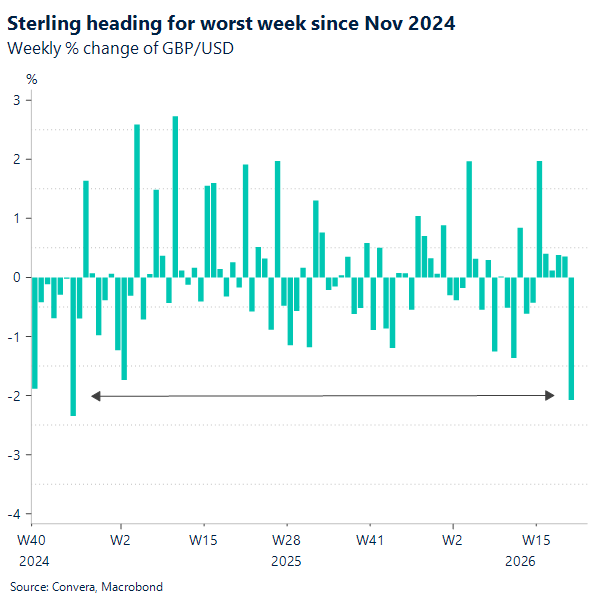

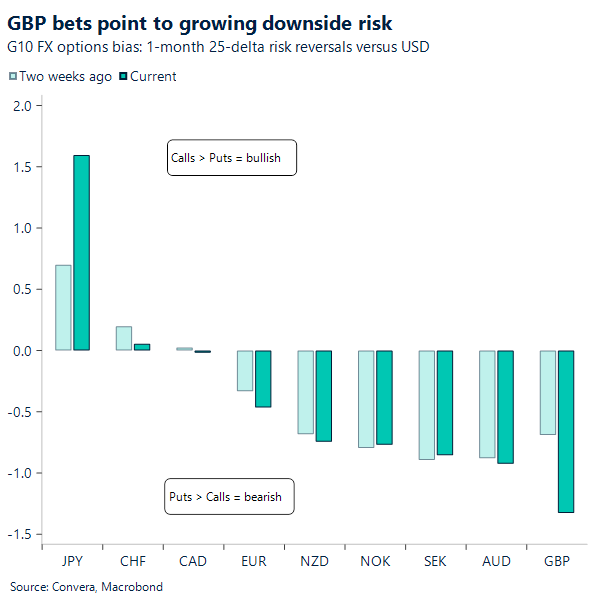

GBP: Pound tumbles on political uncertainty

Sterling is under broad pressure this week, weakening against all major peers and down over 1% versus the dollar, putting it on track for its largest weekly loss in over 18 months. Having traded as high as 1.3653 last week, GBP/USD has since retreated into the low‑1.33s, erasing four weeks of gains and breaking below all key daily moving averages – signalling a clear deterioration in near‑term momentum. A similar dynamic is evident in GBP/EUR, where momentum has also bearish after slipping below 1.15 and key support levels this week.

Part of the move reflects a resurgent US dollar, driven by stronger‑than‑expected US data and rising Treasury yields. However, sterling is also contending with a distinct domestic headwind: rising political uncertainty and the increasing risk of a UK leadership contest.

UK politics has entered a more turbulent phase, with growing pressure on Prime Minister Starmer following calls from within the Labour Party for his resignation. The situation escalated midweek as Health Secretary Wes Streeting resigned and urged the prime minister to outline a departure timetable. While Streeting did not formally launch a leadership challenge, the sequence of events has intensified speculation around succession.

More significantly for markets, Andy Burnham has emerged as a potential contender, following moves to facilitate his return to parliament. With a relatively strong public approval profile and support across parts of the Labour base, Burnham’s potential candidacy raises the likelihood of a shift toward a more expansive fiscal stance — a development that could unsettle gilt markets and weigh on sterling.

Taken together, the backdrop points to rising political risk premia for UK assets. However, for a more sustained repricing, markets will need greater clarity on whether a formal leadership contest materialises and, crucially, what policy direction any successor might pursue.

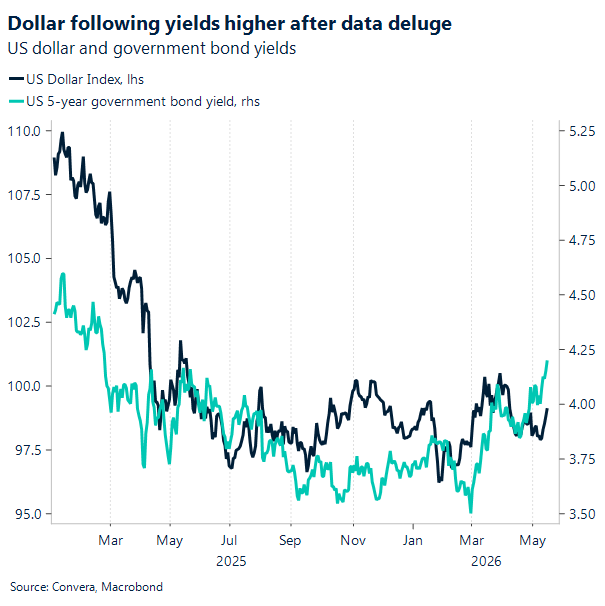

USD: Rising yields underpin dollar demand

The US dollar is set for its strongest weekly performance in nine, with the DXY up around 1.2% week-to-date. The primary support remains geopolitical: the lack of progress in the Gulf has kept energy prices elevated, reinforcing the dollar’s relative position.

Beyond the immediate geopolitical backdrop, the medium-term case for a firmer dollar remains intact. The energy shock continues to weigh more heavily on Europe and large parts of Asia, while Canada remains constrained by lingering trade pressures. These dynamics limit the scope for tighter policy elsewhere, while the US economy continues to demonstrate resilience. That divergence is increasingly visible in economic surprise indices, which have begun to separate more clearly in favour of the US.

Recent data reinforce that narrative. Retail sales rose 0.5% m/m in April, suggesting that higher fuel costs have yet to materially dent consumer spending. Given the central role of consumption in the US growth model, this points to a degree of insulation from the energy shock. Labour market conditions remain broadly firm, with jobless claims still low in absolute terms, providing further support to household demand. At the same time, price pressures remain elevated. Both import and export prices surprised to the upside, adding to a run of firm inflation data, including this week’s CPI and PPI releases.

Taken together, the data flow is strengthening the market’s more hawkish interpretation of the Fed outlook, helping to underpin the dollar via the rates channel. Overall, the USD remains supported by a combination of geopolitics, relative growth resilience, and firmer inflation dynamics, even as near-term upside may be tempered by shifts in global risk sentiment.

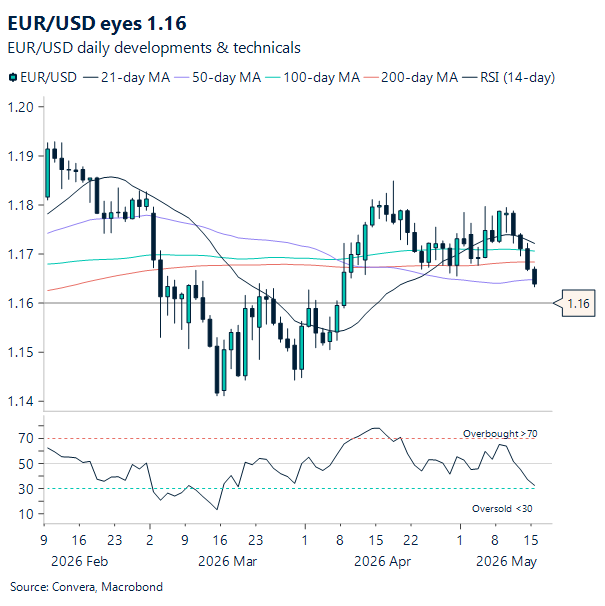

EUR: A selfish dollar weighs on EUR/USD

EUR/USD closed lower yesterday for a third consecutive session and softened further during the Asian session today. The Sino-American summit in Beijing has worked selfishly in favour of the US dollar and the Chinese yuan, with the euro weakening against both currencies. The common currency has lacked supportive headlines from the summit regarding the Iran-US conflict, to which it remains highly sensitive, while the dollar has advanced uncharacteristically amid a pro-risk backdrop. This has been fuelled by a cordial Beijing summit, which has added to an already optimistic corporate backdrop underpinned by solid earnings momentum.

Risk sentiment appears to have turned quickly, with the summit uplift fading as conflict worries loom large. Asian equities traded lower today, while oil prices have come under upward pressure, hovering near $107 per barrel. Beyond broader risk sentiment, the dollar’s advance yesterday – and its bid tone this morning (BST) – may have, therefore, been more idiosyncratic in nature. The conciliatory tone on trade, with Trump and Xi reaffirming their commitment to stability, may have been mildly dollar-supportive. Notably, in 2025 the greenback proved particularly vulnerable on the downside to renewed US-China trade tensions. Finally, yesterday’s solid US retail sales print for April added a data-driven tailwind, reinforcing the dollar’s bullish run.

EUR/USD has breached the 1.1650-1.1660 area, which had gathered buying interest throughout April. This break suggests euro sellers may be emboldened amid the ongoing geopolitical impasse and a solid US macro backdrop, alongside an ECB perceived as less credible on the hawkish side. The common currency’s lifeline now hinges on a post-summit refocus on the conflict and on whether the US and Iran continue to face paralysis on the negotiation front.

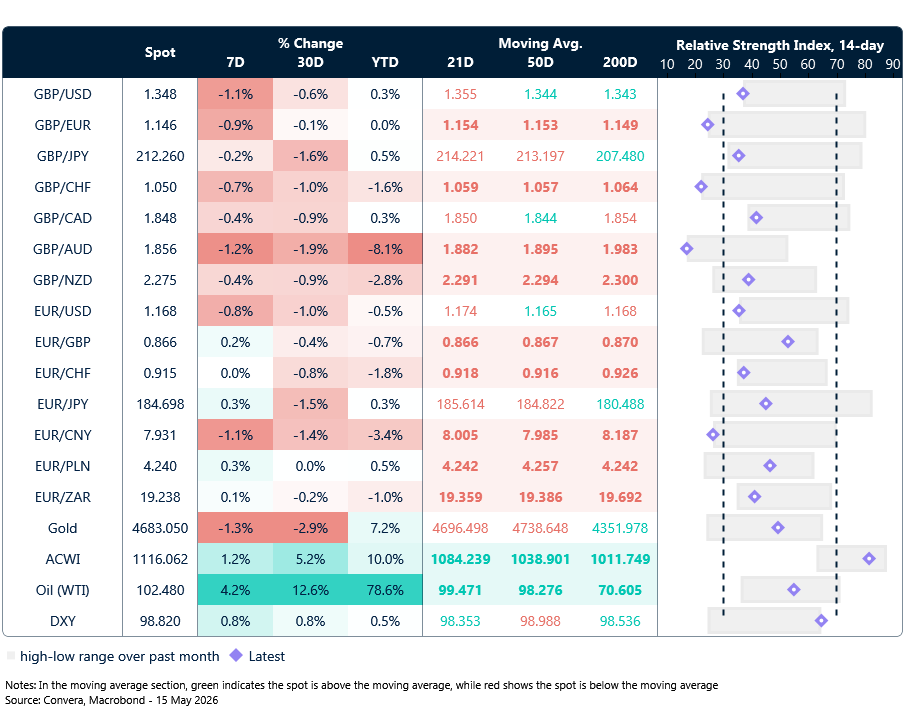

Market snapshot

Table: Currency trends, trading ranges & technical indicators

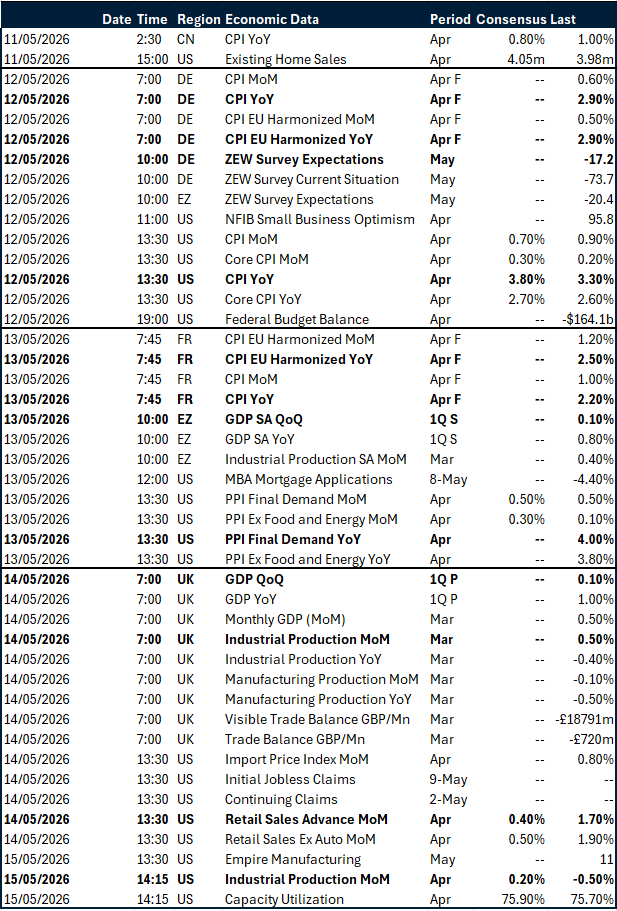

Key global risk events

Calendar: May 11-15

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.