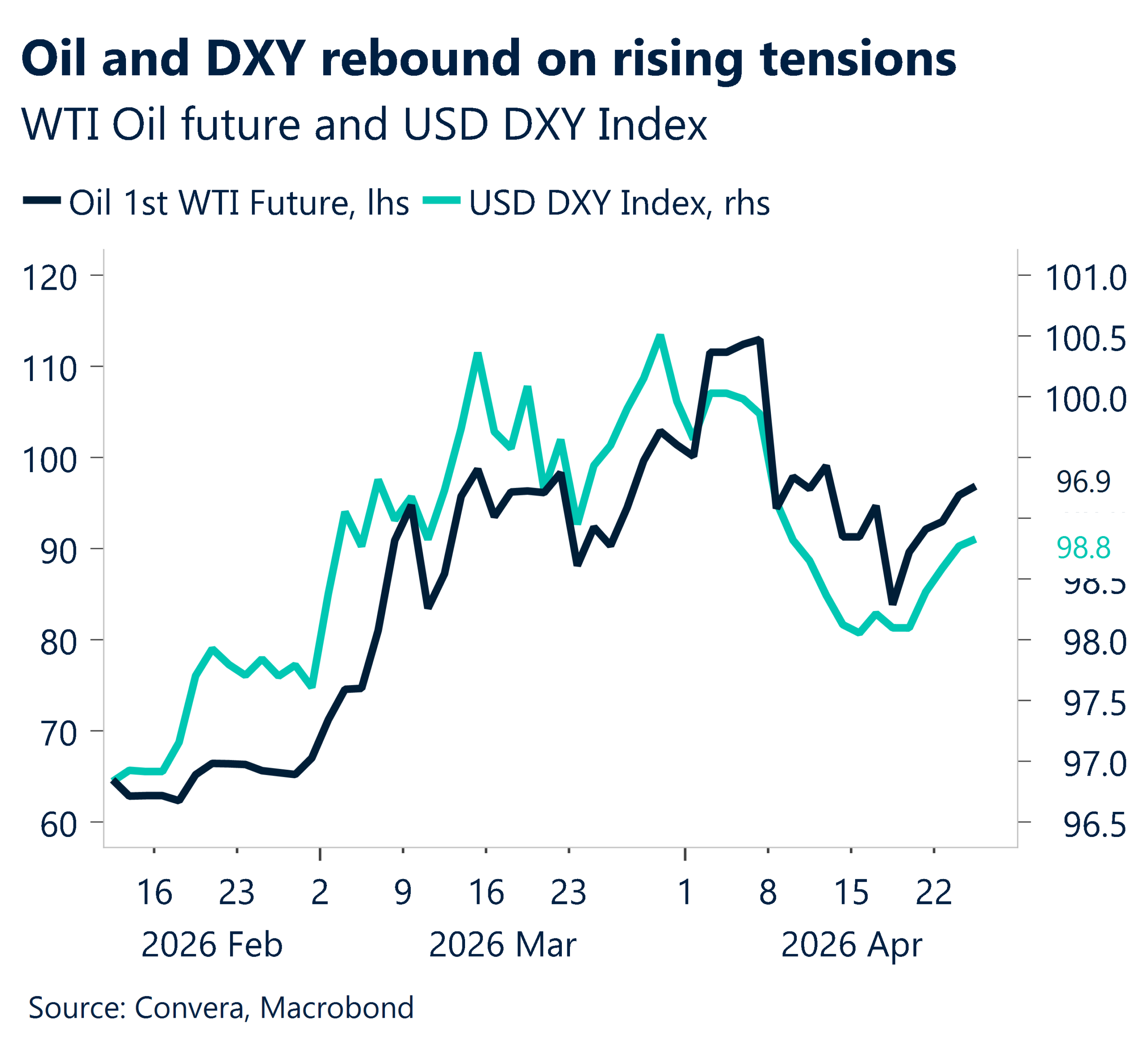

Oil surges on Middle East tensions

Oil prices surged roughly 4%, extending advances to a fourth day, driven by rising geopolitical tensions as the US navy was ordered to strictly enforce a blockade in the Strait of Hormuz. Meanwhile, a three-week ceasefire extension was announced for Israel and Lebanon.

US Treasuries bear-flattened as energy prices climbed and economic data surprised to the upside. Both US services and manufacturing PMIs beat expectations, with input and output price components reaching multi-year highs.

US equities finished lower, weighed down by a broad selloff in major technology names.

In the UK, gilts opened lower with 30-year yields hitting their highest levels since September 2025 after the government made only minimal cuts to long-dated bond sales. Surging UK composite PMIs and price indices further prompted traders to boost bets on near-term interest rate hikes.

In Asia, the Philippine central bank delivered a 25bp rate hike to 4.50%, signaling a return to monetary tightening amid broadening inflation pressures. Concurrently, Japanese officials remain on high alert regarding speculative market movements that continue to weaken the Yen.

In FX, the dollar hovered near 98.77. Overnight, AUD/USD down 0.45%, USD/SGD rose 0.20%, and USD/CNH was flat.

Australian business activity improves

Australian business activity picked up slightly in April, pushing the economy back into mild growth. Services bounced back and manufacturing expanded, though weaker factory output limited the overall lift.

Export orders to North America, Asia, and New Zealand rose modestly, but domestic demand remained soft. Total new business fell for a second straight month, highlighting ongoing caution at home.

Supply chains came under strain as the Middle East conflict pushed fuel and freight costs higher. Delivery times stretched to their longest since July 2022. As a result, business costs rose at the fastest pace since August 2022, prompting companies to lift selling prices to near four‑year highs.

Overall, activity has steadied, but higher prices and stretched supply lines leave the outlook fragile.

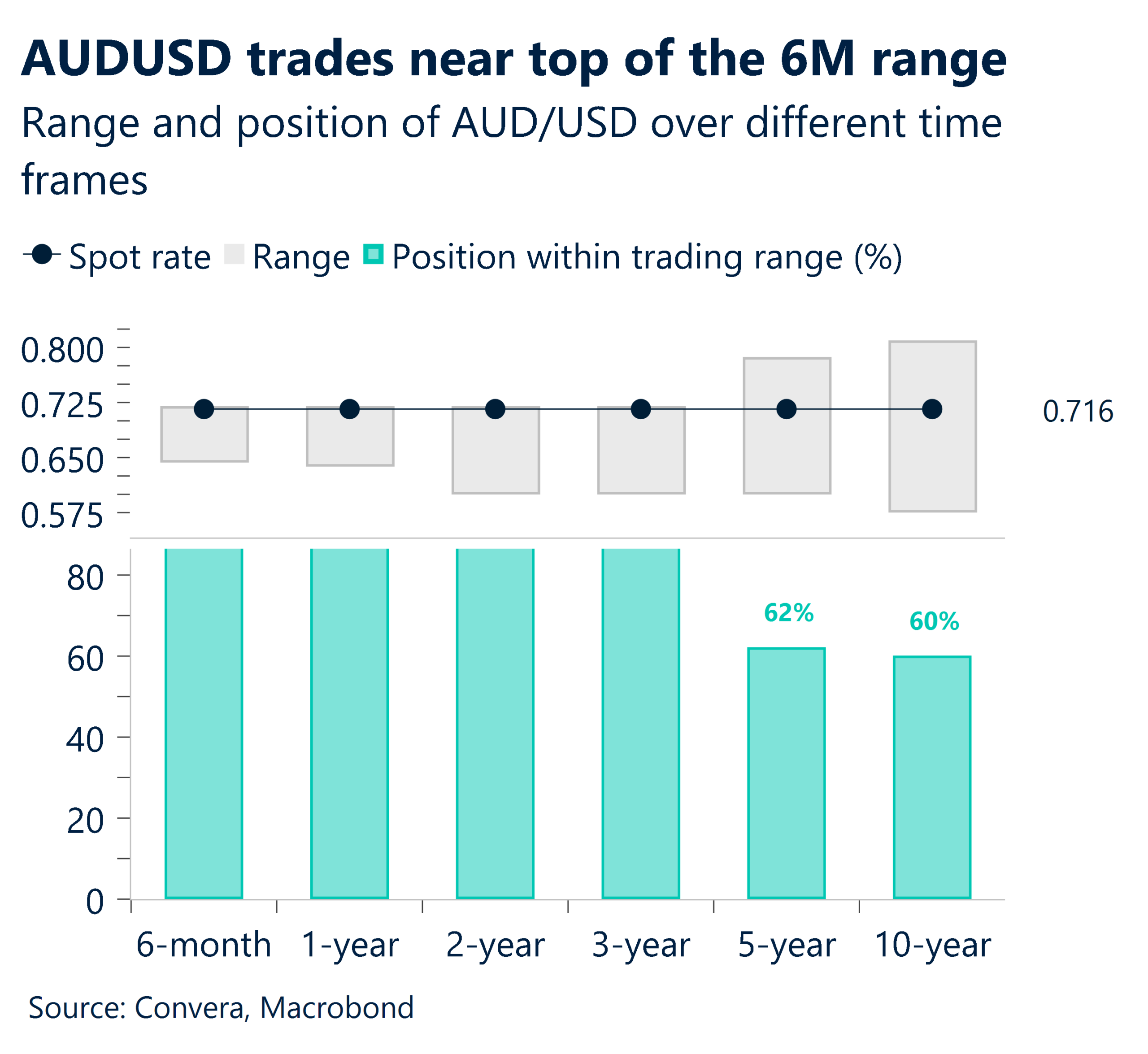

Turning to currencies, AUD/USD now trades about 1.3% below its recent peak near 0.7222, last seen on 17 April. Even so, the pair remains near the top of its six‑month range.

On the downside, initial support comes in near the 21‑day EMA at 0.7087, followed by the 50‑day EMA around 0.7029.

Conversely, next key psychological resistance will be 0.7200.

Jobless claims tick up

US jobless claims came in at 214,000, slightly above expectations. The four‑week average held steady at 210,750, in line with the narrow range seen over the past year. Continuing claims rose to 1.821 million, just above forecasts.

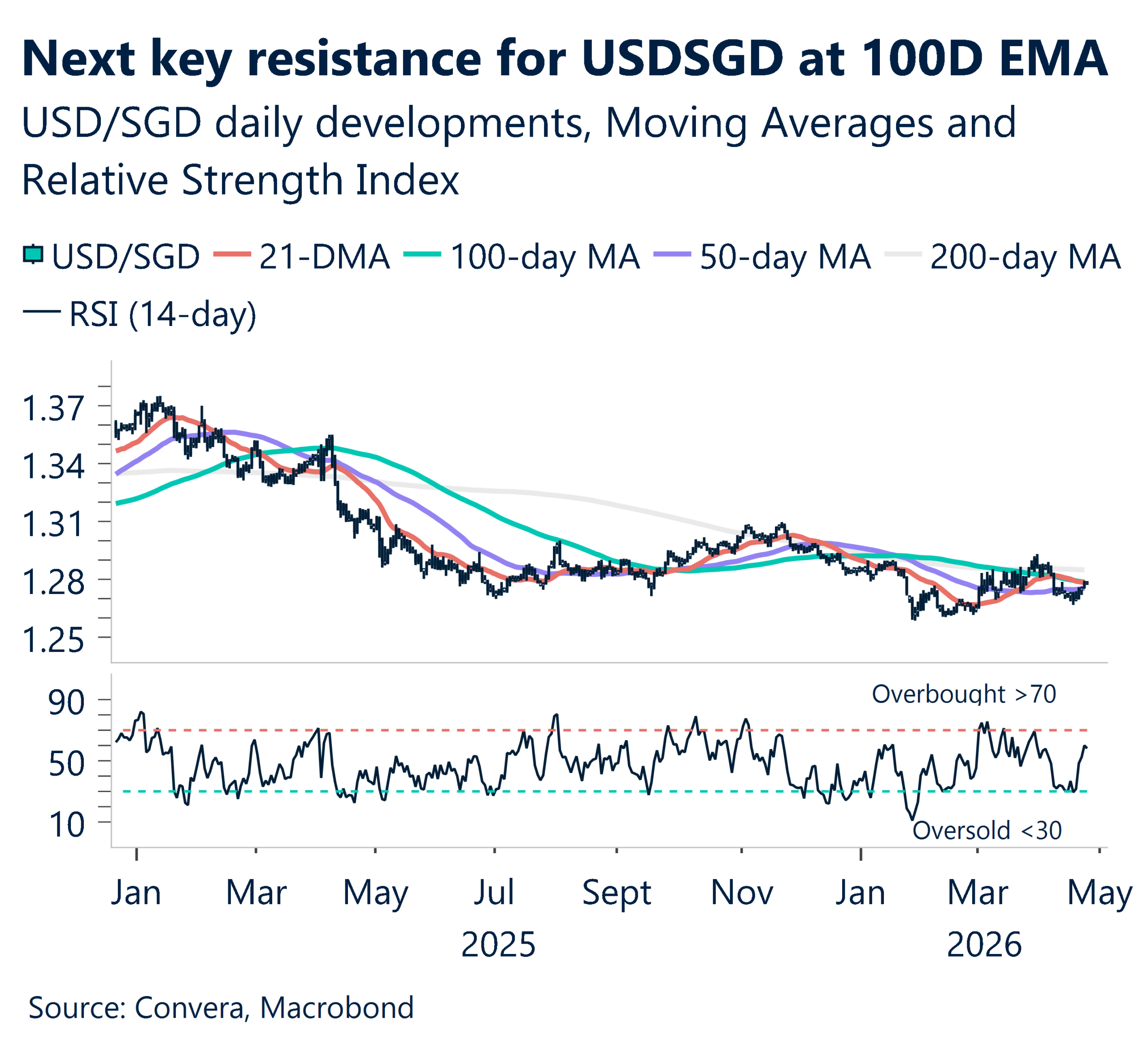

In Asia, SGD/CNH has slipped to its lowest level in more than twelve months.

Meanwhile, USD/SGD is trading about 1.5% above its recent low of 1.2586, last seen on 28 January. The next key resistance sits at the 100-day EMA of 1.2795.

USD buyers may look to take advantage now as we’ve mentioned on previous occasions.

Antipodeans corrected from overbought territory

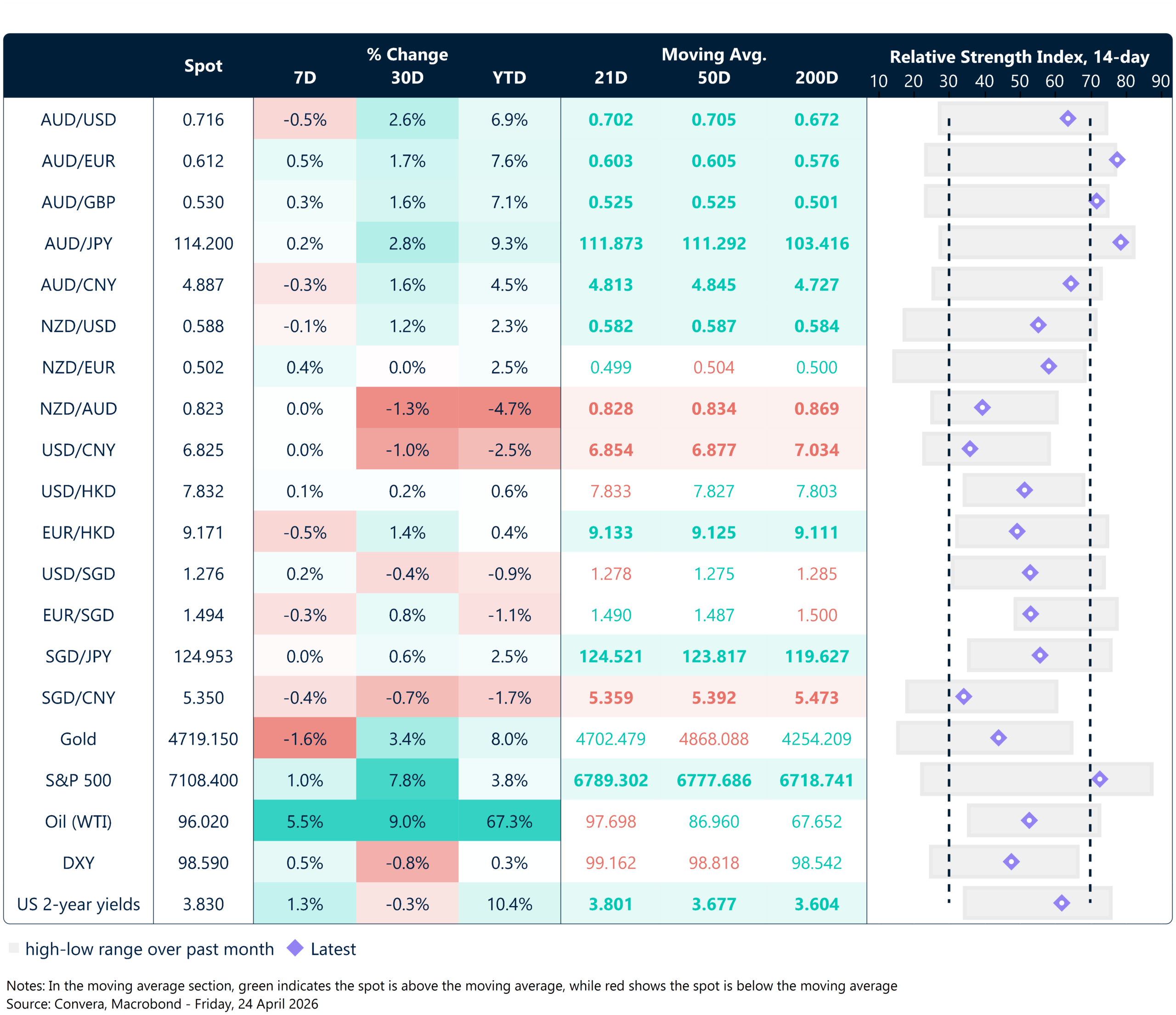

Table: seven-day rolling currency trends and trading ranges

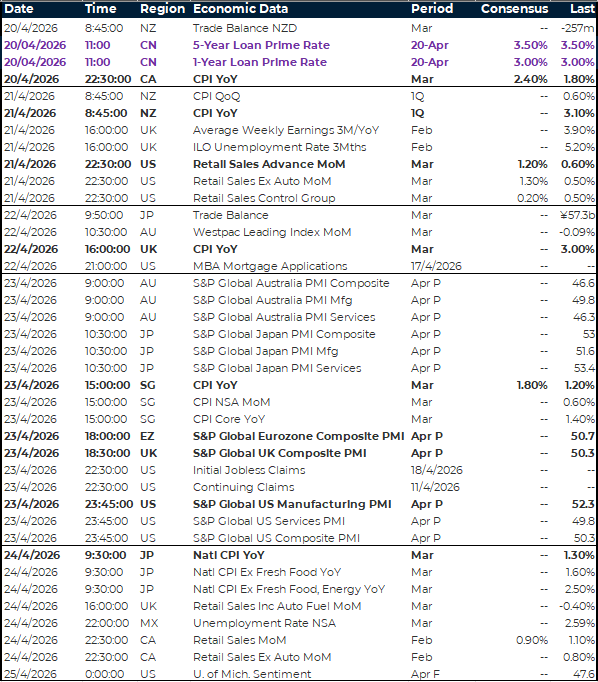

Key global risk events

Calendar: 20 – 25 April

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.