- Conflicting signals. Markets have been whipsawed by conflicting US signals about how long the conflict could last. One day officials hint at a rapid de‑escalation, the next they warn of a prolonged campaign. That headline‑driven volatility has kept risk appetite fragile.

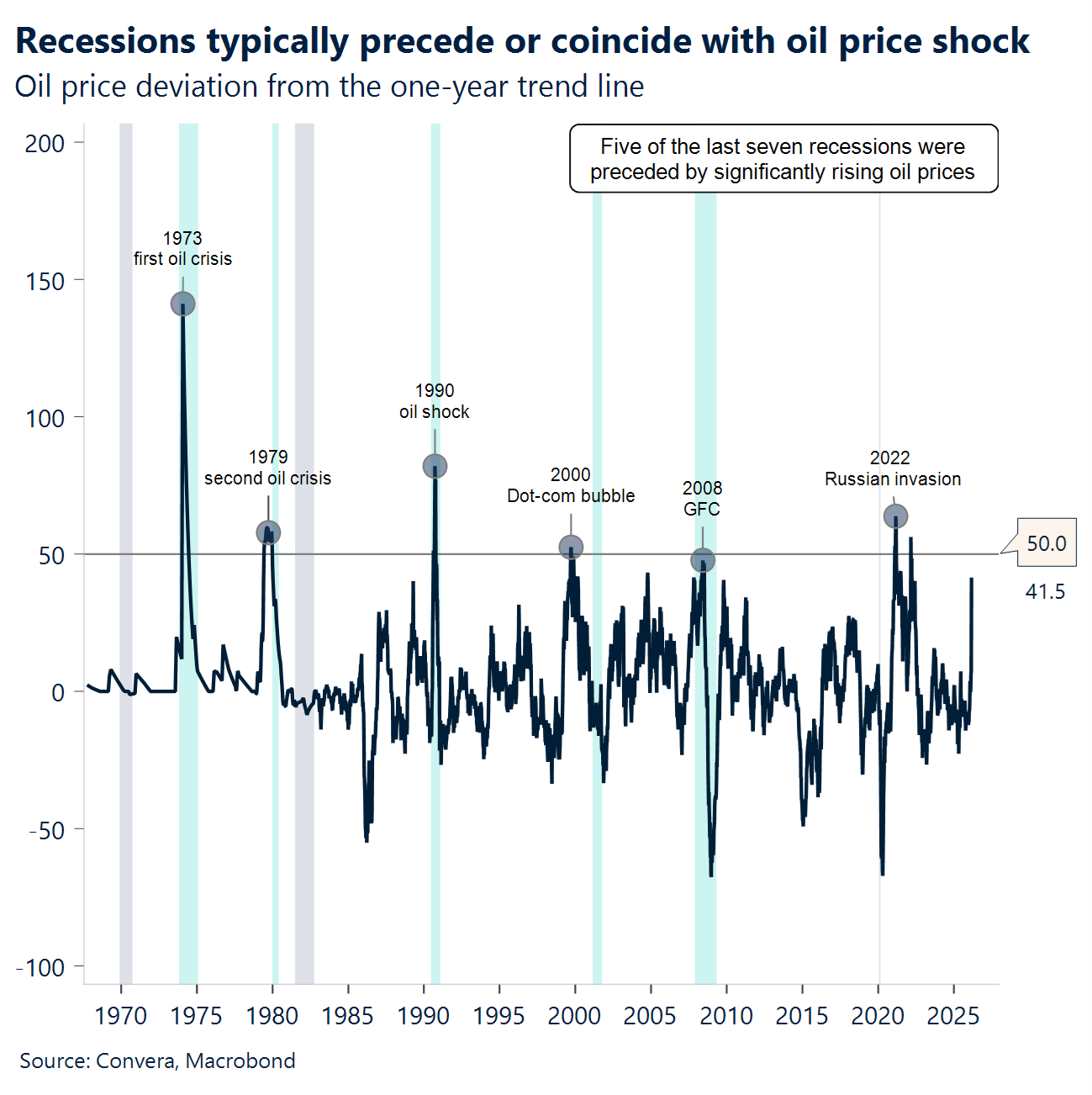

- Mine the gap. Iran has reportedly laid mines across the Strait of Hormuz. That’s a material escalation for energy markets already running a structural shortfall, with crude rising over 16% this week, up over 60% year-to-date.

- Not enough. The IEA’s coordinated drawdown of 400mln barrels of oil briefly steadied nerves, but it’s a band‑aid on a far bigger wound. Some 18mln barrels a day — nearly 20% of global supply — should be flowing through Hormuz.

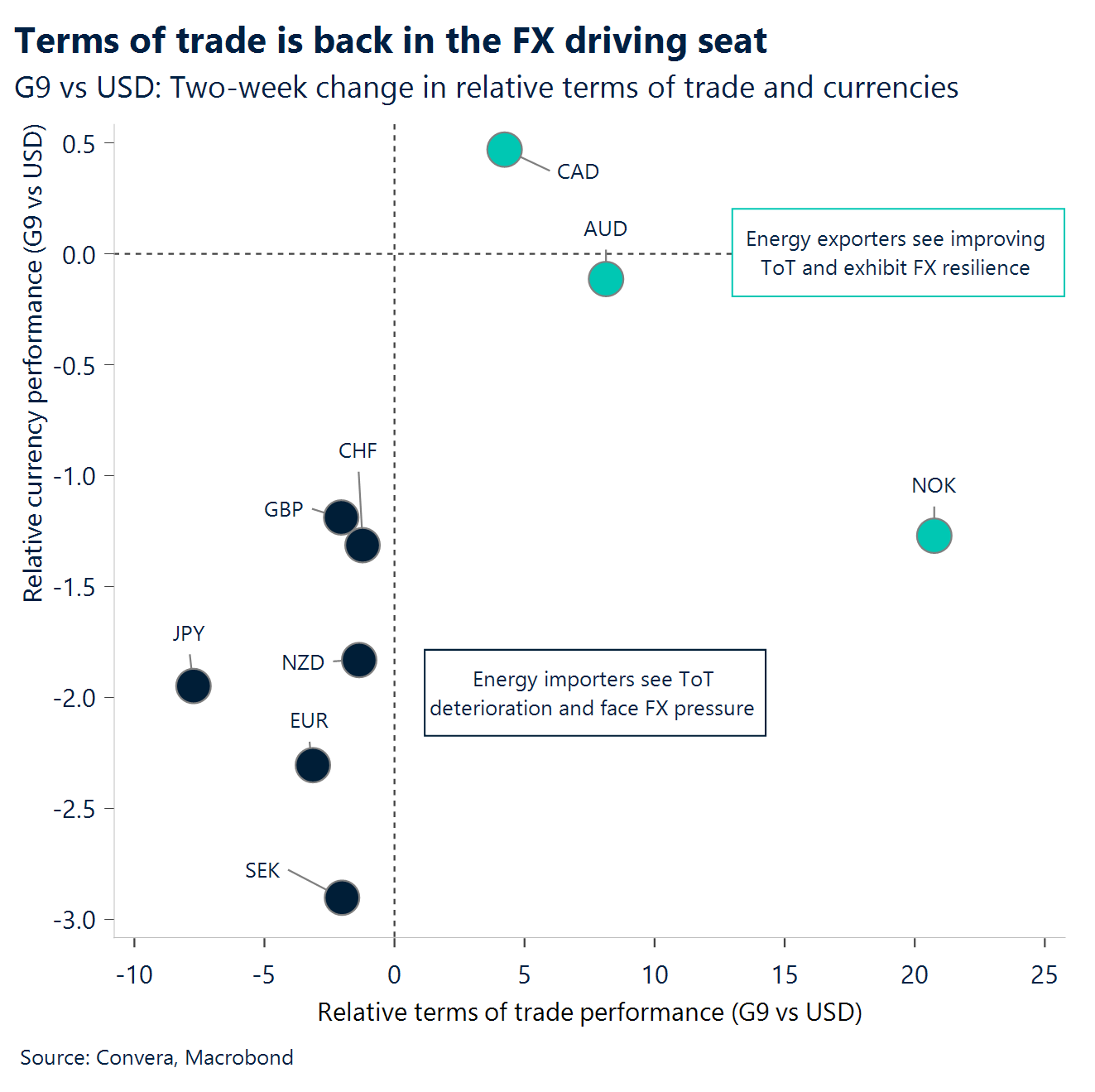

- Duration drives the damage. The only thing that really matters is the duration of the conflict and the scale of energy‑flow disruption. That’s why terms of trade is now firmly back in the FX driving seat.

- Aussie assault. Risk‑sensitive but commodity‑backed, the AUD surged to its strongest level against the USD since June 2022, and although it’s dropped 2% since then, it is still the best‑performing major currency year‑to‑date..

- Reflation risks. February’s US inflation numbers were heading in the right direction, but the surge in energy prices has drastically changed the global macro landscape, with short-term inflation expectations jumping.

- Policy problems. Amid stagflation fears, the upcoming influx of central bank decisions will be closely monitored as markets pare back easing bets.

Global Macro

Stagflation fears rise as Iran war drags on

Stagflation fears. Brent crude’s jump to $100 per barrel has fed directly into front-loaded inflation expectations. While the front end of the curve is spiking, long-term expectations remain anchored as markets bet on the Fed’s ability to rein in inflation and view the current energy disruption as temporary. Despite leading indicators suggesting a healthy US Q1 GDP rebound, Middle East instability and higher energy costs increase the risk of a stagflationary backdrop. Consequently, monetary policy guidance could become increasingly murky, as traders reassess interest rate path from central banks. For now, markets remain in a high level of tension, closely tied to headline risk.

IEA intervention. In an emergency meeting on Wednesday (March 11), the International Energy Agency (IEA) announced a release of 400 million barrels from strategic reserves, the largest in history. Despite this, the market has “shrugged off” the move, as the total closure of the Strait of Hormuz has essentially cut off 20% of global daily supply.

BoE commentary. Governor Bailey emphasized that while UK RPI (around 5y5y) remains elevated, the bank is monitoring the “stagflationary impulse” of high energy prices on the broader UK recovery.

China’s deflationary thaw. Data from Monday (March 9) showed a surprise jump in CPI to 1.3% YoY, well above the 0.9% estimate. This marks a decisive shift away from last year’s deflationary trend, signaling a recovery in domestic Chinese demand.

US CPI, PCE. The February’s inflation numbers, both CPI and PCE were heading in the right direction, but the surge in energy prices has drastically changed the global macro landscape.

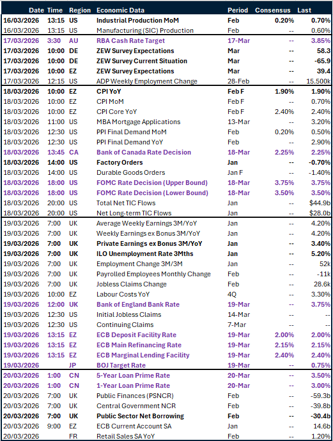

Week ahead

Policy caution takes centre stage

- Surging oil prices keep markets on edge. The conflict in the Middle East will continue to grab headlines next week. With Brent looking increasingly comfortable around $100 a barrel and neither side showing signs of de‑escalation, markets are growing more wary of the longer‑term consequences for growth and inflation.

- A cautious week for central banks. Away from geopolitics, it’s a packed week for major central banks. We’ll be watching the Fed, ECB and BoE closely. A conflict‑driven note of caution is likely to run through all three, regardless of region‑specific risk balances. At the same time, each bank will aim to reassure markets by highlighting the extensive toolkit available to manage rising price pressures.

- Soft jobs, stubborn inflation. The UK’s jobs report is due. Softness has become a constant theme: unemployment is hovering near a five‑year high at 5.2%, while wage growth across several measures continues to edge lower. Yet with inflation still above target — and the disinflation path now jeopardised by the ongoing conflict — risks are building that the easing needed to support the soft backdrop may not materialise as soon as markets had hoped.

FX views

A week ruled by headlines

Oil up, cuts down, USD up. The dollar index kept climbing this week, up 1.1%, as headlines showed no sign of de‑escalation. Even with the G7 trying to lean against the surge through policy intervention, oil is still hovering near $100 a barrel – over 60% higher year‑to‑date – giving the dollar a mechanical lift beyond any classic safe‑haven bid. The US and its major peers have also faced an aggressive hawkish repricing since the conflict began, with markets shifting from roughly two Fed cuts priced in at the start of the week to less than one today. Similar recalibrations have played out across the G10, but with the US seen as more oil‑independent – and therefore better placed to absorb rising inflation expectations – the bullish pass‑through to FX is cleaner, adding a stickier layer of support for the greenback. The dollar index is now testing the 100 handle, a level it hasn’t held above since the April 2025 sell‑off. Next resistance targets are November’s 100.395 and May’s 101.977.

Euro buckles under $100 oil. Just like a mirror image, EUR/USD grinds lower – down 1.4% into week’s end and more than 3% lower on a month‑to‑date basis. Brent consolidating near $100 a barrel today – unlike earlier in the week, when any spike quickly faded – reflects a shift in risk pricing toward a longer and more disruptive scenario. The severe sell‑off in the common currency on Friday captures that change in sentiment. As a net oil importer, the eurozone is seen as highly exposed to rising energy prices. One amplifier behind the euro’s bearish reaction (versus, say, GBP) is the previously solidified expectation of a 2026 growth rebound tied to Germany’s fiscal stimulus. With that optimism already dented by domestic concerns, this external shock adds another layer of pressure, adding to a sharper downside response in the currency. Barring any meaningful sign of de‑escalation, the euro remains poised for further weakness. It is now flirting with the November low at 1.1469, with July’s low at 1.1392 next in line.

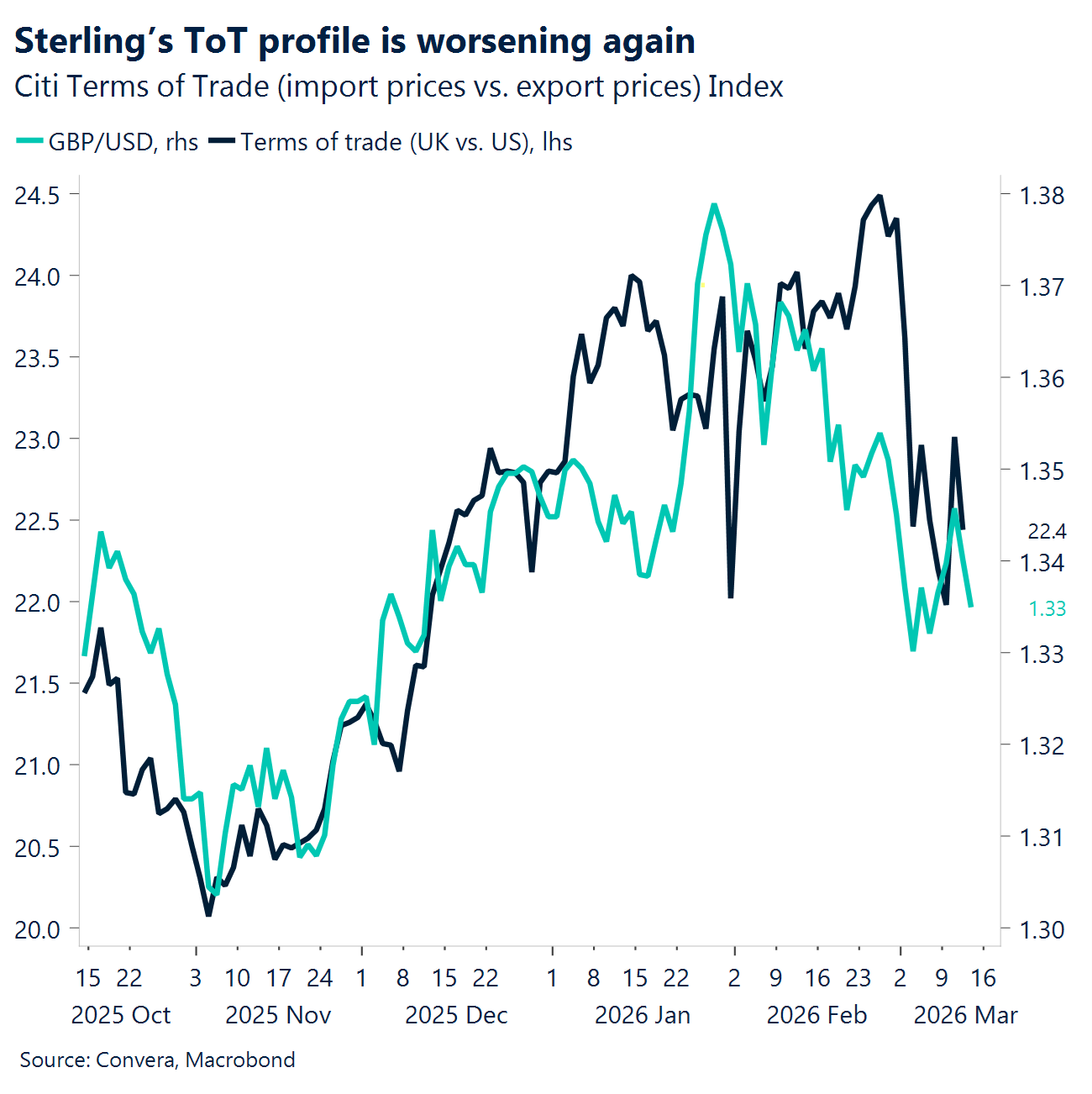

GBP Trading the energy whiplash. Sterling is still dancing to the tune of volatile energy markets. When oil prices slumped earlier in the week, the dollar softened and GBP/USD looked ready to punch through $1.35. But the relief was fleeting. As the conflict escalated and energy prices snapped higher again, the dollar regained its footing and cable was dragged back down. The pound is down nearly 1.5% against the dollar this month, and that weakness comes at a time when UK growth had already stalled heading into the conflict. GBP/USD has slipped back below $1.33, and if geopolitical tensions fail to ease, a drift toward $1.31 in the coming weeks is entirely plausible. So far, the move has been more about broad USD strength than a sterling‑specific story — but that could change. If the BoE hesitates in confronting the risk of resurgent inflation, the pound could face an additional domestic headwind just as global conditions remain hostile. We think the BoE will hold rates steady at 3.75% next week and that rate cuts are off the table this year if energy prices stay elevated for longer than two months.

CHF Franc force meets SNB course. The Swiss franc surged to fresh multi‑year highs against the euro, extending a rally that has already delivered over 3% gains this year. A recent warning that the SNB is “increasingly prepared to intervene” has done little to slow the move. It leaves the SNB in an increasingly uncomfortable position: tolerate further appreciation and risk damaging exports or push back more forcefully and invite accusations of currency manipulation. EUR/CHF broke below 0.90 for the first time since 2015, with risk aversion and Europe’s energy vulnerability reinforcing the franc’s appeal. USD/CHF has risen, but that matters less for policymakers given Switzerland’s import basket is overwhelmingly euro‑centric. The dilemma is sharpening. Haven flows remain powerful, verbal intervention is losing traction, and a return to negative rates can no longer be ruled out if the SNB feels compelled to reassert control. With the policy meeting just days away, traders are likely to keep testing the SNB’s tolerance. Absent tangible action, the path of least resistance remains further CHF strength as long as global risk sentiment stays fragile.

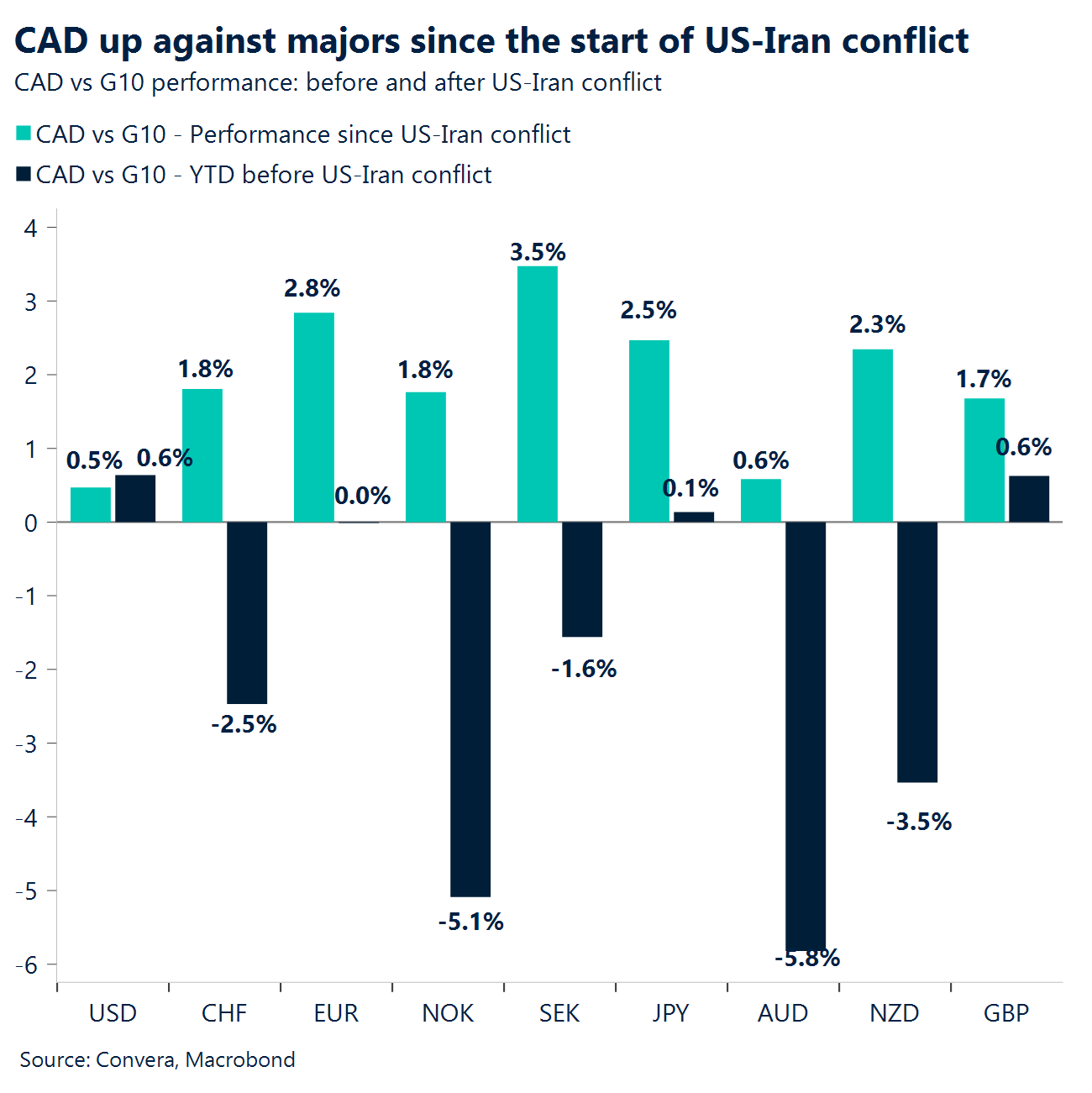

CAD’s ‘exceptionalism’. A disappointing jobs report, marking the steepest decline since January 2022, has pushed USD/CAD from 1.366 toward 1.372. As regional conflicts drag on, this latest labor data weakens the case for a stronger Loonie once the geopolitical premium eventually fades. For now, however, oil prices dictate the currency’s direction and continue to cushion the impact of domestic macro softness. This energy support remains the primary shield for the Canadian dollar, even as the labor market shows significant distress. While the Loonie trailed the G10 for most of last year, it has recently stolen the headlines following the start of military operations in Iran. Markets are clearly rewarding energy independence, drawing a sharp distinction between net exporters and importers. Since late January, USD/CAD has consolidated within a 1.35 to 1.37 range. Flat moving averages across all timeframes confirm this sideways trend, with recent attempts to break above 1.37 meeting consistent selling pressure. The outlook shifts next week with a packed calendar: February CPI on Monday, a “double header” of BoC and Fed holds on Wednesday, and retail sales on Friday.

AUD RBA to hike? AUD/USD jumped to its highest level since June 2022 before reversing course on wavering risk appetite. A new Melbourne Institute survey shows that Australians now expect inflation to rise to 5.2% in March, up from 5.0% in February and 3.6% a year ago. This is the highest level since July 2023 and suggests inflation pressures are picking up again. Rising global oil prices are also adding to costs, amid the ongoing US-Iran conflict. Expectations for tighter policy have grown, with markets now pricing a 67% chance of a rate hike on 17 March. AUD/USD is trading 2% below its recent high of 0.7187, reached on 11 March. Key support sits near the 50‑day EMA at 0.6967, followed by the 100‑day EMA at 0.6838. Traders will be watching the RBA rate decision, the accompanying statement, and Australia’s unemployment data for further direction.

CNH China grows uneasy as summit prep stalls. Chinese officials are growing frustrated with what they view as the US taking a last‑minute approach to preparations for the upcoming Xi–Trump summit, according to Bloomberg. Beijing worries the rushed planning will narrow the talks to trade issues while sidelining broader diplomatic and security concerns. USD/CNH has rebounded 0.9% from its recent low of 6.8267, last seen on 26 February. The next key resistance stands near the 50‑day EMA at 6.9273, followed by the 100‑day EMA at 6.9815. Markets will be watching China’s industrial production, unemployment rate and loan prime rate decisions for further direction.

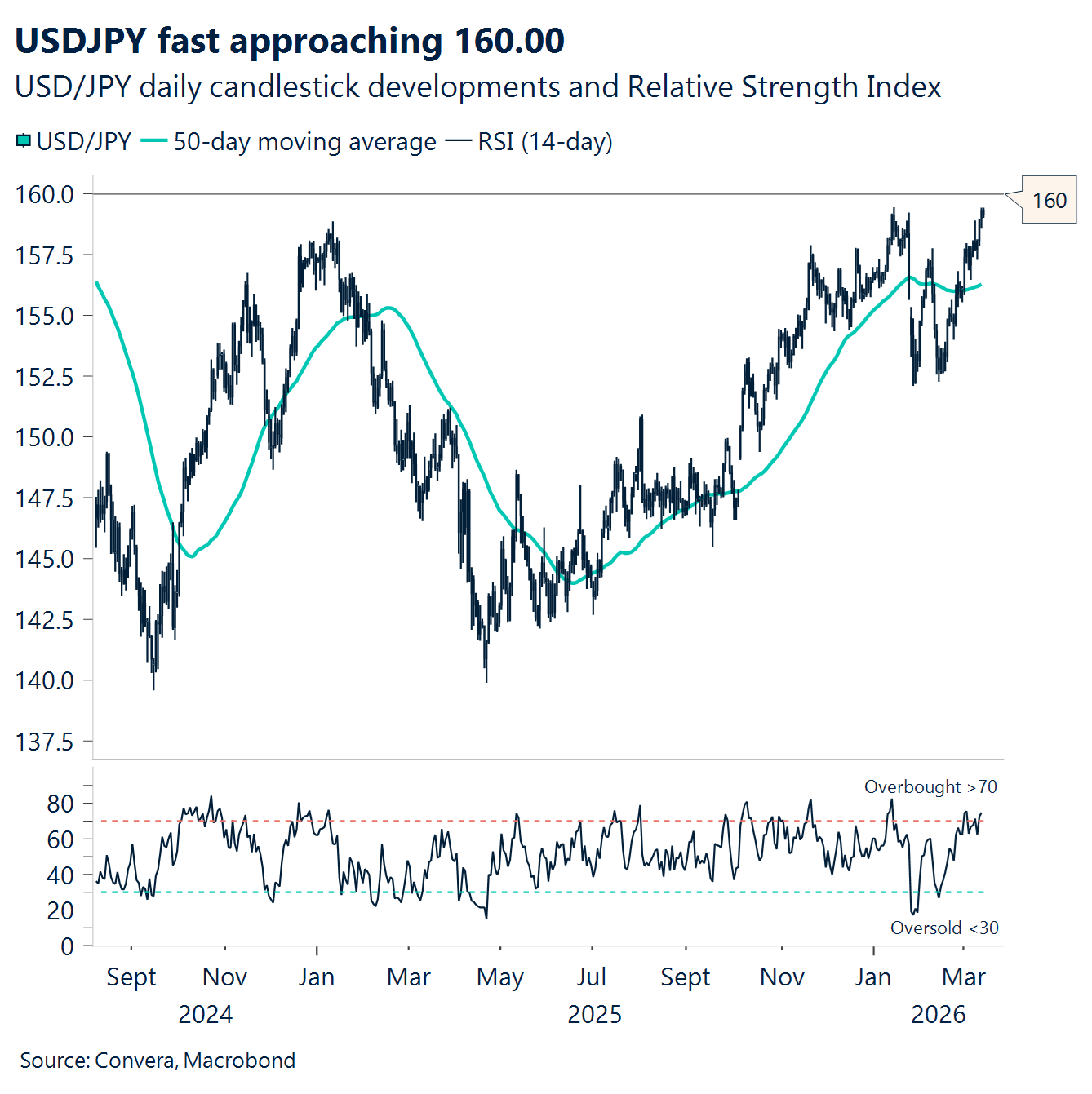

JPY USD/JPY slides toward 160.00. USD/JPY edges higher toward 160.00, but markets don’t expect the government to step in to support the currency. Unlike past situations, the yen’s decline now is seen as driven by economic fundamentals, not speculation, so intervention is less likely. Even though Japan has acted before when the yen was in the 160–162 range, traders believe simply hitting 160 won’t trigger action. Officials may likely stick to verbal warnings., with geopolitical uncertainties and limited support from the U.S. The next key support levels for USD/JPY sit at the 21‑day EMA of 157.1350, followed by the 50‑day EMA of 156.3150. Markets will focus on upcoming data and events, including the trade balance, industrial production, the Bank of Japan rate decision, and the BoJ monetary policy statement.

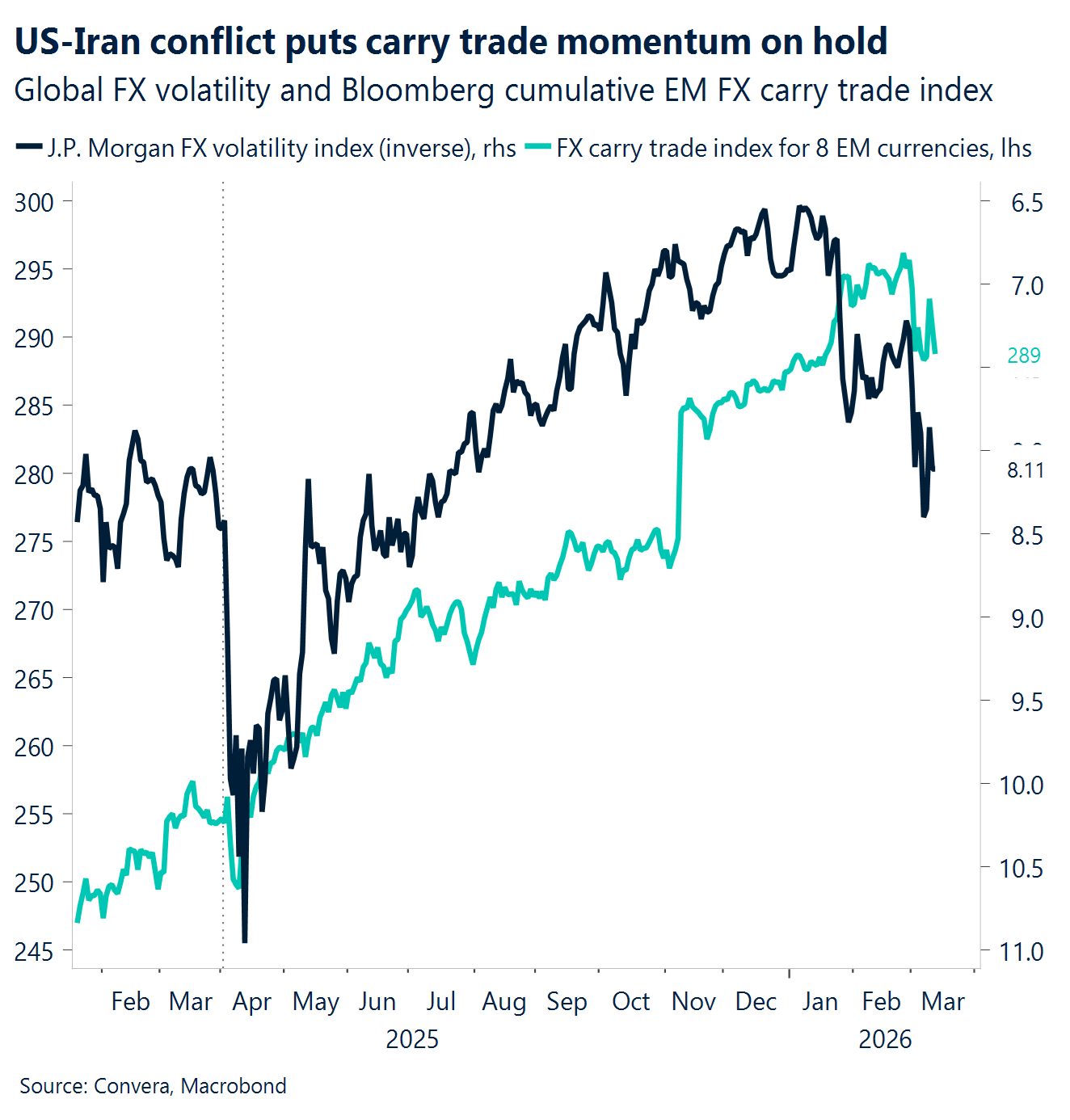

MXN Peso under pressure. The recent surge in emerging market (EM) currency volatility marks a significant shift in recent market action. For months, EM volatility traded uncharacteristically below G7 levels, but this trend has reversed sharply as geopolitical tensions in the Middle East have intensified. This shift signals a breakdown in the carry trade environment, as the stability that previously favored high-yielding EM currencies is replaced by heightened idiosyncratic risks and global uncertainty. The Mexican Peso has felt this shift, seeing intense selling pressure that has seen the pair move from the 17.10–17.20 range in mid-February to a peak of 18.02, effectively erasing its year-to-date gains. While the market has recently stabilized closer to 17.7, the outlook remains clouded.

BRL Geopolitics strain real. The Brazilian real has recently faced significant headwinds, retreating toward the 5.22 level against the dollar as heightened geopolitical tensions in the Middle East drive a global flight to safe-haven assets. While surging crude prices, with Brent flirting with the $100 mark, traditionally act as a fiscal tailwind for Brazil due to its status as a net oil exporter, the market is currently more preoccupied with the specter of higher inflation. This shift in sentiment has fundamentally altered the outlook for domestic monetary policy; although recent data showed cooling consumer prices, the Central Bank is now expected to moderate its pace of interest rate cuts. Despite the spike in volatility, the real has proven remarkably resilient compared to its emerging market peers. The 2026 low of 5.12 remains a critical support level ahead of next Wednesday’s central bank meeting. Bloomberg’s consensus forecast anticipates a 50-basis-point cut, bringing the Selic rate down to 14.5%, a move that would mark Banco Central do Brasil’s first interest rate reduction in three years.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.