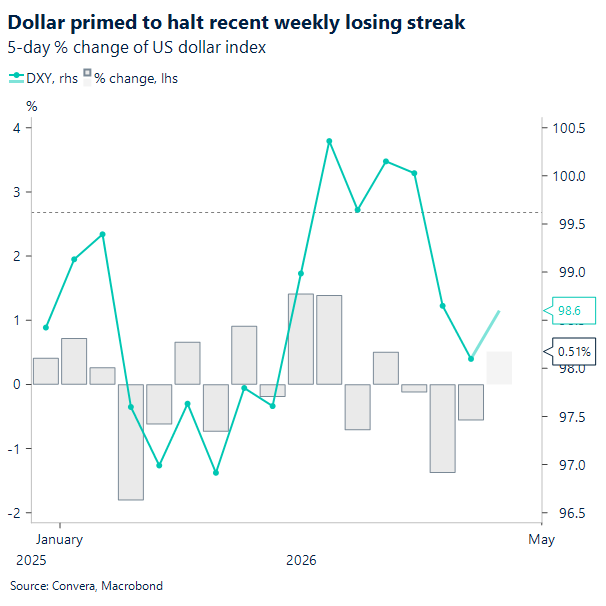

USD: On track to snap 3-week losing streak

The USD backdrop has grown more complex as tensions between the US and Iran over the Strait of Hormuz persist, with neither side showing meaningful movement toward reopening the critical shipping lane. With roughly 20% of global oil flows passing through Hormuz, the ongoing disruption continues to underpin energy risk, keeping WTI above $90 and Brent back above $100 — levels that sustain inflation sensitivity even as broader risk sentiment oscillates.

This has marked a shift away from last week’s clean de‑escalation unwind toward a more nuanced debate around containment and duration. Earlier in the week, the dollar weakened alongside falling crude and improving risk appetite. That move has since stalled. Markets appear increasingly skeptical of ceasefire extensions that fail to translate into tangible progress on shipping flows, leaving the removal of the war premium incomplete rather than decisive.

The US dollar index bouncing off the 98 area reflects that reassessment, as the US currency aims to snap a 3-week losing streak. Higher oil prices have reintroduced a terms‑of‑trade floor for the dollar, while rates markets are signalling that prolonged energy disruption could constrain the Fed’s room to ease. In FX, this has driven renewed pressure on low‑yielding, energy‑importing currencies, while the dollar and select commodity currencies have proved more resilient. With US equities losing momentum too, the USD risks emerging as the primary relative safe harbour if sentiment continues to deteriorate.

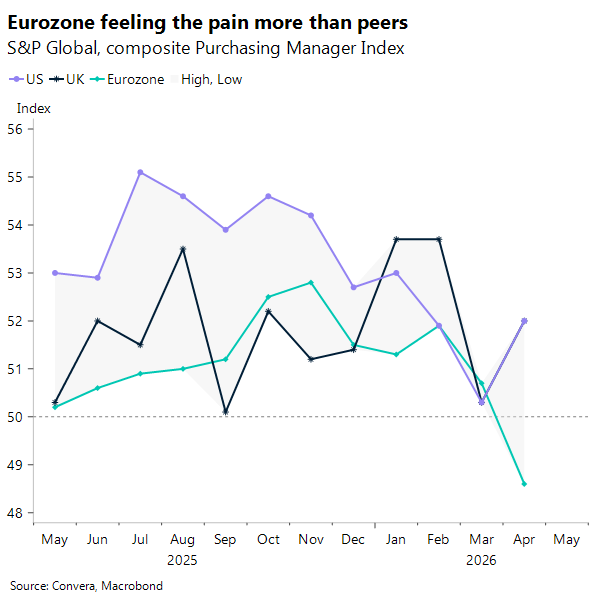

Macro data have reinforced that divergence. The latest S&P Global PMIs showed US manufacturing and services activity beating expectations by a wide margin and outperforming Europe decisively, underscoring ongoing US growth resilience at a time when euro‑area momentum continues to fade. That relative strength helps limit USD downside too, even if risk sentiment picks up again.

EUR: Facing economic headwinds

The euro’s late‑April price action continues to reflect resilience without conviction, as geopolitical volatility increasingly collides with a softening growth backdrop. EUR/USD has unwound most of its March war‑driven losses and remains anchored above 1.17, but repeated failures in the 1.18–1.19 zone highlight the absence of a catalyst for a decisive upside break. Headline swings around the Strait of Hormuz have produced sharp moves in oil, yet FX follow‑through has been limited, reinforcing the sense that markets are now trading uncertainty itself, rather than a clear escalation or peace outcome.

Fundamentals have tilted modestly more negative. Recent German downgrades and weak industry PMIs underline how the conflict is feeding directly into Europe’s confidence, investment, and energy‑sensitive growth channels. The Eurozone composite PMI slipping to 48.6, back into contraction territory, underpins concerns that growth momentum is fading just as energy prices remain elevated.

This complicates the ECB outlook. Inflation risks tied to energy argue for caution on easing, while weakening activity constrains the case for aggressive tightening. Markets remain anchored around two convictions: an ECB hold in April and a hike in June, with expectations for two hikes in 2026 broadly intact. That provides some structural support for the euro, but it has not been enough to displace oil prices and global equity performance as the dominant drivers of EUR/USD.

Relative rates dynamics initially helped underpin euro resilience, with the 2‑year EUR/USD swap spread now around 20bp tighter than pre‑war levels, reflecting the view that the ECB is more responsive to energy shocks than the Fed. However, recent sessions suggest that risk sentiment has overtaken rates as the primary influence. In practice, EUR/USD’s ability to hold above 1.17 now depends less on ECB expectations and more on equity stability, even when oil prices push higher.

Absent a genuine ECB surprise or a clear geopolitical resolution, the euro looks set to remain supported, but capped, with conviction still in short supply.

GBP: Sterling steady, conviction still missing

Sterling traded quietly yesterday, marginally supported by better‑than‑expected April S&P PMIs. The composite index rose to 52 from 50.3, versus expectations for a dip into contraction territory at 49.8. The upside surprise is more likely to reflect firms front‑loading activity ahead of incoming conflict‑related inflationary pressures, rather than a genuine improvement in underlying momentum.

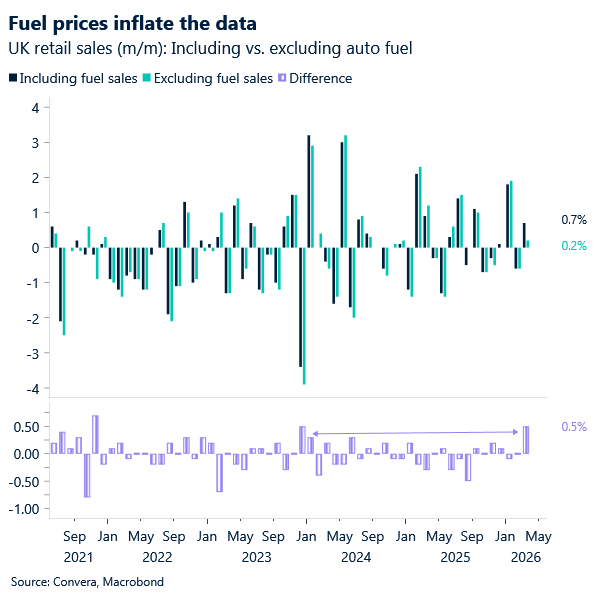

A similar, conflict‑distorted optimism emerged in this morning’s retail sales data, with the m/m print including auto fuel rising 0.7% in March versus a 0.0% consensus. Excluding fuel sales, the increase was more contained at 0.2%, though still above expectations (0.0%), suggesting that the apparent strength in demand largely reflected higher fuel prices.

Even so, as investors continue to parse recent macro data for signs of conflict‑driven economic drag ahead of next week’s slate of central bank policy meetings, these somewhat upbeat releases failed to trigger a more bearish reaction in sterling. If anything, the BoE’s relatively more pronounced hawkish bias – at least as interpreted by markets – may have received some tentative validation ahead of next week’s decision.

That view remains fragile, however, as there is still insufficient data to assess how the increasingly two‑pronged risk profile facing central banks – high prices versus weakening activity, to varying degrees – will ultimately shape perceptions of their hawkish credibility and, in turn, the strength of the FX transmission channel in the months ahead.

For now, GBP/USD is hovering around the 1.34 handle amid limited visibility on the next phase of the geopolitical narrative. We favour a more hesitant grind lower as investors look for signals on how imminent a reopening of the Strait may be. Absent a swift resolution, elevated oil prices would continue to favour the US dollar, while a renewed souring in risk sentiment would have a compounded bearish effect on GBP/USD. In that scenario, the 1.34 level becomes a clear downside target.

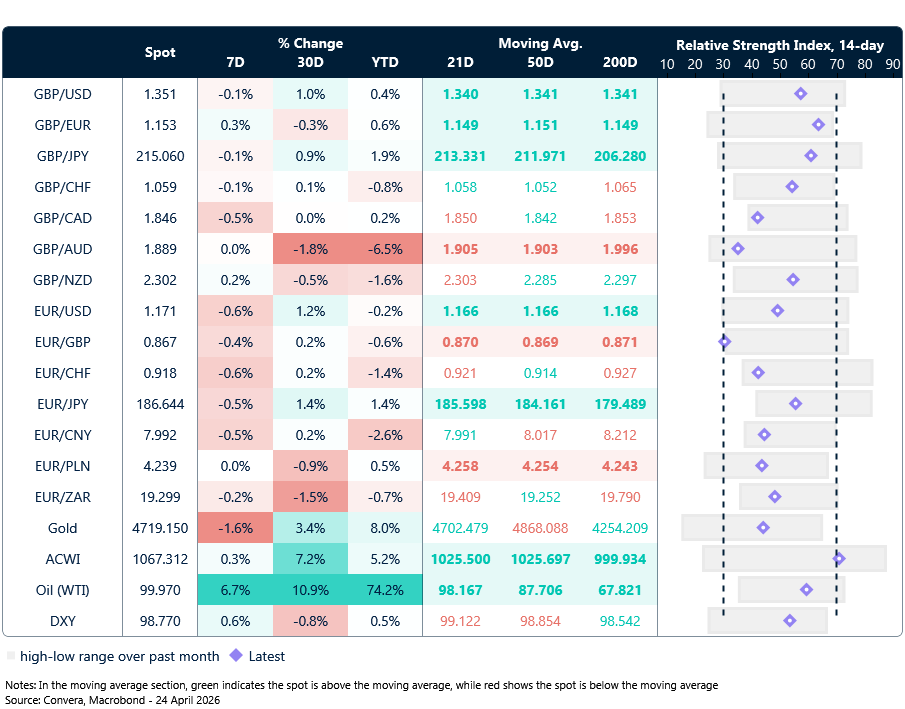

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

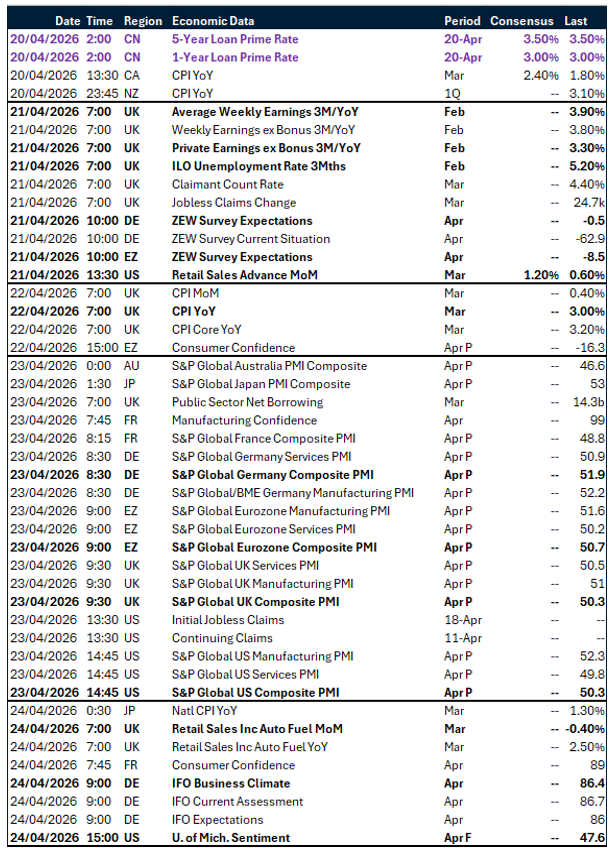

Calendar: April 20-24

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.