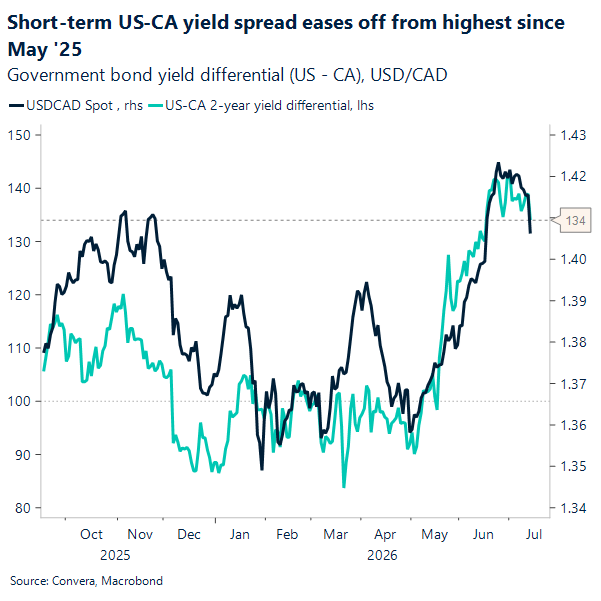

The Canadian dollar has gained ground against the US dollar after softer-than-expected US CPI pushed the greenback lower and cooled the recent rise in US yields. Firmer oil prices also helped, with WTI near $80 a barrel and Brent around $86 after the US and Iran exchanged weekend strikes. Still, the bigger driver for USD/CAD is the inflation story, since weaker US price data reduces the risk of a more hawkish Federal Reserve. That eases pressure on the loonie after widening yield spreads had worked against it over the past month.

The Bank of Canada now becomes the next major focus for CAD markets. The full decision package arrives this morning, with the statement, Monetary Policy Report and Governor Tiff Macklem’s prepared remarks due at 9:45 a.m. ET. The press conference follows at 10:30 a.m. No rate change is expected, with the overnight rate widely seen staying at 2.25%. The bigger question is how cautious the Bank sounds on inflation, oil prices, trade risks and the recent shift in global financial conditions.

The latest Canadian labor report is unlikely to shift the Bank’s thinking much. Job growth has cooled, but slower population growth makes that less troubling than it would have looked a year ago. On a per-worker basis, the labor market looks steadier, which leaves room for unemployment to edge lower later this year. Still, the elevated jobless rate should help contain wage pressure. That gives the BoC room to stay patient rather than push back hard against market pricing.

The Monetary Policy Report will likely carry the main signal for markets. The Bank may trim its 2026 growth view after a weak first quarter, while giving some credit to a stronger second-quarter rebound. Inflation forecasts could be revised higher if the Bank sees lasting pressure from energy costs, shipping costs or supply disruptions. The Bank is also likely to keep stressing excess supply in the Canadian economy, even as headline inflation remains uncomfortable. Any comments on the balance sheet will also be watched, especially after Macklem’s recent reference to a “steady state.”

USD/CAD has broken below 1.41 after spending much of the past three weeks between roughly 1.411 and 1.424. The pair is now trading closer to 1.405, helped by softer US inflation, lower US yields and a weaker Dollar. Higher oil prices offer another source of support for the loonie, but that tailwind may fade if energy markets stabilize. One US CPI print is not a trend, and markets are treading carefully as oil prices have rebounded. Warsh’s comments on not reigning on inflation yet add to the cautious backdrop. Domestically, a cautious BoC could limit CAD gains if Macklem keeps the door open to a long hold. At the same time, a more confident tone on disinflation, would likely add pressure on USD/CAD.

Cooler inflation pressures Dollar

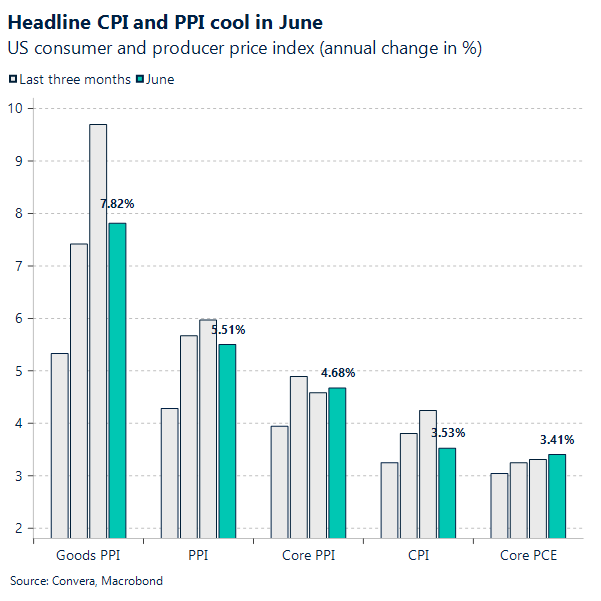

US inflation data has delivered a second downside surprise in as many days, adding pressure on the Dollar and easing fears of another Fed hike. Headline CPI came in below forecast on Tuesday, and June PPI followed with a 0.3% monthly decline, against expectations for a flat reading. Final-demand PPI slowed to 5.5% year over year, below the 6.2% consensus and down from 6.0%. Core measures also cooled, with PPI excluding food, energy and trade rising just 0.1% on the month. One print doesn’t make a trend, but back-to-back softer CPI and PPI reports give markets more reason to question how much tightening risk remains.

Energy again did much of the heavy lifting. Final-demand goods prices fell 1.4%, the largest decline since July 2022, led by a 6.4% drop in energy prices. Gasoline prices fell 12.0%, while diesel fuel, jet fuel and crude petroleum also moved lower. Food prices declined 0.6%, adding to the softer goods backdrop. Services were firmer, rising 0.2%, but not enough to offset the broader pullback in producer prices.

The PPI report reinforces the message from CPI that inflation pressure cooled in June. Core CPI was flat on the month, and core PPI excluding food, energy and trade rose only slightly after a much stronger May gain. That combination has helped markets move away from the idea of a July rate hike. Still, Fed Chairman Kevin Warsh has pushed back against any “mission accomplished” reading of the data. That keeps investors cautious, even as inflation surprises are finally moving in the Fed’s direction.

For the US Dollar, the data has shifted the short-term balance lower. Softer CPI and PPI reduce the appeal of chasing the Dollar on Fed hawkishness, especially as front-end yields and real yields adjust lower. The move looks more like a repricing of near-term Fed risk than a full breakdown in the Dollar backdrop. Inflation remains above target, energy risks have not disappeared, and the labor market is still holding up. Those factors should limit how far markets can price early easing for now.

Markets reacted by leaning further into a less hawkish Fed path. The two-year Treasury yield fell after CPI and remains sensitive to softer inflation data, even as yields have pared some of the initial decline following Warsh’s comments. The Dollar traded lower across major pairs as rate-hike expectations faded. Stocks found support from lower yields and a reduced risk of near-term Fed tightening. The next test is whether Warsh’s congressional remarks reinforce that caution or allow markets to keep extending the post-CPI and PPI relief trade.

Softer US Dollar helps Peso

The latest US CPI and PPI downside surprises have added a new tailwind for Mexican assets. Softer-than-expected inflation helped cool concerns that higher oil prices would force the Federal Reserve back toward a more hawkish stance. US yields fell, the Dollar weakened, and rate-sensitive trades found fresh support. For Banxico, the local inflation story still drives policy, but a softer US inflation print reduces external pressure. It also gives investors more room to lean into Mexico’s carry advantage.

Banxico’s June minutes showed more confidence in disinflation, but not enough to restart the easing cycle. The board kept the policy rate at 6.50% and signaled that a prolonged hold remains the preferred path. Slack in the economy, peso strength and fading inflation shocks support that stance. Sticky services inflation still keeps Banxico cautious and limits the case for near-term cuts. That leaves the central bank patient, even as the inflation backdrop improves.

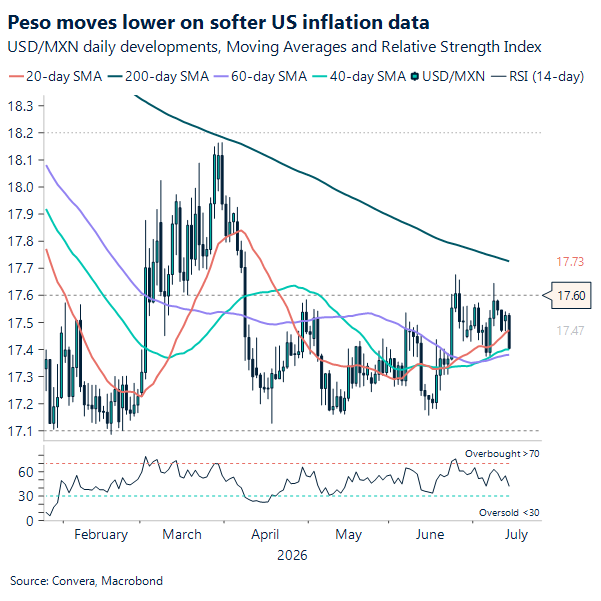

For MXN, the setup remains constructive. USD/MXN is trading near 17.40, down about 0.7% yesterday as the Peso gains from the weaker Dollar backdrop. The pair has moved lower after failing to sustain a push toward the 200-day moving average near 17.73. Short-term moving averages still point to some consolidation risk, but momentum has cooled from overbought levels. Global sentiment, US yields and the Dollar may remain the bigger drivers for the Peso this week.

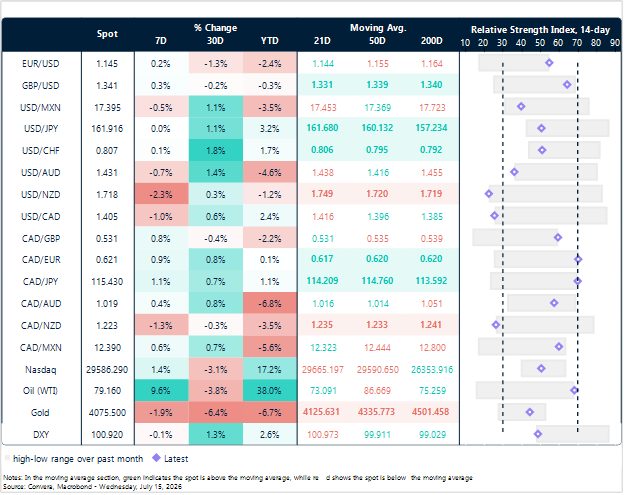

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

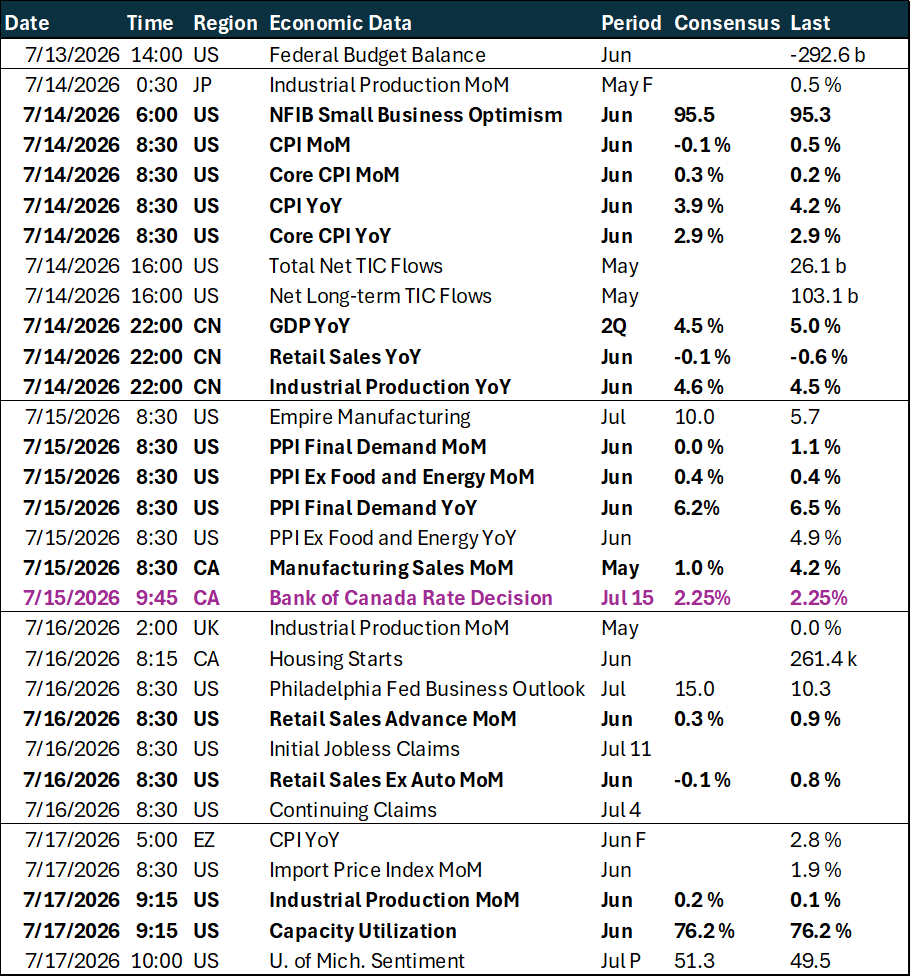

Calendar: July 13 – 17

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.