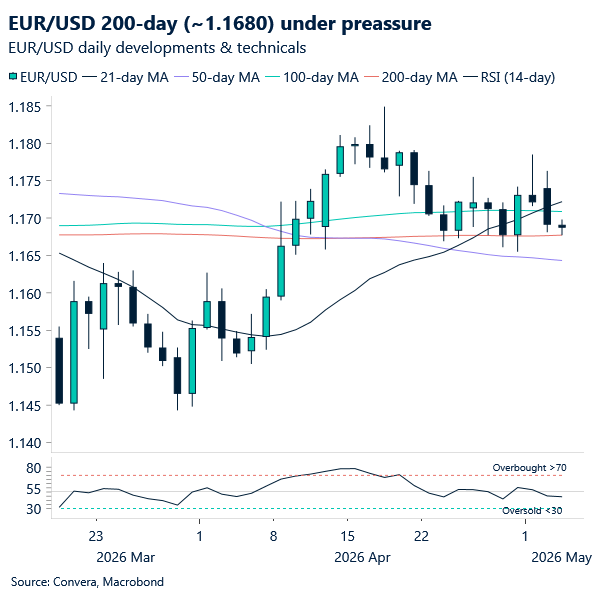

EUR: Escalation flare‑up, downside bias builds

The fragile ceasefire between the US and Iran came under renewed strain yesterday as the two sides exchanged fire in the Persian Gulf, in what appeared to be the most violent bout of re‑escalation since the truce was announced roughly a month ago. Just a day after President Trump unveiled “Project Freedom” to help escort neutral vessels out of the Gulf (see more below), US forces repelled attacks from Iranian drones, missiles, and armed small boats while facilitating the passage of two US-flagged vessels through the Strait of Hormuz. Adding to tensions, the UAE reported intercepting Iranian missiles targeting a state‑owned oil tanker and critical energy infrastructure.

The flare‑up triggered March‑like market moves, though these were more muted by the London open today, with oil prices easing somewhat through the Asian session. The euro weakened around 0.4% against the dollar yesterday, while gaining against G10 and CEE high‑beta currencies. We remain alert to this escalation episode as we assess whether it marks the start of a more durable phase of tension. Until then, markets remain in cautious mode, as there have been too many de‑escalation signals from both sides to abandon the de‑escalation narrative altogether just yet. Nonetheless, EUR/USD’s 1.1680–1.1750 trading range has developed a clearer downside bias, with euro sellers awaiting further signs of re‑escalation to justify a downside break.

USD: Oil risk, Yen intervention, and April’s risk rally

Brent and WTI have faded early dips and bounced to start the week, as traders remain unconvinced that an escort‑and‑coordination framework proposed by President Trump can quickly restore normal flows through the Strait of Hormuz. President Trump’s “Project Freedom” aims to guide neutral ships out of the Gulf, with US Central Command describing support that includes guided‑missile destroyers, aircraft, unmanned platforms, and roughly 15,000 service members. Still, with mine risk, attack risk, and war‑risk insurance constraints lingering, the route remains difficult to “normalize” quickly. Should Brent climb back above the $110 area, it could trigger again some nervousness across markets.

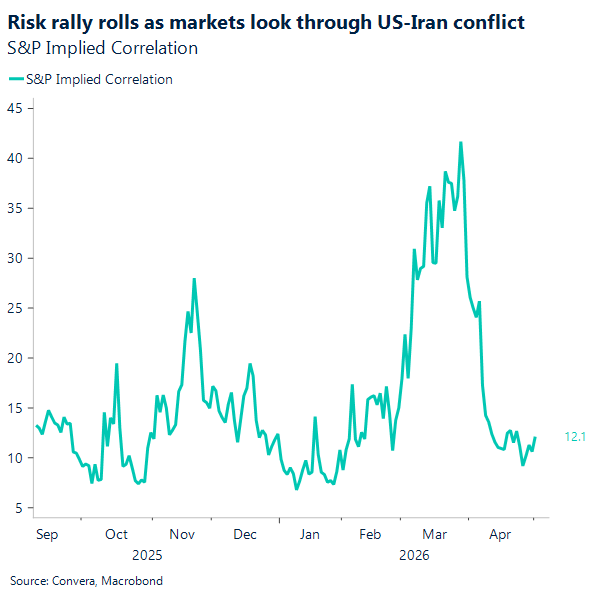

At the same time, equities have been in a world of their own, capping a remarkable April. The month delivered a powerful risk rally, with the S&P 500 up about 10.4% to a record 7,209, the Nasdaq up about 15.3%, and the Dow up about 7.1%. Investors largely treated the energy shock as noisy and temporary, and they were willing to pay up for growth and earnings visibility even while the oil tape stayed volatile. That “markets moved on” vibe has shown up in correlation, too. The Implied Correlation Index has fallen sharply from its late‑March spike (peak near 41.68 on 03/27/26) to about 12.13 recently, which fits with a market that’s no longer pricing a single, macro‑driven liquidation. As I mentioned here, “It often feels like the stock market operates in an alternate universe… It’s less an alternate universe than an alternate timeline.” Markets are looking through the headline risk, have priced in the war impact, and don’t see the conflict surviving beyond spring.

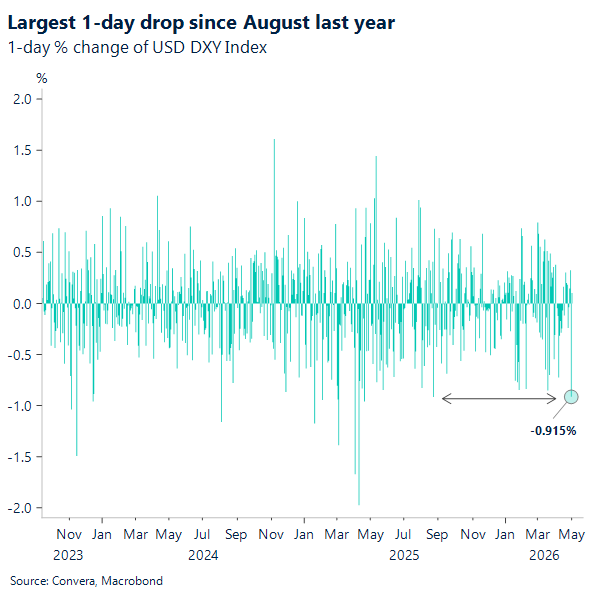

Where markets have not looked through the noise is the US dollar, because Japan’s intervention forced immediate repricing. On April 30, the Bank of Japan (BoJ) reportedly intervened by buying yen and selling dollars, sending the yen up as much as ~3% and pushing USD/JPY down toward ~156.7, with the dollar marked for its biggest one‑day drop since August last year. By Friday, the intervention still mattered because it reset the near‑term reaction function: traders had to price a higher chance of follow‑through if depreciation pressure returned, which can cap USD/JPY rallies even when oil headlines stay loud. While US economic data remains resilient and Powell signals a policy drift toward a “more neutral place”, the seismic shock of the Yen’s intervention-led surge has superseded energy concerns momentarily, and weighed more heavily on the dollar, casting a more significant shadow over short-term dollar sentiment than the ongoing volatility in the crude markets. However, the lingering uncertainty around the new military operation, could see the Dollar paring back some of its late month losses.

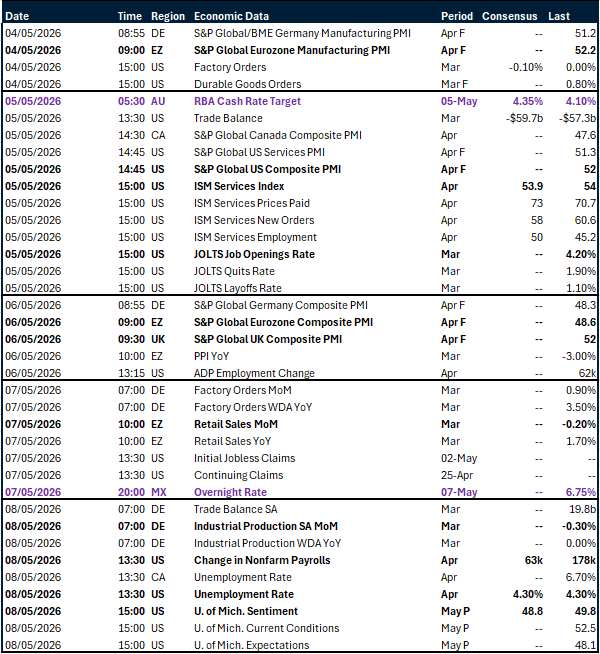

This week markets will be attentive to US JOLTS job openings (Tue), which provide key insights into global policy shifts and labor demand. These events lead directly to the private sector ADP employment change and the US Treasury’s quarterly refunding announcement (Wed) as the heavy earnings season continues to ramp up. Political and regional highlights follow with the high-stakes UK local elections and rate decisions from the Riksbank, Norges Bank and Banxico (Thu). On the same day, investors will monitor German factory orders and Euro-area retail sales for signs of a broader European recovery. The week reaches its peak with the highly anticipated US nonfarm payrolls and Canada’s employment report (Fri), serving as the ultimate health check for the North American economy.

GBP: Upside stalls as local elections loom

Following the long UK weekend, sterling has started the week on the back foot, pressured by a renewed escalation in Middle East tensions that has capped risk appetite and driven another sharp leg higher in oil prices. Against this backdrop, the risk‑ and energy‑sensitive pound has underperformed most major peers, with GBP/USD slipping back toward 1.35 after once again failing to hold a break above the 1.36 resistance zone highlighted in recent sessions. At the same time, the approach of UK local elections adds a domestic layer of uncertainty, keeping sterling vulnerable to downside shocks.

That said, the broader April recovery remains intact for now. Cable’s pullback looks corrective rather than trend‑breaking, with price still holding above key daily moving averages, keeping upside risks alive as long as support in the 1.34–1.35 region holds. The problem is, the balance of risks is increasingly shifting toward rates and domestic vulnerability.

Longer‑dated gilt yields have climbed sharply, with UK 30‑year yields up around 65bp since the Iran war began, nearing levels that have historically worked against sterling rather than supported it. At the front end, two‑year yields are nearly 90bp higher, but the relationship with GBP/USD has turned adverse, with the 20‑day correlation falling to its weakest since October. This suggests markets are beginning to worry that tighter financial conditions, potentially compounded by post‑election political uncertainty, could undermine UK growth, and therefore higher yields won’t necessarily support sterling like they ought to.

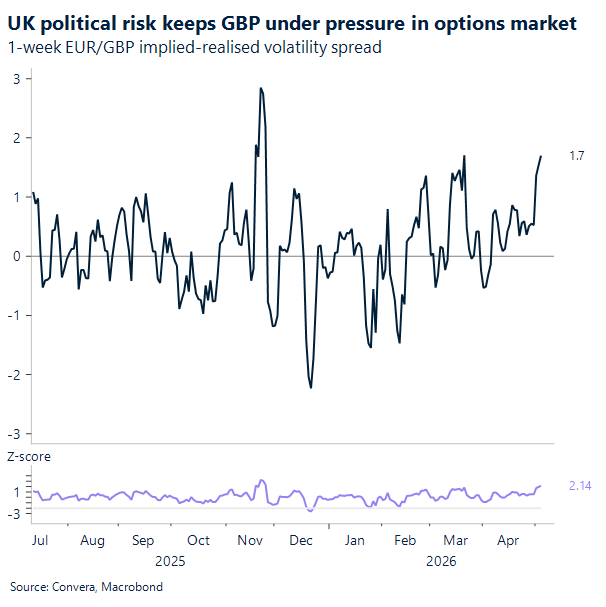

Options markets echo this caution, with implied volatility spiking. GBP/USD reflects a heavier mix of geopolitical and monetary‑policy risk, but political uncertainty linked to the upcoming local elections — and renewed scrutiny of Prime Minister Starmer’s position — is being expressed more directly via EUR/GBP, where one‑week implied volatility is at its richest since November.

In short, sterling remains resilient but increasingly constrained: upside is technically intact, yet higher oil prices, stretched yields, and looming political risk are raising the bar for further gains.

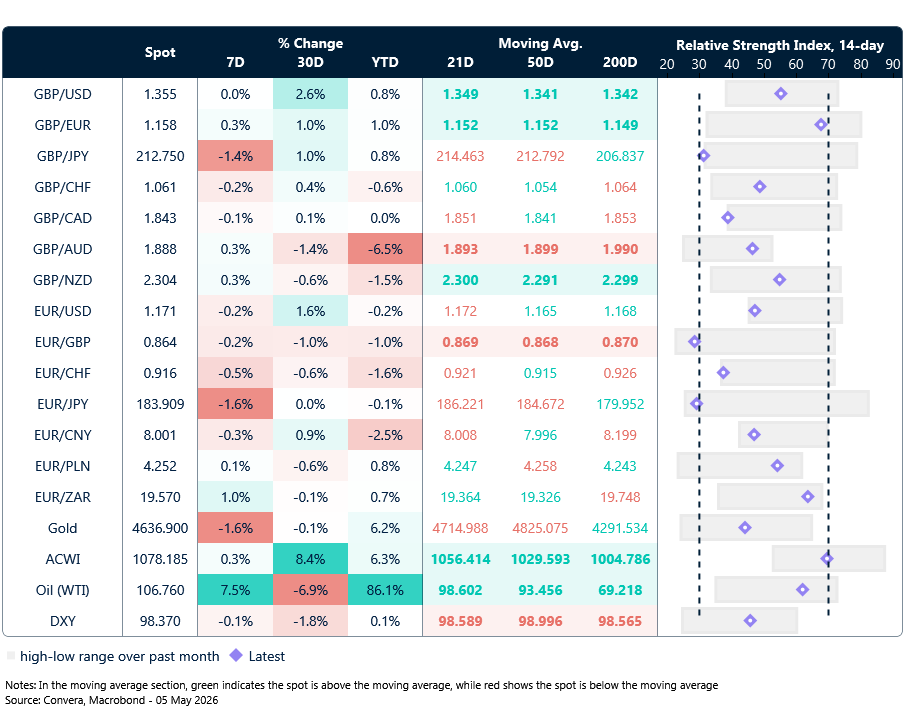

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: May 4-8

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.