- Decision deluge. From the US Federal Reserve and Bank of Canada, to the Bank of England and Bank of Japan, markets have been steered by a rapid-fire sequence of rate decision of late – each revealing a different tempo in the global monetary mix.

- Dovish North. Recent moves by the Fed and Bank of Canada underscore a weakening macro backdrop across North America, with both central banks signaling a readiness to ease further to shore up economies teetering on the edge of stagnation. Two more 25bps cuts by the Fed this year are expected.

- Cautious BoE. The pound quickly ceded kneejerk gains it made after the Bank of England decision to keep rates unchanged at 4%, a clear sign that any strength will be capped heading into the UK Treasury’s crucial Autumn Budget.

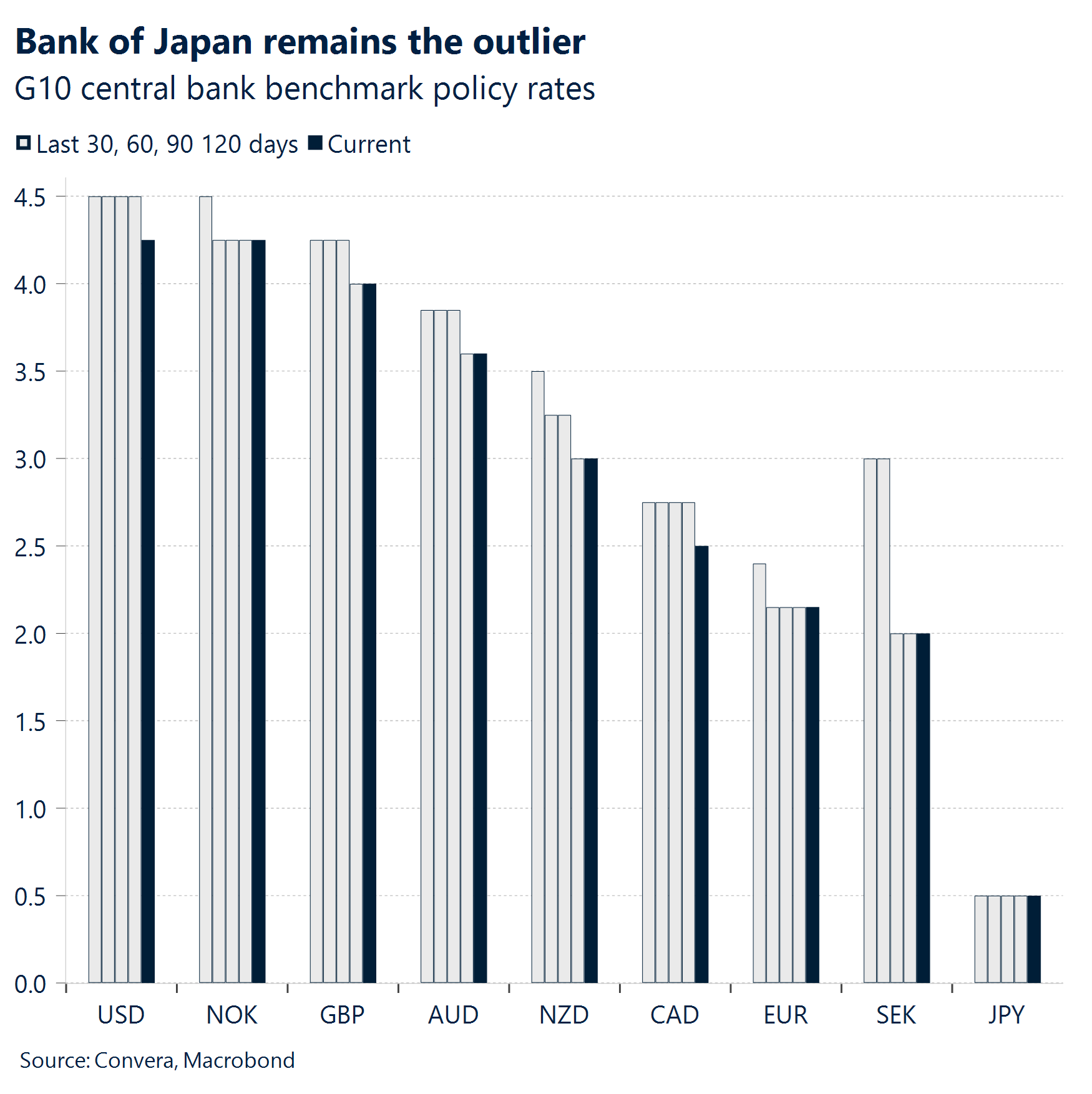

- Hawkish BoJ. The Bank of Japan’s remains the outlier. Two dissenting votes have led traders to price in higher odds of a 25bp hike at the October meeting.

- Quad milestone. With the Fed easing, four key US equity benchmarks, the S&P 500, Nasdaq 100, Dow Jones Industrial Average, and Russell 2000 all closed at record highs simultaneously, a rare event that has occurred only 25 other times this century.

- FX fears. Despite the risk rally in equities, safe haven currencies, like JPY and CHF have dominated this week, while high-beta currencies such as the Scandis and Antipodeans have lagged. The divergence underscores lingering macro uncertainty beneath the surface of the equity rally.

Global Macro

Forward guidance fades from Central Banks playbook

Fed cuts, but internal divisions expected to intensify . The U.S. Federal Reserve delivered an expected 25-basis-point interest rate cut, the first cut since December 2024. Policymakers emphasized the ongoing risks from persistent inflation, suggesting that the path forward would is still uncertain. There is now growing anticipation that internal divisions within the Committee will intensify in the meetings ahead.

Bank of Canada eases to counter weakening economy. The Bank of Canada cut its key interest rate by 25 basis points to 2.5% on Wednesday. This move was largely anticipated and reflects the bank’s shift in focus from inflation to stimulating a weakening economy, particularly amid trade uncertainty and U.S. tariffs. However, the BoC reiterated the challenge of offering forward guidance amid elevated inflation uncertainty.

Bank of England holds steady amid inflation fears. In contrast to the Fed, the BoE decided to keep its interest rate unchanged at 4.0% during its meeting on Thursday. The decision, which was largely in line with expectations, reflects the BoE’s cautious stance as it balances a sluggish economy with inflation that remains well above its 2% target.

Mixed picture on other US macro data releases. Various economic reports painted a complex picture of the U.S. economy. Labor market data showed surprising strength, with initial jobless claims coming in at 231,000, lower than the consensus forecast of 240,000. However, the housing sector disappointed, as new housing starts dropped to 1.307 million, well below expectations. Manufacturing data was also mixed, with a strong surprise from the Philadelphia Fed Index contrasting with a contraction reported by the Empire State Index.

Week ahead

Sentiment under scrutiny

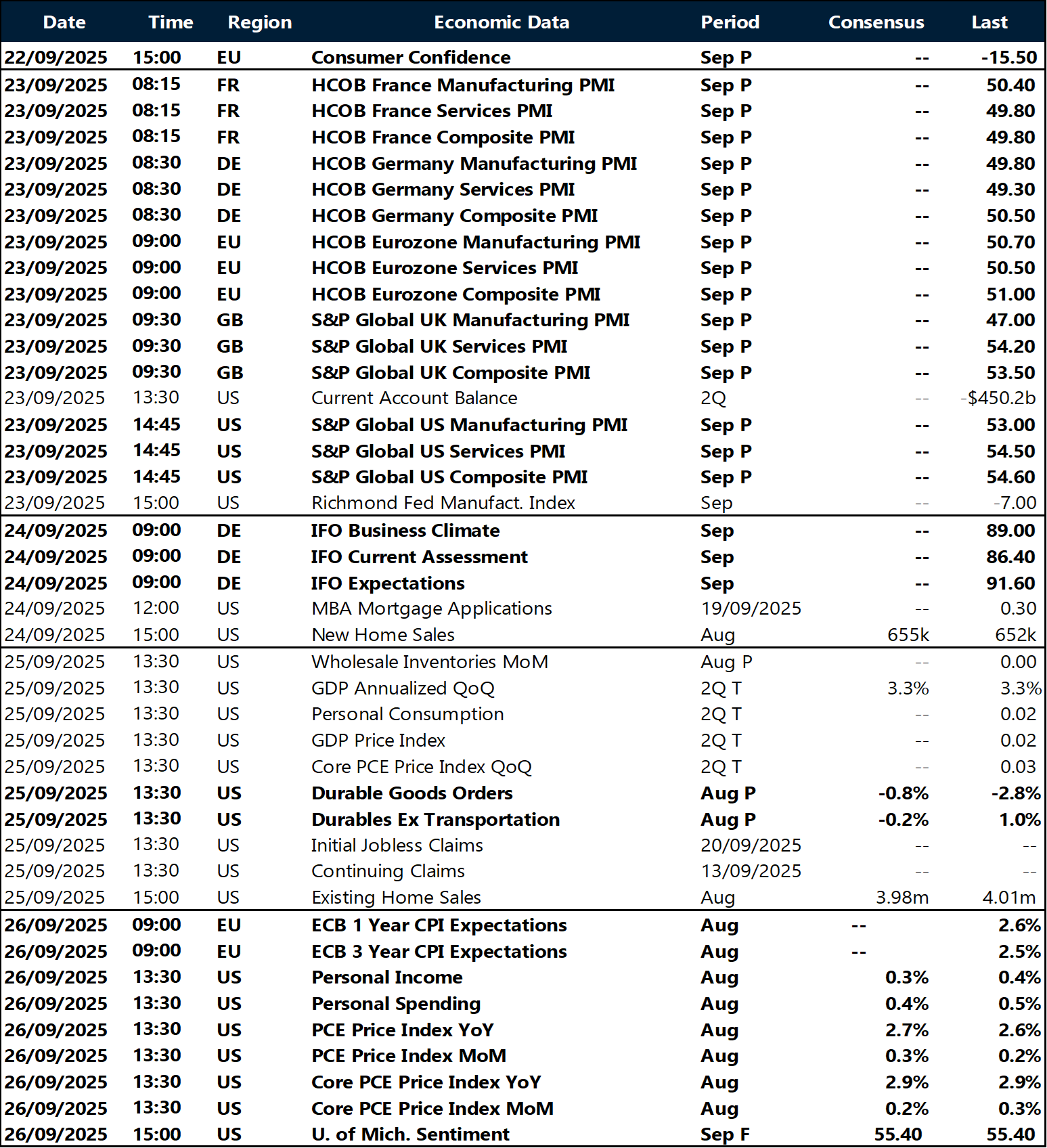

- PMIs in the spotlight. A raft of PMI indicators across the U.S. and Europe (including the aggregate index) will help paint a clearer picture of how both regions are faring under Trump’s tariff regime. So far, the data has been mixed, with little consensus across macro indicators.

- Sentiment meets data. Germany’s ZEW survey showed upbeat expectations earlier this month, contrasting with a more cautious current conditions index. Meanwhile, factory orders plunged, casting doubt on the optimism reflected in leading indicators – perhaps still buoyed by the recent relaxation of the debt ceiling. Uncertainty remains high, and next week’s Ifo assessment will help gauge whether sentiment is beginning to align with economic reality.

- PCE takes stage. The PCE deflator – the Fed’s preferred inflation gauge – is due at a time when the Fed has just enacted a cautious rate cut, prompted by tariff-driven price pressures. The print will either reinforce or challenge the prevailing view that the inflationary impact of tariffs will be short-lived.

- Consumers keep spending. The US personal spending release may complement the upbeat retail sales data from earlier this month, highlighting resilient U.S. consumer demand despite lingering uncertainty.

FX Views

Markets recalibrate expectations

USD Dollar flips fast. The dollar rebounded impressively after a tumultuous week in which the Dollar Index (DXY) fell more than 1% in its early stages. With the wave of acute negative sentiment that had driven the dollar lower — and heightened its volatility — now behind us, we believe it’s reasonable to expect the dollar to become increasingly sensitive to macroeconomic developments and Fed expectations. These factors are likely to dominate price action and exert greater influence on short-term sentiment. While we don’t rule out a partial reversal of recent gains as markets settle, the “hawkish cut” delivered by the Fed — acknowledging the need to support the labour market while maintaining a data-dependent stance — prompted a moderate repricing higher in hawkish bets, as reflected in the 2-year OIS curve. The dollar also found support from a much stronger-than-expected weekly jobless claims report, which showed a ~30,000 drop from the previous week. We expect the dollar to remain firm above the 97 level but lower funding costs should weigh on the buck – especially as seasonal headwinds build into year-end.

EUR Euro edges higher. The euro is on track to close half a percentage point higher against the dollar, with the Fed’s policy meeting serving as the main risk event. In anticipation of what was expected to be a much more dovish outcome, EUR/USD hit fresh highs at 1.1919 before paring back some gains as positioning was readjusted following digestion of the meeting’s more cautious tone than expected. The pair is now finding buying interest around 1.1775, appearing more comfortable at these elevated levels after a complete reshuffling of rate expectations. What began with a hawkish Fed and a hawkish ECB has now flipped – the roles have completely reversed. We expect 1.18 to establish itself as a new support level for the pair. While the 1.20 target for EUR/USD seems more attainable today, the dollar still has heavy lifting to do. It has always been the primary driver of the euro’s rally, especially given that, on the fundamentals front, the ECB has already delivered all it can: the end of the easing cycle. From here, it’s up to the US administration to rattle markets and the Fed to continue cutting rates in order to keep the momentum alive.

GBP Not cuts, no comfort. Sterling traded with mixed momentum this week as markets absorbed a flurry of data and risk events. GBP/USD briefly broke above $1.37, a two-month high, following the Fed’s rate cut and sticky UK wage and services inflation, which reinforced the BoE’s cautious stance and sustained policy divergence. Still, the swift reversal below $1.36, despite the BoE’s decision to keep rates unchanged suggests the rally may be losing steam. Options markets reflect that caution. Risk reversals – a gauge of sentiment toward a currency – continue to point to GBP-negative positioning further out. Against the euro, GBP/EUR remained boxed in a narrow €1.1450–€1.16 range, underpinned by aligned rate expectations and limited macro divergence. Sterling continues to draw support from elevated front-end yields, but upside is capped by stagflation risks, fiscal uncertainty, and slowing growth. Without a clear domestic catalyst, direction will hinge on incoming data and broader risk sentiment heading into the Nov. 26 Autumn Budget.

CHF Volatility drought. The Swiss franc continues to show remarkable resilience, buoyed by safe-haven demand, subdued dollar strength, and Switzerland’s steady political backdrop. USD/CHF briefly dropped to its lowest since 2015 this week. With Swiss inflation remaining marginally positive for three straight months, the Swiss National Bank faces little urgency to ease further. While policymakers keep the door open to FX intervention, they’ve allowed the currency’s strength to persist far longer than many expected – contributing to a collapse in CHF volatility. One-month implied vols have dropped to their lowest since early 2022, mirroring the muted price action that’s kept EUR/CHF locked in a narrow 0.93–0.94 range. The broader context supports this calm: the SNB appears constrained, the ECB is inactive, and global FX remains sluggish post-summer. Even short-dated options tied to the upcoming SNB meeting are pricing in minimal movement. Still, history offers a cautionary note. The franc is known for prolonged periods of quiet – followed by sharp, sudden moves. Traders would be wise not to mistake calm for permanence.

CAD Cut with dovish hints. Following the double header of central bank decisions, the Canadian dollar’s move back above 1.38 reflects a divergence in tone. A dovish Bank of Canada, despite offering no forward guidance, and markets reading Fed Chair Powell’s remarks as unexpectedly hawkish have left the Loonie vulnerable to further US dollar strength. Given the dovish outlook in monetary policy, the CAD should remain unattractive. While both central banks avoided forward guidance amid lingering inflation uncertainty, Canada’s path now points to more easing than was expected a couple of months ago, which is unfavorable for the Loonie. With rate differentials between the US and Canada still wide, and the relative monetary policy landscape largely unchanged, the Canadian dollar remains exposed to further US dollar gains. Next week’s July GDP print will be key to assessing whether the recent economic deterioration extended into the start of Q3. Markets will also be closely watching the US PCE report for August, which is expected to edge slightly higher.

AUD Aussie dips on soft jobs. Australian employment data disappointed, with a decline in full-time jobs and a lower participation rate, though the unemployment rate was steady at 4.2%. AUD/USD slipped to near one-week low after failing to break above 0.6700, where RSI level was in overbought territory. Key support levels lie at 50-day EMA of 0.6547 and 100-day EMA of 0.6506. The market is discounting the weak jobs report for now, instead focusing on global risk sentiment and the prospect of resilient domestic demand. Looking ahead, upcoming manufacturing and services PMIs will be closely watched for further clues on economic momentum.

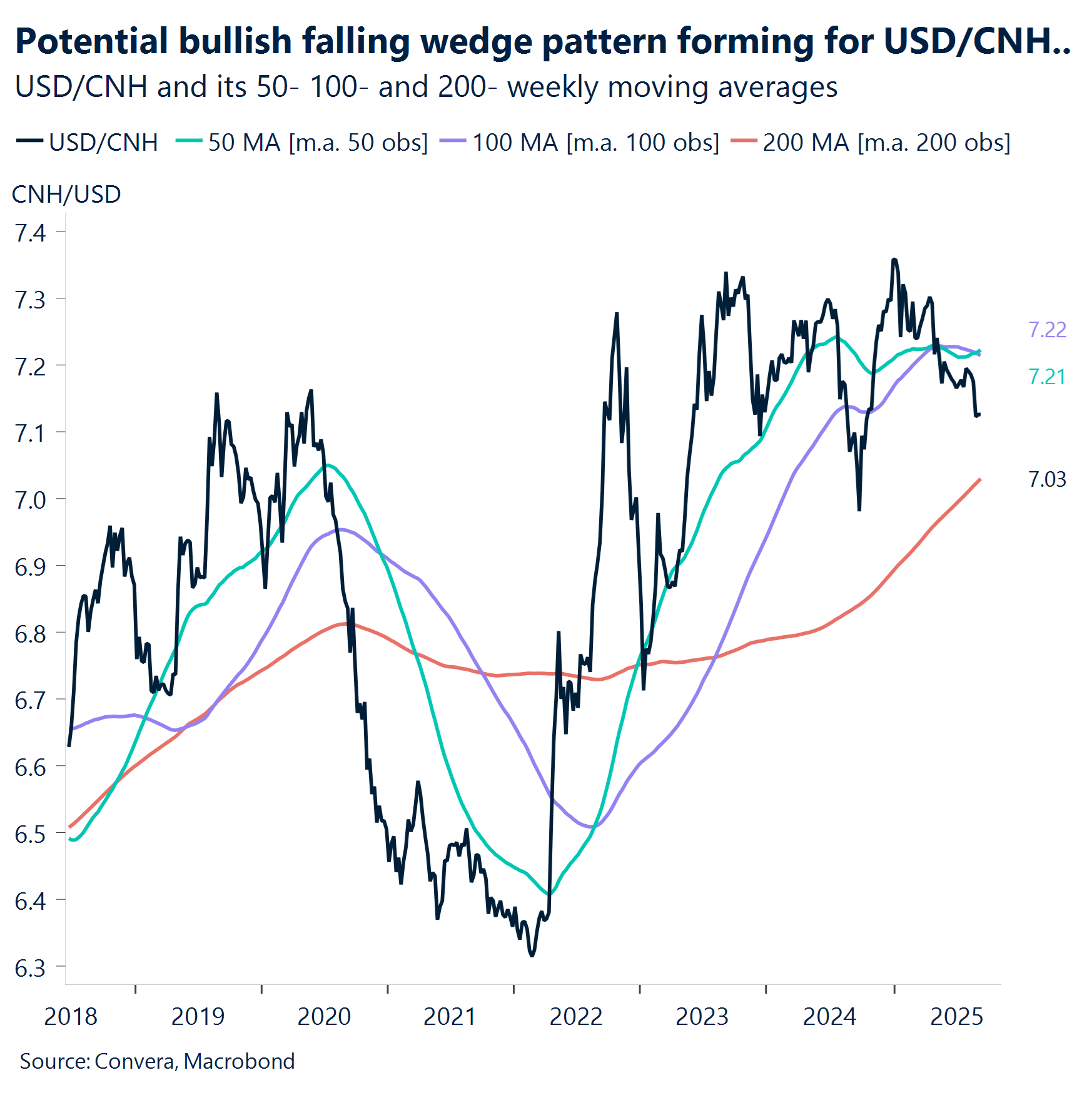

CNH Weak China data may put Yuan on the ropes. China’s latest economic data underwhelmed: industrial output and retail sales both missed expectations, and new home prices continued their steady decline. These signs of economic softness weighed on the yuan, with USD/CNH bouncing off support at 7.0851 and forming a potential bullish falling wedge pattern. Next key resistance levels lie at 21-day EMA of 7.1292, and 50-day EMA of 7.1520. The pair’s resilience above the recent lows suggests a rebound could materialize, especially if the People’s Bank of China signals further policy support. The market’s focus will shift to China’s loan prime rate decision, which could further influence the yuan’s trajectory.

JPY Yen drifts as BoJ plays it safe. The Bank of Japan held rates unchanged, as widely expected, but the decision came with a twist—two board members dissented, and the BoJ unveiled a gradual ETF disposal plan, signaling cautious policy normalization. On the technical front, USD/JPY remains confined between the strong 144.97–146.84 support zone, and resistance below the 147.84 200-day moving average. Momentum is muted and traders appear reluctant to commit until a clear breakout. With the BoJ in wait-and-see mode, USD/JPY is likely to remain range-bound in the near term. Key upcoming data include the Jibun Bank Services PMI, BoJ meeting minutes, and Tokyo core CPI, all of which could provide fresh direction for the yen.

MXN Super peso on a roll. Despite US dollar strength following the Fed’s meeting, the Mexican Peso remains 2% higher month-to-date, supported by a market environment favoring risk and high-yield opportunities beyond developed markets. After hitting a new 2025 low at 18.2, USD/MXN has rebounded from oversold levels and is now finding support near 18.3. The Peso’s most notable rally has unfolded since “Liberation Day,” with roughly two-thirds of its 8% appreciation occurring in just three months. This exceptional resilience stems from a combination of powerful drivers: its high-carry appeal, a stable macro backdrop that attracts global investors, and a broader appetite for Emerging Market local assets, all reinforcing its status as a top-performing currency.Looking ahead, the supportive risk backdrop and expected Fed easing should allow the Peso to continue outperforming, well beyond our short-term floor of 18.5. Even as rate differentials with the U.S. narrow, Banxico has little reason for concern. The central bank is expected to cut rates by 25 basis points next week, bringing the policy rate to 7.5%. The move is largely priced in, and the Peso will remain sensitive to US dollar dynamics and global demand for risk assets.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.