The share of central banks cutting interest rates is rising by the week and communication from the big three is becoming more dovish by the meeting.

Investors have welcomed the lack of pushback against easing financial conditions and feel reassured in their hopes that the peak of the tightening cycle is behind us.

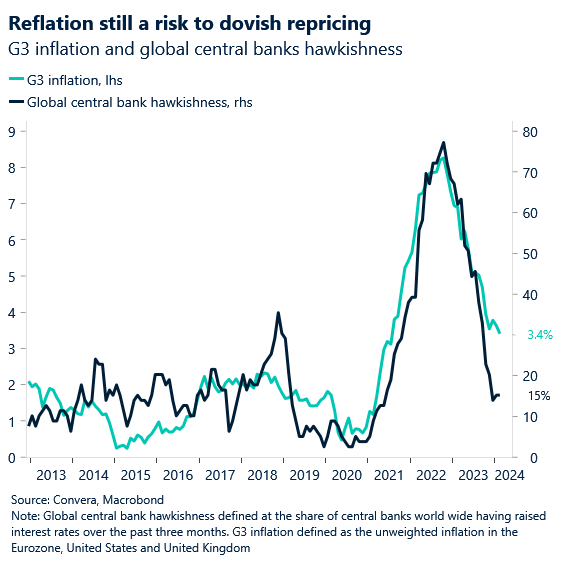

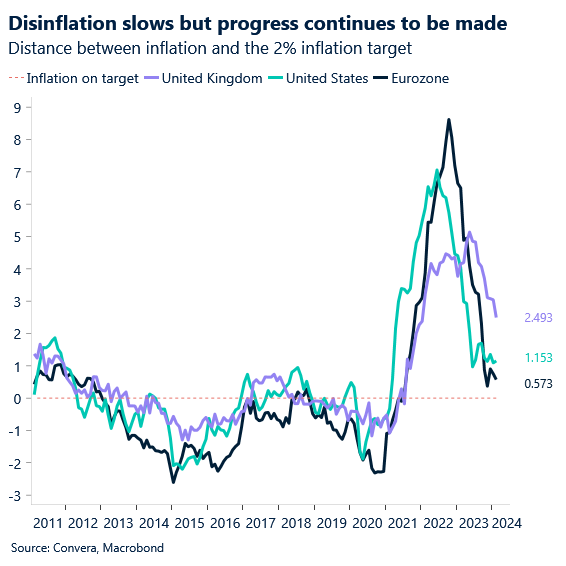

The US is the most at risk of inflation settling above 2% as the incoming macro data continues to remain robust. All macro data surprised to the upside last week.

As widely expected, the Federal Reserve (Fed) left its main policy rate target unchanged at a 23-year high between 5.25% and 5.5%.

The Bank of England (BoE) left its Bank Rate at 5.25% yesterday, but it was a dovish hold given the Monetary Policy Committee’s 8-1 vote split.

Most leading indicators continue to signal a bottoming of the European economy as inflation rates fall. This puts the June meeting in sight for a first ECB rate cut.

While a lot of economic data is scheduled to be releases next week, most of the prints lack the ability to move markets. The only potential catalyst will be the PCE report on Friday.

Global Macro

Dovishness overflow despite macro uptick

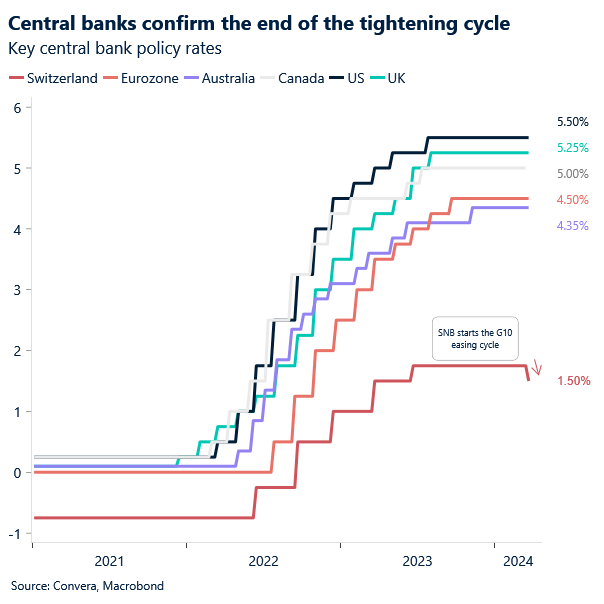

Turning dovish. G10 Central banks have come a large step closer to joining the monetary policy easing cycle that their peers in emerging markets have kickstarted this year. The share of central banks cutting interest rates is rising by the week and communication from the big three is becoming more dovish by the meeting. The Swiss National Bank has made the beginning as the first G10 institution to cut interest rates, while the Federal Reserve and Bank of England failed to deliver hawkish messages this week.

Goldilocks. Investors have welcomed the lack of pushback with open arms and feel reassured in their hopes that the peak of the global tightening cycle is behind us. The European equity benchmark rose for a seventh consecutive week and has extended its gain since November to 18%. The S&P 500 pushed higher as well and has now risen in 18 out of the last 21 weeks with a 10% year-to-date gain under its belt. Bond yields across countries and the curve fell against the backdrop of this week’s dovish central banks deliveries. The US dollar did manage to rise despite its Fed-induced fall on Wednesday, mostly due to idiosyncratic weakness from the pound, yen and euro.

Hawkish macro data. While this development does play into our global macro thesis of monetary policy having to turn more accommodative, it is important to not lose sight of the currently discounted macro and inflation risks. The US is the most at risk of inflation settling above 2% as the incoming macro data continues to remain robust. Last week saw five economic data releases in the US surprise to the upside. Inflation expectations are on the rise as well, showing how narrow the Fed’s path seems to be. Hard- and soft-landing, while on opposite ends of the forecasting spectrum, do seem to be separated by just one or two miscalculations by the Federal Reserve.

Regional outlook: US

Dovish Fed perception despite strong data

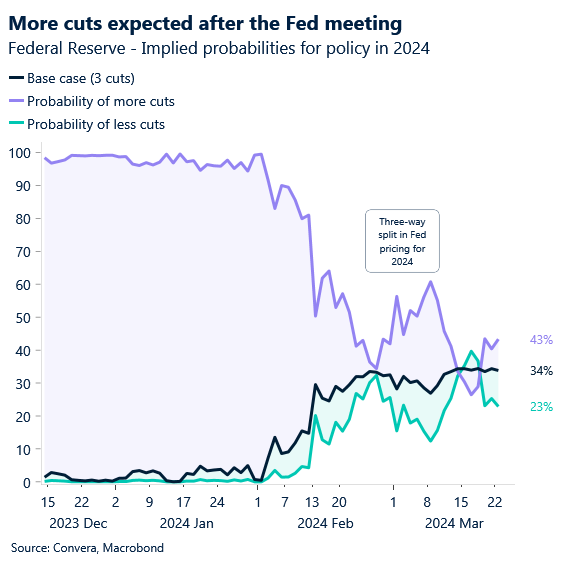

Unchanged policy. As widely expected, the Federal Reserve (Fed) left its main policy rate target unchanged at a 23-year high between 5.25% and 5.5%. The Fed’s updated economic projections were the main focus though, and the Dot Plot revealed officials still expect to make three lots of 0.25 percentage point rate cuts this year, signalling confidence that inflation is cooling sufficiently to reduce borrowing costs.

Higher long-term dot-plot. Policymakers’ revised rate forecasts showed a median interest rate of 4.625% for the end of this year, unchanged from December, while forecasts for the next two years and the long-run were higher than last quarter with just three reductions in 2025, down from four forecast in December. The dispersion of the Dot Plot is overall more hawkish despite the median sticking with three cuts for this year, but officials said that any future adjustment in rates will depend on the data, the outlook, and the balance of risks.

Hawkish macro data. This week featured some second-tier economic data from the United States that painted a slightly better picture of the world’s largest economy than the recent news flow would have suggested. All five economic releases surprised the consensus to the upside with housing and manufacturing data continuing to distance itself from the recent bottom as labor market data remains robust. The NAHB Housing Sentiment Index improved across the board, something that was echoed by both housing starts and existing home sales being up 10.7% and 9.5% last month. Initial jobless claims remained low at 210 thousand, while the forward-looking components of the Philadelphia Fed Manufacturing PMI surged.

Markets continue to perceive the Fed as dovish as Jerome Powell did not push back against the easing of financial conditions. The macro data has been mixed recently and offers something for both the doves and hawks. Incoming data will be crucial to watch.

Regional outlook: UK

Bank of England now likely to join Fed, ECB in cuts

Downside inflation surprise. The latest inflation report confirmed an expected slowdown in the British inflation rate. Headline inflation eased to 3.4% y/y in February, a low not seen since September 2021, while the core rate fell to a two-year low of 4.5% y/y. Both prints came in lower than expected with the slowdown in the headline rate predominantly driven by a slowdown in price increases for food and several service sector components.

Dovish rate decision. As expected, the Bank of England (BoE) left its Bank Rate at 5.25% yesterday, but it was a dovish hold given the Monetary Policy Committee’s 8-1 vote split. The two previously hawkish dissenters voted with the majority to keep rates unchanged this time, while Swati Dhingra once again voted for a cut. GBP/USD suffered its worst day in over a month, while GBP/EUR slipped to its lowest level in nine weeks. The forward guidance from the BoE remained unchanged, stating that rates need to stay sufficiently restrictive for an extended period of time, but BoE Governor Andrew Bailey said things are moving in the right direction.

Still in expansion. The flash PMI figures released before the meeting also pointed to slowing momentum in the UK’s dominant services sector, although it was the fifth month of expansion in the country’s private sector overall. Friday’s UK retail sales data came in slightly stronger than expected, but stagnated in February, offering the pound little support.

The hawks within the Bank of England have dispersed and the probability of a June cut have risen to 75%. This has put pressure on GILTS and the pound as British policy makers are now seen as less likely to divergence from the dovish Fed and ECB.

Regional outlook: Eurozone

Still on track for a June cut

Three conditions to cut. Speaking at a conference in Frankfurt, ECB’s President Lagarde laid out three tests that the central bank will apply to judge the optimal time to cut interest rates, cautioning, however, that the ECB would not commit to a predetermined rate cut path and will continue to depend on incoming data: (1) – Wage growth. (2) – Corporate profit margins. (3) + Productivity growth. These factor would allow the bloc to recover more rapidly even as inflation dissipates.

Slower wage growth. The latest data from Eurozone revealed that bloc’s labour costs rose by 3.4% y/y in Q4 2023, the slowest pace since Q3 2022, and below market expectations of 4.6%. Although the moderation in pay growth strengthens the case for a June rate cut, interest rate traders are hesitant to reprice ECB rate cut expectations ahead of the FOMC decision.

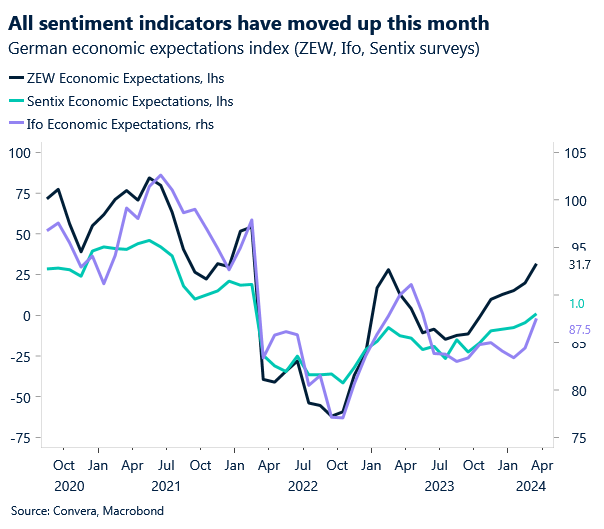

Rebounding data. The preliminary composite PMI reading for the bloc rose to 49.9, up from 49.2 in the previous month and slightly surpassing the market expectations. Although the latest reading was the highest for nine months, manufacturing output continued to decline for the twelfth consecutive month, albeit at a slightly slower pace. Elsewhere, the ZEW Indicator of Economic Sentiment for Germany reached its highest level since February 2022, but was shrugged off by FX markets as investors are now looking for a larger bone to chew on. The German business climate also jumped to the highest level since June, according to the Ifo institute.

Wage growth is cooling, and inflation is expected to fall below 2% this year. The economic data is rebounding from historically low levels. This will allow the ECB to cut interest rates in June, without having to worry about financial risks.

Week ahead

Looking for a signal with a lot of noise

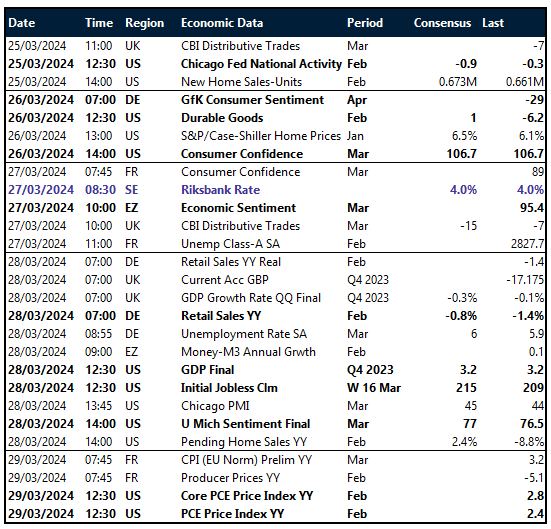

Tier two data. The upcoming week is filled with various secondary economic data points. While not displaying market moving potential on their own, such data acts as a testing ground for existing narratives. Last week was about US macro data surprising to the upside. It will be interesting to confirm the uptick in momentum with data points such as the Chicago Fed Index, consumer confidence and Michigan consumer sentiment.

PCE inflation report. The main event and only tier one release will come in the form of the US PCE report. The last five inflation releases have surprised the consensus to the upside, which puts the focus on Friday’s PCE inflation print. While the core reading should slow to down to a monthly growth rate of 0.3%, the headline rate is expected to accelerate from 0.3% to 0.4%. This should keep the Fed on their toes and limit dovish repricing.

Low-level macro flow. The European macro flow will be watched as well. A mixture of soft- and hard data points are scheduled to be released. Consumer confidence on Tuesday and retail sales and unemployment on Thursday are up in Germany.

The data dependent of central banks and the ambiguity of the future policy easing path are making the macro data invaluable in gauging where markets are headed. However, while a lot of economic data is scheduled to be releases next week, most of the prints lack the ability to move markets. The only potential catalyst will be the PCE report on Friday.

FX Views

Dollar gains on dovishness from outside

USD Asymmetric reaction function. The US dollar index (DXY) has rebounded almost 2% since hitting a 2-month low two weeks ago. The DXY recorded its biggest daily rise since early February this Thursday on weak data from Europe and a dovish delivery from the BoE. Even as global central banks set out a synchronized easing trajectory, the Fed is moving in a marginally more hawkish direction, meaning rate differentials are playing a supportive role for the buck. However, the Greenback’s sensitivity to strong macro data has been underwhelming, showing the clear bias of investors against the US dollar. The reaction function of the dollar to incoming data is asymmetric in the sense that weaker data seems to be moving the currency more than upside surprises. This does not mean that the dollar cannot rise from current levels, especially as US inflation is expected to remain higher than in the Eurozone and UK. However, the extent of positive data surprises needed for a substantially higher dollar has risen in recent weeks.

EUR Risks tilted to downside. The euro slumped to its lowest level since the start of the month following a week of central bank decisions and key data releases. EUR/USD has fallen about 1.4% over the past two weeks and short-term risks appear to be tilted to the downside. Reasons for higher ECB policy rates beyond June are depleting with the latest CPI and wage growth reports surprising to the downside. As the Governing Council continues to turn more dovish, money markets are now pricing in 87 basis points of ECB cuts this year, with the probability of a June rate cut at 68%. In the near-term, EUR/USD faces a strong resistance barrier at the $1.09500 – a level above which it has only been able to sustain for 8.2% of the time during 2024. In fact, the interquartile trading range throughout Q1 has remained remarkably tight, with the pair spending 50% of its time oscillating in the $1.08165 – $1.09225 range. Without a meaningfully large shift in monetary policy expectations for either the Fed or the ECB, volatility in EUR/USD is likely to remain depressed. We do, however, expect EUR/USD volatility to pick up around corporate margin, wage growth and labour productivity data events as the ECB’s President Lagarde highlighted those as the three key criteria going forward for ECB rate cuts.

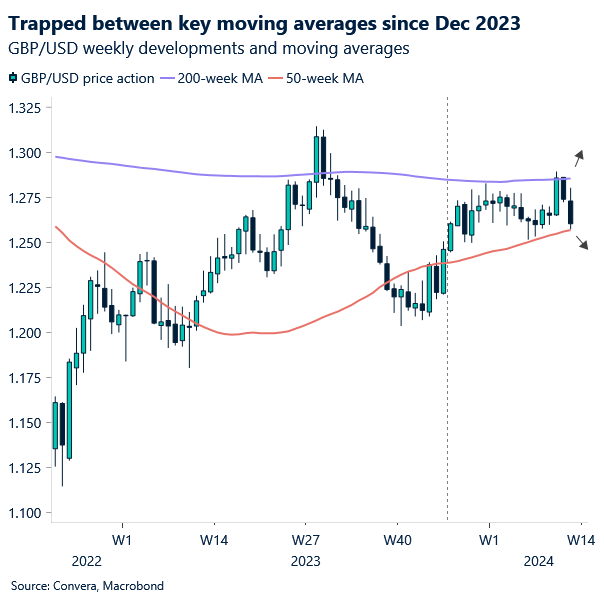

GBP Dovish shift by BoE rocks sterling. We highlighted recently that risks to the pound lean asymmetrically to the downside in the short term given policy pricing and stretched positioning. Indeed, sterling has appreciated against less than half of its global peers so far this month and the past week has seen it appreciate against just 14%. The pound’s weakness gained momentum after two BoE policymakers switched from hawkish to neutral this week, which led to the probability of a rate cut as soon as May being priced in by markets. GBP/USD suffered its worst day since October and GBP/EUR slipped to a 9-week low. On the data front, a bigger-than-expected drop in UK inflation last month, coupled with stagnant consumer spending and an overall easing in economic activity also supported the BoE’s dovish guidance that rate cuts are in play this year. Consequently, the UK-US 2-year yield spread dropped to its lowest level in a year, accelerating the decline in GBP/USD to over 2% from 7-month highs just shy of $1.29 two weeks ago. The currency pair continues to float in a circa 3-cent range between key moving averages. In fact, the interquartile trading range throughout Q1 has remained remarkably tight, with the pair spending 50% of its time oscillating in the $1.26330 – $1.2727 range. An extended break to the downside looks plausible if the pair closes below its 50-week moving average currently located at $1.2575.

CHF SNB commences G10 easing cycle. The Swiss National Bank (SNB) cut interest rates by 25 basis points to 1.50% making it the first G10 central bank to cut rates this cycle. The SNB stressed the impact real appreciation in the Swiss franc over the past year was having on its manufacturing sector and goods inflation to motivate its decision. Markets were pricing just a 30% probability of a cut, hence the aggressive sell off in the Swiss franc. USD/CHF jumped to a 4-month high (0.8984), rising over 1.3% on the day, its biggest daily advance in a year. EUR/CHF notched its highest level (0.9787) since July last year and has now risen for 7 weeks on the trot – its longest weekly winning streak since 2008. The currency pair has risen over 5% since the start of the year and is testing its 100-week moving average for the first time since 2021. The SNB’s decision confirms the franc’s status as the most viable G10 funding currency, both due to its lower rates and the SNB’s intolerance towards further CHF appreciation.

CNY China’s industrial output surpasses expectations despite property market challenges. China’s economic data for January-February exceeded expectations, with industrial production growing at its fastest pace in nearly two years and fixed asset investment outperforming forecasts. However, retail sales growth slightly disappoints, signaling some moderation in consumer spending. Despite government stimulus efforts, property investment continues to decline, posing a significant drag on the economy. USD/CNH is nearing initial upside targets (re Weekly Jan 19th publication: targeting 7.239-7.2665 resistance) after consolidating between November-January. Attention now turns to Chinese industrial profit data for further insights into the country’s economic health.

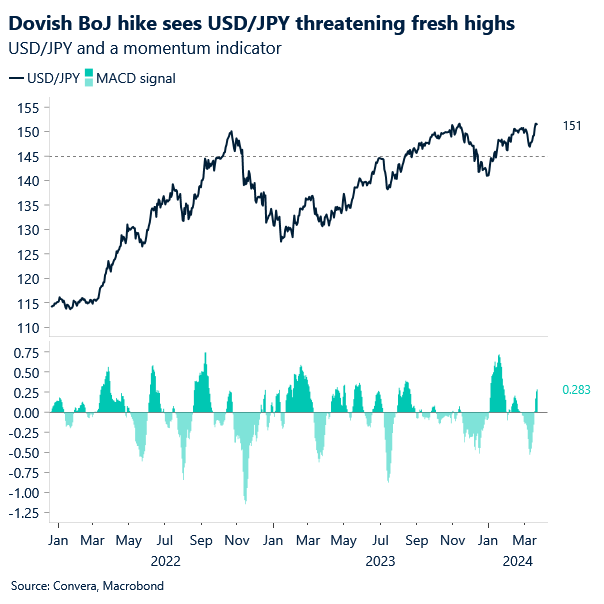

JPY BOJ Governor reaffirms accommodative stance amid uncertain inflation outlook. BoJ Governor Kazuo Ueda reaffirms the central bank’s dovish stance on rate hikes, emphasizing the ongoing need for accommodative measures until inflation reaches the 2% target. Ueda assures markets of the bank’s cautious approach, indicating a willingness to maintain accommodative policies as needed. While considering various tools for easing, the BoJ remains vigilant about economic conditions and the inflation trajectory. Additionally, Japan’s Finance Minister Shunichi said officials are keeping a close eye on economic and FX market developments following recent BoJ policy changes. As for USD/JPY technical levels, key resistance remains at 151.188-151.945 until the pair sees a sustained break below 145 (see RHS chart). Key economic indicators to monitor include the unemployment rate, industrial production, retail sales, and CPIs this coming week.

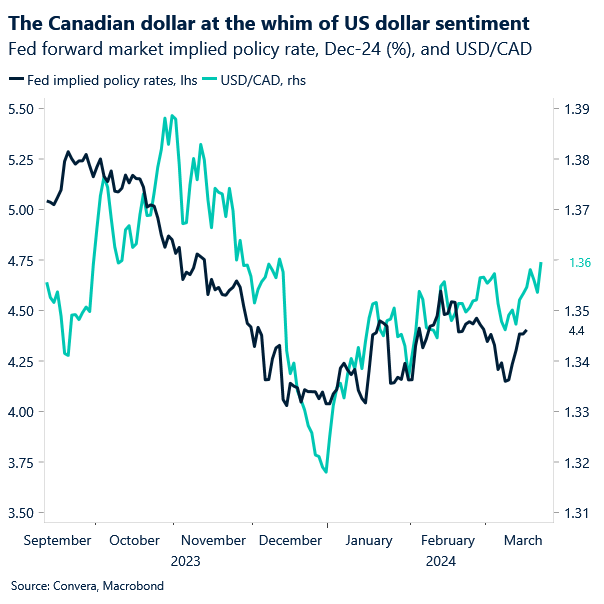

CAD Rescued by dovish FOMC. Earlier in the week, the Canadian dollar weakened to a near-four month low, touching $1.3613 per US dollar, as the latest domestic CPI print surprised to the downside, bringing forward the BoC rate cut expectations. The underwhelming mid-week performance was salvaged by a US dollar sell off typically observed post-FOMC meeting, but the pair already appears to be stabilising around $1.3550 level. USD/CAD remains in a bullish trend channel in place since Dec 27, and for now there are few reasons to challenge that. With the Canadian economy weakening, a delay in the BoC rate easing cycle could further hurt the economy. On the flip side, if the central bank cuts before the Fed, it could significantly weaken the Canadian dollar. The only saving grace is the BoC remains reluctant to unveil the timing or the magnitude of interest rate cuts, while the Fed’s dot plot signals 75bps easing is to come by year-end. In the short term, $1.3600/$1.3610 looks to be a very firm resistance level, with the pair managing to close above this threshold only 5 out of the past 60 trading days. As the USD/CAD gain in Q1 of +1.85% exceeds the interquartile range for YTD performances over the past 70 years, we should expect to see a slowdown in the velocity of USD/CAD appreciation as it edges towards the elusive $1.3600 barrier.

AUD RBA adopts a gradually dovish tone. The RBA’s recent statement subtly shifts its tone, moving from a more definitive stance on interest rate increases to a more ambiguous position, indicating a gradual dovish shift. The language adjustment suggests a cautious approach, especially considering the fluctuating monthly CPI data. While noting some positive signs, such as moderating inflation, the focus remains on potential weaknesses, particularly in household consumption growth. This shift confirms recent market expectations and supports the recent rally in AUD rates. The AUD/USD trading patter reflects this uncertainty, with the pair caught within a broader trading range amid mixed market sentiment. Looking ahead, upcoming indicators like Westpac consumer sentiment and CPI data will be closely watched for further insights.