- Few Fed cuts. Economic uncertainty is rising as the Fed monitors Trump’s policies on trade, immigration, and fiscal spending. While Atlanta Fed President Bostic expects two rate cuts in 2025, markets now anticipate less than one.

- ECB remains cautious. Eurozone consumer confidence improved, driven by expectations of continued ECB rate cuts. However, geopolitical tensions in Germany and Ukraine add uncertainty

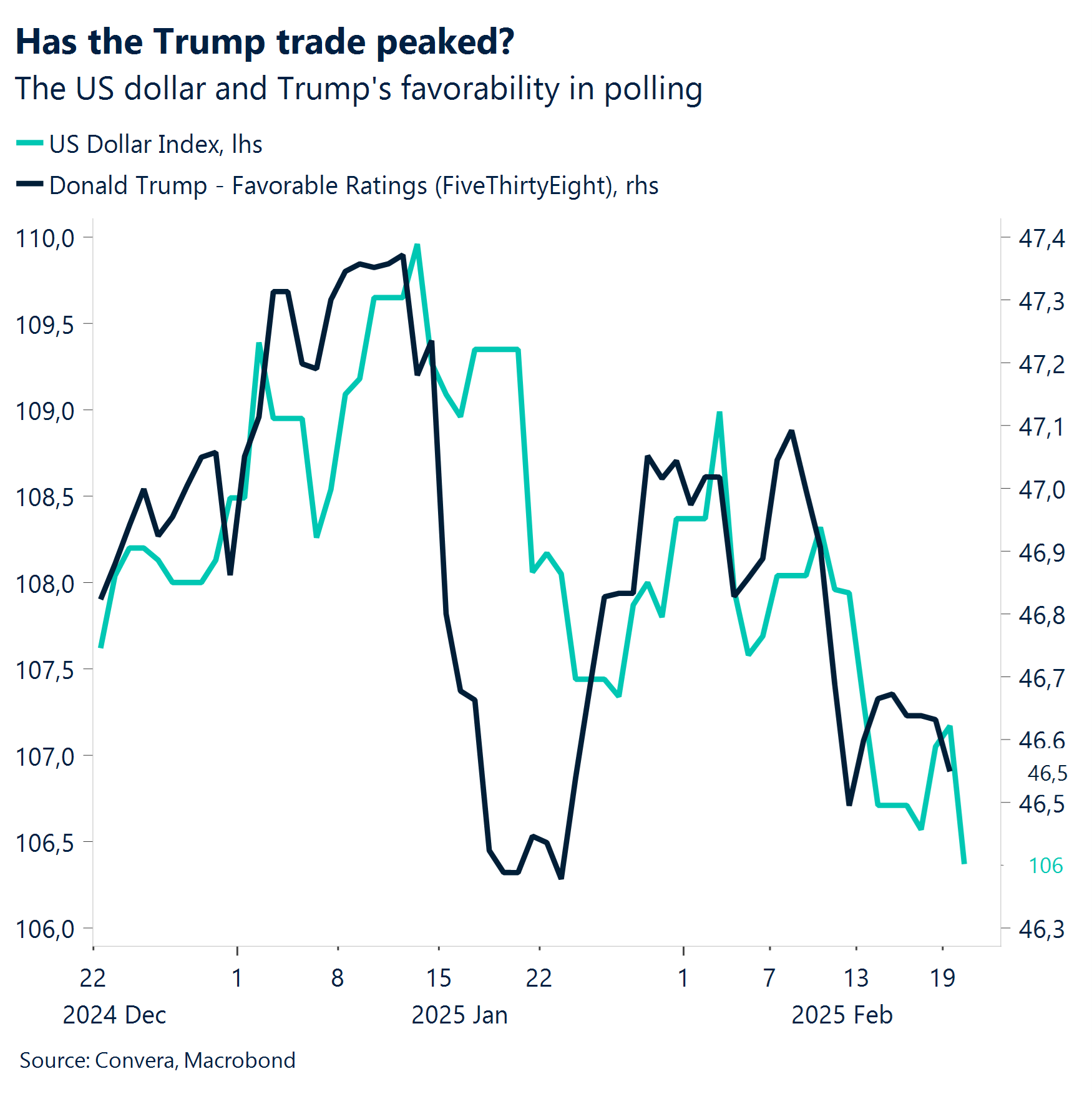

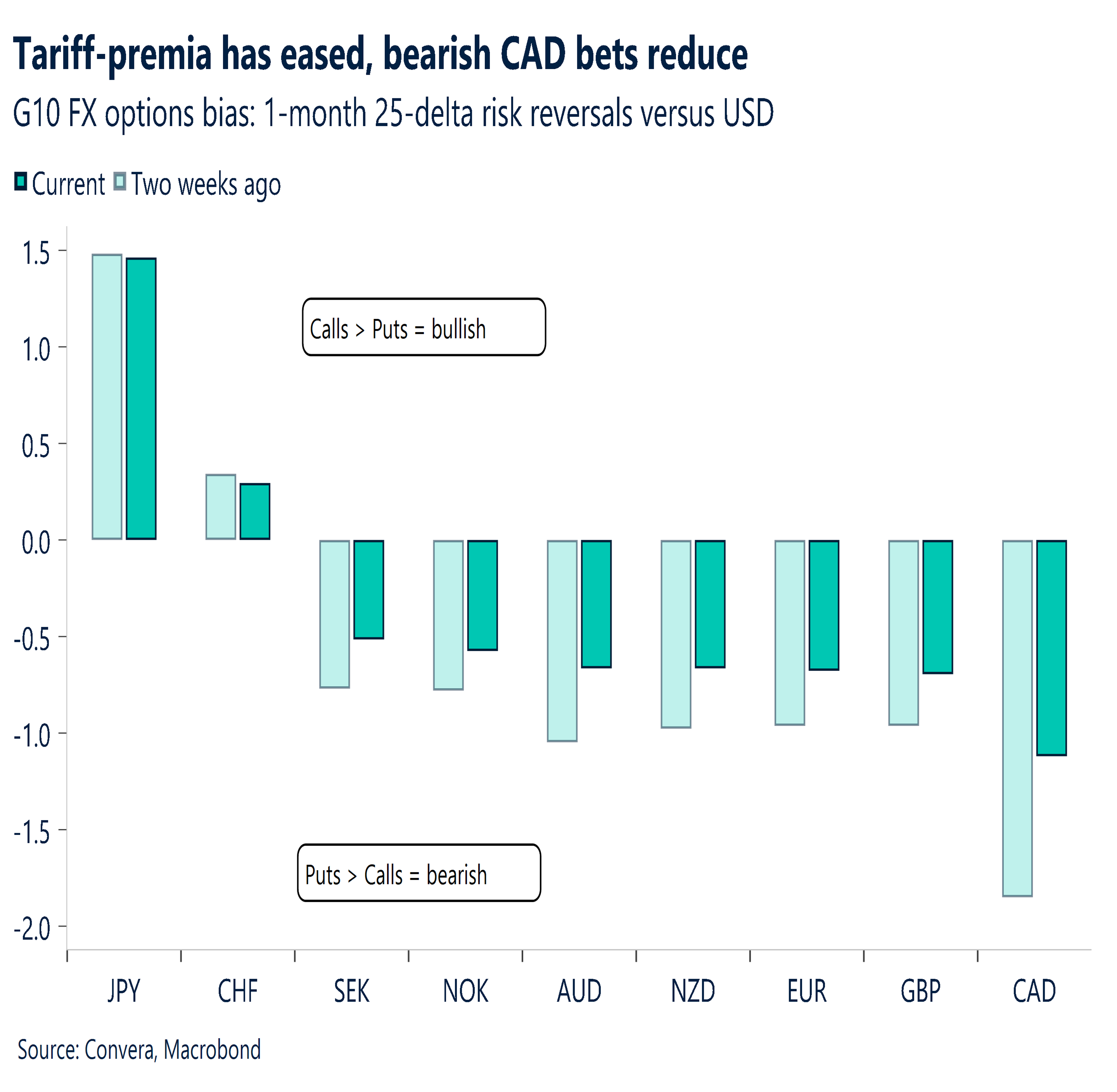

- Trump dominates FX. Markets are showing fatigue toward tariff-related headlines, reacting more selectively to Trump’s shifting trade rhetoric. With the Fed pause already priced in, Trump’s policies remain the key market driver.

- Dollar under pressure. Despite reduced Fed easing expectations, the USD has weakened due to a lack of new tariffs reducing safe-haven demand. The Greenback is down 3.4% since January

- Euro testing $1.05. The euro remains highly reactive to Trump’s stance on Ukraine and Germany’s upcoming election. Hawkish ECB comments and rising German bond yields have provided some support, but uncertainty remains a key risk factor.

- Pound extends rally. GBP/USD is on track for a third consecutive weekly gain, nearing 1.27. Strong UK inflation and wage growth data have reduced rate-cut expectations, keeping sterling supported.

- Week ahead. Inflation, Fed policy shifts, and geopolitical developments will continue shaping market sentiment. Key focus areas include US and European inflation data.

Global Macro

Tariff fatigue sets in

Few cuts from the Fed this year. Economic uncertainty is rising as the Fed monitors Trump’s policies on trade, immigration, and fiscal spending. While Atlanta Fed President Bostic expects two rate cuts in 2025, businesses worry about higher costs from tariffs and labor shortages due to mass deportations. Signs of rising inflation are mounting, with headline CPI and PPI figures accelerating and recent surveys indicating increased price pressures. As a result, investors have pared back expectations for Fed easing to less than one rate cut this year.

Hawkish ECB tilt? Eurozone consumer confidence rose to -13.6 in February—its highest level in four months—beating expectations. Optimism is fueled by hopes that the European Central Bank (ECB) will continue cutting rates, with markets pricing in a 25 bps cut at each of the next three meetings, bringing the deposit rate below 2% by 2026. These economic shifts unfold amid rising geopolitical tensions, particularly in Germany, where the upcoming election could reshape European leadership. Conservative challenger Friedrich Merz reaffirmed support for Ukraine, while the UK and France are drafting plans for a European-led “reassurance force” to safeguard Ukraine if a ceasefire is reached.

Trump is the elephant in the room. FX markets are clearly showing signs of fatigue when it comes to tariff-related headlines. While Trump’s trade rhetoric and tariff developments will continue to be major market drivers, investors are becoming more selective in their reactions. Markets are taking a more measured approach rather than overreacting to every headline given Trump’s history of shifting positions and postponing tariffs. Hawkish monetary policy can only do so much as to help the Greenback because the Fed pause is already fully priced in. Also, US economic momentum is slowing and not providing a supportive backdrop to the currency. That’s why Trump is moving markets more. He is the elephant in the room, not the Fed.

Week ahead

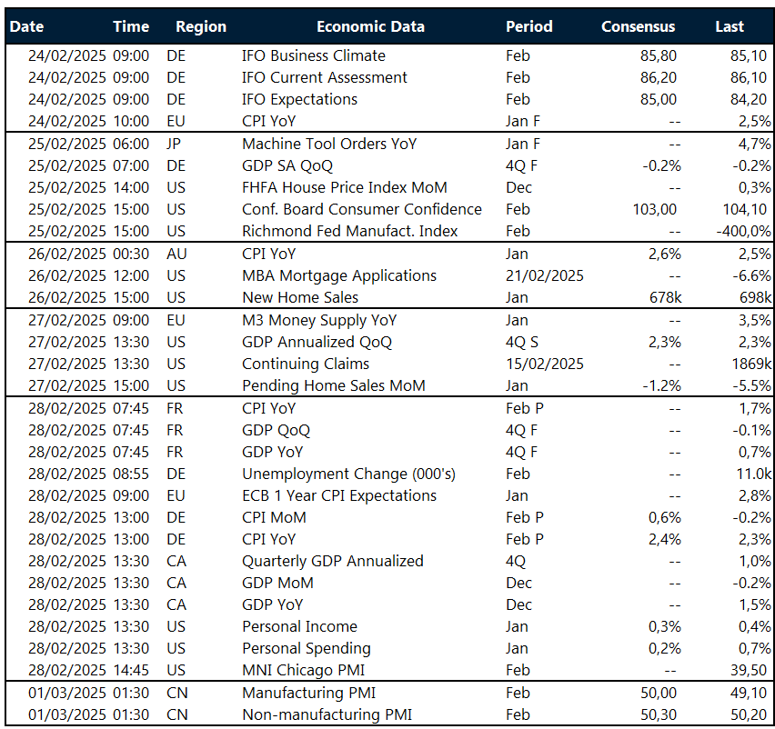

Secondary data and PCE inflation

With inflation, GDP, and labor data from multiple regions, monetary policy expectations will remain the dominant market driver. Investors will be particularly focused on inflation trends and consumer confidence figures, while Chinese PMI data will be key in shaping global growth sentiment.

Europe. The week starts with Germany’s IFO Business Climate (Feb), providing insights into business sentiment amid ongoing economic challenges. On Feb 25, Germany’s GDP data (Q4 F) is expected to confirm a -0.2% contraction, highlighting the struggles of Europe’s largest economy. Inflation remains in focus, with Eurozone CPI due on Feb 24, followed by French CPI and GDP data on Feb 28. Meanwhile, Germany’s CPI (Feb P) and unemployment change (Feb) will shed light on labor market dynamics and price pressures. These figures will help shape expectations for the European Central Bank’s upcoming rate decisions, as markets anticipate a continued easing cycle.

US. The US economic calendar is packed with secondary data releases that could influence sentiment around the Fed’s next move. On Feb 25, the Conference Board Consumer Confidence (Feb) will reveal sentiment trends amid persistent inflation concerns. GDP figures follow on Feb 27, with the annualized Q4 growth rate expected to hold steady at 2.3%. Inflation remains a primary focus, with personal income and spending (Jan) released on Feb 28, alongside the Fed’s preferred PCE inflation gauge.

APAC. In Japan, Machine Tool Orders (Jan F) on Feb 25 will provide a snapshot of industrial activity. Australia’s CPI (Jan), expected at 2.6%, is set for release on Feb 26, offering clues about inflation trends and potential Reserve Bank of Australia policy moves. The week concludes with China’s Manufacturing and Non-Manufacturing PMIs (Feb) on Mar 1, crucial for assessing the momentum of the country’s economic recovery. Weak PMI readings could further dampen global risk sentiment.

FX Views

Broad based dollar weakness

USD Weighed down by data. Signs of rising inflation are mounting. As a result, investors have pared back expectations for Fed easing to less than one rate cut this year. The US dollar has not strengthened despite this, likely due to two factors: first, the absence of new tariffs has reduced safe-haven demand and the trade premium; second, the Fed pause narrative is driven by rising inflation expectations rather than stronger macro data. With this week’s data reflecting these trends, the dollar has been unable to benefit from the Fed holding rates steady. The Greenback is now at its lowest level this year, down 3.4% since its January peak. As we have previously noted, dollar bulls would need either continued tariff implementation by Trump or stronger macroeconomic data for a sustained rebound.

EUR Euro testing $1.05. The euro remains in the palm of US President Donald Trump as his daily commentary continued to drive the common currency and sentiment around it. Trump has made it clear to Zelenskiy—either make peace with Russia quickly or risk losing Ukraine altogether. Uncertainty therefore remains high, especially ahead of Germany’s general election on Sunday, but the euro has benefited from broad dollar weakness and soft US data. Hawkish comments from ECB Board Member Isabel Schnabel helped as well when she called for caution and a rethink to rate cuts amidst tariff threats and rising inflation rates. German bond yields pushed higher across the board with the 10-year Bund reaching a 3-week high at 2.55%.EUR/USD is testing the $1.05 level, with a break potentially targeting $1.0540.

GBP 3rd week up in a row. For the third consecutive week, the pound has appreciated against the USD, posting a two-month high and approaching 1.27, nearing the overbought zone. Sterling’s initial positive reaction to the hot UK inflation report on Wednesday lost momentum but recovered by the end of the week, trading above 1.266. Despite uncertainties, recent data supports a Bank of England (BoE) hold in March and potential rate cuts from May. Inflation is projected to remain elevated, with growth possibly surprising to the upside. Traders have adjusted BoE easing bets to 50 basis points, anticipating two rate cuts by year-end, slightly below the BoE’s forecast. The pound’s sensitivity to global risk appetite and the UK’s current exemption from tariffs provide sterling with an advantage over the euro.

MXN Peso moves sideways. Volatility in the Mexican Peso is expected to rise as the risk of tariffs resurfaces, with the tariff suspension expiring on March 4th. Negotiations between Mexico and the US are likely to ramp up next week. Despite this uncertainty, Mexican central bank policymakers have committed to continuing monetary policy easing. They have mentioned a “new stage” of monetary policy, aiming for swift adjustments to bring inflation closer to the 3% target. Another half-point rate cut is being considered for the March decision, according to the bank’s Feb. 6 meeting minutes. Recent economic data from Mexico revealed a dip in consumer spending compared to November, but it exceeded economists’ expectations. Banco de Mexico (Banxico) confirmed its dovish stance and hinted at further rate cuts in its latest meeting minutes. While the tariff threat has not been entirely eliminated, markets can expect heightened uncertainty until there is more clarity on the more structural issue of the USMCA renegotiation, which is expected to take some time. Additionally, carry erosion may affect the MXN, reducing the currency’s ability to cushion against unexpected shocks.

CNY Yuan gains on trade deal hopes. Recent diplomatic developments between the US and China have triggered notable yuan strength, with potential for further gains. While trade tensions persist around tariffs and policy disagreements, the improving tone in bilateral communications has provided support for the CNH. Technical analysis shows USDCNH demonstrating negative trend momentum, with immediate support at the Cloud base of 7.2283. A decisive break below this level would accelerate downside momentum toward our target of 7.1475. The pair faces strong resistance at 7.3682, with any advances likely to face selling pressure. Only a sustained break above 7.3682 would warrant reconsidering our negative trend outlook, potentially opening up moves toward 7.4888. The yuan’s sensitivity to trade headlines suggests continued volatility around diplomatic developments.

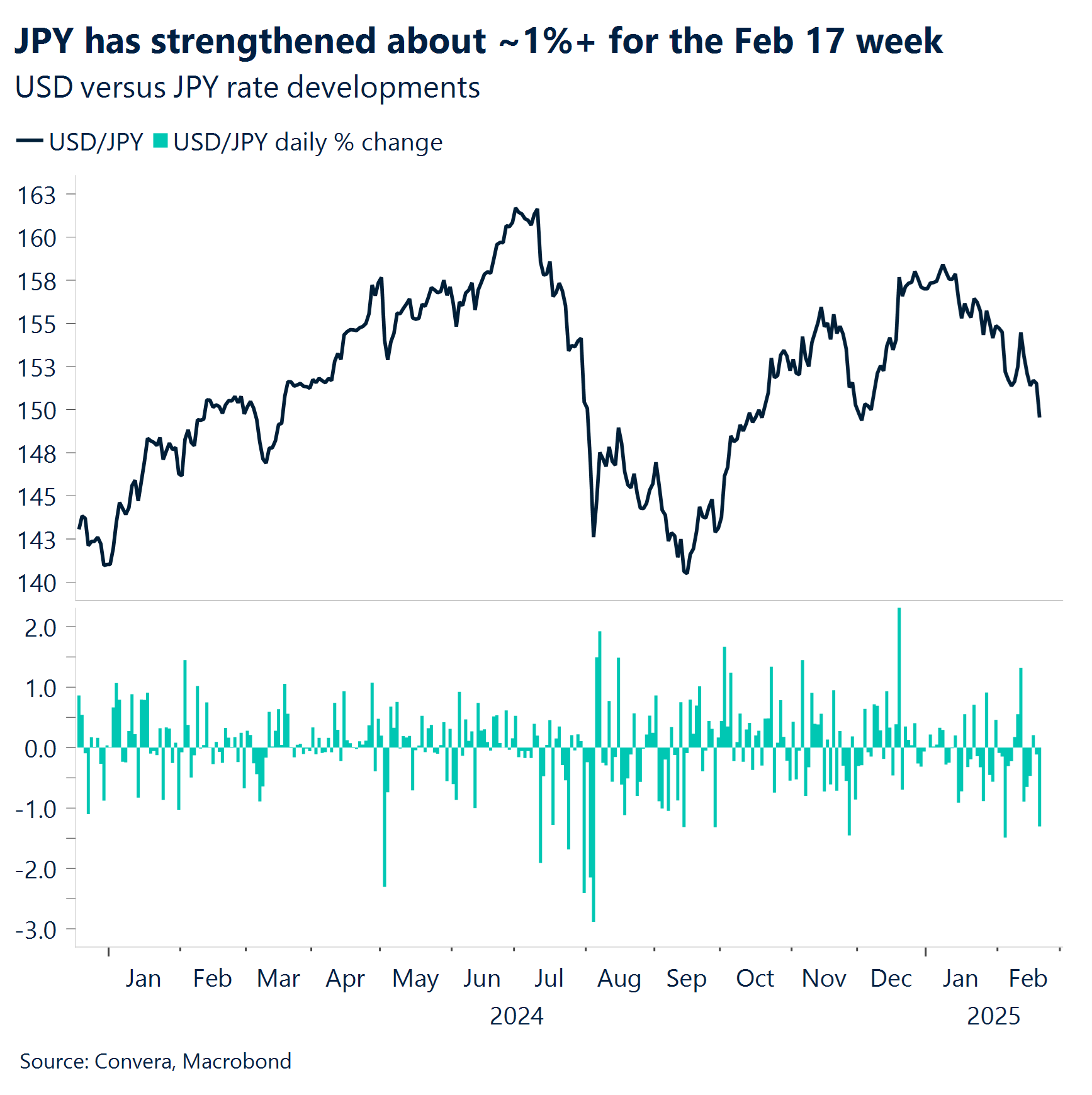

JPY Trade data misses mark as USDJPY forms negative trend pattern. Japan’s substantial January trade deficit of JPY2.76 trillion, exceeding the expected JPY2.1 trillion, highlights ongoing trade challenges despite rising exports. While export growth continued for a fourth month at 7.2% y/y, the surge in imports to 16.7% y/y influenced the negative trade balance. Technically, USDJPY shows negative formation at 152.89, with a rising wedge pattern targeting 145.50, supporting our immediate target of 149.30. The developing head and shoulders pattern on weekly charts reinforces the negative outlook. Resistance at 158.50 remains crucial – a break above would invalidate our negative view and suggest potential moves toward 161.95. Market focus now shifts to upcoming Tokyo CPI, industrial production, and retail sales data for further directional cues.

CAD Quiet week. Only 86 pips of trade range for the Loonie, mostly trading below the 1.42 level, with a weekly low of 1.416, high of 1.4245, as it awaits clarity or resolution on US trade policy developments. So far, Trump’s bark has been louder than his bite. In his first month in office, he proposed four different tariffs affecting key trade partners: 25% on Mexico and Canada, 25% on all aluminum and steel, reciprocal tariffs on all trading partners, and this week, 25% on autos, semiconductors, and pharmaceutical products. The imposition of these tariffs will depend on the Canadian government’s ability to negotiate key aspects of the USMCA trade deal.

Key support levels for 2025 are at the year’s low of 1.415 and the 100-day SMA at 1.414. Resistance levels include 1.425 and the 50-day SMA at 1.435.

Next week, we expect a similar story, but markets might get choppier by the end of the week as the 30-day delay period approaches on March 4th. Key data from the macro calendar include Canada and US 4Q24 GDP and special focus will be on the US PCE index for January, to be published on Thursday.

AUD Rising labor market strength tests resistance. Australian employment surged beyond expectations with 44k jobs added in January, dominated by full-time positions at 54k. While unemployment edged up to 4.1%, the rising participation rate to 67.3% indicates underlying labor market strength. On the technical front, AUDUSD maintains positive momentum above 0.6260, with immediate resistance at the Cloud top of 0.6409. The pair’s position within the Ichimoku Cloud suggests strengthening positive trend bias, supporting our target of 0.6545. Key support lies at 0.6131 – a breach would invalidate our positive outlook and shift focus to 0.5980. The strong jobs data reinforces hawkish RBA positioning, though upcoming monthly CPI indicator, capital expenditure data, and housing credit figures will be crucial for near-term direction.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.