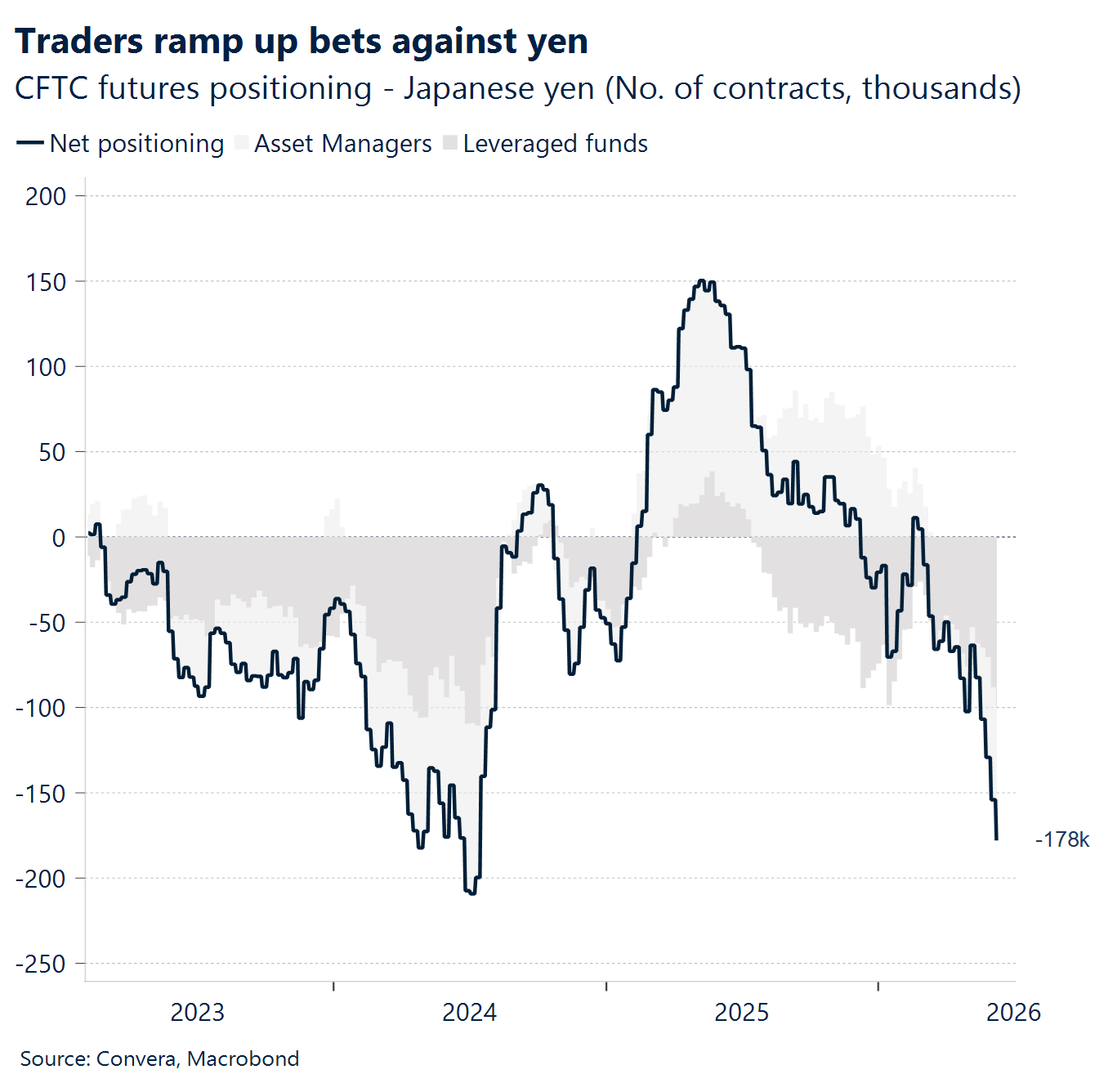

JPY USD/JPY holds firm near four-decade highs. The BoJ lifted rates by 25bp to 1% in a 7–1 vote, marking a clear move away from ultra-loose policy as price pressures persist. With Governor Ueda away, Deputy Governor Uchida will guide near-term messaging. The question is whether rising business costs feed more broadly into consumer prices and shape the rate path from here. USD/JPY holds above 160 and trades close to 40-year highs, supported by strong dollar demand post-Fed meeting despite the BoJ move. The pair sits just below resistance at 161.81 (18 June high). A break would confirm further upside. On the downside, the 21-day EMA (160.10) offers initial support, followed by the 50-day EMA (159.34). As long as these levels hold, dips may attract USD buyers. Upcoming services PMI and Tokyo core CPI will test whether USD/JPY extends higher, with intervention risks in the background.

MXN Carry challenged. The USD/MXN has edged higher, though the move resembles a tactical test. Upward pressure is primarily driven by a hawkish turn from the Federal Reserve at its June meeting, which provided fresh momentum for the greenback. Conversely, Mexico’s domestic backdrop remains stable; May inflation slowed to 3.94% year-on-year, while core inflation eased to 4.19%. This deceleration justifies Banxico holding interest rates steady at 6.50%, though it offers the peso only partial insulation from broad dollar strength. Technically, spot at 17.37 sits just above the 20-day (17.33) and 50-day (17.32) moving averages. However, it remains capped by the 100-day (17.43) and sits well below the 200-day (17.81). While the short-term bias has firmed, the broader range remains intact. Initial resistance is seen at 17.43–17.45, with a more significant cap at 17.56, which has held since April. Support rests near 17.33 and 17.20. Sub-17.56, the price action signals a corrective rebound within a range rather than a structural trend reversal.

BRL Real reverses. The USD/BRL has moved higher as markets digest a challenging domestic mix. The central bank cut the Selic rate by 25 basis points to 14.25% but paired the decision with hawkish guidance and a downgraded inflation outlook. This combination clouded investor sentiment; the immediate policy easing sits uncomfortably alongside rhetoric pointing toward an extended pause or potential hikes ahead. Pressure on the real is compounding politically as Flávio Bolsonaro’s market-friendly candidacy falters in the polls, reducing expectations for a fiscal policy reset in 2026. The real retains a roughly 6% year-to-date gain against the dollar, that buffer is eroding. Technically, the short-term bias for USD/BRL has turned constructive. Spot at 5.176 has cleared the 20-day (5.08), 50-day (5.02), and 100-day (5.12) moving averages, confirming that upside momentum has broadened since the May lows. Initial resistance is pegged near 5.20, above which the 200-day moving average at 5.25 comes into play. Conversely, support rests at 5.12, followed by 5.08 and 5.02.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.