USD: Backs off as energy risks persist

Yesterday’s economic data set a mixed but resilient backdrop. February JOLTS job openings eased to 6.88 million, reinforcing a gradual cooling in labor demand that was already underway on the eve of the US‑Israeli attack on Iran. At the same time, consumer confidence surprised to the upside, with the Conference Board index rising to 91.8 in March. The macro tone was stable enough to start the session, but international headlines quickly took control of the narrative.

Geopolitics dominated price action. Reports indicated Iran’s president signaled a willingness to end the war contingent on guarantees against future aggression, while President Trump publicly pressed other countries to take responsibility for securing the Strait of Hormuz. Iran has maintained similar demands throughout the conflict, so little of this is strictly new; the strong market reaction instead underscored how eager investors are for a path to de‑escalation and, arguably, a cleaner quarter‑end.

The S&P 500 jumped 2.65%, with the Nasdaq 100 and S&P 500 notching their best sessions since May 12, 2025. Brent fell about 2.5%, while WTI remained above $100 per barrel, making the equity move larger than what the oil decline alone would imply. The scale of the rally suggests investors are leaning hard into de‑escalation risk, not merely responding to energy beta.

In FX, after five consecutive up sessions and a test of its highest level since May 2025, the greenback slipped roughly 0.7% even as WTI held above $100. That reversal points to an unwind of safe‑haven flows and position‑squaring into quarter‑end, and it is an important barometer of how credibly markets view a potential diplomatic off‑ramp. FX looks like the cleaner tell from here, sustained Dollar softness alongside firm energy would corroborate a risk‑friendly shift, while a Dollar snapback would warn that the de‑escalation trade is over‑extended.

On the ground, however, little has materially changed. Energy is not flowing freely through the Strait of Hormuz, and strikes continue across the region, including a recent attack on a Kuwaiti oil tanker. Yes, markets are forward looking, but they have also showed their predisposition to get way ahead of themselves, trading on hope rather than hard improvements in physical flows. Until shipping normalizes and regional violence meaningfully recedes, the equity move looks ahead of fundamentals.

The next checkpoints are straightforward. First, we’ll stay keeping an eye on hard confirmation of ceasefire guarantees and operational proof in restored shipping, normalized insurance, and lower war‑risk premia. Also, we’ll see whether the roughly 0.7% pullback extends (validating risk‑on) or reverses (flagging vulnerability). Finally, we’ll keep monitoring energy‑risk alignment: can equities remain buoyant if WTI stays above $100 and Strait risk persists?

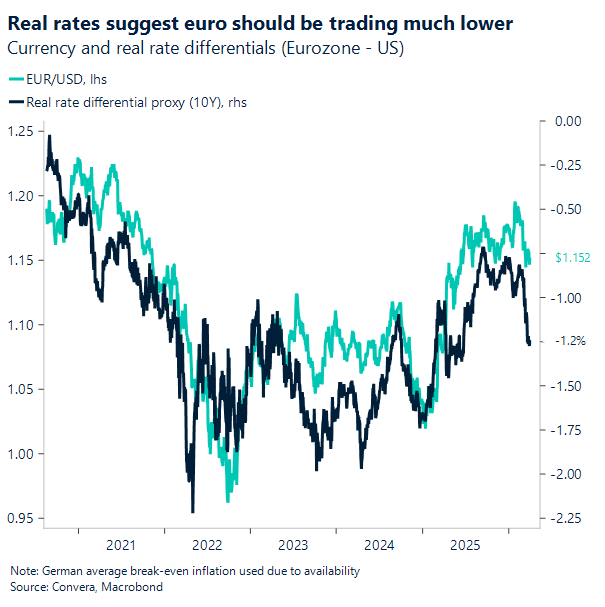

EUR: Real rates are a warning signal

The euro rallied nearly 0.8% against the dollar yesterday, helped by hopes of a potential de‑escalation in Iran and a sharp upside surprise in Eurozone inflation — the steepest monthly jump since 2022. This data backed expectations that the European Central Bank (ECB) will have to raise interest rates, but the euro is at risk if the ECB doesn’t go ahead.

The rise in nominal euro rates has barely kept pace with the surge in inflation expectations, meaning the 10‑year real rate differential has actually moved against EUR/USD. If the ECB opts against a hike in April while inflation expectations stay elevated, that mix turns euro‑negative. In short, persistently high energy prices and an ECB unwilling to tighten leave EUR/USD vulnerable to a move toward the 1.12 area.

EUR/USD closed March between 1.15 and 1.16 after dipping to 1.1411 earlier in the month. But with the pair starting March near 1.18, the monthly drop of more than 2% was its worst since July and extends the drawdown from the 2026 peak to 4%. Despite yesterday’s bounce, EUR/USD remains locked in a short‑term downtrend, with the 50‑week moving average continuing to cap the topside.

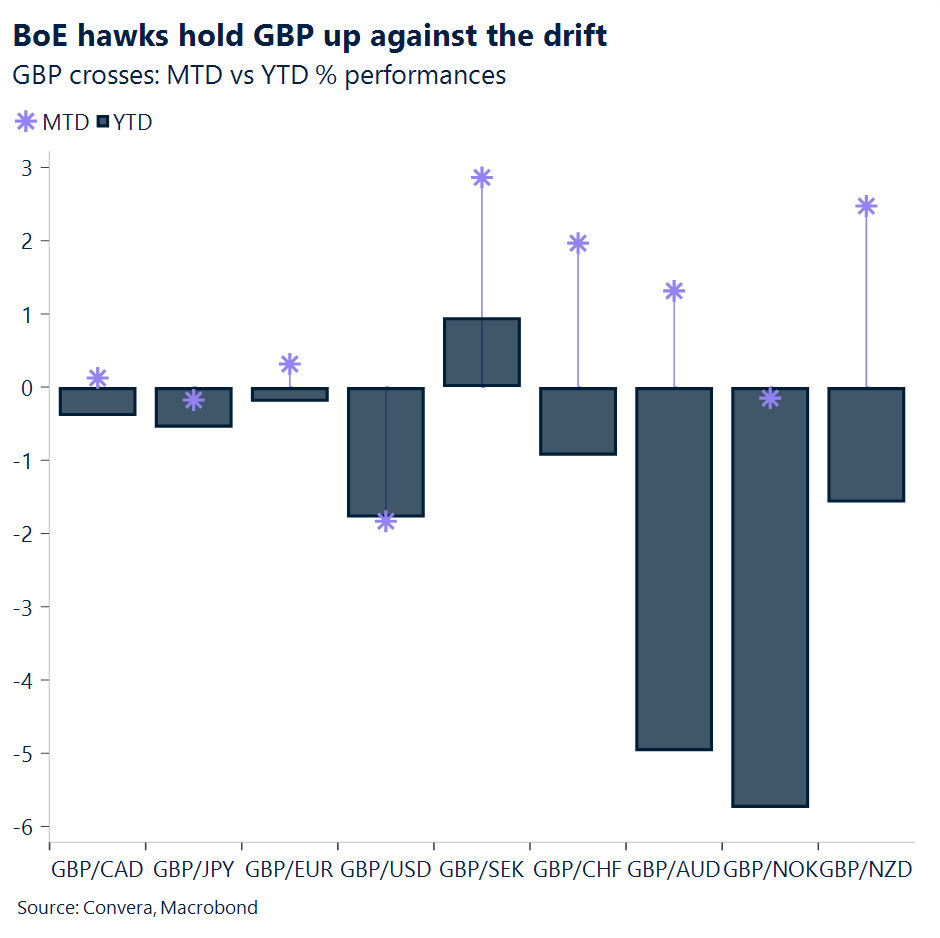

GBP: An uneasy balance

Sterling has fallen by around 2% against the dollar on a year-to-date basis, while holding broadly flat versus the euro. A more dovish shift in BoE expectations in February, driven by clearer signs of easing inflation, combined with political uncertainty around Starmer’s leadership and, more recently, a deterioration in global risk sentiment linked to the ongoing conflict, have weighed on the currency. Even so, losses have been partially pared as March’s aggressive hawkish repricing in the BoE path tied to the conflict has offered some support.

The pound continues to be tossed between erratic, hawkish leaning rates repricing and a risk off backdrop that pulls it lower. Markets remain reluctant to fully reprice longer term growth expectations in a conflict-ridden world, as tentative optimism around a potential resolution, supported in part by President Trump’s recent remarks that negotiations are progressing, keeps risk off from fully deteriorating while still bolstering some of sterling’s yield advantage.

As a result, rate differentials continue to matter at the margin. When hawkish expectations are rebuilt, sterling finds support; when they are unwound, it comes back under pressure. We read sterling’s four consecutive daily declines against the dollar last week, and the continuation into this week despite a more contained rise in oil prices, as driven by the unpricing of some of those hawkish bets (now hovering around two hikes by year-end versus four earlier in the month). For now, the currency sits in that tension: as rate support fades, sterling becomes more exposed to the broader risk backdrop, with an incomplete shift toward growth-driven repricing keeping the push and pull alive.

GBP/USD held above support at 1.32 yesterday, a key level that has acted as a stronghold throughout the post‑ “Liberation Day” (2 April 2025) trading range. Spills below it appear plausible if de‑escalation signals remain unsubstantiated. That said, in the medium term, we expect a firmer re‑establishment of 1.32 as a support guide once the conflict begins to de‑escalate, easing risk off while keeping the BoE on the hawkish side.

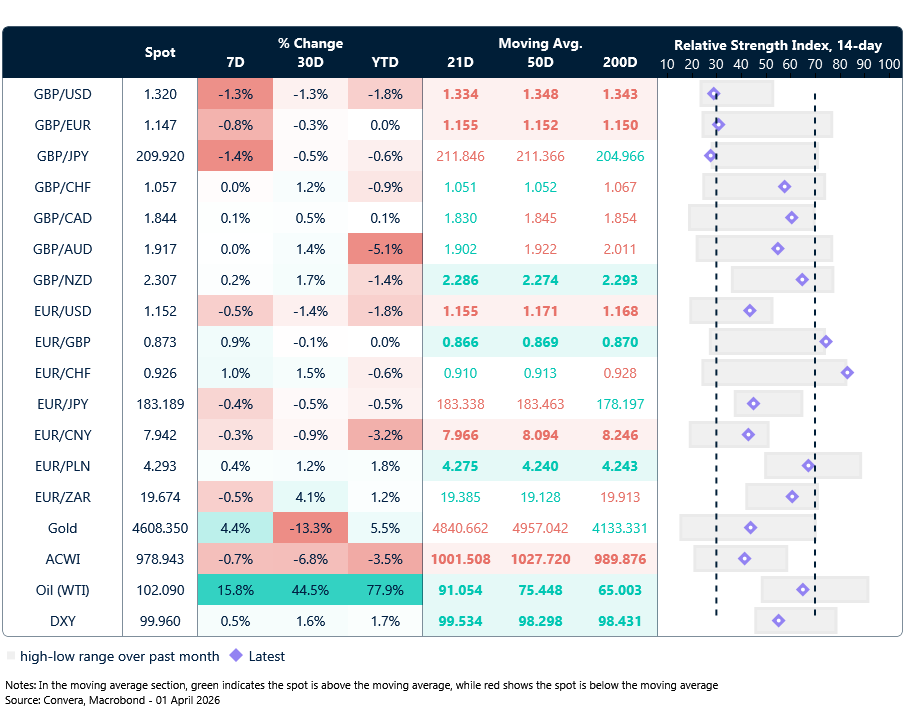

Market snapshot

Table: Currency trends, trading ranges & technical indicators

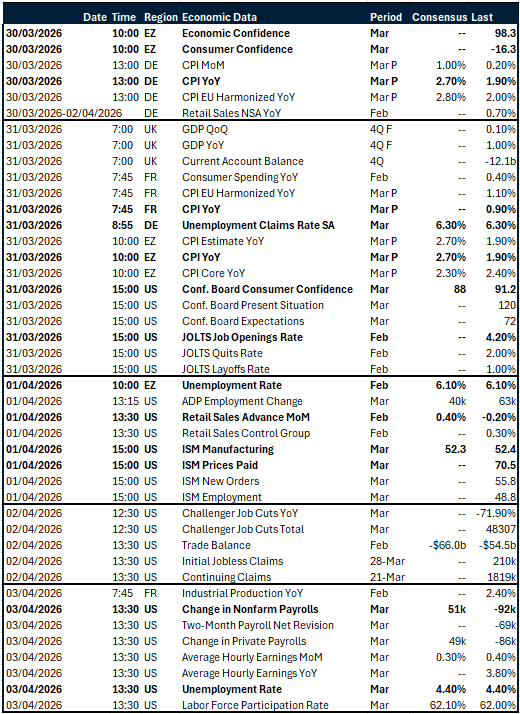

Key global risk events

Calendar: March 30 – April 03

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.