- Relentless resilience. Equities continue to look through inflation and energy risks, with the S&P 500 on track for its longest winning streak since 2023, supported by persistent AI‑driven optimism and renewed hopes of US–Iran de‑escalation.

- De-escalation fatigue. However, markets have grown more cautious about chasing positive geopolitical headlines, with weaker reactions to “final stage” negotiations reflecting reduced conviction in the peace trade.

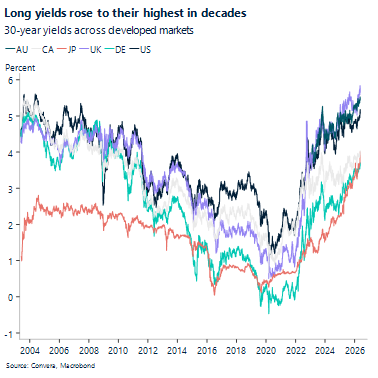

- Historic sell-off. The dominant macro story has been a global bond sell-off led by the US long end, with bearish steepening driven by rising inflation fears. The sharp moves started to cool off by week’s end, but remain a key concern.

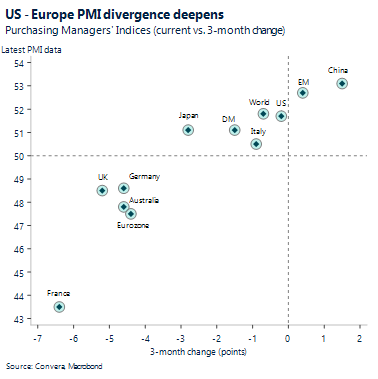

- Higher oil, harder landing. The combination of elevated energy prices and tighter financial conditions is raising concerns about a stagflationary drag on global growth. Weak European PMIs are thus forcing a repricing of ECB tightening expectations lower.

- Dollar’s quiet rebuild. FX has been re-anchored to real yield dynamics, with higher US rates emerging as the primary driver of dollar strength, overtaking geopolitics in importance. A blend of yield support, haven demand, and relative growth outperformance gives the USD an edge over its peers.

- Long weekend, low liquidity. Heading into the long weekend across Europe and the US, market liquidity is likely to thin, which could amplify short‑term price moves and leave markets more sensitive to headlines.

Global macro

Growth divergence deepens as Europe PMIs break

PMI breaks. The growth pulse in Europe deteriorated sharply: the UK Composite PMI (May flash) fell into contraction at 48.5 vs 51.6 expected, the first drop below 50 in over a year and driven by a steep services decline. The Eurozone Composite PMI also disappointed at 47.5 vs 48.8 expected, confirming the growth downshift and reinforcing a “Europe weakening” macro tone. The US was more mixed but relatively resilient: manufacturing jumped to 55.3 vs 53.8 expected while services eased to 50.9 vs 51.1 expected, leaving the US picture as still expanding, but uneven.

China slumps. China delivered a clean growth downside miss this week. Retail sales (Apr) essentially stalled at +0.2% y/y vs +1.9% expected, a sharp downside surprise that confirms consumption is still the weak link. Industrial production (Apr) also cooled to +4.1% y/y vs +6.0% expected, reinforcing that the slowdown is not confined to household demand.

Japan beats. Japan’s Q1 GDP (prelim) surprised modestly to the upside at +0.5% q/q vs +0.4% expected (from +0.3% prior). Relative to weak China data and deteriorating Europe PMIs, it helped keep the Japan narrative on the “still holding up” side. The key caveat is timing: markets treated it as supportive but not definitive because it likely doesn’t fully capture the more recent energy/supply-chain drag.

Europe mixed. The UK delivered a clean downside inflation surprise: CPI (Apr) slowed to +2.8% y/y vs +3.0% expected (from +3.3% prior), with ONS noting disinflation driven heavily by housing/household services dynamics. The euro area, by contrast, did not offer the same relief: HICP (Apr final) held at +3.0% y/y, which was above the +2.8% expectation, which underscores that the euro area remains energy-sensitive in this shock.

Week ahead

Last evidence before policy calls

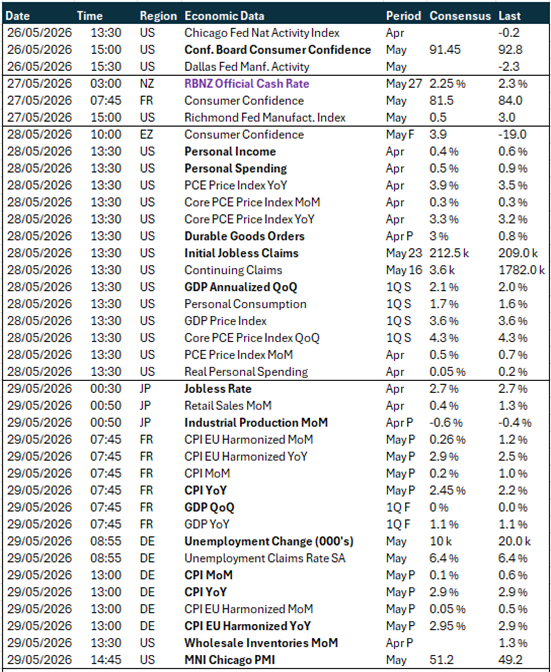

- Growth test ahead of FOMC. Next week brings the second estimate of US Q1 annualised QoQ GDP growth, with the initial release showing a 2% expansion. Any upside surprise would reinforce the narrative of a strong start to the US macro outlook this year. With the June Fed meeting approaching, the release, despite its backward-looking nature, would likely strengthen the case among FOMC members for maintaining a wait-and-see approach on rates.

- PCE to reinforce Fed patience. Attention will also turn to the Personal Consumption Expenditures price deflator. This is the Fed’s preferred inflation gauge, as it feeds directly into GDP calculations, acting as the deflator for personal consumption, which will also be released next week. The measure is expected to rise on a year-on-year basis, from 3.5% to 3.9%.

- ECB caught between growth and inflation. Next week features Germany’s labour market report, alongside May’s preliminary inflation release – both key inputs in shaping expectations for the ECB. The central bank remains at a crossroads over how far it can tighten policy amid persistent inflation. At the same time, the broader eurozone backdrop remains underwhelming, with downside risks intensifying due to the ongoing conflict, still-fragile trade relations with the US, and competitive pressure from Chinese exports.

FX views

Stalemate holds, dollar bias up

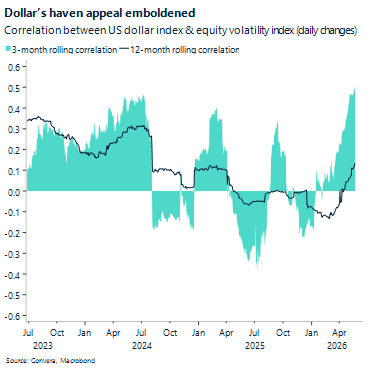

USD Dollar bid endures amid fragile diplomacy Cautious optimism over a more durable peace deal between the US and Iran has contained the dollar’s safe-haven bid this week. Investors, however, have learned to look through de-escalation noise that fails to translate into more concrete progress. The steady ~1% rise in the DXY so far this month illustrates this skepticism, as the two sides remain apart on a deal despite continued attempts to resolve the conflict. In April, by contrast, the dollar’s price action was more volatile, as markets were more responsive to signals of conflict resolution. Meanwhile, recent hawkish Fed repricing – with an 80% probability of a rate hike by year-end – a solid macro backdrop, and the global bond sell-off amid fears of accelerating conflict-driven inflation have all contributed to strengthening the dollar’s safe-haven appeal, beyond a mechanical lift from higher oil prices alone. The bullish case for the USD therefore remains intact in the absence of meaningful geopolitical developments. A test of 99.50 remains our base case over the next few days.

EUR EUR/USD pressured into 1.16 test EUR/USD has moved away from the 1.18 resistance it attempted to breach during peak de-escalation momentum in April and early May. A more cautious market response to conflict headlines justifies a lower trading range, with the pair now below all key moving averages and hovering near the 1.16 lows. Tighter global financial conditions and the recent bond sell-off have reinforced the bearish profile. Against a softer macro backdrop, investors are increasingly reluctant to hold European debt relative to the US. In the US, upward pressure on yields has been driven more by stronger growth expectations and a hawkish Fed outlook (real yields) than by rising uncertainty (term premia). At the same time, with close to three ECB hikes already priced in, there is more room for expectations to be unwound than extended, further reducing the appeal of European fixed income. Overall, EUR/USD looks poised to break below 1.16 in the coming days, barring significant developments in the Middle East.

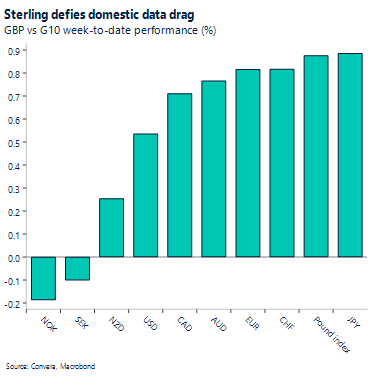

GBP Rebound without revival. Sterling has outperformed most G10 peers this week, suggesting a more GBP‑centric driver is at play. It climbed close to 1% against the EUR, JPY and AUD, while holding above 1.34 versus the USD after trading nearer 1.33 last week. However, the move is better characterised as a retracement from last week’s politically driven sell-off rather than the start of a fresh bullish impulse. Recent support appears to stem from a partial easing in domestic political risk. Signals such as Andy Burnham’s emphasis on fiscal discipline and Wes Streeting’s pledge to deepen UK–EU ties have helped stabilise sentiment. In parallel, bond market volatility has moderated through the week, aided in part by tentative optimism around US–Iran developments. That said, the UK macro backdrop appears to be softening. A cooling labour market, softer inflation, weaker retail sales and declining contracting PMIs all reinforce the case for the BoE to remain on hold next month. Sterling’s muted reaction to this data suggests that the partial trimming of UK political risk premia is offsetting macro headwinds for now. However, this repricing appears incomplete. Political uncertainty has diminished but not disappeared, and with the UK data pulse weakening, these residual risks remain lingering in the background. As such, sterling’s resilience may prove fragile as underlying macro and political headwinds begin to reassert themselves.

CHF Hawkish shift. The franc remains underpinned by domestic fundamentals but continues to trade within a regime shaped by valuation and policy asymmetry. Stronger‑than‑expected Q1 growth and a recent uptick in inflation have shifted the policy debate, with markets now pricing a full SNB rate hike by year‑end – a sharp reversal from pre‑conflict expectations of easing. Despite this hawkish repricing, CHF gains have been modest, underscoring persistent market caution around SNB intervention risk at elevated levels. With the real effective exchange rate near multi‑year highs, policymakers remain sensitive to further appreciation, even as no clear evidence of active FX intervention has emerged in sight deposits or reserves data. This leaves the franc supported but not unconstrained: domestic strength and policy repricing provide a floor, while intervention risk caps upside, keeping EUR/CHF broadly anchored near the 0.91 range.

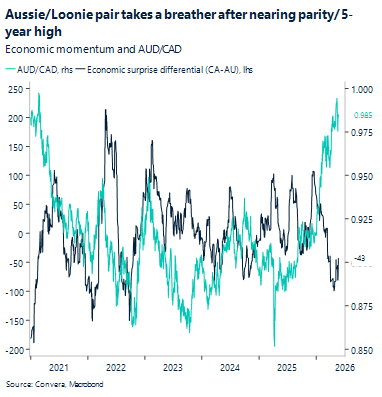

CAD Weak momentum. Throughout this week, the USD/CAD has maintained an upward bias, breaking firmly above its recent trading range to trade around 1.3775 despite a bout of mid-week volatility and a brief dip to a low of 1.373 where buyers aggressively stepped in. While the trading range has since narrowed and overall volatility has cooled, the pair’s path of least resistance remains heavily skewed to the upside due to a widening macroeconomic gap between the two nations. A major catalyst for this price action was the latest Canadian inflation print; although headline CPI ticked up, it missed expectations, and critically, underlying core inflation measures cooled. This softer core reading undercuts the Canadian Dollar by reinforcing a more dovish policy outlook for the Bank of Canada, even as markets stubbornly price in more than one quarter-point rate hike by year-end. At the same time, Canadian bond yields are now trading at their most negative spread versus the United States in six months, dragging down forward points and leaving the Loonie highly vulnerable against a greenback buoyed by higher yields, resilient US economic data, and higher oil prices. Next week, markets will be focused on Q1 GDP on Friday, expected to print at an annualized 1..5% rate.

AUD Jobs miss doesn’t tell the full Aussie story. Australian employment fell 19k in April, well short of the 15k gain the market had pencilled in, while annual jobs growth of 0.9% was the weakest since 2021. Even so, we think the labour market remains relatively firm. Hours worked surged 0.8% for the month and 3.5% year-on-year — a much stronger signal than the headline number alone. The jobless rate climbed to 4.5%, topping the 4.3% expected, but it still sits below the estimated full-employment level of around 4.75%. We continue to expect the RBA to raise rates by 0.25% in August. AUD/USD has pulled back from its highest level in more than four years and now trades around 1.9% below its 6 May peak of 0.7278. Near-term support sits around the 50-day EMA at 0.7116, with the 100-day EMA near 0.7015 the next level to watch if selling gathers pace. On the upside, 0.7200 is the key resistance to clear. We will be watching upcoming inflation data and private capital spending figures.

CNH China’s April numbers disappoint. China’s retail sales barely moved in April, rising just 0.2% year-on-year against expectations for 2% growth and a prior reading of 1.7% — the worst outcome since December 2022. Industrial output grew 4.1% year-on-year, falling well short of the 6% forecast and slowing from 5.7% previously, the weakest pace in almost three years. Fixed asset investment contracted 1.6% year-on-year in the January-to-April period, a sharp miss against expectations for steady growth of 1.7%. The data paints a clear picture: domestic demand remains soft, and while exports are holding up, geopolitical pressures continue to weigh. Noted that CNH is Asia FX’s top YTD performer, up 2.6% in spot terms. USD/CNH sits just 0.3% above its recent low of 6.7816, reached on 14 May. For the USD/CNH to build upward momentum, it needs to break above the 50-day EMA at 6.8392 before testing the 100-day EMA at 6.8879. We will be watching upcoming Chinese industrial profit data.

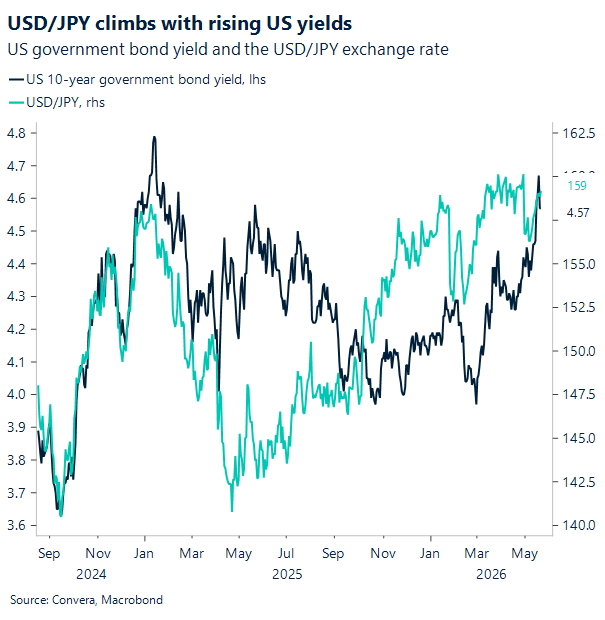

JPY Rate hike timing in doubt. Japan’s core inflation slowed to 1.4% in April from 1.8% the prior month, coming in below the 1.7% forecast and hitting its lowest level since March 2022. Headline inflation also eased, dipping to 1.4% from 1.5%, while the narrower measure stripping out both food and energy dropped to 1.9% from 2.4%. All three gauges now sit below the Bank of Japan’s 2% target. Energy prices fell 3.9% year-on-year — a smaller drop than the 5.7% decline in March — keeping the focus on subsidy dynamics against the backdrop of the Iran conflict. The softer numbers weaken the case for an early rate rise, though solid growth and a weak yen keep the prospect of further tightening on the table. In FX, USD/JPY is holding above 159.00 at the time of writing, around 1% below its 30 April high of 160.72. Support is seen at the 21-day EMA near 158.44, followed by the 50-day EMA at 158.26. The key resistance level to watch is 160.00, with potential intervention again. Elsewhere, SGD/JPY has climbed to a three-week high. The chart shows how closely USD/JPY has tracked US 10-year yields over the past two years — a reminder that as long as the yield gap between the US and Japan stays wide, yen weakness is hard to reverse. We will be watching upcoming Tokyo core inflation and industrial production data.

MXN Resilient Peso. Moody’s downgrade of Mexico to Baa3 landed with a muted market reaction, underscoring how much of the bad news was already priced into USD/MXN. The peso softened briefly on the headlines but quickly retraced, supported by broader EM FX tailwinds as a softer US dollar and improving global risk sentiment continue to drive demand for high-yielding currencies. The USD/MXN, is showing signs of consolidation within a broader downtrend. Spot near 17.3 is hovering around the 20-day moving average (~17.34), while the 50-day and 100-day (~17.50–17.52) cap the topside and define a clear resistance zone. The 200-day (~17.94) continues to trend lower, reinforcing the medium-term bias toward peso strength. Price action since the start of the year suggests a range between roughly 17.10 support and 17.50 resistance, with neither side yet delivering a decisive breakout. A sustained move above that 50/100-day cluster would shift momentum toward 17.90, while a break below the 17.10–17.20 floor would reassert the downtrend and reopen a move toward 17.00, keeping the peso’s relative resilience intact despite deteriorating credit fundamentals.

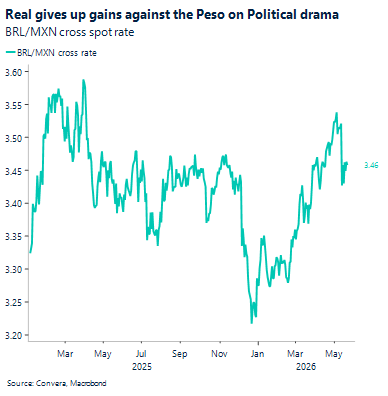

BRL Political arena. The uncertainty surrounding Flávio Bolsonaro’s candidacy, where public support masks growing private doubts, injects a fresh layer of risk premium into the Real. With political insiders explicitly noting a critical 10 to 15-day window to reassess his viability, we are looking at a clear near-term catalyst, even as his camp attempts to project stability by previewing future government appointments. This impending political volatility could very well be the fundamental spark that dictates the USD/BRL’s next technical leg. The pair is currently consolidating near 5.0, trapped between near-term support at the 20-day SMA (4.969) and immediate resistance at the 50-day SMA (5.075). While the broader structural downtrend remains intact beneath the 100-day and 200-day moving averages, this tight short-term range reflects a market waiting for a catalyst, now likely to come from the political arena.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.