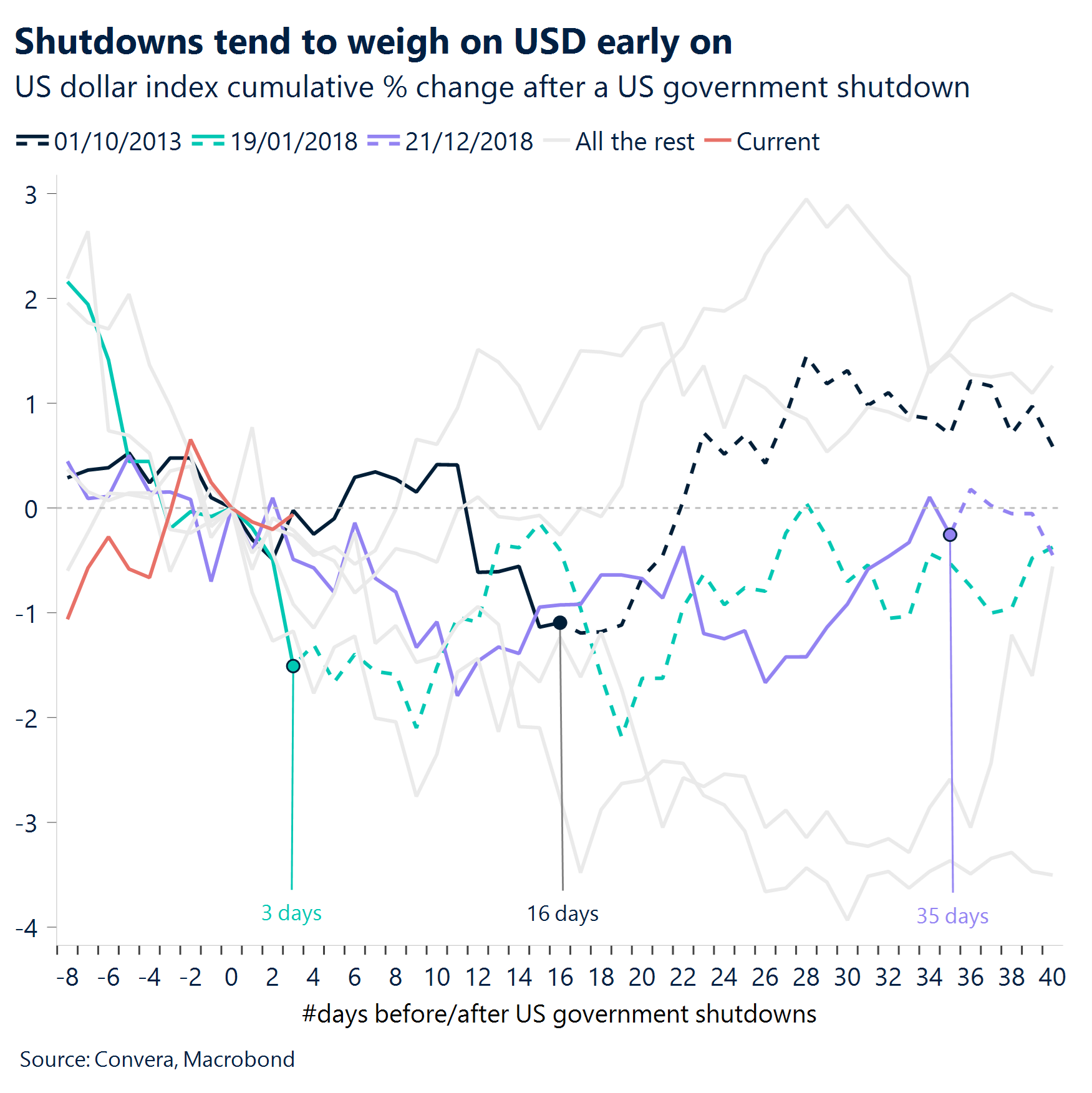

- Shutdown. The US entered its first government shutdown in nearly seven years because Congress couldn’t reach a funding agreement. Shutdowns have typically lasted anywhere from three to 35 days.

- Calm with caveats. Equities continue to hit record highs as investors brush off near-term risks, yet strong demand for traditional safe havens like gold and the Japanese yen signals lingering unease beneath the surface

- Dreary dollar. The USD suffered its longest losing streak in a month, with downside bias building. History offers little comfort – during the last three shutdowns (2013, early 2018, and late 2018–2019), the dollar drifted lower through the impasse.

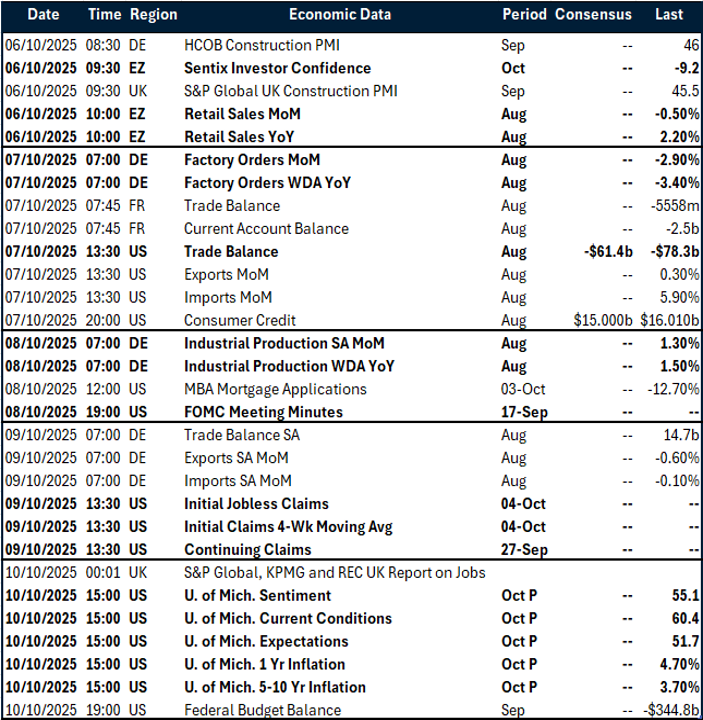

- Data blackout. The federal shutdown threatens to suspend key economic releases, leaving investors and policymakers without critical inputs to assess the trajectory of the world’s largest economy and Fed policy.

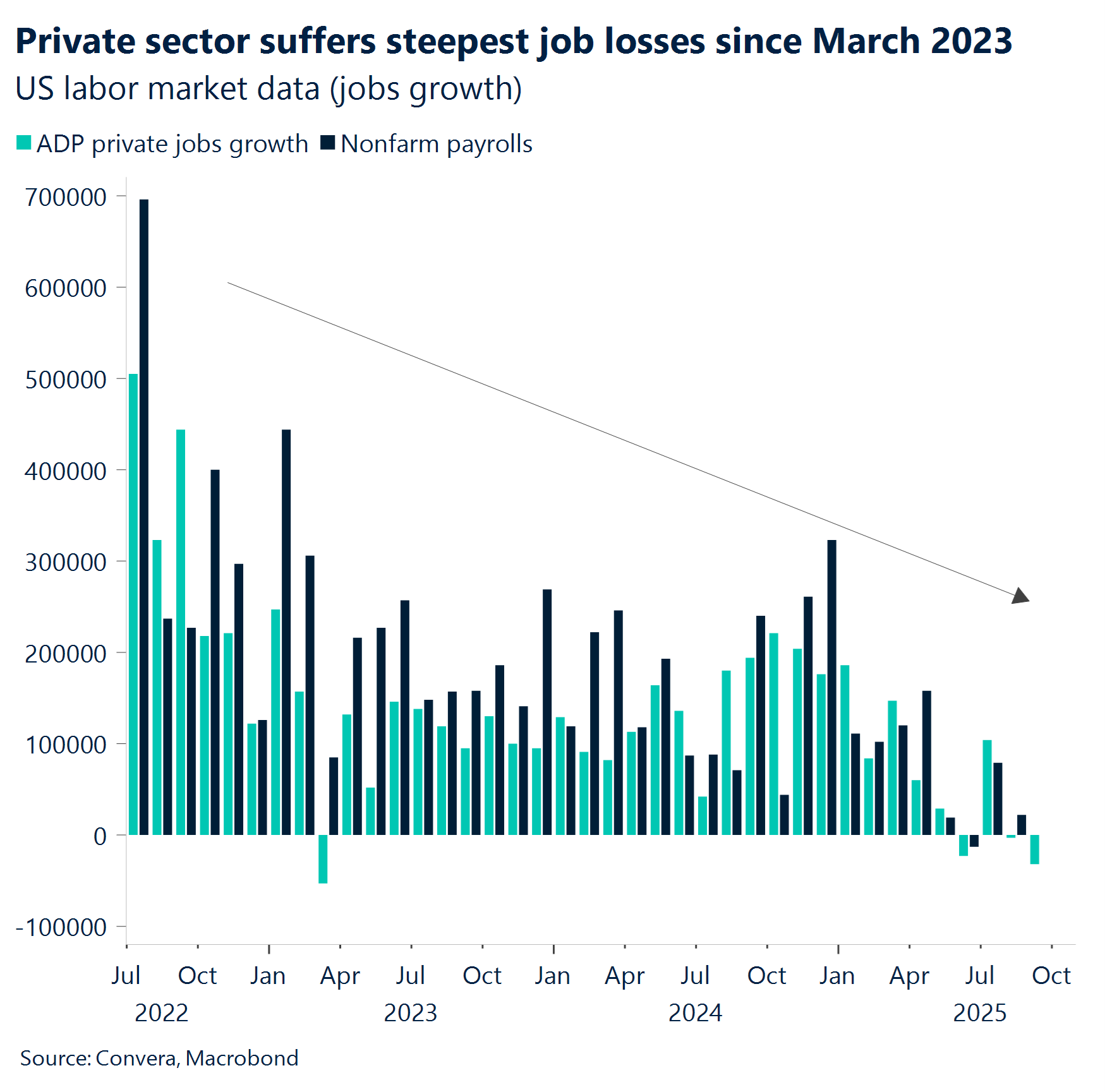

- ADP lights the way. However, ADP data was released because it is privately produced. It reported a drop in private payroll – reinforcing October Fed rate cut expectations.

- Duration matters. Investor concerns are rising over a longer shutdown, which could hit consumer confidence and job security. If extended and paired with proposed federal workforce cuts, the economic impact may be deeper than in past episodes.

Global Macro

Shutdown makes ADP key report of the week

Private sector job loss. In the absence of the NFP report due to the shutdown, peripheral macro data releases for the week have surged in importance. The US private sector shed 32,000 jobs in September. This was a significant miss compared to the analyst consensus, which had forecast a gain of around 50,000 jobs. This signaled a sharp slowdown in labor market momentum and a potential contraction in private payrolls, driven largely by job losses at small and medium-sized businesses in cyclical sectors like leisure and professional services.

US economic activity for September. Manufacturing activity remains in contraction (ISM PMI 49.2), though contracting at a slightly slower rate than August; meanwhile, consumer confidence dipped (Conf. Board 95.8), and the decline in Pending Home Sales moderated (−0.4% MoM).

S&P Global PMIs. Global manufacturing activity showed a clear divide, with most major economies contracting: Severe Contraction in the West: Both the UK (46.2) and the Eurozone (49.5) reported contractions, with the UK slowing at a more severe pace. North American Weakness: Canada (48.3) remained in contraction, and Mexico’s manufacturing sector surprisingly fell into contraction at 49.6, dropping from 50.2 in the previous month. Asia’s Modest Growth: In contrast, China’s manufacturing sector continued its modest expansion, albeit easing slightly to 50.5.

Australia. The Reserve Bank of Australia (RBA) chose to hold the cash rate steady at 3.6% for the September meeting, matching the consensus expectation.

Week ahead

Markets in the fog

Blindfolded markets. US data releases from public sources are on pause due to the ongoing shutdown – with no clarity on when it may be lifted. The absence of fresh macro inputs leaves markets flying blind, amplifying reliance on private surveys and central bank communications.

Cut, then what? A key event will be the release of FOMC minutes from the September meeting. Unaffected by the shutdown, the minutes will shed light on the rationale behind the rate cut – and more importantly, where the board stands on next steps. Was this a pre-emptive one-off move, or the beginning of a broader easing cycle? We lean toward the former.

Tariffs vs. Momentum. A batch of macro data from the eurozone (retail sales) and Germany (factory orders and industrial production) will be key to assessing momentum across the bloc, which continues to grapple with a high-tariff rate environment imposed by the White House.

Shutdown stress test. University of Michigan sentiment data may add to the weak signals from PMIs and the Conference Board. While UMich captures a more recent reference period – thanks to its rolling survey methodology – we don’t expect notable improvement, given that the shutdown falls squarely within the timeframe covered by this release.

FX Views

No prints, no breakouts

USD No print, no pulse. The dollar declined for four consecutive sessions, before trimming some losses later in the week. The government shutdown deprived investors of key macroeconomic releases that could have supported the dollar, leaving markets unable to gauge whether the underlying momentum was still intact. While shutdowns are typically not major FX drivers, the political backdrop under Trump’s second administration has added weight. Repeated attacks on the Fed – targeting Powell and Cook – the dismissal of the head of the Bureau of Labor Statistics, and Trump’s stated intent to reduce the federal workforce in response to the shutdown have introduced a layer of political interference into an otherwise negligible risk event, exerting moderate pressure on the dollar. Also, with little data at hand, investors were left with weak sentiment indicators (Conference Board, PMIs) and underwhelming – though not outright bad – JOLTS data. The poor ADP print was largely discounted, as it stemmed primarily from a change in methodology. Altogether, nothing stood out that could have reignited the now-defunct data-driven rebound the dollar had enjoyed the previous week.

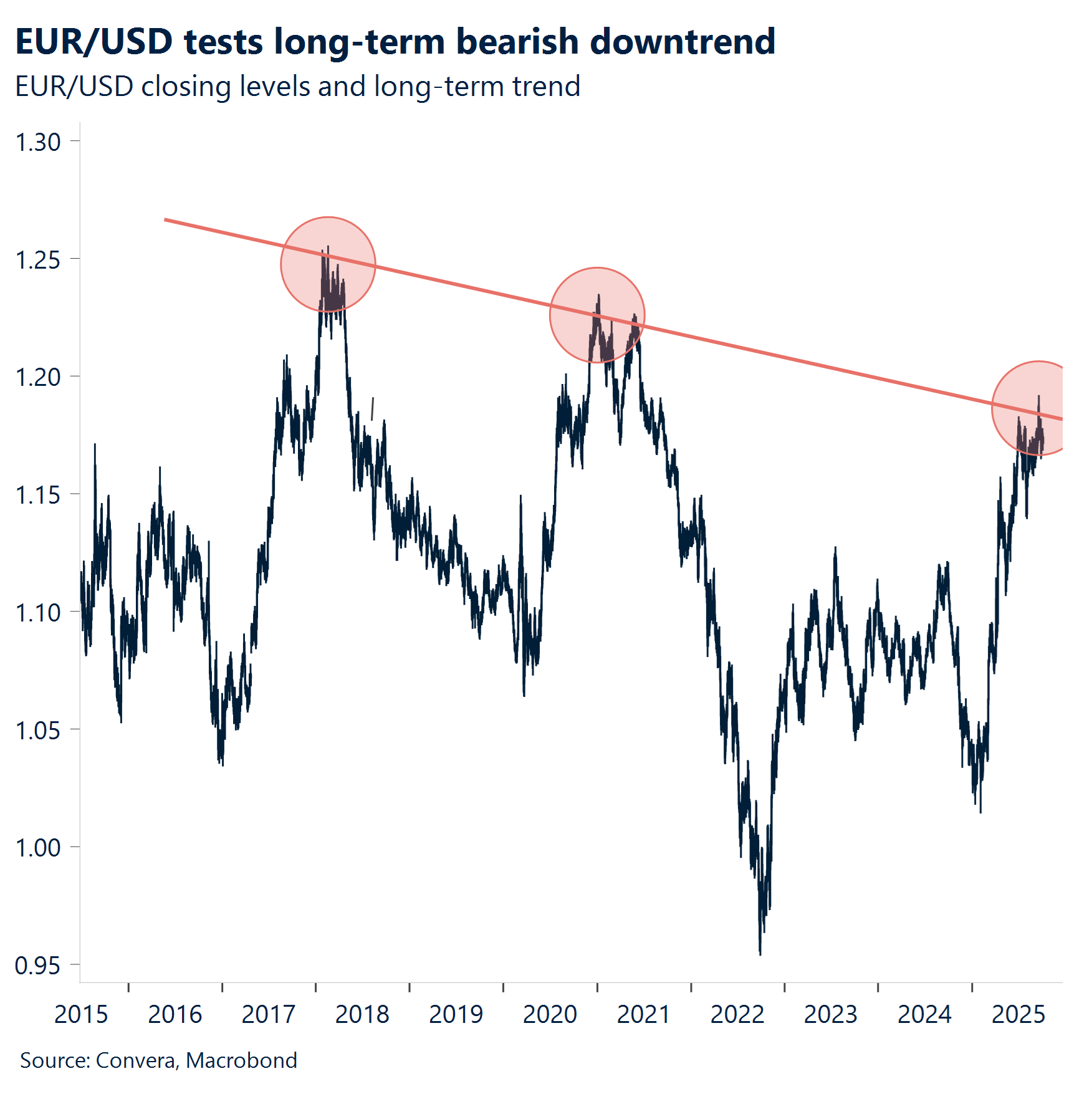

EUR Resistance holds, catalysts missing. With little further guidance from the ever-hawkish Fed, and ECB President Lagarde delivering more dovish remarks than expected, including comments that the path is not fixed and that the bank is open to further cuts, EUR/USD was unable to breach newly formed resistance at 1.1750 this week. A more convincingly dovish Fed is likely what the pair needs to break north of 1.18, but the euro rally is showing signs of fatigue, with no substantial catalysts on the horizon. On the data front, inflation releases were orderly, contributing to an overall benign price pressure environment, despite a negligible flare-up in the eurozone headline driven by energy base effects. That said, the risk of undershooting is elevated in the months ahead, with a stronger euro and lower energy prices being the main culprits. This may evolve into a non-negligible euro-negative as we head into 2026.

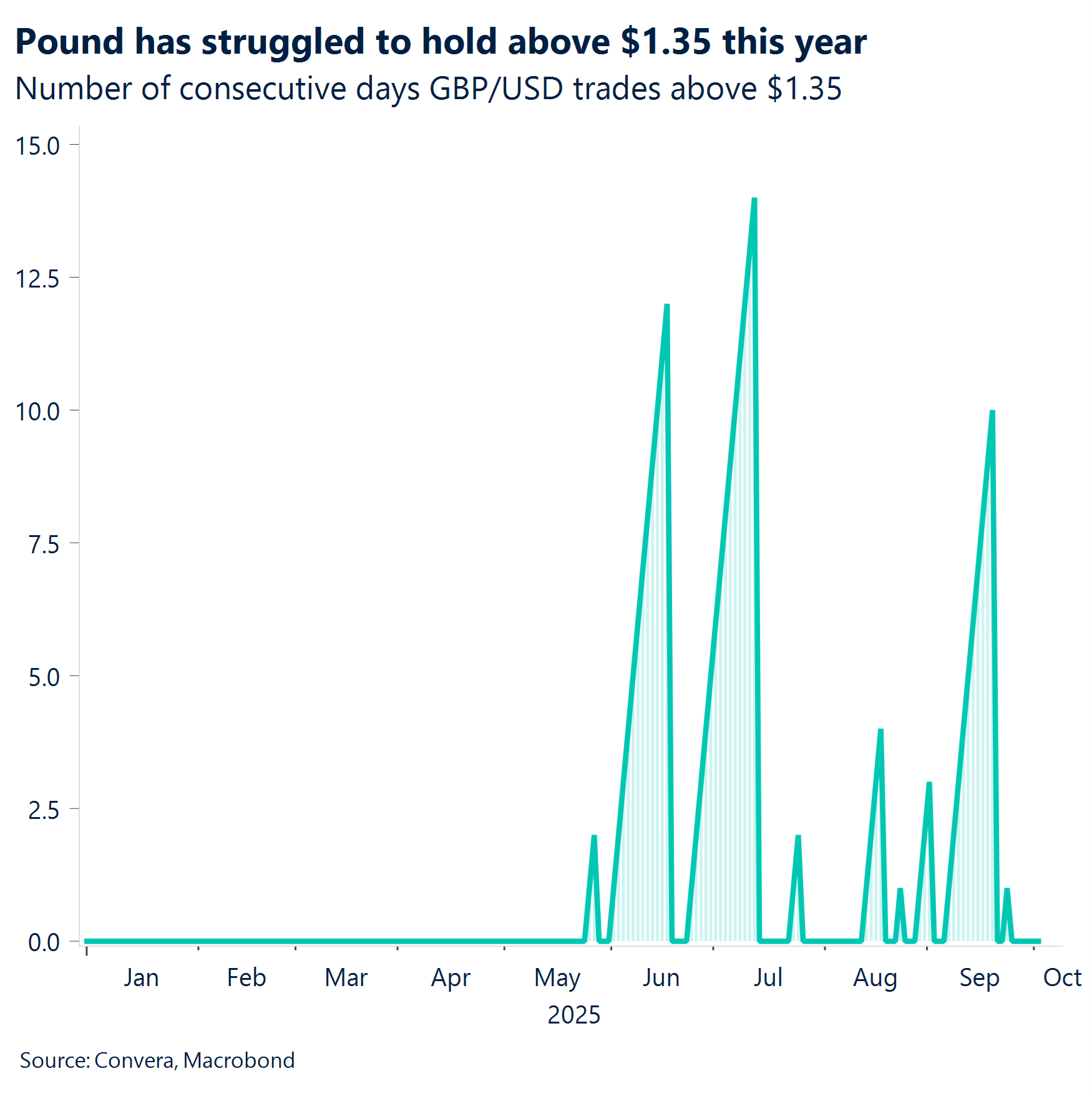

GBP Uphill battle. Sterling began Q4 on a relatively strong note within the G10 FX space, lifted by market relief following the Labour Party’s annual conference. Fears of a pivot toward aggressive fiscal expansion failed to materialize, easing a key political overhang for the pound. GBP/EUR briefly tested €1.15 before slipping to €1.1460, while GBP/USD climbed to $1.3527 before retreating – reinforcing the view that sterling remains sensitive to broader macro shifts. Despite the removal of near-term political risk, sterling’s struggle to hold intraday highs highlights lingering investor caution. In today’s low-volatility environment, GBP’s high yield should, in theory, offer support. But stagflation concerns, where inflation stays elevated while growth falters, continue to cloud sentiment. That backdrop makes investors hesitant to fully embrace the pound, even with its rate advantage. Still, if the Bank of England’s hawkish stance is backed by signs of economic resilience rather than just stubborn inflation, the case for sterling could strengthen. A more balanced narrative – where yield appeal is underpinned by growth stability – may prove more durable than markets currently expect.

CHF Two-sided story. The Swiss franc has surged roughly 14% against the USD this year, with USD/CHF breaking below 0.84 and remaining highly sensitive to U.S. growth and yield expectations. With the Fed easing in response to a cooling labor market, further downside in the pair looks increasingly likely. EUR/CHF, however, tells a different story. The SNB re-entered the market in Q2, purchasing CHF5.1 billion in FX – its largest intervention since early 2022. FX reserve data reveal a strategic shift: the euro’s share rose to 40.2%, while the dollar’s dropped to 36.5%. As a result, EUR/CHF has largely held above 0.93, hinting that the SNB may be defending this level as a de facto floor. Meanwhile, the softer-than-expected headline inflation print this week highlights the deflationary pressure from a strong franc – raising the prospect of a December rate cut by the SNB.

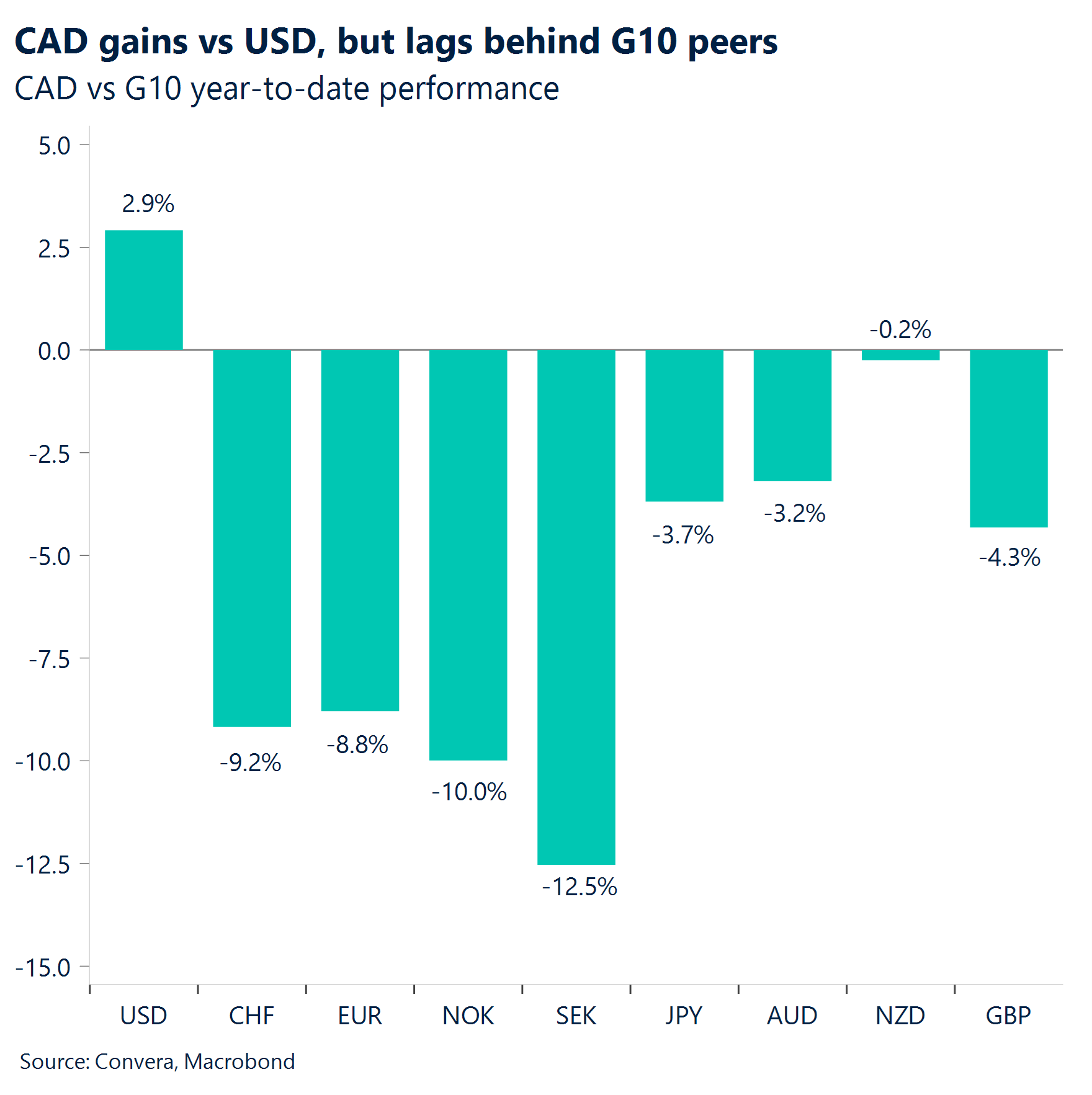

CAD Momentum stalled. In the absence of major catalysts for the week, the Canadian Dollar remains under pressure. Despite a generally softer U.S. dollar, the USD/CAD has traded within a tight, narrow range this week, holding between 1.389 and 1.395 after breaking above the 1.39 a week ago. Year-to-date, the CAD has exhibited marked underperformance relative to its G10 counterparts, with weakness being most pronounced against key European currencies. The currency’s struggle has led to notable valuation extremes: EUR/CAD is currently trading at its highest level since 2009, CHF/CAD has reached an all-time high, and SEK/CAD stands at its strongest level since 2021. While the CAD has registered a gain of approximately 3% when measured against the US dollar (USD), it remains the worst-performing G10 currency on a year-to-date basis. The USD/CAD pair’s upward momentum has stalled but continues to hold above the technically significant 1.39 level. The employment report due next Friday stands as the week’s most pivotal data release, poised to shape the Bank of Canada’s monetary policy direction ahead of its October 29th decision.

AUD Resilience tested as global risks rise. The Reserve Bank of Australia (RBA) highlighted increasing risks to the global financial system in its Financial Stability Review but expressed confidence in the resilience of Australia’s financial system. On the technical front, AUD/USD failed to sustain its 0.6500-0.6600 support zone after rejecting the 0.6683-0.6707 resistance levels. However, the medium-term positive trend remains intact above this key support. Looking ahead, upcoming building approvals and NAB business confidence data will be pivotal as market participants assess domestic economic resilience in the face of global risks.

CNH Weak China PMI keeps Yuan under pressure. China’s official manufacturing PMI showed contraction for the sixth consecutive month in September, printing at 49.8, marginally above estimates but still below the 50.0 threshold. New orders (49.7) and export orders (47.8) remained in contraction territory, reflecting subdued domestic demand and ongoing impacts from U.S. tariffs. The non-manufacturing PMI dipped to 50, slipping below expectations, suggesting broad-based economic softness. The absence of meaningful policy responses so far has left concerns about China’s growth trajectory unresolved. Next key resistance for USD/CNH lies at 50-day EMA of 7.1455 and 100-day EMA of 7.1695. Key support is at 21-day EMA of 7.1312. Upcoming trade balance data post-holidays will provide clues about export recovery but is unlikely to shift sentiment unless accompanied by significant policy adjustments.

JPY Yen steadies as factory slump deepens. Japan’s manufacturing PMI fell to 48.5 in September, signaling a deepening contraction in factory activity. Both output and new orders weakened, with sluggish demand from key export markets like China weighing on the sector. While domestic demand remains stable, the outlook for Japan’s manufacturing sector depends heavily on global recovery, especially in China and the U.S. Technically, USD/JPY rebounded strongly from its key support zone at 144.97-146.84 and is now testing the 148-150 resistance area. A breakout above this level could set the stage for a move toward 154.17-154.71. However, intervention concerns may limit upside momentum in the near term. Market participants will closely watch upcoming household spending and current account data, which could influence the yen’s direction amid heightened volatility.

MXN Weekly weakness. The Mexican Peso has traded within a narrow range at the start of both the month and the quarter, showing an upside bias that has pushed it to 18.5. In the absence of global macro news, the Peso has become more sensitive to domestic macro sentiment. Selling pressure has intensified near the lower bound, reinforcing 18.20 as a key short-term support level. Despite broad-based softness in the U.S. Dollar, the Peso has struggled to extend its momentum and break below this threshold. Signs of fatigue are beginning to surface, even as USD/MXN remains below its 20-, 40-, and 60-day moving averages, suggesting waning downside conviction. Economic data has added to the cautious tone. Mexico’s S&P Global Manufacturing PMI slipped to 49.6 in September from 50.2 in August, falling back below the 50.0 neutral mark and indicating a modest contraction in factory activity. Looking ahead, next week’s CPI report for September will be a critical input for Banxico’s monetary policy outlook. While inflation dynamics remain in focus, market consensus still anticipates two additional rate cuts from the central bank before year-end, bringing the benchmark rate down to 7%. Should the Federal Reserve also deliver two cuts, the interest rate differential is expected to remain near its historical floor, limiting the scope for Peso outperformance.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.