The new tariff is political interference

August saw the Dollar Index (DXY) drop just over 1.5%, with 97.600 acting as a key support level. Two major bearish events contributed to the steepest sell-offs: first, on August 1st, a disappointing Non-Farm Payroll (NFP) report was followed by the dismissal of the head of the Bureau of Labor Statistics (BLS). Then, on August 22nd, building on the earlier developments, Fed Chair Jerome Powell emphasized that a weakening labor market could open the door to a rate cut in September. Outside of these events, the DXY remained range-bound between 97.600 and 98.500.

The Fed’s policy rate trajectory – alongside the evolving narrative around central bank independence – continues to be the dollar’s most influential driver, alongside broader U.S. macroeconomic data. This week, those forces played out over a compressed time frame, causing the dollar to whipsaw. On Monday, markets digested the Jackson Hole symposium and Powell’s remarks about a higher post-GFC neutral rate, which implies elevated rates today despite entering a potential cutting cycle. The dollar rose by approximately 0.7%, but gave back about half of those gains yesterday following threats by former President Trump to dismiss Fed Governor Lisa Cook.

Based on August’s performance, therefore, the sentiment-driven narrative has shifted from tariff-related noise to concerns over Fed independence. The former has evolved into concerns that tariffs may adversely affect the U.S. economy, with some data evidence suggesting that tariffs, and the uncertainty around them, has dampened economic activity and weakened the labor market – this month’s NFP report being the clearest indication. The latter stands today as the dominant, despite weaker, force in dollar movements. It will be interesting to see whether, in the longer run, the Fed independence narrative, unlike the tariff story (which primarily led to dollar weakness via the hedging channel), can trigger outright selling of U.S.- denominated assets – particularly at the long end of the Treasury curve.

Fragmentation risk returns

While yesterday’s Fed saga developments ultimately dominated headlines and overshadowed the French debacle, with EUR/USD closing 0.33% higher, the pair oscillated during the day between 1.1600 and 1.1650 amid these contrasting forces. The market-moving power of the former has been clearly demonstrated, yet it remains uncertain to what extent the likely collapse of the French government will exert downward pressure on the euro.

At a time when the unity of the European Union has already been challenged – most recently by a poorly negotiated trade deal – we believe the euro is more vulnerable than usual. Fragmentation within the bloc becomes a more significant weakness precisely when cohesion is most needed.

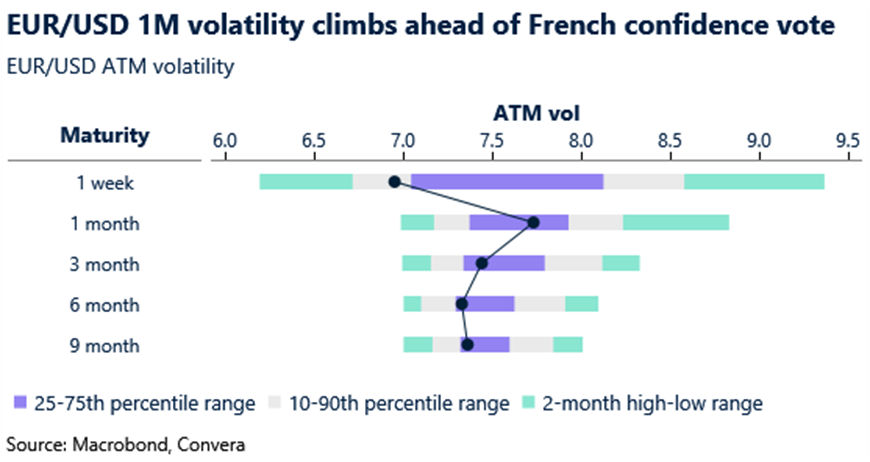

In response, we observe one-month EUR/USD volatility trading higher relative to other maturities, as September shapes up to be a pivotal month for France. The confidence vote on September 8, 2025, will determine whether Prime Minister François Bayrou’s government survives.

What’s next for sterling-euro?

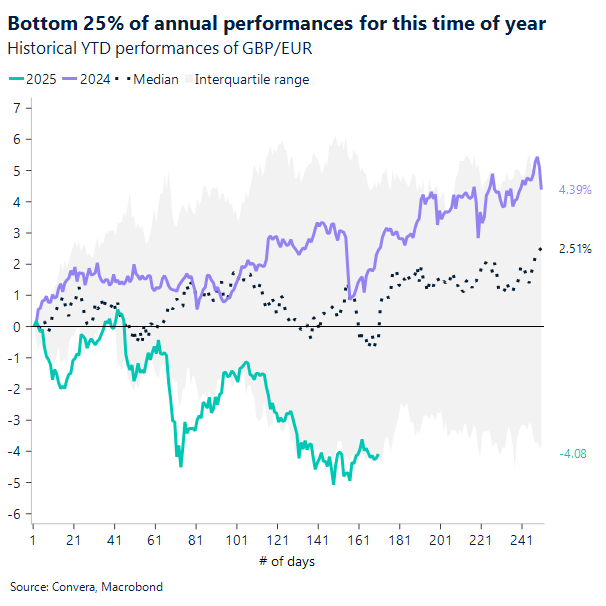

GBP/EUR has fallen over 4% year-to-date, placing it in the lower quartile of its historical performance range for this time of year. The decline has occurred despite the UK’s yield advantage, highlighting how structural forces – such as Germany’s fiscal expansion and eurozone capital inflows – are increasingly outweighing traditional rate-based fundamentals in driving FX trends.

Rate and growth differentials between the UK and eurozone have remained broadly stable since late 2024, offering little fresh directional impetus. Instead, the euro has benefited from a broader reallocation of FX flows, absorbing demand that might otherwise have supported the dollar. Germany’s fiscal stimulus – anchored in record infrastructure and defence spending – has further supported the euro by boosting long-term growth expectations and overshadowing the ECB’s dovish pivot.

In the near term, rising political tensions in France may offer the pound some reprieve, weighing on the euro. This coincides with a gradual upturn in the 21-day moving average, adding technical momentum to GBP/EUR, whilst implied volatility has compressed to multi-month lows, often a precursor to a more decisive directional move. A close above €1.16 this week would mark the first breakout above this level since early Q2 and could signal a move beyond the summer range of €1.14–1.16. However, caution is warranted – previous breakouts have quickly reversed, and without sustained macro or political follow-through, the risk of another false move remains high.

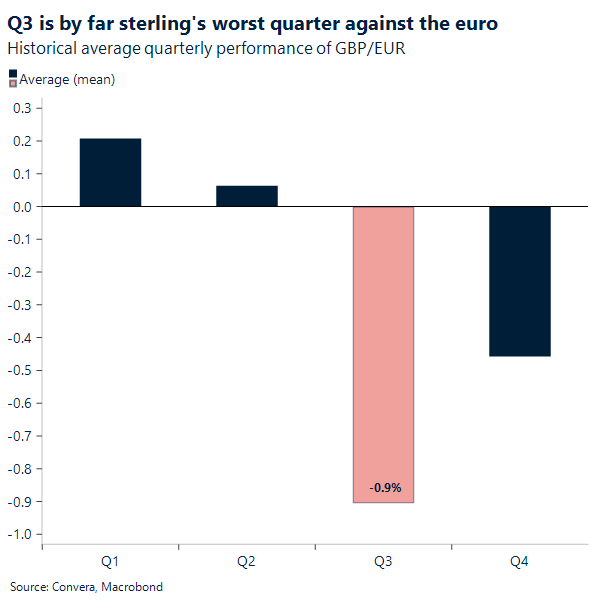

Moreover, seasonally, GBP/EUR tends to underperform in Q3, showing a median decline of ~0.9%. The currency pair is currently tracking 0.7% lower quarter-to-date – adding another layer of resistance to any sustained rally.

Looking further ahead, sluggish UK growth and looming fiscal challenges could return to weigh on the pound this autumn. If the BoE is seen as constrained by persistent inflation while growth risks remain elevated, any support for sterling via the yield channel may prove short-lived and fragile.

Sterling’s short-term performance weakens

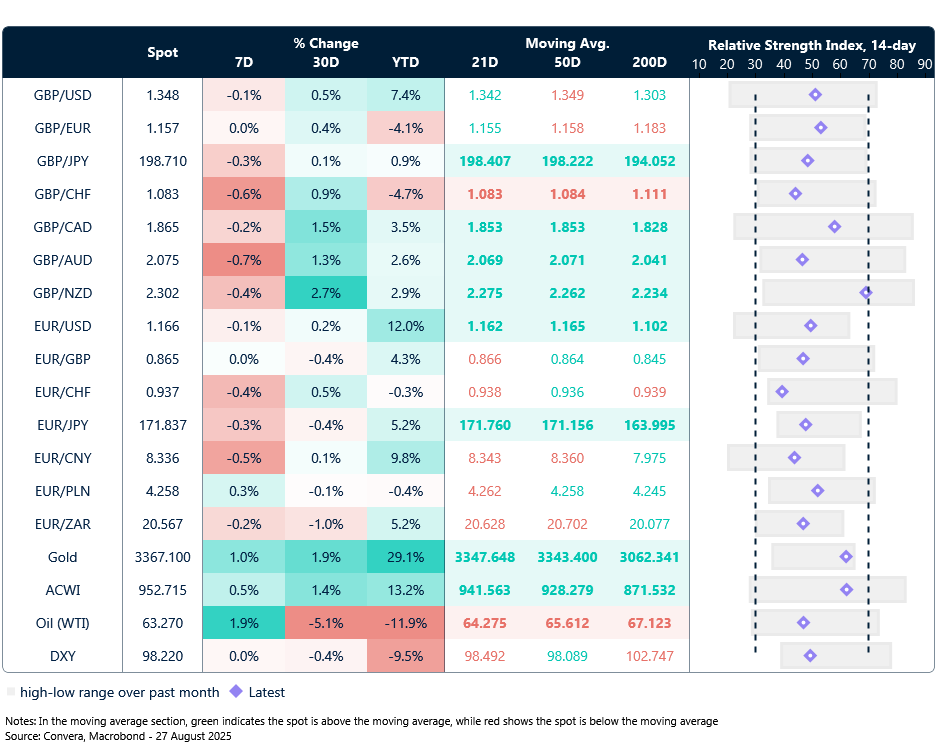

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: August 25-29

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.