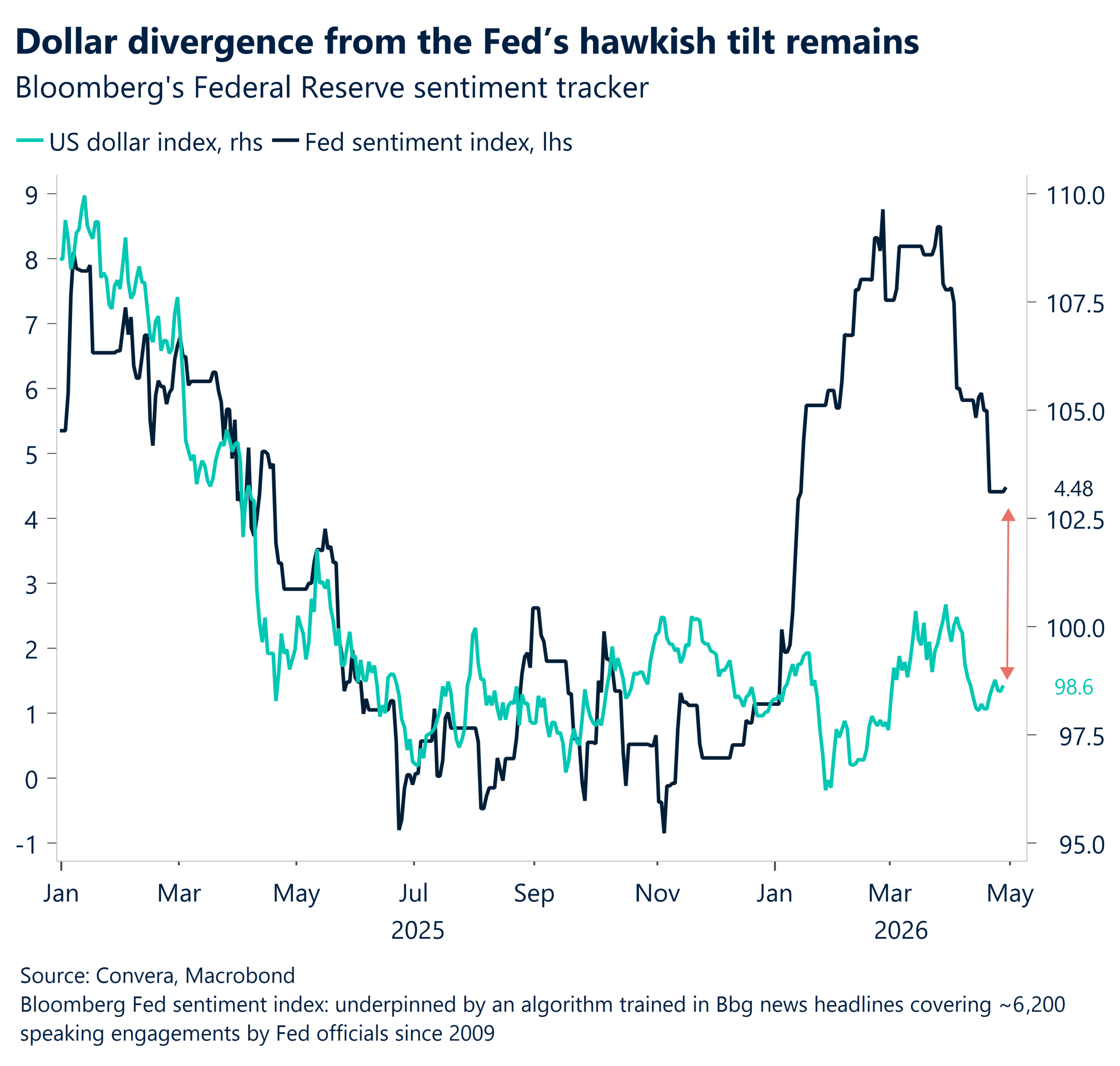

Greenback gains as Federal Reserve delivers most divided decision in decades

The US dollar strengthened after the Federal Reserve held interest rates steady overnight, but the decision exposed deep divisions within the central bank.

The Federal Open Market Committee vote included four dissents, making it the most divided Federal Reserve decision since the early 1990s.

Three voting members argued against signalling future rate cuts, citing inflation risks and resilient economic conditions. In contrast, Trump‑appointed board member Stephen Miran dissented in favour of an immediate 25 basis point rate cut, arguing policy had become unnecessarily restrictive.

The extent of disagreement highlights the growing tension between inflation control and concerns about slowing growth. Despite holding rates unchanged, the tone of the outcome was interpreted as mildly supportive of the US dollar, given the resistance among several policymakers to easing policy too quickly.

In his final press conference as Federal Reserve Chair, Jerome Powell said he intended to remain in his role until he was confident that ongoing Department of Justice investigations would not be reopened, adding an additional layer of uncertainty around future leadership.

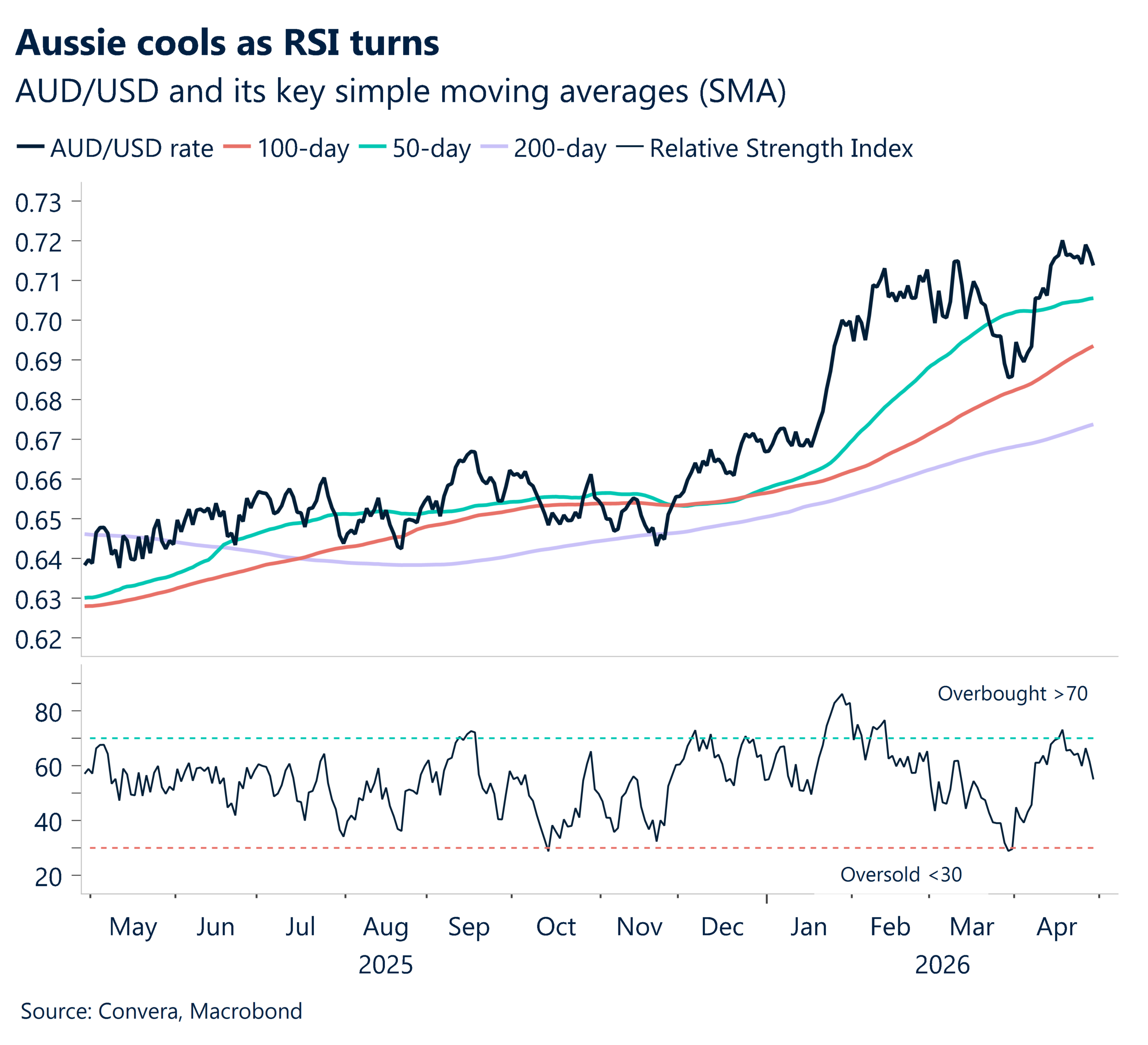

Australian and New Zealand dollars slide after inflation data

The mainstream media highlighted yesterday’s Australian inflation numbers as making rate hikes a certainty but the reaction in financial markets was more nuanced.

Headline annual inflation came in slightly below expectations at 4.6 percent, compared with 4.8 percent expected. The closely watched trimmed mean inflation measure, which strips out volatile items, was unchanged at 3.3 percent, broadly in line with forecasts.

As a result, market pricing for an interest rate hike at next week’s Reserve Bank of Australia meeting edged lower. The implied probability of a hike fell from around 80 percent on Tuesday to roughly 74 percent after the data.

Meanwhile, Reserve Bank of New Zealand Governor Anna Berman pushed back against fears of renewed tightening, noting that inflation in New Zealand remains within the central bank’s 1 to 3 percent target band. Her comments helped ease expectations of further rate increases across the region.

In foreign exchange markets, AUD/USD and AUD/NZD both fell around 0.9 percent, reflecting a combination of softer rate expectations and broad US dollar strength.

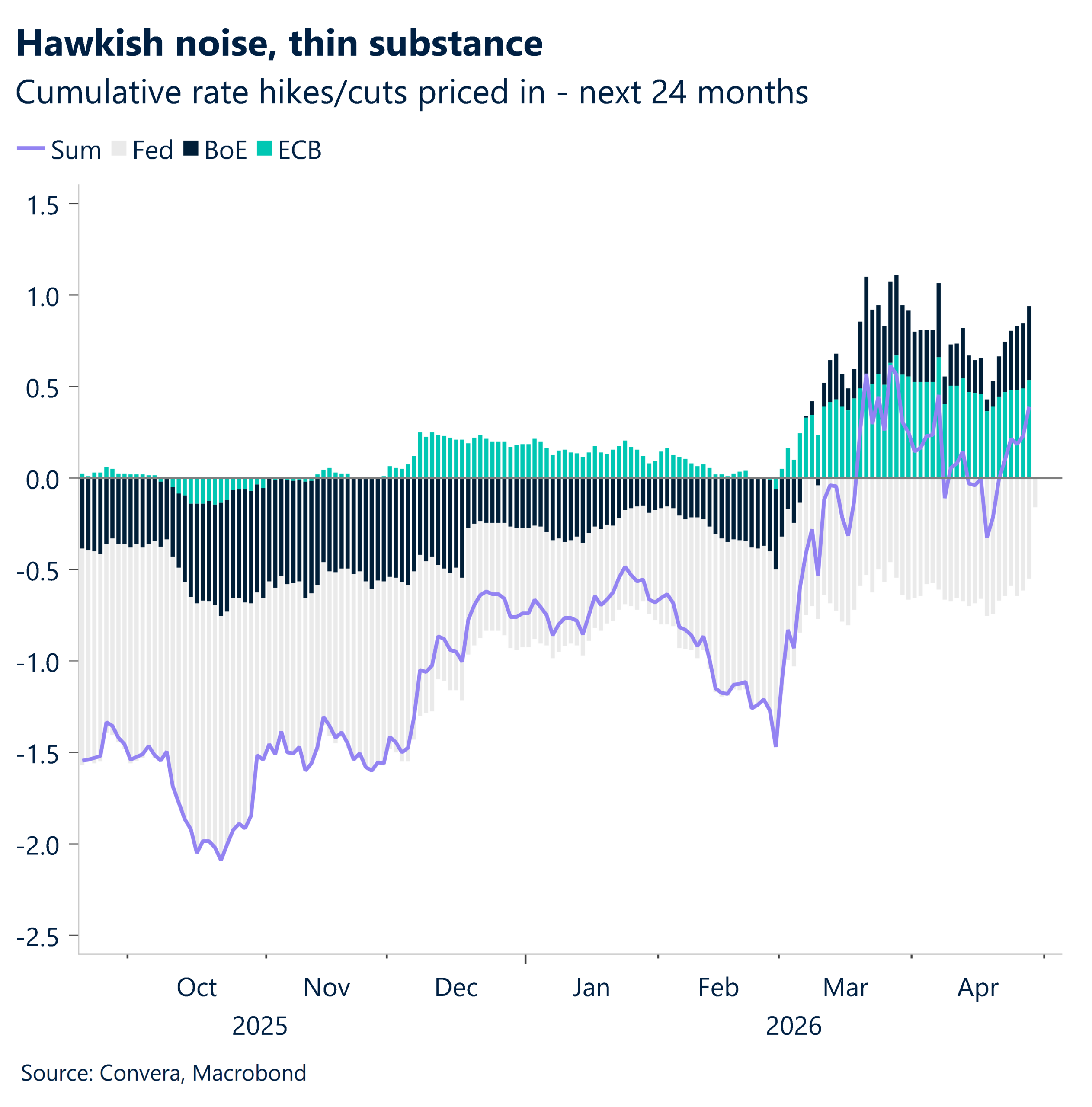

Bank of England and European Central Bank up next

After a non-stop week of global central bank meetings, attention now turns to the Bank of England and the European Central Bank.

The Bank of England meets at 9.00pm AEST. Markets see little chance of a rate increase, with pricing suggesting only a 10 percent probability of a hike from the current 3.75 percent policy rate.

Sterling has generally weakened in recent sessions. AUD/GBP remains near two‑year highs, although momentum has faded. Technical indicators such as the RSI (Relative Strength Index) and MACD (Moving Average Convergence Divergence) point to waning upside momentum and the risk of near‑term pullbacks.

By contrast, the pound has performed better against the Singapore dollar and New Zealand dollar.

The European Central Bank decision follows at 10.15pm AEST, with markets assigning roughly a 15 percent chance of a rate hike.

The Australian dollar has already retreated from recent strength against the euro, with AUD/EUR slipping from 18‑month highs, suggesting traders are increasingly cautious ahead of the decision.

Aussie, kiwi slip from highs

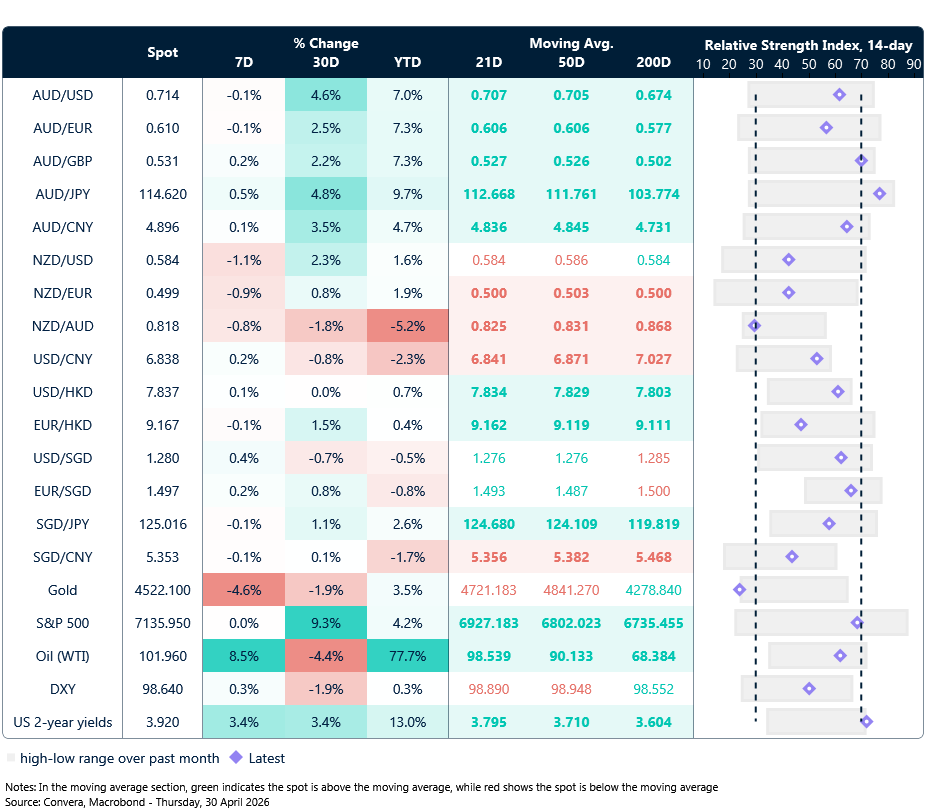

Table: seven-day rolling currency trends and trading ranges

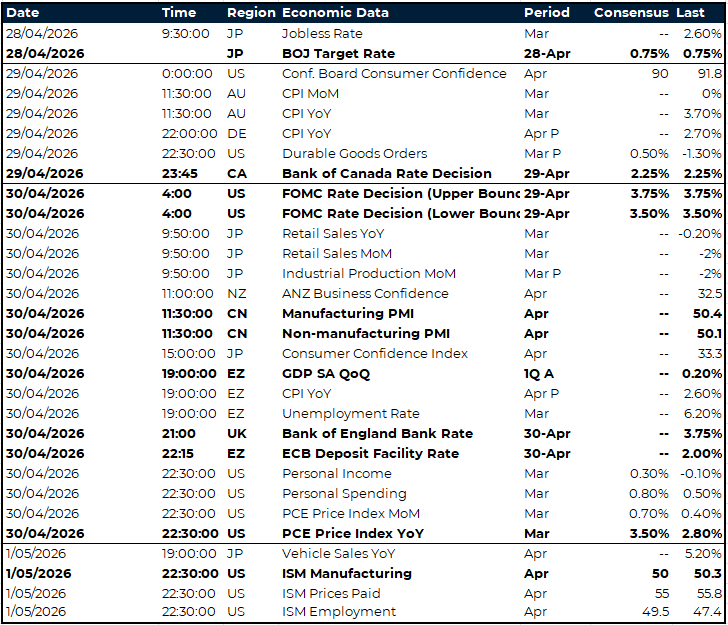

Key global risk events

Calendar: 27 April – 1 May

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.