Revisiting short-term downside risks

As the calendar edges toward late July, markets appear complacent despite a storm of potential macro and policy disruptions coming month-end. For the U.S. dollar, this period carries heightened vulnerability as investors appear to underestimate the scope of event risks. This echoes last year’s volatility episode, with nearly identical timing and a similar buildup of pressure points. The combination of major economic data releases, policy decisions, and geopolitical developments creates a perfect environment for abrupt sentiment shifts, and the dollar stands right in the crossfire.

Central among the threats is the looming tariff shock, with significant hikes proposed against major partners like the EU, Canada, and Japan. Markets are currently assigning low odds to these measures materializing, yet their potential implementation would likely trigger a wave of risk-off flows, placing downward pressure on the dollar. Adding fuel to the fire is the possibility of retaliatory action, specially from the EU and Canada, as trade partners have already signaled readiness to respond. Such an escalation would not only rattle trade dynamics but also amplify investor anxiety at a time when sentiment is already fragile.

Compounding these geopolitical risks are domestic fiscal and macroeconomic challenges. The 30-year Treasury yield is pressing toward 5%, reigniting concerns over fiscal sustainability following the approval of the OBBB. Friedman’s “helicopter money” concept hangs in the air, as the tax overhaul threatens to unleash another round of debt-fueled stimulus reminiscent of the post-COVID boom. Meanwhile, the Fed faces mounting political pressure to ease rates ahead of its July 30 decision. The Fed will likely hold steady, backlash could grow, and even when markets have grown more tolerant of Trump’s fire-the-chair rhetoric, the noise isn’t likely to do the dollar any favors. Additionally, the upcoming Quarterly Refunding Announcement (July 28) carries some influence, as it brings echoes of last year’s Treasury selloff.

Finally, the ‘summer lull’ and thin liquidity leaves markets more susceptible to sharp and disorderly moves. A disappointing jobs report on August 1 could serve as the spark.

The clustering of event risks and potential narrative shifts pose the biggest Q3 test for the dollar and broader markets this month-end. While the “soft landing” remains the base case, a sudden pivot to a “hard landing”, though unlikely given the latest macro data (strong retail sales, falling jobless claims), remains key macro downside risks.

For now, with no news from the Fed next week and no major news expected from the European Central Bank meeting on Thursday, market attention will turn to PMI data and a blockbuster lineup of Q2 earnings, including Google, Tesla, Coca-Cola, and over 500 other companies, where investors will be watching closely for commentary on how they have navigated the lingering uncertainty of global trade tensions and tariff pressures.

Dollar narrative keeps euro on the defensive

Following a fleeting uptick driven by speculation around the Fed Chair’s potential departure earlier in the week, EUR/USD has settled comfortably in the low $1.16s. Upside surprises in US data just keep rolling in, leading to the EZ-US economic surprise differential rolling over. Resilient US data has also led to a reduction in Fed easing bets this year, leading to higher US yields and a stronger dollar of late, all of which have dragged EUR/USD 2.3% from its recent peak.

At present, euro-specific developments are having limited influence on the currency pair. While political tensions in France could resurface later this year and introduce volatility, they’ve yet to leave a meaningful mark on FX markets. Broader EU dynamics are similarly subdued. The European Commission’s ambitious proposal to expand the EU budget by €2 trillion has already met resistance from Germany, setting the stage for prolonged negotiations. Commission President Ursula von der Leyen aims to secure unanimous approval by 2027, but progress is likely to be slow and contentious.

Though the long-term implications for euro valuation are significant — particularly if fiscal integration deepens — they remain distant. For now, the euro continues to grapple with structural headwinds, including persistently weak productivity growth relative to the US, which has kept medium-term EUR/USD fair value constrained over the past decade.

Meanwhile, in the near term, the outlook for EUR/USD remains largely bound to incoming US data. The timing of a final European Central Bank cut is less relevant for FX, given the disconnect from short-term rates. With limited eurozone catalysts and Fed policy in flux, we see downside risks outweighing upside potential. A drift toward $1.15 appears more plausible than a rally to $1.17 in the very short term, especially if US inflation surprises to the upside or Fed rhetoric turns more hawkish.

Sterling rises on thin hawkish air

Some pressure eased off the Bank of England (BoE) yesterday, as May’s payroll figure was upwardly revised from a shocking –109k to –25k. While the data still points to a soft labour market, combined with persistently strong wage growth, the revision helped alleviate some concerns about more imminent dovish action, allowing GBP/EUR to gain 0.4% in yesterday’s session.

Despite this, the pair remains roughly 2.5% lower compared to May’s peak of €1.1966, with long-term (200- and 50-day) and short-term (21-day) moving averages continuing to point downward.

This week’s uptick in the pair has been largely driven by a better-shielded pound amid tariff-related noise, which has instead weighed on the more exposed euro. Additionally, with two full 25-basis-point cuts already largely priced in, softness in the data doesn’t drag the pound lower as much as signs of improvement do—sparking some hawkish re-pricing that, in turn, supports sterling.

But as additional trade deals materialize, particularly involving the EUR, the current 0.3% week-to-date GBP/EUR performance may struggle to hold its gains.

Also, with no major data releases expected for the rest of the week—and the overall tone still leaning dovish—those “full tanks” of BoE rate cut expectations won’t get a chance to burn much more fuel. As a result, GBP/EUR is likely to stay weighed down below the resistance level at €1.1600.

Small business sentiment recovers in Canada

Small business optimism is showing modest signs of improvement, according to the CFIB Business Barometer Index. Forward-looking sentiment for the next 12 months rose three points from June to 50.9 in July, while short-term expectations held steady at 49.3, just above the prior reading. Despite the uptick, sentiment sits at a neutral point, as half anticipate improvement and half foresee decline. Insufficient demand continues to be the primary constraint on growth. Meanwhile, the average price increase planned over the next year eased slightly, falling to 2.7 percent from 2.9 percent in June.

After climbing above its 20- and 40-day moving averages, the USD/CAD tested resistance at the 60-day moving average, closing the week near 1.375 without a clear breakout. The pair remains under upward pressure, driven by resurgence in dollar demand as short USD positions unwind. On the weekly chart, momentum is evident with two straight weeks of gains, rising from 1.359 to a peak of 1.377, just shy of firm resistance at the 100-week moving average of 1.378. Looking ahead, Thursday’s retail sales data for May stands out as the key macro release, likely offering additional insight into the broader economic landscape.

Risk on – equities hit fresh record highs

Table: 7-day currency trends and trading ranges

Key global risk events

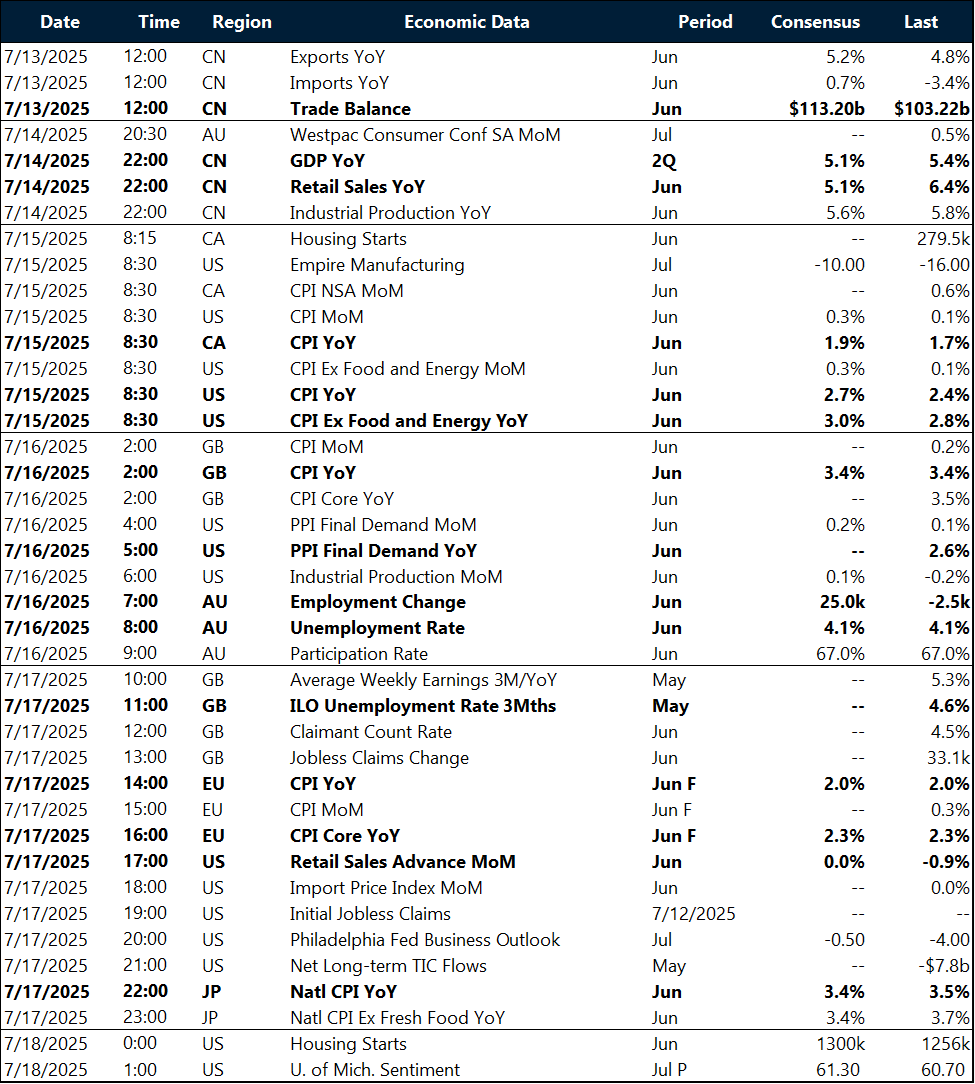

Calendar: July 14-18

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.