Global markets are rallying today as a potential breakthrough in the Strait of Hormuz sparks widespread investor optimism. US equity futures and Asian indexes climbed after Iran reportedly proposed a ceasefire extension to reopen the waterway through Pakistani mediators. While the US dollar initially spiked when President Trump canceled earlier talks, it retreated to 98.3 once news of the diplomatic offer surfaced.

This geopolitical shift occurs just before a Federal Reserve meeting where Jerome Powell is expected to hold interest rates steady. This session will likely be his last before Kevin Warsh takes over as chair in May. Consequently, all eyes remain on the Situation Room today as the administration evaluates Tehran’s latest overture.

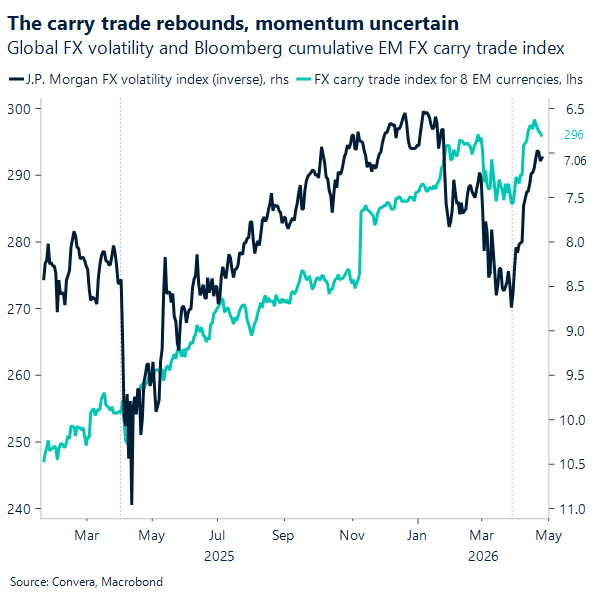

USD: Markets price containment as carry quietly returns

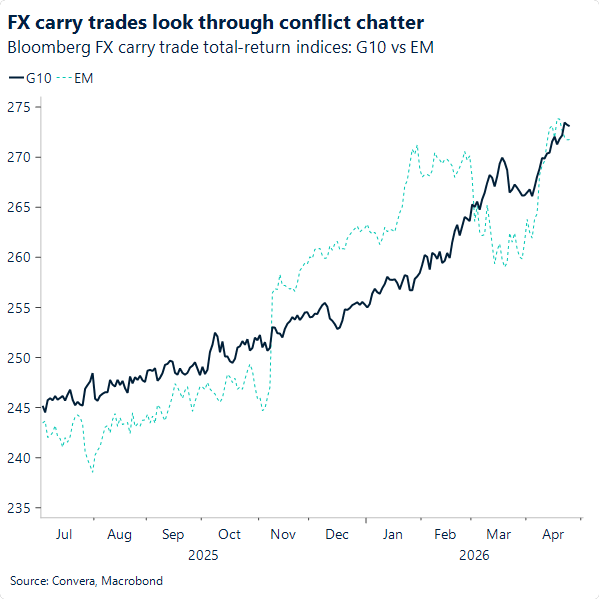

Risk appetite has quietly come back to life, and FX is showing it. As volatility eases, investors typically stop paying up for pure safety and begin looking for yield again. That shift has helped the emerging market carry trade recover some lost ground, as the US Dollar no longer carries the same geopolitical premium it wore during the most anxious stretch of the conflict. However, this does not look like a blind rush into high beta. It feels more selective, with investors leaning back toward yield while keeping a close eye on what sits behind it, especially energy exposure.

Energy is doing more of the sorting this time. In Latin America, net commodity and energy exporters benefit more cleanly when global prices hold firm. Their yields are supported by improving external balances and healthier trade dynamics. By contrast, high yielding currencies tied to net energy importers struggle to keep pace, as higher energy prices act like a current account tax and complicate inflation expectations. Carry is back, but it is no longer one trade. That split is visible in the tape, with the Brazilian Real up roughly 9% year to date versus about 3% for the Mexican Peso.

This is also why the Strait of Hormuz still matters, even when markets feel calmer. Hormuz rarely trades like a simple on or off switch. The current episode is serious, but price action depends on whether disruptions prove persistent and large enough to force a lasting inflation shock. History is instructive here. During the Tanker War, attacks on shipping continued without a permanent closure, and markets ultimately focused on whether navigation risk could be stabilized and priced as a premium rather than treated as a systemic break.

That framework ties the Dollar, carry, and Hormuz together. The Dollar tends to peak when markets fear disorderly outcomes, as safety demand and liquidity preference rise together. When investors start to see disruption as containable or backstopped, that premium fades, and the Dollar reverts toward its funding role. Carry then becomes less about volatility alone and more about terms of trade, with energy exporters and importers diverging sharply. If confidence holds, carry can keep grinding back. If it wobbles, the Dollar will not need much of a push to regain its defensive bid.

A busy week ahead

This week is packed with crucial market updates, starting with a wave of major central bank meetings. Things kick off with the BOJ interest rate decision (Tue), followed closely by the Federal reserve interest rate decision (Wed) and the Bank of Canada interest rate decision (Wed). Rounding out the group, we will see the ECB interest rate decision (Thu) and the BOE interest rate decision (Thu). Most analysts expect all these institutions to simply leave their current policy rates on hold for now. At the same time, Wall Street will heavily focus on corporate results as five of the Magnificent Seven share their latest figures. Massive tech reports like the Microsoft, Alphabet, Amazon.com and Meta Platforms earnings (Wed) will easily dominate mid-week headlines, just before we get the highly anticipated Apple earnings (Thu).

Beyond those central bank moves and big tech announcements, fresh economic data will play a huge role in driving investor sentiment. Markets will closely watch first-quarter growth readings, specifically the US GDP A (Thu) and the Euro-area GDP A (Thu), to gauge the underlying strength of the economy. Because inflation remains a stubborn global issue, experts will also scrutinize the US core PCE price index (Thu) alongside the Euro-area CPI P (Thu) and the Japan Tokyo CPI (Fri). Finally, global manufacturing health will get a major pulse check with the release of the China PMI (Thu). Altogether, this steady stream of critical reports should give everyone a much clearer picture of where the global economy is heading next.

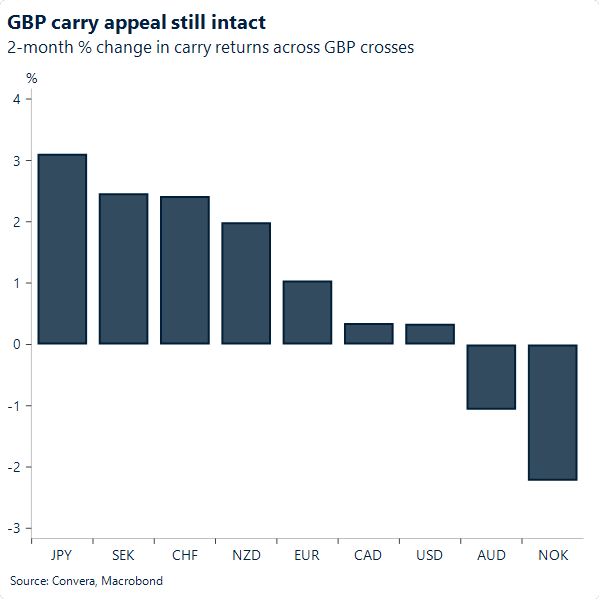

GBP: Hawkish bias, real carry appeal

Sterling ended last week broadly higher against the G10 complex. A slate of stronger‑than‑expected macroeconomic releases – against a backdrop of fragile but still‑intact risk sentiment – brought the familiar hawkish stickiness of the Bank of England, and sterling’s associated carry appeal, into sharper focus ahead of this week’s policy meeting.

Markets currently price just over two rate hikes by year‑end, and with the policy rate already at 3.75% – among the highest in the G10 – sterling has attracted renewed demand from a carry‑trade perspective.

Importantly, this carry appeal remains intact:

We interpret this as investors continuing to discount geopolitical tail risks, with long‑term growth and inflation expectations still anchored: Long‑dated bonds have continued to sell off to geopolitical headlines, signalling that markets are reluctant to price in a structural low‑inflation, low‑growth regime, and are instead repricing uncertainty and fiscal‑related term premia. Stable 5y5y forward inflation swaps and real 10‑year yields reinforce this interpretation of the yield curve.

Against this backdrop, sterling appears better positioned to benefit from any hawkish signals from the BoE this week, particularly relative to the euro. In fact, the conflict narrative has also been less punitive for sterling than for the single currency, with investors viewing the UK shock primarily as a price issue rather than a growth one – reflecting the UK’s lower physical exposure to imported energy versus the euro area. This environment supports a cleaner FX transmission channel from policy expectations for the pound.

Barring significant developments on the domestic UK political front this week, we therefore maintain a mild upside bias for GBP/EUR, with a test of 1.1550 likely. For GBP/USD, we retain a more neutral stance amid still‑fragile but not materially deteriorating geopolitical conditions, and see 1.35 as a reasonable trading anchor for the week, absent meaningful geopolitical developments.

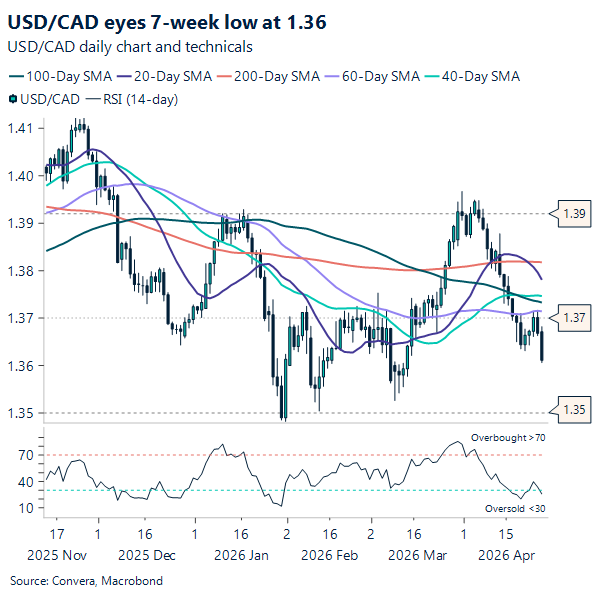

CAD: USD/CAD eyes 7-week low ahead of BoC meeting

The Canadian Dollar started the week on a strong note, pushing the USD/CAD pair down toward 1.361, which after 3 consecutive weeks of moving down, it nears now a seven-week low. This recent strength reflects a notable 2.2% gain for the Loonie over the past month, partly supported by a softening US Dollar as diplomatic hopes regarding Iran ease global tensions.

Looking ahead, investor attention is firmly fixed on Wednesday’s Bank of Canada meeting. While Governor Macklem is widely expected to maintain the overnight rate at 2.25%, the market remains highly sensitive to the central bank’s underlying message. A surprisingly aggressive tone from the Governing Council could further bolster the Canadian currency, making the policy statement far more influential than the interest rate decision itself.

Macklem has been increasingly clear that the bigger risk may no longer be doing too much, but doing too little. Medium‑term inflation expectations are now sitting at the upper end of the Bank’s target range, and that’s clearly getting attention in Ottawa. One small but telling shift was the removal of language describing the current policy stance as “appropriate.” It’s a subtle change, but it opens the door to the idea that rates may need to move higher if progress on inflation stalls.

Wednesday’s BoC messaging, combined with the Fed decision and February GDP prints on Thursday, should provide more clarity on the CAD’s direction. If Macklem strikes a firmer tone while the dollar remains subdued, the Loonie may get a reason to break out further below 1.36.

That said, the backdrop remains fragile. Conflict-driven headlines, a packed global central bank and macro calendar, and lingering growth concerns mean any move is unlikely to be one‑way traffic. If growth anxieties resurface, the Canadian dollar may struggle to gain traction and could stay anchored closer to the 1.37 area, at least until the macro picture becomes clearer.

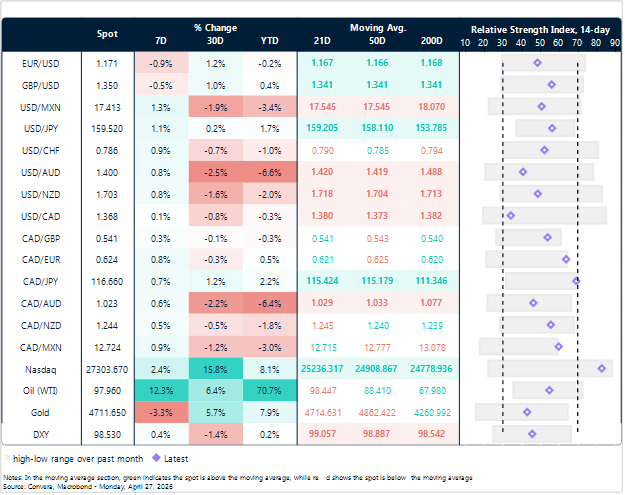

Market snapshot

Table: Currency trends, trading ranges & technical indicators

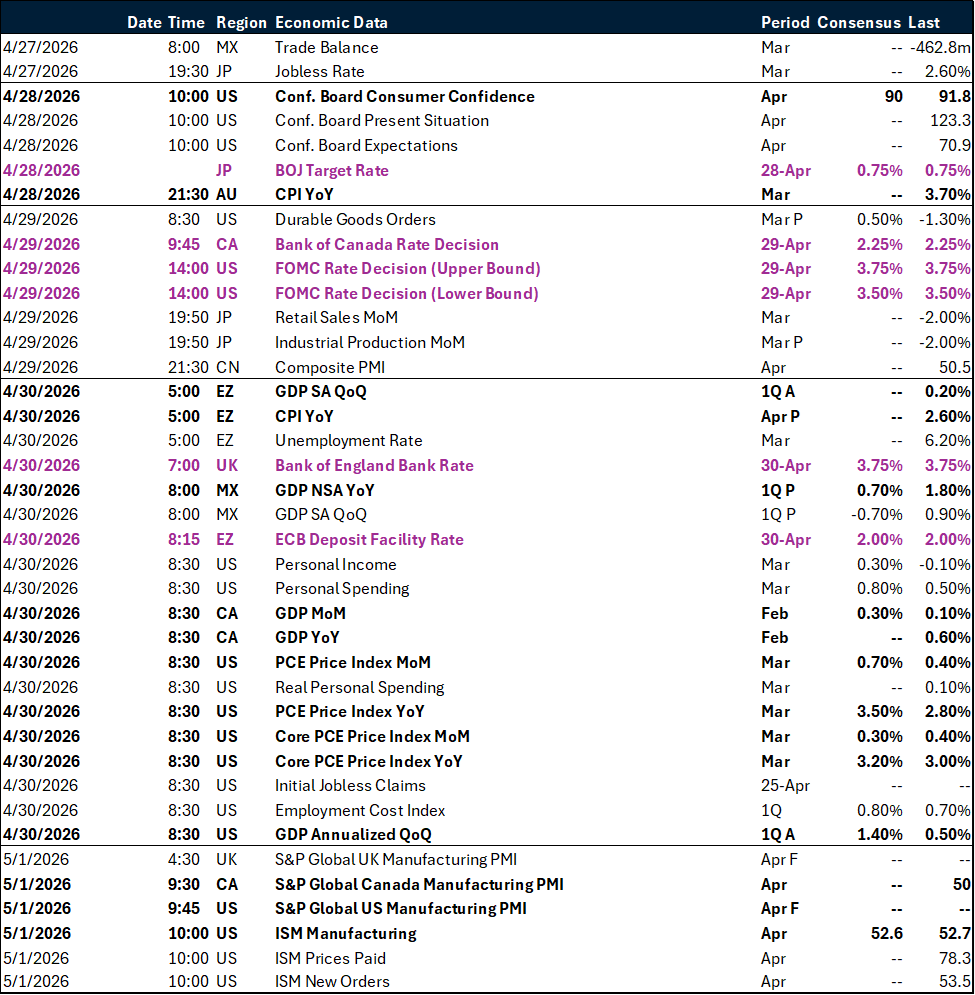

Key global risk events

Calendar: April 27 – May 01

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.