USD: Xi–Trump meet as conflict looms large

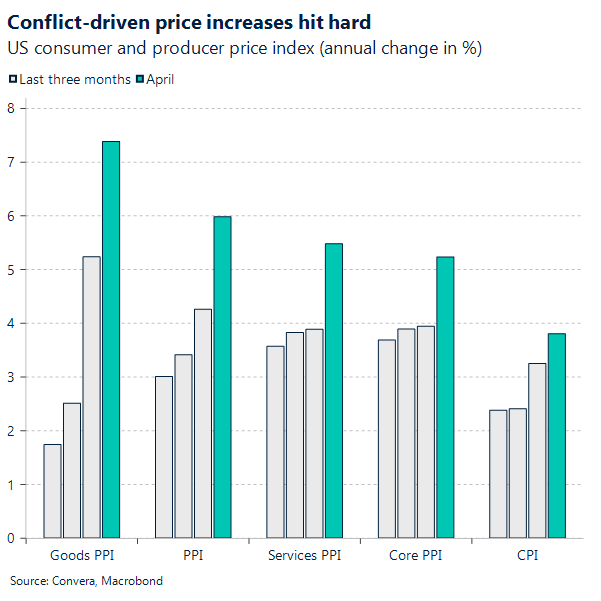

Yesterday saw the release of a very hot US PPI report for April. Adding to Tuesday’s above-expectation CPI print, and last week’s solid labour market report, recent data momentum has strengthened the market’s hawkish read on the Fed outlook this year, and with it, supported a firmer dollar. US wholesale inflation accelerated in April to the fastest pace since 2022, driven by war-related increases. The index rose 6% year-on-year and 1.4% month-on-month. In response, the yield on the 10-year Treasury note moved close to its highest level since July, with markets now pricing in close no policy moves from the Fed for the remainder of the year.

While conflict-related headlines may continue to carry the strongest market-moving power, as the conflict enters its third month its influence may increasingly feed through the incoming data and, in turn, into market perceptions of central bank outlooks. The US is an interesting case in point: the recent streak of hawkish-leaning data releases, amid a highly uncertain geopolitical backdrop, may be dampening market jitters around the appointment of Kevin Warsh as the new Fed Chair to replace Jerome Powell, and concerns that he may lean politically toward Trump’s preference for lower rates. Warsh’s chairmanship was just confirmed by the Senate yesterday. Overall, with risk sentiment subdued but not deteriorating, and US-centric risk premia somewhat anesthetised, the backdrop points to mild support for the dollar. An escalation in the geopolitical environment would, however, inject a more forceful bullish impulse into the greenback.

Meanwhile, today President Trump and his delegation are meeting with their Chinese counterparts in Beijing – the first visit by a US president in nine years. Many issues are being addressed, most notably bilateral trade relations and whether the two sides can move beyond the truce agreed last year. At that time, China was able to leverage its rare earth reserves to pressure Trump to roll back threatened tariffs. However, markets are likely to pay closer attention to the conflict topic. Iran is one of China’s most important trading partners, with crude oil a key import from the Islamic Republic. Whether the conflict, and the associated economic pressure on China, leads Xi to further exert that leverage remains to be seen. Monitoring Trump’s posture toward the conflict after the summit will therefore be key.

For the week, we see the DXY continuing to hover around its 200-day moving average near 98.50, as markets wait to assess Trump’s post-summit stance on the conflict before committing more directionally.

EUR: Drifting lower as sentiment wavers

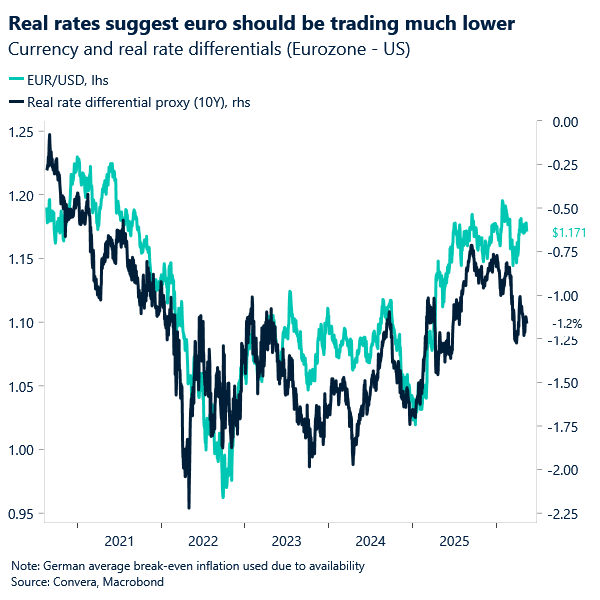

The euro continues to edge lower against the dollar, with EUR/USD hovering around its 100‑day moving average just above 1.17, as risk sentiment softens once again. The primary driver remains geopolitics. The rejection of competing US and Iran proposals earlier this week has dented confidence in a near‑term resolution, reinforcing the pattern seen throughout the conflict: EUR/USD trading closely alongside swings in global risk appetite.

In the near term, this leaves the euro vulnerable. Absent tangible progress toward reopening the Strait of Hormuz, deteriorating risk sentiment is likely to remain the dominant bearish impulse. However, the underlying macro backdrop is also becoming more challenging. The longer energy disruption persists, the greater the strain on the eurozone’s energy‑intensive economy, raising the risk that the ECB’s hawkish pivot becomes less credible relative to the Fed.

This divergence is increasingly visible in the data. While Germany’s ZEW expectations index improved modestly in May, it remains firmly negative, highlighting ongoing uncertainty around the growth outlook. Hard data paints a softer picture: Eurozone GDP expanded just 0.1% in Q1, marking the weakest growth since mid‑2025, while rising unemployment in both France and Germany points to a gradual deterioration in labour market conditions.

By contrast, the US economy continues to show greater resilience, particularly in employment. This divergence challenges current market pricing, which still leans toward ECB tightening alongside a relatively benign Fed outlook. It raises the risk of yield differentials shifting back in the dollar’s favour, adding another layer of pressure on EUR/USD.

For now, the euro remains technically supported, but both sentiment and fundamentals are beginning to lean against it, suggesting downside risks are building if the geopolitical backdrop fails to improve.

GBP: Real challenge or just smoke?

Juicy updates from the UK political saga see Health Secretary Wes Streeting threatening to resign and launch a leadership bid to replace Starmer. Their rivalry is long-standing, with last year’s accusations from Starmer’s camp – claiming Streeting was plotting an overthrow – among the most recent flashpoints. Streeting later denied those claims.

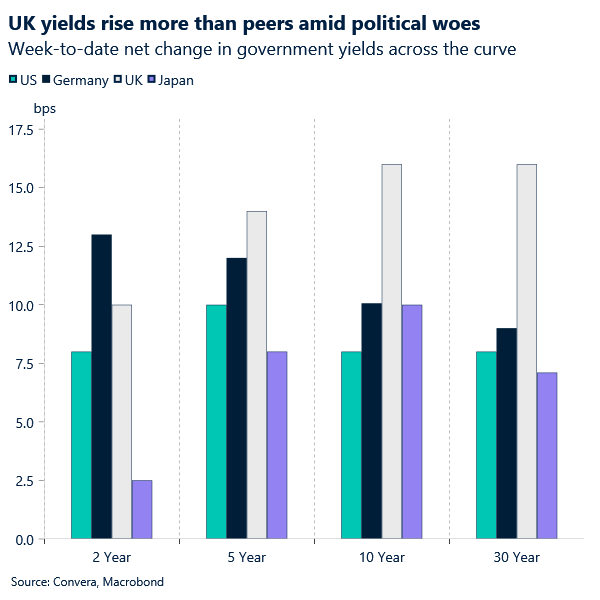

The pound took yesterday’s development in stride, however, suggesting that tuesday’s meaningful sell-off in gilts and sterling may have been partially driven by expectations of a more radical, spend-friendly alternative emerging – such as Andy Burnham. Not only is Streeting’s stance seen as more fiscally disciplined, but he also lacks broad support beyond parts of the Labour party and among UK voters, making him less of an immediate threat to markets. That risk may, however, be re-emerging now thatformer Deputy Prime Minister Angela Rayner, who has just been cleared by HMRC over her tax affairs, would stand as a more left-leaning contender. This is something the pound may be more susceptible to on the downside, with markets beginning to take notice in early London trading as sterling softens slightly across the board.

That said, whether this softness turns into something more durable will depend on whether Streeting formally triggers a challenge in the coming days, which would likely inject additional volatility into sterling, with downside risks building now that Rayner has cleared her path to potentially enter a contest to replace Starmer as well. Absent that, we doubt GBP/EUR has much room to move, with downside likely capped at 1.1520/30, where buying interest has recently built up.

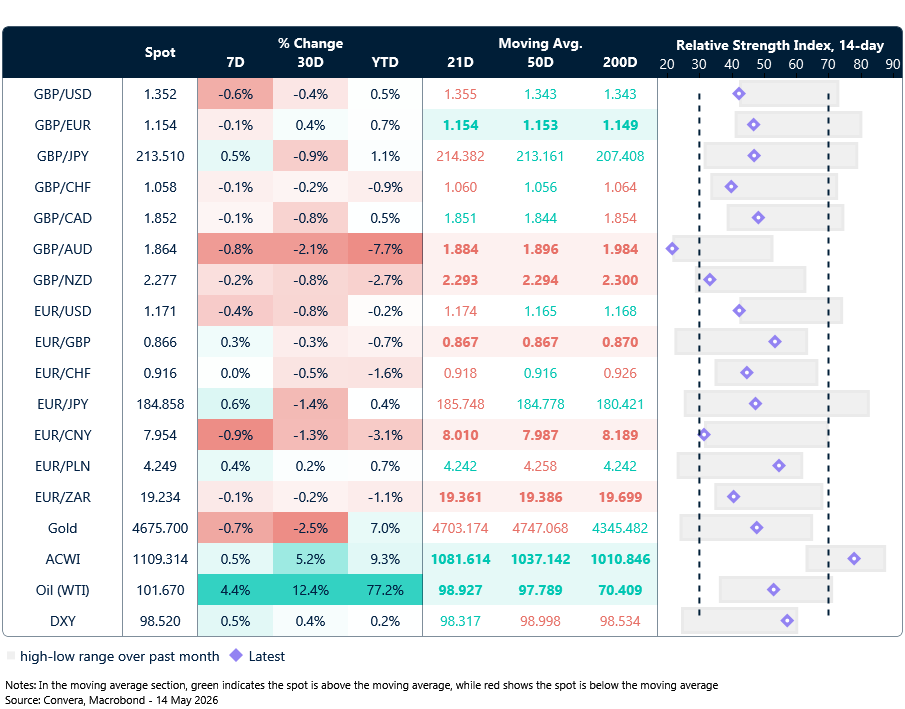

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: May 11-15

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.