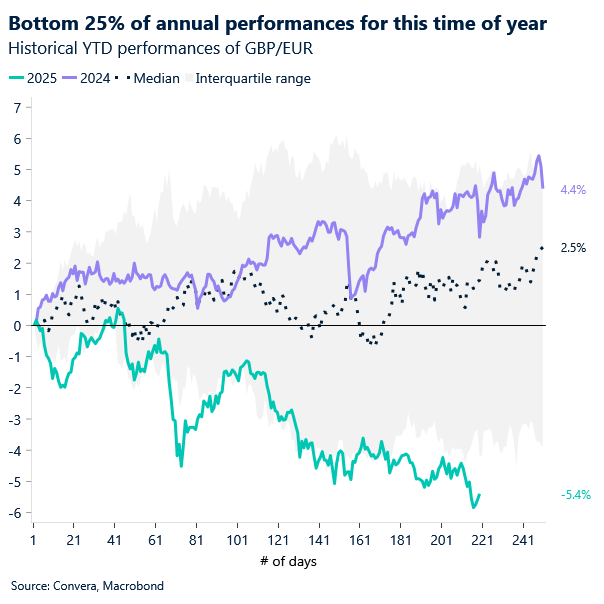

GBP: Relief rallies likely to be capped

The pound has weakened notably over the past month, driven by a combination of softer UK data, heightened fiscal uncertainty, and a dovish recalibration of interest rate expectations. Markets have increasingly priced in further easing from the Bank of England (BoE) as the prospect of looming tax rises grow. This has eased stress in the UK bond market though, dragging gilt yields lower.

The rationale is clear: anticipated tax hikes and tighter fiscal policy are expected to dampen UK growth over the medium term. That softer growth outlook reduces inflationary pressure, giving the BoE greater scope to ease rates. Markets have already responded by lowering their expectations for the terminal rate – now closer to 3.30%, down from 3.60% just weeks ago. This shift has helped narrow the risk premium on longer-dated gilts, easing the strain that had built up earlier in the year.

Crucially, this repricing has also unlocked additional fiscal breathing room. The decline in gilt yields could provide the Treasury with up to £5 billion in extra flexibility – a meaningful cushion as Chancellor Reeves prepares to tackle a fiscal gap estimated to be at least £25 billion annually.

But declining yields hasn’t helped the pound. The pound’s selloff has already absorbed much of the shift in rate expectations, though, reducing downside risks into Thursday’s BoE meeting. If the BoE opts to hold rates, sterling could benefit from a short-lived relief rally. Importantly, however, a hold this week does not change the broader direction of travel. The Bank is still expected to cut rates before year-end and therefore momentum remains tilted toward further GBP downside, so any gains are likely to be shallow and temporary.

This is especially true given the November 26 Budget presents a key risk event. Talk of significant tax increases is stirring uncertainty – a dynamic sterling historically dislikes. While the formal announcement may lift some of that uncertainty and trigger a GBP rebound as well, the longer-term growth impact of fiscal tightening could weigh on sterling and reinforce the case for further BoE easing.

In short, sterling may find some near-term support after the BoE meeting and Budget this month, but the broader macro and policy backdrop remains challenging. Relief rallies are likely to be capped, and the path into year-end still points toward a cautious, data-dependent BoE and a currency vulnerable to fiscal and growth headwinds.

CAD: Is a Christmas election coming?

Is a Christmas election looming in Canada? The Liberal government is set to table the federal budget in the House of Commons today. MPs will have about a week to debate it before the scheduled constituency break. They return on November 17. If a vote of no confidence is triggered that week, a federal election must be called.

Prime Minister Carney is expected to meet with the Leader of the Official Opposition. A key Conservative demand is a firm commitment to reduce the federal deficit, specifically, to keep it under $42 billion. That appears unlikely. Canada’s budget watchdog has projected a worsening fiscal outlook, with deficits and debt rising as a share of GDP. Given the minority government, the Liberals will need support from at least one other party to pass the budget. The Bloc Québécois and the Greens are likely to vote against it, leaving the NDP as the potential kingmaker. If they withhold support, Canadians could be heading to the polls around Christmas.

By law, Election Day must fall between 36 and 51 days after a confidence vote.

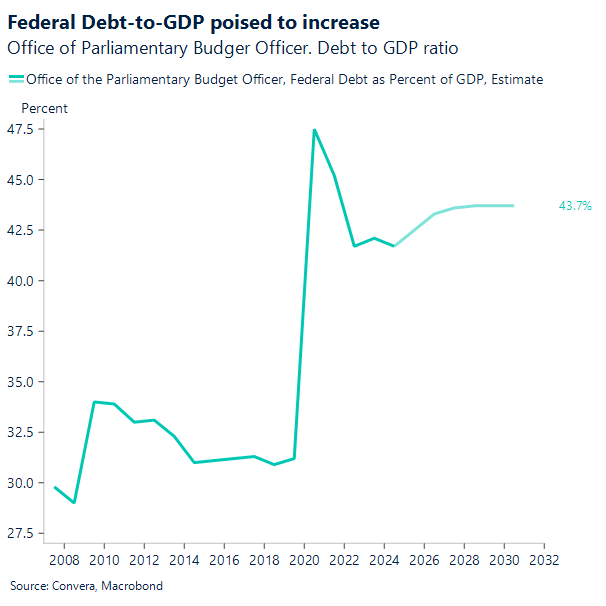

Weeks ago, the Parliamentary Budget Officer (PBO) essentially rung the alarm bell, warning that the federal government’s current financial path may not be sustainable. The PBO’s new report says Prime Minister Mark Carney’s government is on track to run a C$68.5 billion ($49.2 billion) deficit this fiscal year, a significant jump from about C$52 billion in 2024-25. This will see the total federal debt ballooning from an estimated $1.281 trillion in 2024-2025 to $1.655 trillion by 2030-2031.

Perhaps the most critical warning sign is the debt-to-GDP ratio, think of it as the size of the national mortgage compared to the country’s total annual income. For a long time, the government’s goal was to keep this ratio on a steady “declining path,” proving that our debt was manageable. The PBO’s new forecast completely reverses that, showing the ratio will rise to 41.7% in 2024-2025 and remain above 43% for the rest of the decade. The watchdog is now stating in no uncertain terms that this crucial metric is “no longer projected to be on a declining path.”

Canada’s federal finances are currently facing a severe squeeze: on the spending side, massive new commitments for priorities like defense, infrastructure, and housing are expected to add C$115 billion in net new spending through 2029-30, while simultaneously, the “income” side of the ledger is shrinking due to a struggling economy and lower tax revenues (partially a result of U.S. tariffs). This perilous combination of growing liabilities and declining revenue prompted a remarkably blunt assessment from interim Parliamentary Budget Officer (PBO) Jason Jacques, who recently warned lawmakers that the federal government may not even have any “fiscal anchors”, the firm rules or targets necessary to keep the country’s finances on solid ground, essentially warning that Canada is “flying without a compass.” With the Liberal government tabling its highly anticipated financial plan in the House of Commons today, the country’s fiscal state will be the singular focus in Canada, starting now.

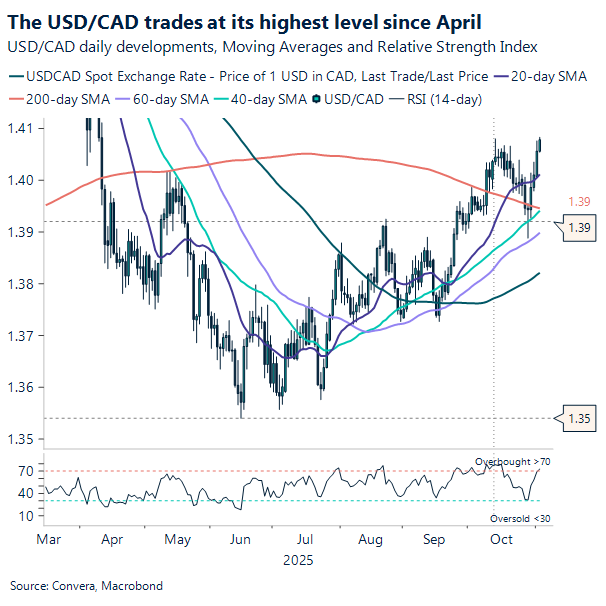

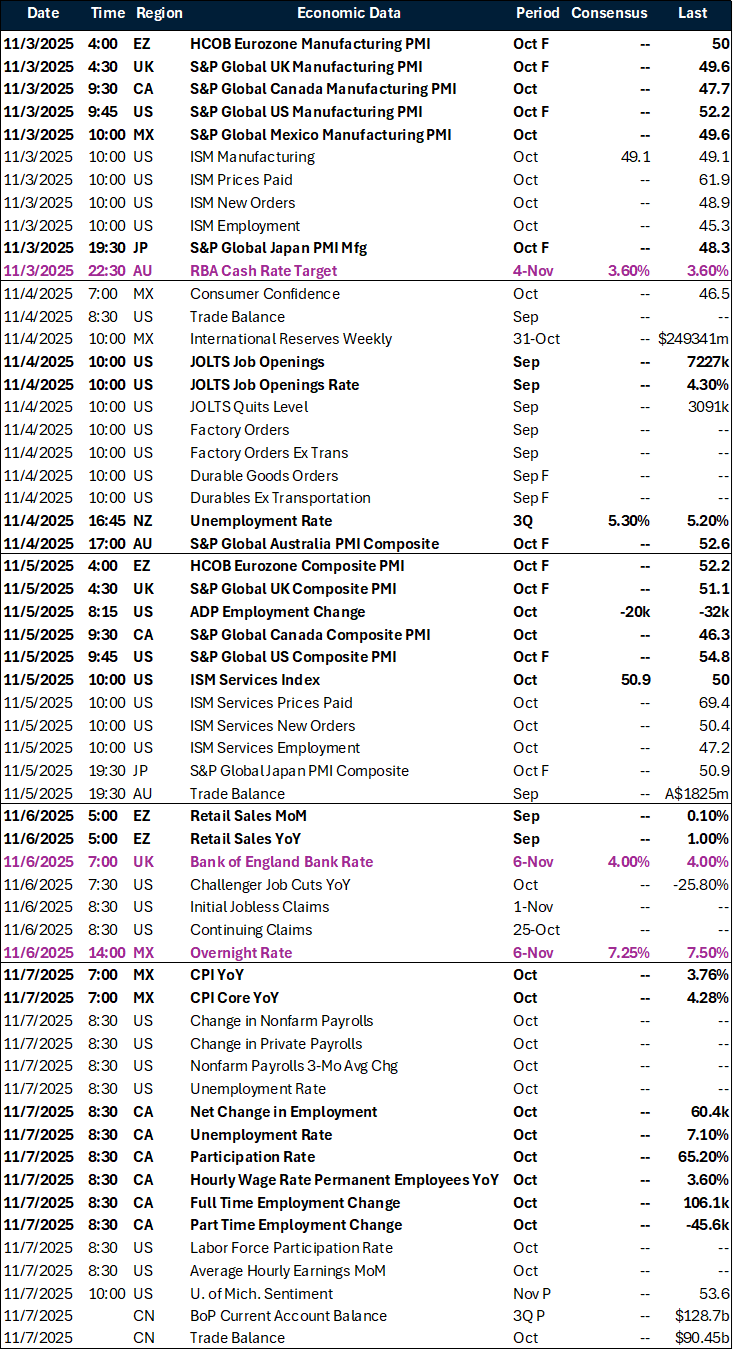

In FX, after the latest GDP figure, the USD/CAD pushed higher to 1.404. The 1.408 level marks a critical short-term resistance for USD/CAD, representing the pair’s highest trade in October and its peak since April. If demand for the U.S. Dollar holds and US labor data doesn’t point to weakness, the Loonie will remain under pressure. In Canada, beyond the federal budget discussions, this week’s employment report is expected to reinforce the central bank’s view of a slowing economy and soft labor market.

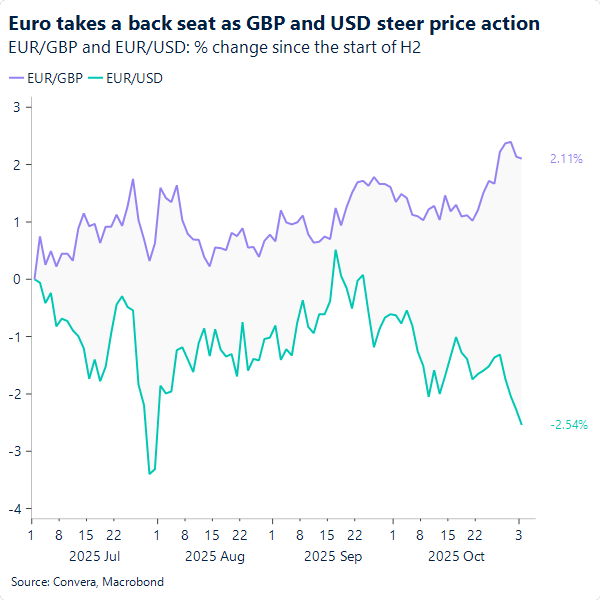

EUR: Bystander in the FX crossfire

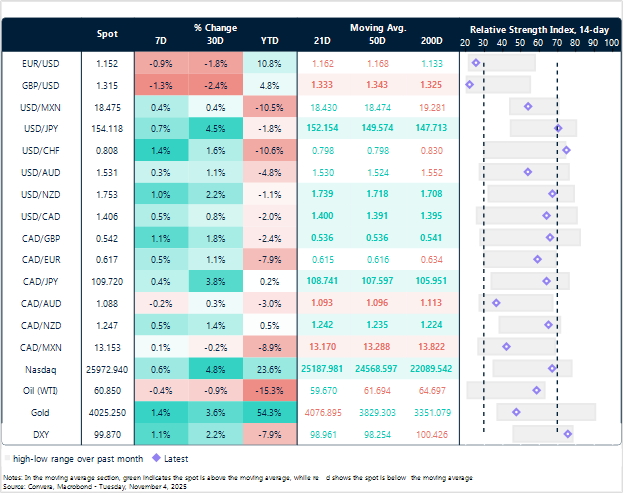

The euro hit a three-month low against the dollar yesterday. The pair has convincingly broken below short-term moving averages – 21-, 50-, and 100-day – and now trades closest to a still-upward-sloping 200-day moving average. This setup points to pronounced short-term bearish momentum, with long-term bears beginning to gain traction as well. With the relative strength index nearing oversold territory in the 35–40 range, EUR/USD spot may well attract buying interest around the 1.15 support level. That said, stronger-than-expected alternative data out of the US this week could test that threshold.

Meanwhile, against sterling, the euro recently hit fresh highs of 0.8818 – levels not seen since early 2023. These contrasting performances, in fact, are not indicative of broad-based euro strength, but rather highlight its relatively neutral role in the dollar’s H2 recovery attempts, and sterling’s structural weakness.

EUR/GBP continues to flirt with what appears to be increasingly fragile resistance at 0.88, with BoE easing bets and the upcoming UK budget casting persistent doubt over sterling’s outlook. This week’s BoE meeting could well be the catalyst to propel EUR/GBP more sustainably above that level, with dovishness still underpriced by markets, in our view.

USD DXY Index crosses the 100 level for the first time since early August

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: November 3-7

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.