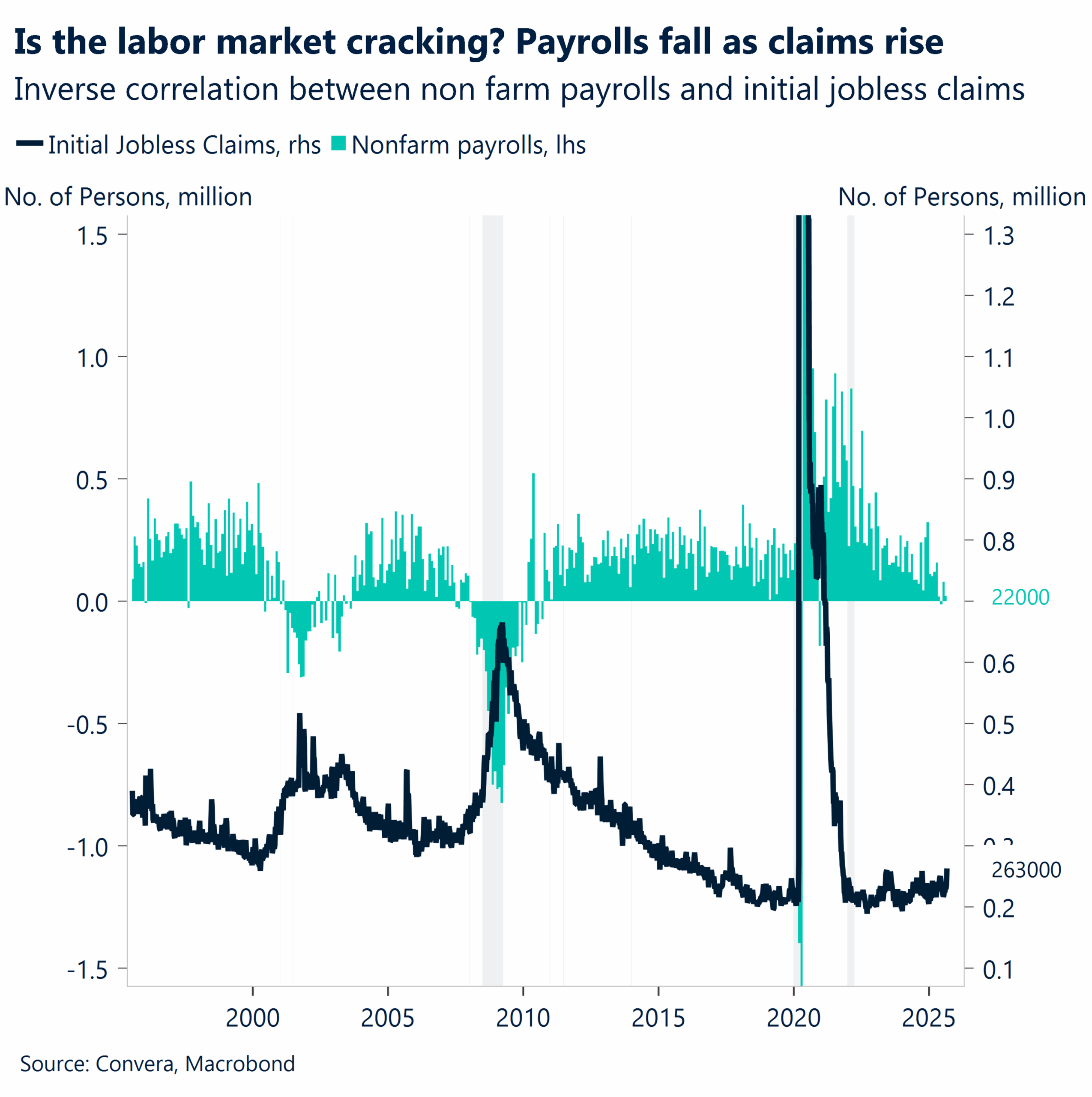

- Inflation overshadowed. The latest US CPI data confirmed inflation remains above the Fed’s 2% target, but not alarmingly so. Meanwhile, jobless claims surged to a near 4-year high, which gained more market attention.

- Soft jobs, soft path. It’s a delicate balancing act, but momentum is shifting toward prioritizing full employment over price stability – especially after this week’s steep downward jobs revision and last week’s weak payrolls print.

- Three cuts validated. As a result of recent data, a dovish repricing in Fed easing bets has increased, making three cuts the clear base case. A 25bp cut next week is expected, followed by similar moves in October and December.

- Risk still rules. That was enough to boost Treasuries and drag the USD lower. With risk appetite still firm, all major US equity benchmarks hit record highs as the liquidity-fuelled rally trumped resurfacing geopolitical risks.

- Geopolitics sidelined. Israel’s strike on Hamas leaders in Doha triggered a brief spike in energy prices, nudging energy-dependent currencies lower, but without Gulf retaliation, seen as unlikely, it’s doubtful to have lasting impact on the market.

- ECB holds fire. The ECB left the deposit rate unchanged at 2%, as widely expected. All in all, the implicit message to markets was that there are no reasons to keep pricing in additional rate cuts as things stand.

Global Macro

Jobs data trumps inflation

U.S. inflation mixed signals. The CPI report showed consumer inflation remains a concern, with headline CPI rising to 2.9% and core CPI holding at 3.1%, underscoring persistent price pressures. In contrast, August’s Producer Price Index (PPI) fell 0.1% m-o-m—its first decline in four months—driven by lower services prices. While PPI can be a leading indicator, markets are left reconciling sticky consumer prices with cooling producer-level inflation.

U.S. job market softens. U.S. jobless claims rose by 27,000 to a four-year high of 263,000 for the week ending September 6, signaling a clear softening in the labor market. This aligned with this week’s release of the staggering downward adjustment made by the BLS of 911,000 jobs between April 2024 and March 2025. Given that the US CPI came in mostly in line with expectations, the job reports became the far more influential market drivers. The claims unexpected weakness was the key piece of information that solidified bets on an impending Fed rate cut.

ECB hits pause. On September 11, the ECB kept its key interest rates unchanged at 2.00%. This was driven by its assessment that inflation is on track to its 2% target and its upgraded growth forecast for the eurozone, which is now projected to expand by 1.2% in 2025. The bank stressed that it would remain “data-dependent” and not pre-commit to any future rate path, noting that economic risks have become more “balanced.”

Japan’s shrinking surplus. Japan’s current account surplus for July declined by 19.1% to ¥2.68 trillion, largely due to a widening services deficit and a decline in the primary income surplus, signaling a potential shift in Japan’s economic fundamentals.

China’s trade slowdown. Despite a large trade surplus of $102.33 billion, China’s August trade data showed that export growth slowed to 4.4% and imports to a mere 1.3% from a year earlier. This indicates cooling global and domestic demand.

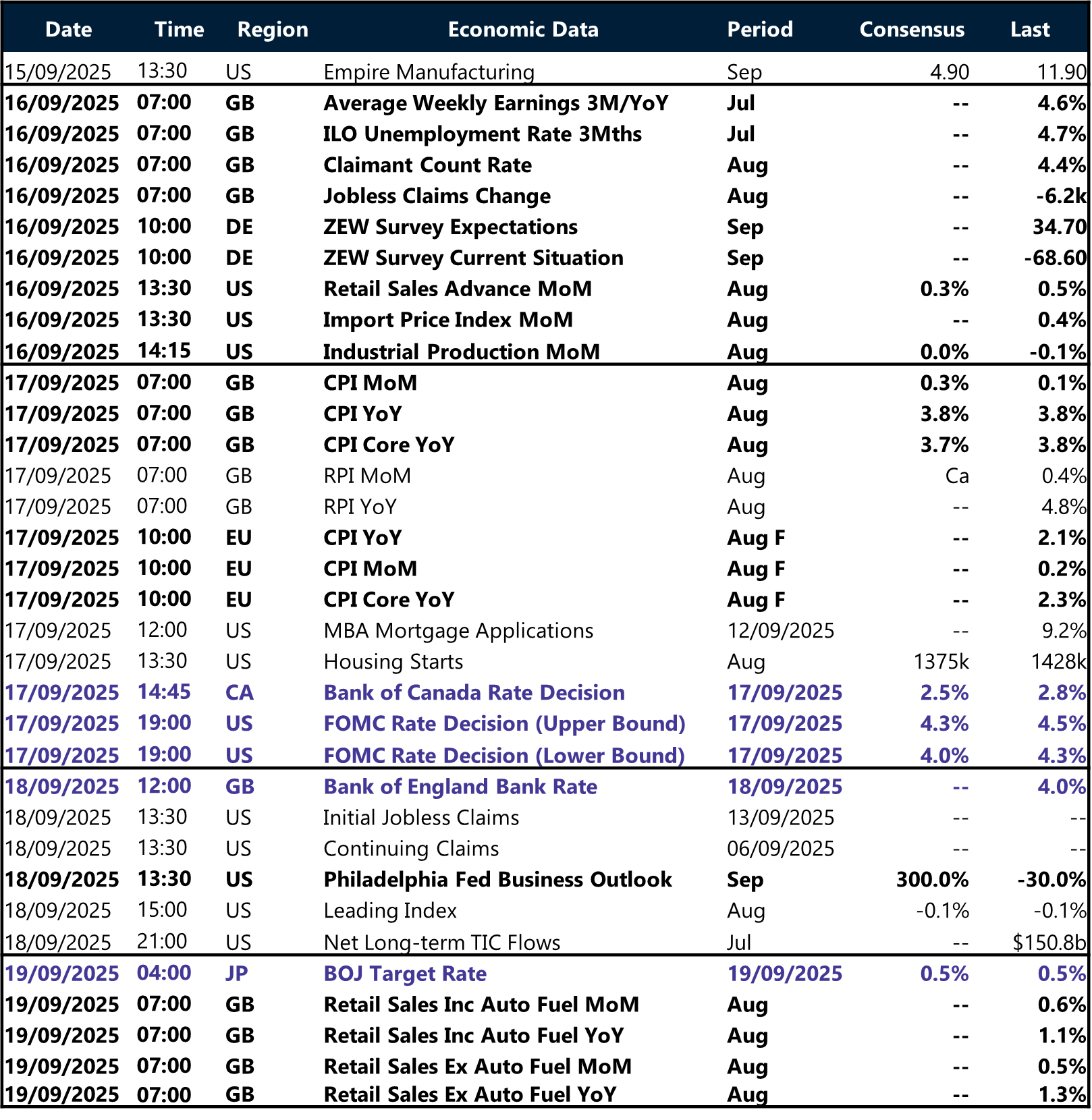

Week ahead

Global rate watch: big week ahead

Central banks in action. We expect the Fed to turn more dovish, with markets widely anticipating a rate cut, given signs of a cooling job market and moderate inflation. Meanwhile, the Bank of England is likely to hold steady, remaining cautious amid persistent price pressures. A rate cut is highly anticipated from the Bank of Canada, following weak employment and GDP data – suggesting tariffs are beginning to weigh on growth.

Japan’s rate outlook turns murky. While stronger-than-expected GDP growth and sticky inflation keep a rate hike on the radar, political instability and global trade uncertainty cloud the outlook, favouring a more cautious tone from policymakers.

Resilience under review Ahead of the BoE meeting, the UK labour market report may reinforce the narrative of a cooling jobs market – especially after Friday’s data showed the UK economy stagnated in July. While a rate cut in September remains unlikely, a soft print would dampen hopes of a sustained economic rebound, suggesting recent resilience may have been short-lived.

BoE’s biggest headache UK Inflation remains the key obstacle to easing. The upcoming MoM print is expected to rise to 0.3% from 0.1% in July and will be closely watched for signs of lingering price pressures.

FX Views

Calm before the cut

USD No waves in dollar trading. This week, the dollar index navigated relatively calm waters. This reflects a mix of sentiment-driven risk factors taking a back seat for now, a light data calendar, and a rate expectations glass already filled to the brim – making it difficult for the dollar to react meaningfully to economic releases or Fed commentary. The spotlight was on inflation data. Both the PPI and CPI reports – capturing price pressures from the perspectives of producers and consumers – came in orderly and broadly in line with expectations. The print adds weight to speculation that the impact of tariffs may be more temporary than initially feared. While this is a short-term negative for the USD (via the yield channel), in the longer run, the greenback could find support as easing stagflation concerns calm investor nerves further. The upcoming Fed policy meeting, widely expected to deliver a rate cut, could be the dollar’s next key bearish catalyst – especially if the tone turns out more dovish than anticipated.

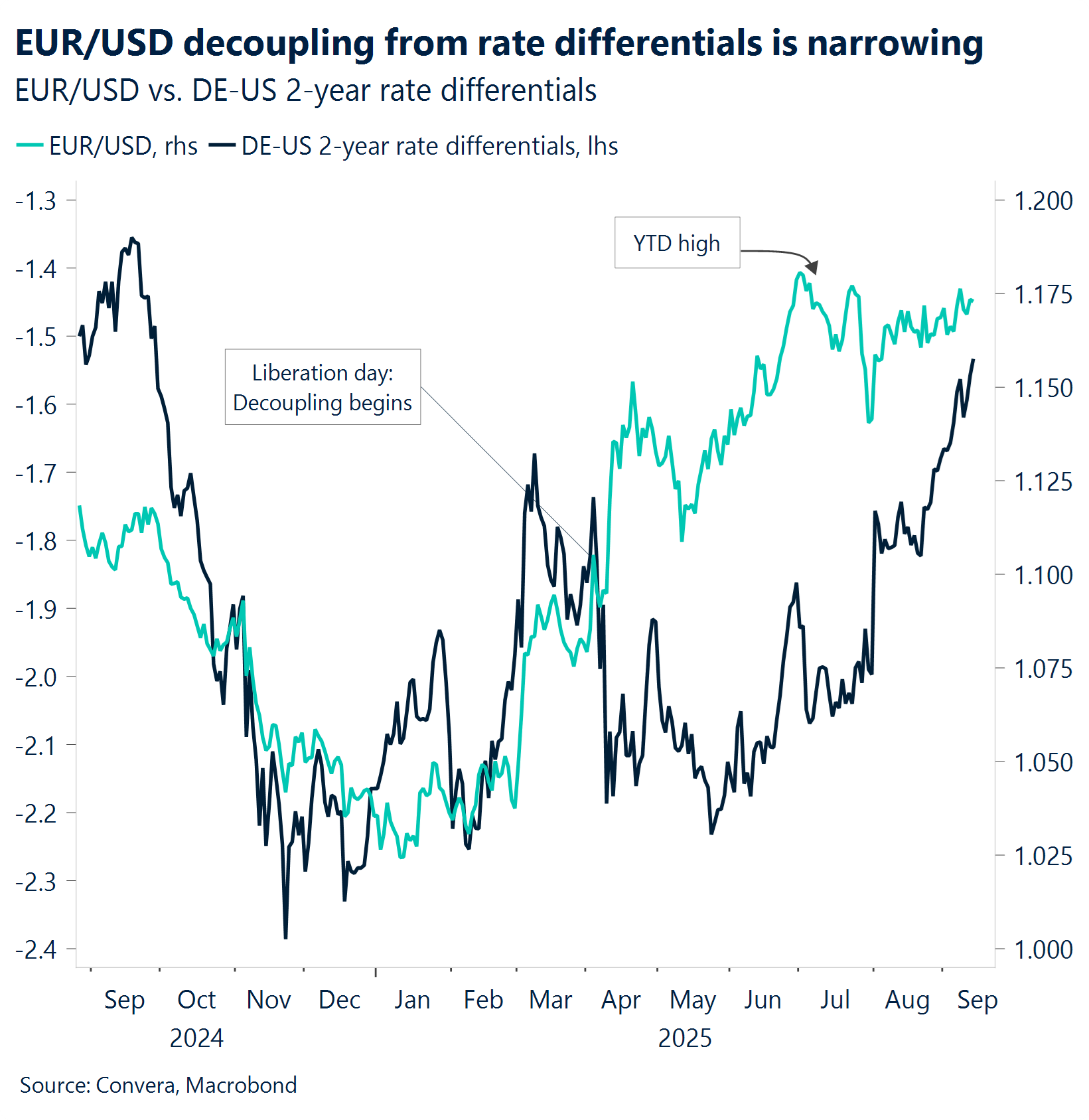

EUR Euro perked up on ECB signals. EUR/USD hovered near the 1.17 level, attempting to consolidate more firmly above it – but ultimately failing to do so. A lack of fresh data and a geopolitical flare-up – Israeli attacks on Doha and Poland’s shutdown of allegedly Russian drones – dampened any confident euro upside. We doubt these events will escalate into something larger (at least for now), keeping FX implications limited. Later in the week, the euro found fresh momentum during Lagarde’s press conference following the ECB policy meeting. Her remarks struck a more hawkish tone than expected, further supported by hints of reduced uncertainty on the trade front. The meeting effectively ruled out a rate cut this month, offering much-needed support to euro bulls.

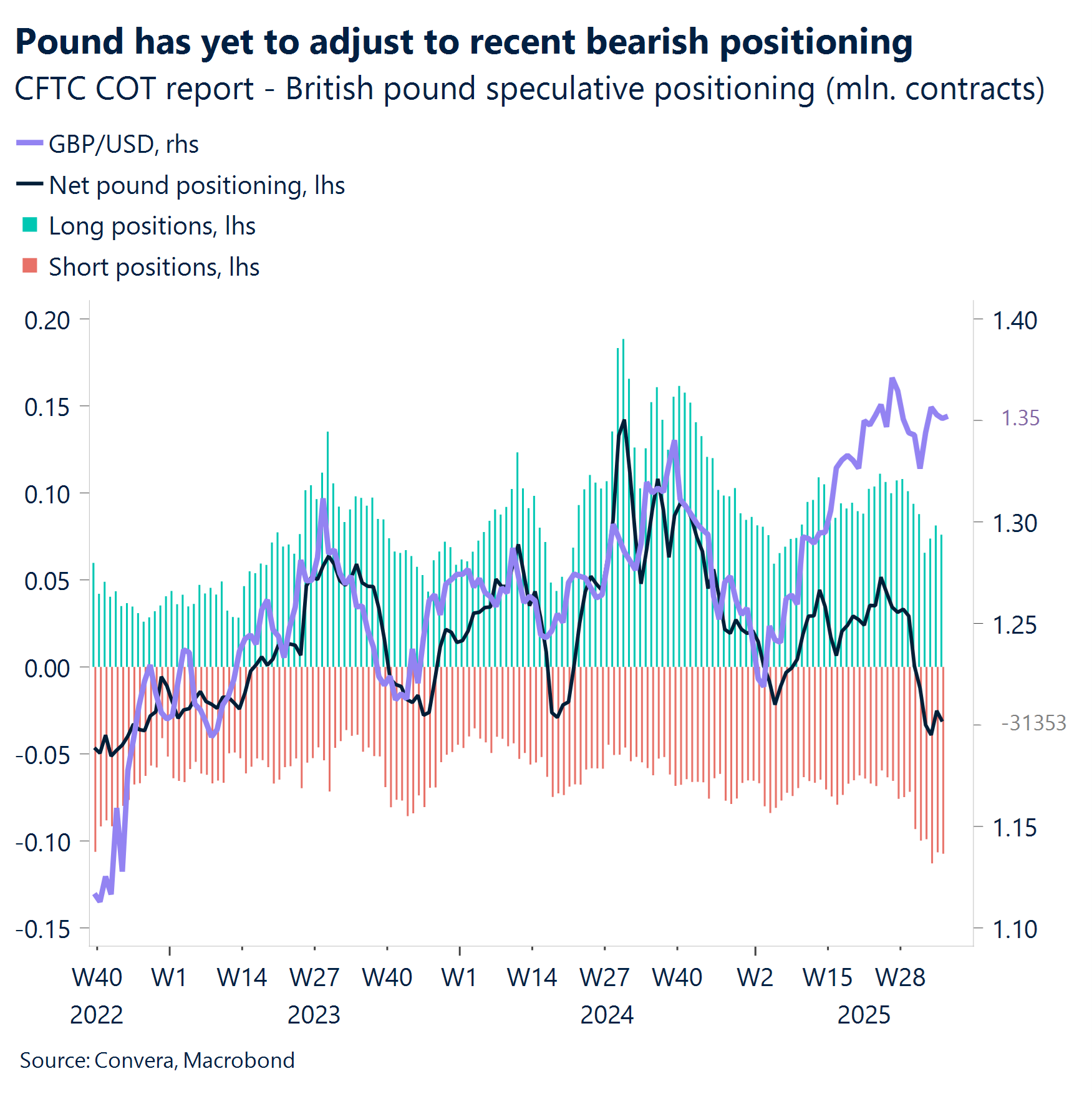

GBP Resilient but risky. Sterling has traded resiliently this week, with GBP/USD rising over 1.5% from last week’s $1.3333 low to test $1.36, before retreating slightly. Gains were driven more by global risk sentiment and Fed rate cut bets than domestic strength. UK front-end yields remain elevated, supporting GBP against low-yielders like JPY and CHF, but long-end gilt yields continue to rise, reflecting fiscal stress and inflation concerns. Domestically, July GDP flatlined, confirming fading momentum after a stronger H1. Retail sales surprised to the upside, but this hasn’t shifted the broader stagflation narrative. Meanwhile, FX positioning data shows a build-up in GBP shorts, yet price action hasn’t fully reflected this, suggesting downside vulnerability. Technically, GBP/USD remains above key moving averages, but $1.36 is proving tough to break. Risks ahead include UK labor and inflation data, which could influence the BoE’s Sept 18 decision, where a hold at 4.00% is expected. The risk of a dovish shift or weak data could trigger a correction in sterling.

CHF Cutting remarks. Swiss National Bank (SNB) Governor Martin Schlegel signaled this week that a return to negative interest rates would face a high bar, while showing greater tolerance for a strong Swiss franc. His comments come as EUR/CHF hovers near 0.93 and USD/CHF dips below 0.80 – levels that reflect a robust nominal franc amid ultra-low inflation, currently just 0.2% year-on-year. The tone suggests the SNB is in no rush to weaken the currency, and that rate cuts – especially into negative territory – are likely off the table for now. In a global FX landscape increasingly shaped by fiscal politics and debt dynamics, Schlegel’s stance lends support to strategic long positions in the franc. A retest of EUR/CHF’s 2025 low near 0.9220 now looks plausible. However, just a day later, Schlegel pivoted somewhat, stating the SNB would not hesitate to cut rates below zero if conditions demand it. That dovish shift pressured the franc lower against both the pound and the dollar, but held firm versus the euro. The SNB’s next policy decision is due 25 September.

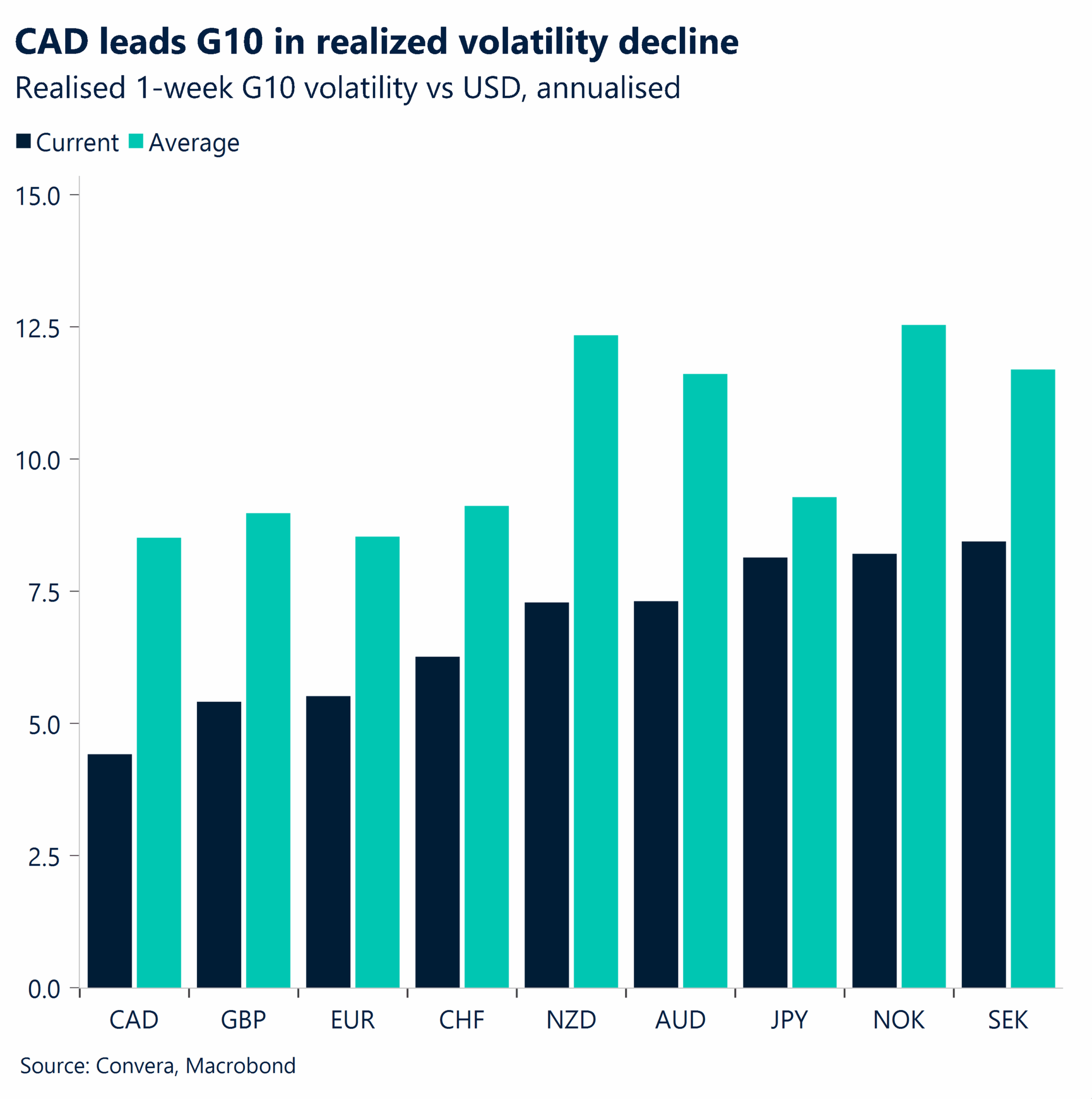

CAD Low vol. No signs of volatility in FX, much less in the Canadian dollar. With few catalysts and a recent weak jobs report, the Canadian dollar has shown little volatility, though it has remained vulnerable to U.S. dollar upticks, After falling as low as 1.378 this week, recent upward pressure has lifted it above 1.385, putting it back above its 20, 40, and 60-day moving averages. Since August, the CAD has underperformed all G10 currencies, which have benefited from renewed U.S. dollar weakness. The Loonie has traded within a range of 1.37 to 1.39, and even with a weaker dollar after this week’s US CPI the CAD has stayed trading above 1.383. The Loonie could be exposed next week, if the upcoming BoC decision and press conference are perceived as more dovish than the Fed’s decision. Before that, Canadian CPI inflation data will provide a clearer picture of how much flexibility BoC Governor Tiff Macklem has, to set a monetary policy path that aligns with recent weak macro data.

AUD Inflate and elevate. Australian inflation expectations jumped to 4.7% in September, reflecting persistent domestic demand pressures. This uptick comes as the RBA maintains a cautious stance, wary that robust consumer spending could delay rate cuts. Fundamentally, the AUD remains underpinned by resilient local data, which has tempered market expectations for aggressive easing by year-end. AUD/USD has reached fresh year-to-date highs. Key support levels are the 21-day EMA at 0.6556 and the 50-day EMA at 0.6526. The next resistance to watch is 0.6688. Looking ahead, traders will be watching for a catalyst from upcoming employment data.

CNH Deflation lingers, but PPI shows signs of bottoming. China’s macro backdrop remains challenging as August CPI slipped 0.4% year-on-year, highlighting subdued consumer demand. However, the pace of producer price deflation eased, with PPI falling 2.9%—a notable improvement from July’s 3.6% drop. This suggests that while domestic demand is still soft, the worst of factory-gate price pressures may be behind us. USD/CNH continues to trade below key resistance at the 21-day EMA of 7.1429 and the 50-day EMA of 7.1615. A close below 7.1100 could pave the way toward 7.1000. Looking ahead, markets will focus on fixed asset investment, industrial production, and unemployment figures for signs of stabilization.

JPY Producer prices sticky, Yen range-bound ahead of BoJ. Japan’s producer prices softened in August, falling 0.2% month-on-month, but annual gains accelerated to 2.7%. Export and import prices remain weak, reflecting ongoing external headwinds. Despite sticky wholesale inflation, the Bank of Japan is expected to hold rates steady at its upcoming meeting, especially after recent political developments reduced the likelihood of an imminent policy shift. USD/JPY remains range-bound, trading above key support at the 100-day EMA of 147.17 and below resistance near the 200-day moving average at 147.83. Technicals suggest a neutral bias in the near term, with range trading likely to persist. However, a decisive break below support could open the door to a deeper correction toward 140. Upcoming trade balance, national CPI, and the BoJ policy decision will be closely watched for fresh direction.

MXN Super peso hits new 2025 high. The Mexican peso has been a standout performer, living up to its “super peso” moniker with year-to-date gains of nearly 12.5% against the U.S. dollar. The most remarkable surge occurred since “Liberation Day” on June 19, with roughly two-thirds of that appreciation, a staggering 8%, happening in just three months. This exceptional resilience is the result of several powerful drivers, including its high-carry attractiveness from elevated interest rates, a stable macroeconomic environment that appeals to global investors, and a broader global appetite for Emerging Market local assets, all of which have solidified its position as a top-performing currency. This week, the CPI for the month of August was released. The latest print shows no clear impact from tariffs, largely due to the USMCA deal. While over 85% of Mexican exports are exempt from new tariffs, non-compliant goods still face a 25% tariff. Additionally, specific 50% tariffs are in effect on steel, aluminum, and copper. A broader 30% tariff was announced but suspended for 90 days, with that pause set to expire in late October. The overall effective tariff rate is not a fixed number, but a weighted average; a recent report from The Budget Lab at Yale estimated the post-substitution effective tariff rate for Mexico at 1.5%. The steady decline in inflation toward Banco de México’s 3% target has given the central bank room to extend its monetary easing cycle. Banxico lowered its overnight interbank interest rate to 7.75% in August, marking its ninth consecutive rate cut since early 2024. As Banxico continues to cut rates, the peso’s resilience will increasingly depend on the pace of future rate adjustments, not only domestically but also from the Federal Reserve.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.