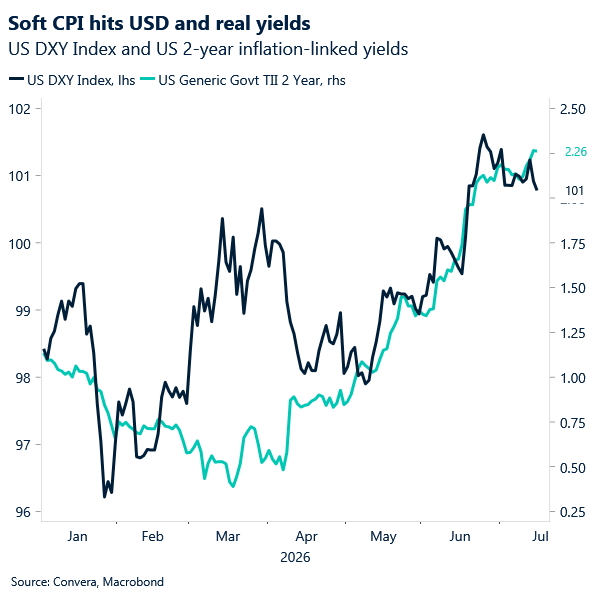

USD: Soft CPI reprises Fed risk

US inflation came in below forecast in June, giving markets a clear reason to fade the recent rise in Fed tightening risk. Headline CPI fell 0.4% on the month, compared with expectations for a 0.1% decline. The annual rate slowed to 3.5% from 4.2%, also below the 3.8% consensus. Core CPI was flat on the month, missing the 0.2% estimate. The annual core rate eased to 2.6% from 2.9%, undershooting expectations for 2.8%.

Energy did most of the work in pulling the headline figure lower, but the softer core print carried more weight for markets. The energy index fell 5.7% in June, led by a 9.7% drop in gasoline prices after earlier supply fears eased. Food prices rose 0.2%, while shelter climbed just 0.1%, its smallest monthly gain since January 2021. Core goods slipped 0.1%, while services excluding energy were flat. That mix gave investors more confidence that price pressure cooled beyond a one-off energy move.

The data quickly reshaped Fed expectations. Swaps largely priced out the risk of a July rate hike, while two-year breakevens fell sharply as inflation fears eased. Still, Fed Chairman Kevin Warsh pushed back against any “mission accomplished” reading of the report. That helped Treasury yields pare part of their initial decline as traders reassessed how far the Fed will lean into one soft CPI print. Inflation remains above the Fed’s 2% target, and geopolitical risks still argue for caution.

The US dollar moved lower as markets marked down the risk of a more hawkish Fed response. The decline looked more like a repricing of July FOMC risk than a deeper shift in the dollar’s broader outlook. A softer inflation print reduces the urgency for more tightening, but it does not automatically open the door to early rate cuts. As long as the labor market holds up and energy risks remain elevated, the Fed can remain patient. That leaves the dollar vulnerable near term, but not without support.

Markets reacted quickly to the downside CPI surprise. The two-year Treasury yield fell 8 bps on the day to 4.2%, even after paring some of the initial move. Stocks rose as lower yields eased pressure on risk assets. The dollar weakened across major pairs as traders adjusted Fed expectations. Attention is to continue on Warsh’s comments before Congress as well as PPI data for the month of June.

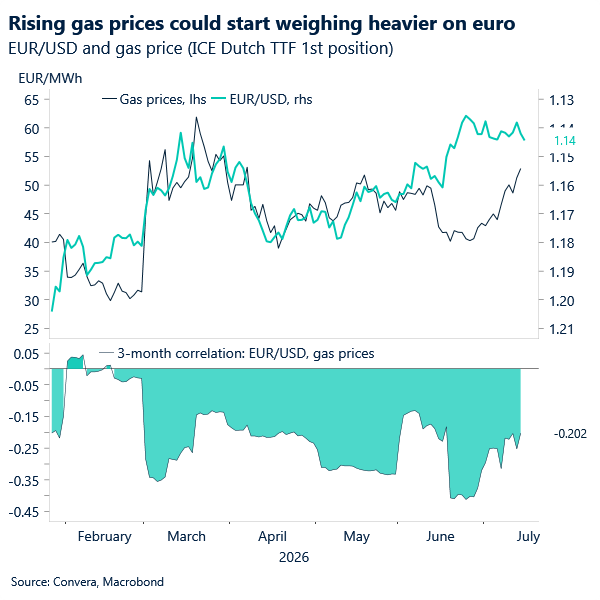

EUR: Holding up but energy risks are growing

Despite a 12% surge in oil prices this week amid renewed tensions in the Gulf, the euro has held up surprisingly well against the dollar. In fact, EUR/USD has reclaimed its 21-day moving average for the first time in a month, helped by a combination of softer-than-expected US inflation data and a hawkish repricing of ECB rate expectations.

For now, the rates market is providing the euro with a cushion. The EUR-USD two-year swap differential has narrowed by over 20bp since the start of July, reflecting a partial recovery in ECB tightening expectations at a time when Fed pricing has become slightly less aggressive. That shift has helped stabilise EUR/USD after several weeks in which widening yield spreads and US economic outperformance dominated the narrative.

However, it is too early to conclude that the euro has regained a sustainable footing. The key reason is energy. While crude prices have risen sharply, markets are not yet fully pricing a significant supply disruption, leaving the risk of further upside shocks. If energy prices continue to climb, the eurozone’s economy is likely to feel the impact more acutely than the US, reviving concerns around growth, inflation and competitiveness.

This highlights a theme that has defined much of the euro’s performance in recent months. ECB repricing can offer temporary support, but it struggles to outweigh the medium-term consequences of higher energy costs. That is particularly true if rising oil and gas prices begin to undermine growth prospects just as policymakers become less enthusiastic about further tightening.

The move in European gas prices is especially important. Unlike oil, higher gas prices have a more direct impact on the eurozone’s terms of trade and economic outlook. As a result, while rates are currently supporting EUR/USD, a continued escalation in energy markets could quickly reassert itself as the dominant driver.

GBP: Pound consolidates after strong run

GBP/USD climbed to test 1.34 yesterday after a softer-than-expected US June inflation report. The data pushed market expectations for the next Fed rate hike to October from September, although one additional hike remains firmly priced by year-end. But the Fed’s hawkish narrative is far from dead amid lingering geopolitical risks, meaning continued GBP/USD upside on a steady unwind of Fed tightening expectations looks unlikely in the near term.

A soft US Producer Price Index (PPI) reading today, coupled with a more conciliatory tone between the US and Iran, could see the pair make a more convincing attempt to break above 1.34.

Meanwhile, GBP/EUR has pulled back from a one-year high of 1.1772, declining for a second consecutive session. The move looks justified given how stretched the rally had become. The two clearest downside risks for the pair this month are who Andy Burnham, the prime minister-in-waiting, appoints as Chancellor of the Exchequer and June’s UK inflation report due next week.

Investors remain wary of the UK’s fiscal outlook, and a Chancellor perceived as more willing to increase public spending would likely weigh on sterling. Wes Streeting, the former Health Secretary, is widely viewed as the most market-friendly alternative.

On inflation, June’s UK CPI release (22 July) could follow the same disinflationary pattern recently seen in both the eurozone and the US. That would add downside pressure to sterling, particularly if reinforced by the MPC’s communication on 30 July. However, a more constructive inflation outlook from BoE officials will depend largely on how the geopolitical backdrop evolves, given the recent re-escalation in tensions.

All told, GBP/EUR appears more likely to consolidate within the 1.16–1.17 range in the coming weeks than to break meaningfully higher.

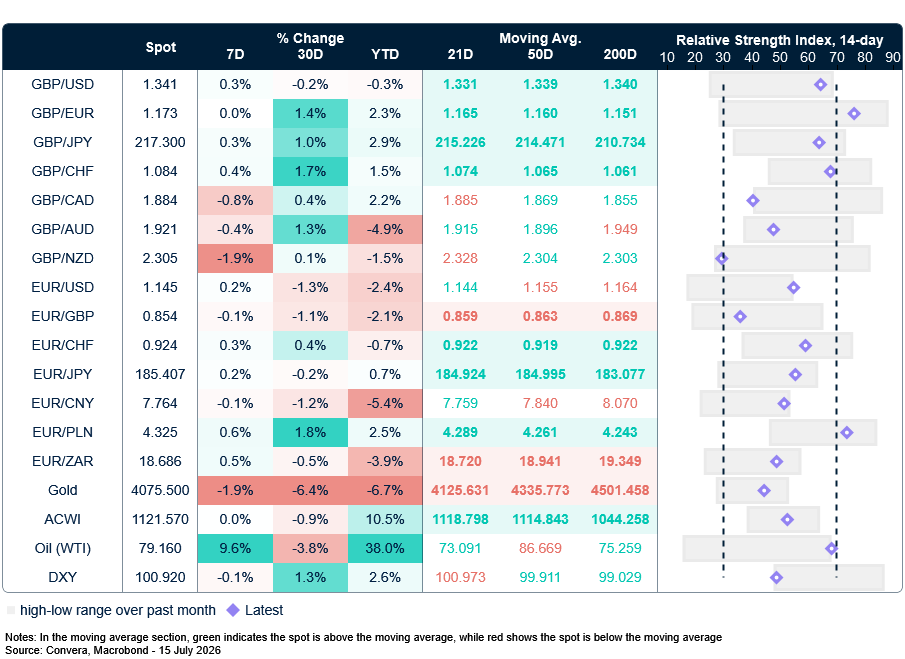

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

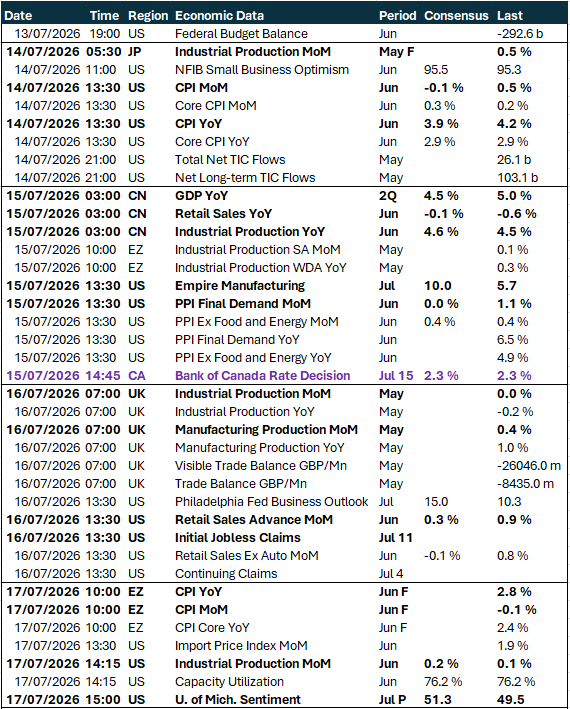

Calendar: July 13-17

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.