Inflation continues to be the main driver of price action as shown by the market reaction to the upside surprise in the US Employment Cost Index. Most inflation indicators have trended higher, suggesting that Q1 was an inflationary month.

The Fed opted to keep interest rates at a 23-year high while voicing fresh concerns about the lack of progress on inflation. However, the pushback against rate hikes by Jerome Powell does signal that peak of Fed hawkishness has been reached.

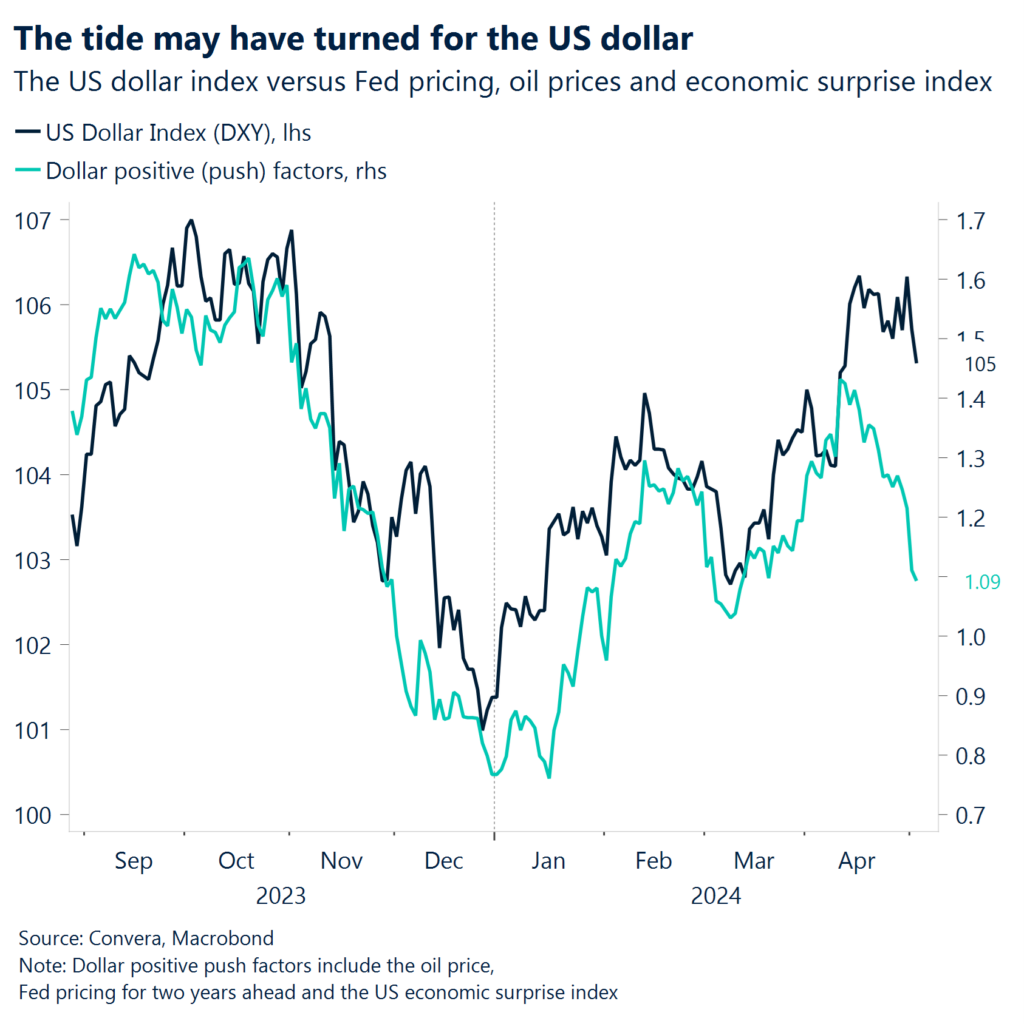

The US dollar came on top of its peers in all months so far this year. However, Jerome Powel’s reluctance to put rate hikes back on the table and weak jobs growth overshadowed inflation and pushed the Greenback to its worst week in 2024.

Downside surprises on survey data this week like the manufacturing PMI, consumer expectations and small business optimism are starting to mount as the US added less people (175k) to its workforce than expected (310k) in April.

An ECB rate cut at the June meeting appears a done deal, with money markets pricing in an over 90% probability of a 25bps cut. What happens thereafter remains contested. It’s an even more complicated picture for the Bank of England.

It seems likely Japan intervened in FX markets twice this week after the USD/JPY exchange rate hit the highest level since 1986 at 160¥.

For the first time in a while, US (and Eurozone) data will play second fiddle to the incoming macro releases out of the United Kingdom with the BoE set to meet.

Global Macro

High inflation, neutral Fed and intervening Japan

A precarious month. April has been about many things. In the United States, it was about inflation surprising to the upside and investors pricing out rate cuts from the Fed. In Asia, it was about a strong dollar leading central banks to verbally and physically intervene in FX markets to prop up demand for their own currencies. And in Europe, it was about confirming the bottoming of economic activity. The US dollar came on top of its peers in all months so far this year. However, Jerome Powels reluctance to put rate hikes back on the table pushed the Greenback to its second worst week in 2024.

Q1 was inflationary. April gave us closure on the first quarter of the year with all data points now being published. The main conclusion can be drawn and its one of inflation having picked up. All three US inflation prints this week in the form of the Employment Cost Index, unit labor costs and the price-component of the manufacturing PMI surprised to the upside. European data painted the same picture of the disinflationary process stagnating. However, the Fed meeting overshadowed the macro data and led bond yields lower on both sides of the Atlantic.

Which data to follow? Hard data like industrial production, retail sales, inflation and goods orders have surprised to the upside in Q1. But just over the past two weeks we got downside surprises on the purchasing manager index, consumer expectations falling to their second-lowest level since 2013, small business optimism falling to the lowest level in 11 years and most labor market indicators pointing to a moderation of hiring.

Markets forcing Japan’s hand. It seems likely Japan intervened in FX markets twice this week after the USD/JPY exchange rate hit the highest level since 1986. While we will have to patiently wait for an official statement from the Ministry of Finance until the end of May, the timing and extent of the FX move do suggest that officials were involved in buying the yen on the market for the first time since 2022.

Deep Dive

Peak Fed hawkishness despite higher for longer

April was quite an interesting month. Not only did it close out the economic data from the first quarter of the year, but it also flowed neatly into the Fed’s rate decision that happened on Wednesday on the first of May.

Unfortunately for investors, the month ended like it began, with US inflation figures surprising to the upside.

At the beginning of the month, markets placed the probability of the Fed not cutting rates at all this year at basically zero percent. But the upside surprise of every possible inflation print changed that. They highlighted that Q1 overall was an inflationary month. And market positioning shifted accordingly as the probability of the Fed fund rate remaining unchanged throughout 2024 rose to 25%. The big anticipation going into the FOMC meeting was that policy makers would shift to a slight hawkish bias. Fed chair Powell did acknowledge that the central bank failed to make any progress on the inflation front in Q1 and that it would take a bit of time for inflation to return to target. This most likely cemented the higher for longer narrative and justifies postponing rate cuts until Q3. However, what took markets by surprise is that Powell pushed back substantially against the idea of the Fed considering to raise interest rates again.

This means that the bar for rate cuts is high but the one for rate hikes is even higher, putting the Fed in a dovish to neutral position for the next six months.

This week’s meeting could be seen as the peak of Fed hawkishness in hindsight as it is unlikely that the inflation surprises from Q1 can continue to such an extent in the coming quarters. Given recent commentary, policy makers are aware of it and looking at the recent weakness of leading indicators from surveys, they are conscious about not overtightening.

Regional outlook: US

Hoping to put Q1 behind us

Unchanged policy. As expected, the Fed signaled fresh concerns about inflation while opting to keep interest rates at a 23-year high yesterday. The decision was again unanimous following a slew of data that pointed to lingering price pressures in the US economy. US yields fell and the US dollar weakened though as Fed Chair Powell ruled rate hikes “unlikely”.

Employment costs elevated. Inflation continues to be the sole driver of price action as shown by the market reaction to the upside surprise in the Employment Cost Index. Growth of 1.2% q/q is a big deal, as all seven categories recorded an increase in wage growth in Q1. It was once again the government sector (as with the NFP and GDP prints) that caused the volatile deviation from consensus. Wages in the public sector jumped by 1.7%, the most since 2007.

Jobs growth down, by a lot. The US jobs report disappointing expectations across the board with the unemployment rate rising, hiring growth moderating and average hourly earnings increasing by less than anticipated. The US added 175 thousand people to its workforce in April, a step down from the 315 thousand created in March and less than the consensus forecast of 240 thousand. Wage growth moderated to just 0.2% on an monthly basis, putting the 3-month annualized rate at 2.8%, the lowest pace since the beginning of 2021. Market pricing back at two rate cuts for the Fed in 2024 with the easing cycle starting in September.

Weaker leading indicators. The Chicago PMI and CB consumer confidence index surprised to the downside with the expectations component falling to the second-lowest level since 2013. Job openings followed suit and fell to the lowest level in three years as the quits and hiring rates continue to moderate below pre-pandemic levels.

Regional outlook: Eurozone

Q1 recovery clouded by disinflationary slowdown

Last mile to 2% could prove sticky. The preliminary report showed that German inflation stalled at 2.2% y/y in April, although below market consensus (2.3% y/y), as a slowdown in services inflation was offset by a rebound in food prices and a smaller decline in energy costs due to the end of a temporary tax cut on natural gas this month. The core inflation, excluding volatile items like food and energy, dipped to 3.0% in April, its lowest level since March 2022. Meanwhile, headline Eurozone inflation remained steady at 2.4% y/y with core cooling further to 2.7% y/y.

Recession dodged. The Eurozone economy expanded by 0.3% in Q1 2024, the fastest growth rate since the third quarter of 2022, and substantially above market expectations (+0.1%). Among the currency bloc’s largest economies, both German and the French GDPs expanded by 0.2%, while Italy’s grew by 0.3% and Spain’s expanded by 0.7% – all above market estimates. On a yearly basis, the bloc grew by 0.4%, above the expected 0.2% figure.

June cut, and then what? An ECB rate cut at the June meeting appears a done deal, with money markets pricing in an over 90% probability of a 25bps cut. What happens thereafter remains contested. The recent reacceleration of inflation in the US is raising concerns of inflation spilling over into the common bloc, while the recent increase in oil prices, as well as a weaker euro exchange rate, could very well push inflation expectations higher due to domestic reasons. The only thing that markets fear more than a higher-for-longer regime, is a policy mistake. If there is not a clear need to cut, this is one more reason to wait and see.

Week ahead

Calm after the storm – dominant UK week ahead

Move over, US. Over the next couple of days, investors will try to recover from the volatility caused by the plethora of critical data releases and the Federal Reserve’s rate decision. For the first time in a while, US data will play second fiddle to the incoming macro releases out of the United Kingdom.

Macro to matter on the edges. The main question going into the week will be how likely the hawkishness markets have placed on the Bank of England is justified given the expected fall of inflation to around 2% at the middle of the year. We are closely watching the BRC sales monitor, House Price Index and new car registrations on Tuesday, the S&P Global UK report on jobs and the BoE rate decision on Thursday and the GDP report on Friday.

Bank of England in the spotlight. British policy makers are broadly expected to hold policy rates unchanged. However, there seems to be a gap between our heightened risk of a June cut versus markets pricing in the beginning of the easing cycle in November.

RBA flipflop. The Australian central bank could deliver on expectations of switching into a more hawkish stance following upside surprises on the labor market and inflation in Q1. This comes just after policy makers started leaning more dovish in March. Markets are not expecting the RBA to start its easing cycle until the end of next year, making the central bank one of the latest to cut interest rates.

FX Views

Fed keeps dollar bulls in check

USD Worst week of 2024. After appreciating against over 60% of global currency peers in April, the US dollar has started May on the defensive, with the dollar index falling 1.4% over the week, to 3-week lows. Upside inflation surprises have been driving USD outperformance so far this year, but after Fed Chair Powell tempered concerns of another US interest rate hike, US yields pulled back to near 1-month lows, taking the steam out of the stronger dollar, whilst the weak US jobs report sent the US currency tumbling further. This year, traders have flipped from betting $10bln against the buck in January to gambling over $36bln on a rise, in parallel with market expectations for rate cuts being severely dialled back from six to just one in 2024. Thus, a contrarian strategy, going against prevailing market trends, is growing in appeal, especially if we’ve now seen the peak hawkish sentiment towards the Fed. But the Fed is responding to unfolding economic data, so the next few months of data are pivotal for the policy path and therefore the dollar.

EUR Tests 3-week highs. With an action-packed week, 1-week EUR/USD realised volatility lifted to an over 2-week high at 6.8% (ann.). Despite such backdrop, the performance proved insufficient to close the gap to this month’s bid open and the pair recorded a fourth consecutive monthly loss in April – its worst monthly run since Q3 2022. With the Fed reluctant to turn hawkish during May’s meeting, bearish euro sentiment eased. 1-week risk reversal bias towards puts scaled to the most more neutral position since Mar 13th and EUR/USD 3-month butterfly option volatility, an indication of demand for tail risk protection, declined to a near 1-month low, with markets less concerned about the near-term adverse euro weakness, despite the time horizon capturing the June ECB rate decision. That is not to say there won’t be any. Euro has a history of losses in May, depreciating by an average of 0.68% since 1971 against the Greenback. Having wrangled out of its recent $1.065-$1.075 range, the euro now faces strong resistance at $1.0798 (200-day SMA), that could hinder its ascent, but a break past this level could see the euro climb to $1.0840 (100-day SMA), recouping its April losses.

GBP Strong bounce, but headwinds ahead. The lack of UK data of late has seen sterling at the mercy of external events, particularly in the US and Japan, which saw realised weekly volatility in GBP/USD and GBP/JPY hitting 9% and 22% (annualised) respectively, the latter twice its 5-year average. UK Gilt yields have pulled back sharply from 5-month highs, alongside global peers, after the Fed allayed fears of another interest rate hike, supporting a rebound in global risk appetite. GBP/USD jumped above its 200-day moving average around the $1.2550 mark and now sits 2.6% higher than its recent year-to-date low of $1.23 but still 2% lower than its 2024 high near $1.29. Seasonal headwinds loom though as GBP/USD has fallen during May in 11 out of the past 13 years, averaging a 1.7% decline over the month. In anticipation, speculators moved to a net-short GBP position at the end of April for the first time since November last year. Sterling is also vulnerable to a dovish repricing in the BoE’s rate outlook. Markets are currently pricing in a 65% chance of a rate cut by the BoE in August and a slim chance of a second cut before year-end. However, any dovish remarks by the BoE at its upcoming meeting could put more rate cut bets back on the table, weakening the pound’s yield advantage.

CHF Rebounds after CPI surprise. After touching a 7-month low against the US dollar on the first day of the month, the Swiss franc rallied strongly due to a hotter-than-expected Swiss inflation report. Daily USD/CHF realised volatility hit 11% (annualised), well above the 5-year average of 7%, whilst EUR/CHF also tumbled, back under 0.98, which is proving a tough resistance level for the pair to hold above. The franc’s rally might not have legs though given this is just one inflation print and the Swiss National Bank (SNB) was always projecting a rebound in price pressures this quarter. Average CPI for the first quarter was 1.2%, in line with the SNB’s target, hence the central bank commenced its easing cycle last quarter and is expected to deliver at least one more cut this year. The Swiss franc has appreciated against less than 20% of global currencies so far this year due to the early dovish tilt by the SNB and we expect further weakness, assuming no black swan events or rise in geopolitical tensions sparking safe haven demand.

CNY China’s divergent manufacturing surveys. The outlook for the Chinese economy remains mixed. China’s official manufacturing PMI for April came in at 50.4, slightly above expectations of 50.3 but slower than March’s 50.8 reading. While production expanded faster, new orders and export orders grew at a weaker pace, suggesting some loss of momentum. In contrast, the Caixin/S&P Global PMI showed the fastest expansion in 14 months at 51.4, beating forecasts. This private survey highlighted robust external demand, with new export orders rising at the quickest pace in nearly 3.5 years, contrasting with the official data. The divergence between the two PMI surveys, which focus on different-sized companies, underscores the uneven nature of China’s economic recovery. The USD/CNY was impacted by USD/JPY weakness and fell back to one-month lows. That said, the USD/CNY might return towards 7.3000 in the upcoming months, contingent upon expectations of increased tolerance from the PBoC. This week, Caixin Services PMI, trade balance and CPIs will be key economic data to watch.

JPY Japan takes a stand. A very significant week for FX markets after the USD/JPY hit new 34-year highs above 160.00 before Japanese authorities finally reacted to the red-hot rally and intervened in FX markets on 29 April. While Japan’s Ministry of Finance refused to confirm or deny any intervention, both the Wall Street Journal and Dow Jones News Wires confirmed the move was led by Japanese authorities in off-the-record interviews. Further suspected intervention was seen after Wednesday’s Fed decision pushing USD/JPY below 153.00. From here, speculators might be cautious pushing USD/JPY back above 160.00. From an economic perspective, Japan’s au Jibun Bank manufacturing PMI climbed to an eight-month high of 49.6 in April from 48.2 previously, nearing the key 50 level that separates expansion from contraction. With expectations of higher sales ahead, manufacturers added workers and raised selling prices to 11-month highs despite broad-based increases in input costs. For USD/JPY, an initial pullback towards previous cycle peaks near 151.945 would likely find support. A sustained break below 149.80-151.40 could confirm a trend reversal. In the upcoming week, all eyes will be on au Jibun Bank Japan Services PMI, household spending, and current account this week.

CAD Converges towards $1.36. Slowing Canadian growth momentum in the form of disappointing Q1 GDP and PMI reports saw the markets increase their bets for near term BoC rate cuts, with the swap implied probability of a 25bps easing in June up to 68% (+19pp w/w). Less favourable domestic backdrop pushed USD/CAD to a near 2-week high of $C1.3780 and saw the Canadian dollar shed over 1.5% in April – its fourth worst performance against the Greenback across the G10. However, the Loonie’s lacklustre performance was salvaged by a US dollar selloff on the back of a less hawkish than anticipated FOMC meeting and Friday’s NFPs. The back end of the Canadian sovereign yield curve declined, closely tracing the developments in US Treasury yields, while tighter US-CA 2-year Treasury spread contributed to an overall CAD rebound by week’s end and its 3rd consecutive weekly win. 1-month USD/CAD implied volatility remained near 5-month high, driven by macro volatility. With the pair past the 35-day SMA support level, CAD will be met with resistance at 50-day SMA around $1.3606 before the psychological level, and a former 2024 ceiling, of $1.36 can be challenged.

AUD Australian manufacturing PMI signals cautious recovery. AUD/USD has been recently stronger, reaching three-week highs, after last month’s Q1 CPI reading was higher than expected. Money markets don’t have a full rate cut priced in until August 2025. More recently, a poor retail sales number was balanced by stronger manufacturing PMI, up to 49.6 in April from 47.3 previously, indicating the sector is inching closer to expansion territory. While output and new orders improved, activity remained below the neutral 50 level. Cost pressures intensified due to expensive raw materials and a weaker Australian dollar, leading to higher input and output price rises. While AUD/USD has crept higher, more broadly, the pair is stuck within its January-March range, and the medium-term bias remains negative until a break above key resistance in the 0.66 area. The Aussie’s been stronger versus European currencies, the kiwi and, of course, the Japanese yen. Tuesday’s RBA interest rate decision will be critical with retail sales and building approvals also in focus.