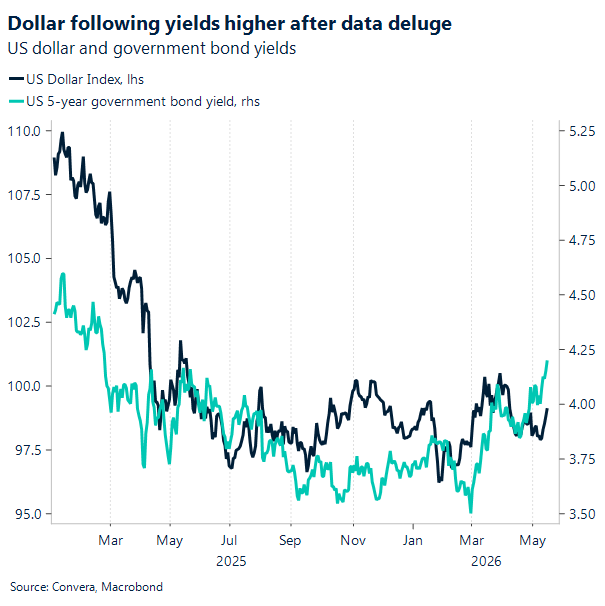

USD: Rising yields underpin US Dollar demand

The US dollar is set for its strongest weekly performance in nine, with the DXY up around 1.2% week-to-date. The primary support remains geopolitical: the lack of progress in the Gulf has kept energy prices elevated, reinforcing the dollar’s relative position.

Beyond the immediate geopolitical backdrop, the medium-term case for a firmer dollar remains intact. The energy shock continues to weigh more heavily on Europe and large parts of Asia, while Canada remains constrained by lingering trade pressures. These dynamics limit the scope for tighter policy elsewhere, while the US economy continues to demonstrate resilience. That divergence is increasingly visible in economic surprise indices, which have begun to separate more clearly in favour of the US.

Recent data reinforce that narrative. Retail sales rose 0.5% m/m in April, suggesting that higher fuel costs have yet to materially dent consumer spending. Given the central role of consumption in the US growth model, this points to a degree of insulation from the energy shock. Labour market conditions remain broadly firm, with jobless claims still low in absolute terms, providing further support to household demand. At the same time, price pressures remain elevated. Both import and export prices surprised to the upside, adding to a run of firm inflation data, including this week’s CPI and PPI releases.

Taken together, the data flow is strengthening the market’s more hawkish interpretation of the Fed outlook, helping to underpin the dollar via the rates channel. Overall, the USD remains supported by a combination of geopolitics, relative growth resilience, and firmer inflation dynamics, even as near-term upside may be tempered by shifts in global risk sentiment.

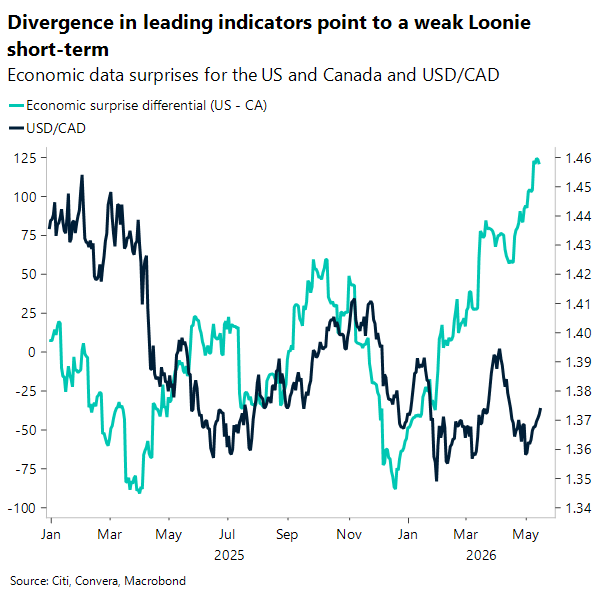

CAD: Four-week high

USD/CAD’s push to a four-week high is really a story of relative momentum. Hotter than expected US inflation has kept the market leaning toward ‘higher for longer’ in the US, while Canada has had little fresh macro this week to push back against last Friday’s softer labour print. That combination widened the near-term rate/yield differential and helped drive a clean reversal from the ~1.355 area to around ~1.373, seven straight up sessions that says positioning and sentiment have turned more cautious on the Bank of Canada outlook.

That said, the two sided risk for the Bank of Canada is still very much alive: softer employment points to patience, but sticky wages and a deliberations summary that didn’t shut the door on further adjustments keep inflation nerves alive. The result is a CAD that, for now, takes its cue mainly from US rates and broad USD strength.

From a technical standpoint, spot is running into a busy inflection zone around 1.3720–1.3730 where the 50‑ and 100‑day moving averages converge, a classic ‘moving‑average magnet’ that can slow follow‑through on the first attempt. The next upside level is clearer: the 200‑day near ~1.381. A break above there would make this look less like a bounce and more like a re‑trend within the well‑worn 1.35–1.39 range; failure to clear it could invite a pullback that tests how much of the move was fundamentals versus positioning.

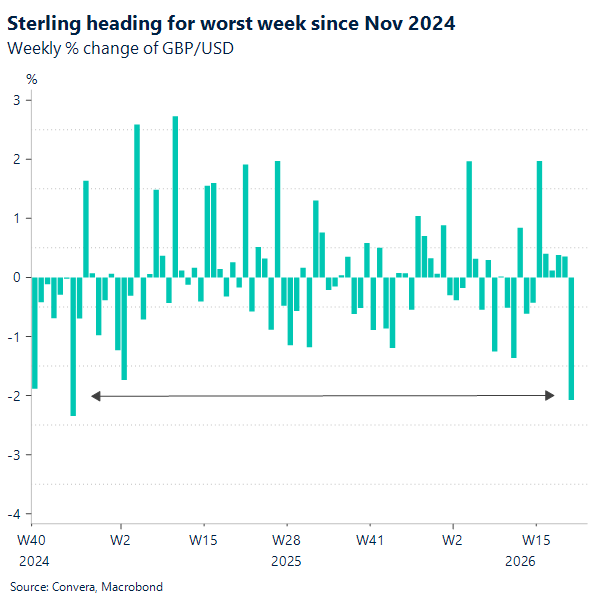

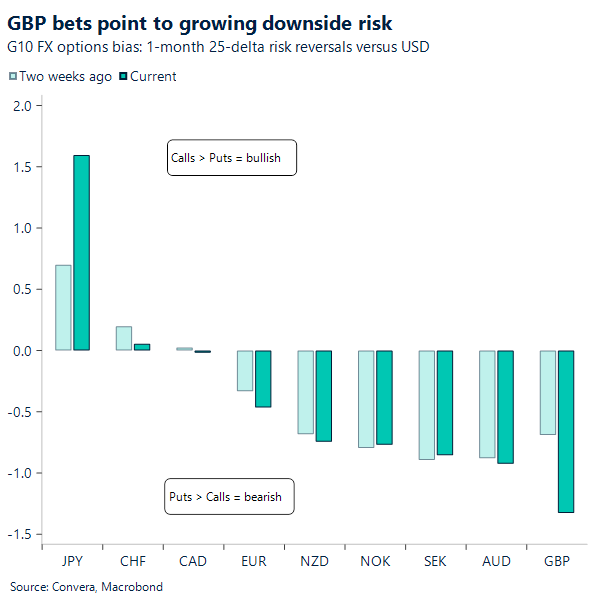

GBP: Pound tumbles on political uncertainty

Sterling is under broad pressure this week, weakening against all major peers and down over 1% versus the dollar, putting it on track for its largest weekly loss in over 18 months. Having traded as high as 1.3653 last week, GBP/USD has since retreated into the low‑1.33s, erasing four weeks of gains and breaking below all key daily moving averages – signalling a clear deterioration in near‑term momentum. A similar dynamic is evident in GBP/EUR, where momentum has also bearish after slipping below 1.15 and key support levels this week.

Part of the move reflects a resurgent US dollar, driven by stronger‑than‑expected US data and rising Treasury yields. However, sterling is also contending with a distinct domestic headwind: rising political uncertainty and the increasing risk of a UK leadership contest.

UK politics has entered a more turbulent phase, with growing pressure on Prime Minister Starmer following calls from within the Labour Party for his resignation. The situation escalated midweek as Health Secretary Wes Streeting resigned and urged the prime minister to outline a departure timetable. While Streeting did not formally launch a leadership challenge, the sequence of events has intensified speculation around succession.

More significantly for markets, Andy Burnham has emerged as a potential contender, following moves to facilitate his return to parliament. With a relatively strong public approval profile and support across parts of the Labour base, Burnham’s potential candidacy raises the likelihood of a shift toward a more expansive fiscal stance — a development that could unsettle gilt markets and weigh on sterling.

Taken together, the backdrop points to rising political risk premia for UK assets. However, for a more sustained repricing, markets will need greater clarity on whether a formal leadership contest materialises and, crucially, what policy direction any successor might pursue.

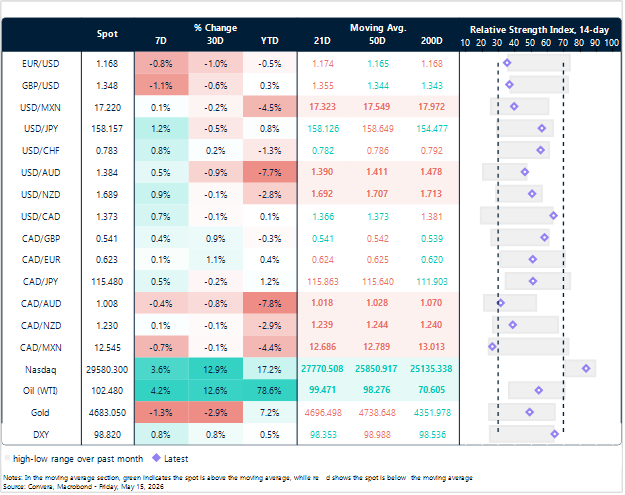

Market snapshot

Table: Currency trends, trading ranges & technical indicators

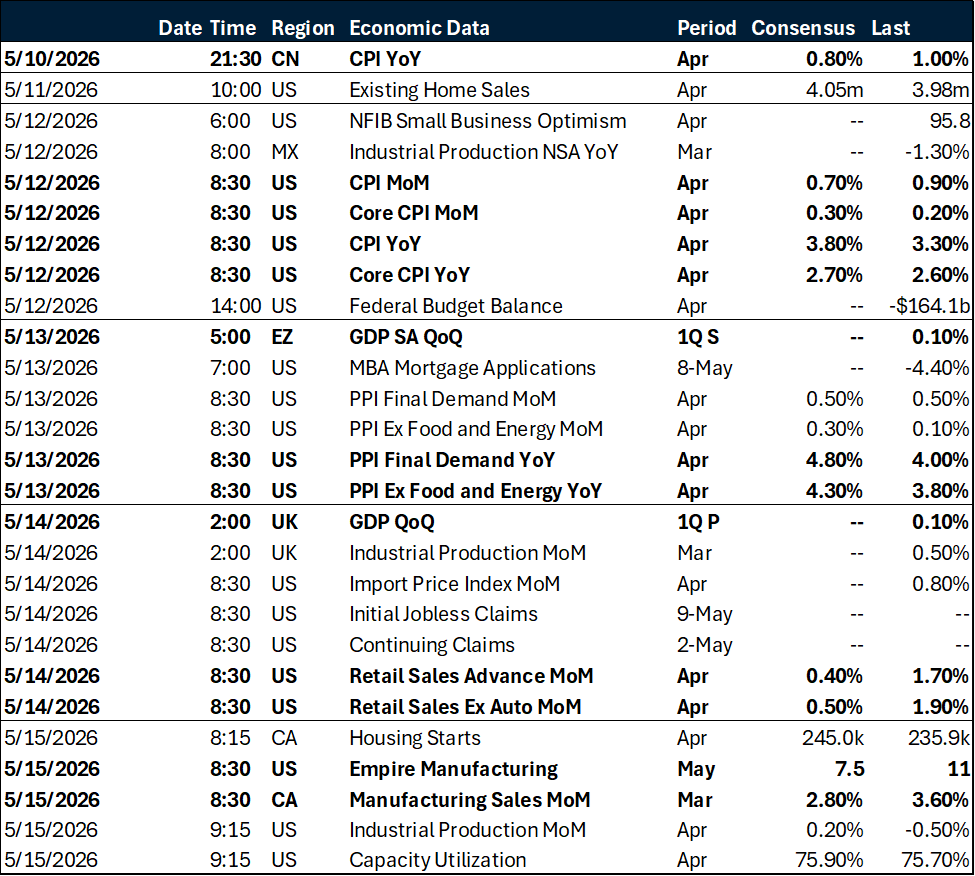

Key global risk events

Calendar: May 11 – 15

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.