GBP: Political strains erode sterling support

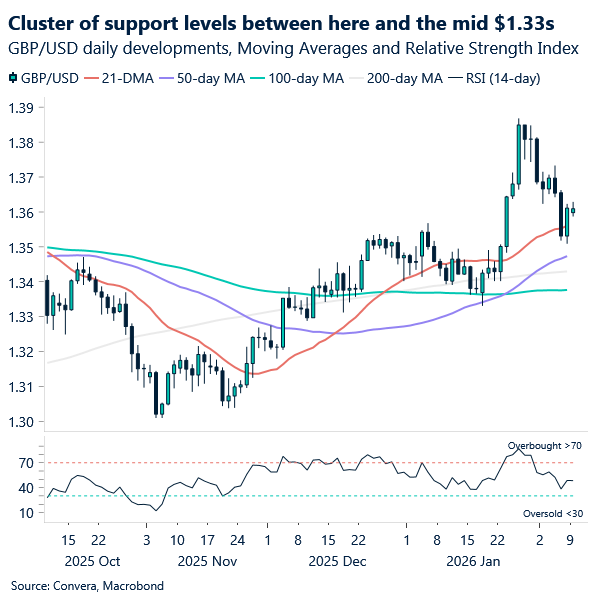

A combination of renewed political risk and last Thursday’s unexpectedly dovish steer from the Bank of England (BoE) has flipped the pound’s near‑term outlook on its head. GBP/USD has slipped below $1.36 this morning and is now fighting to hold the 21‑day moving average. There’s a cluster of support levels between here and the mid‑$1.33s that could slow the pace of decline, but the tone has clearly shifted.

Those political risks escalated over the weekend as Morgan McSweeney resigned as Chief of Staff to the Prime Minister, citing the fallout from the Mandelson–Epstein affair. The move is intended to shield PM Keir Starmer, but recent history suggests such resignations tend to buy limited time, and political commentators now see the leadership backdrop as more fragile.

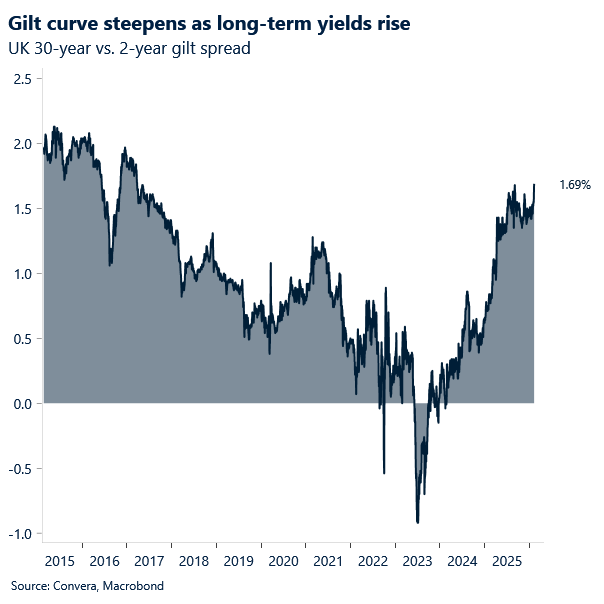

Markets are already drawing the obvious conclusion: policy could tilt leftwards to shore up support within the Labour Party. If that happens, investor nervousness around the UK’s fiscal trajectory and long‑term debt sustainability will grow. That’s feeding directly into the gilt curve, where term premia have been rising and long‑end yields remain sticky even as the front end rallies.

For sterling, this is an uncomfortable mix. The BoE’s dovish vote split has eroded the pound’s rate‑supportive cushion, and the political layer adds another risk premium that investors are reluctant to fade. Until the policy path and political narrative stabilise, the balance of risks for GBP skews lower.

For GBP/EUR, although the broader uptrend technically remains intact — holding above the lower‑bound trendline of the post‑November rally — sentiment has deteriorated and momentum indicators have rolled over. The next key level is €1.1457, the 100‑day moving average. A clean break below there would signal that the corrective phase has further to run and could open the door to deeper declines, especially if political risk premia continue to build.

USD: Packed data week will test the dollar’s rebound

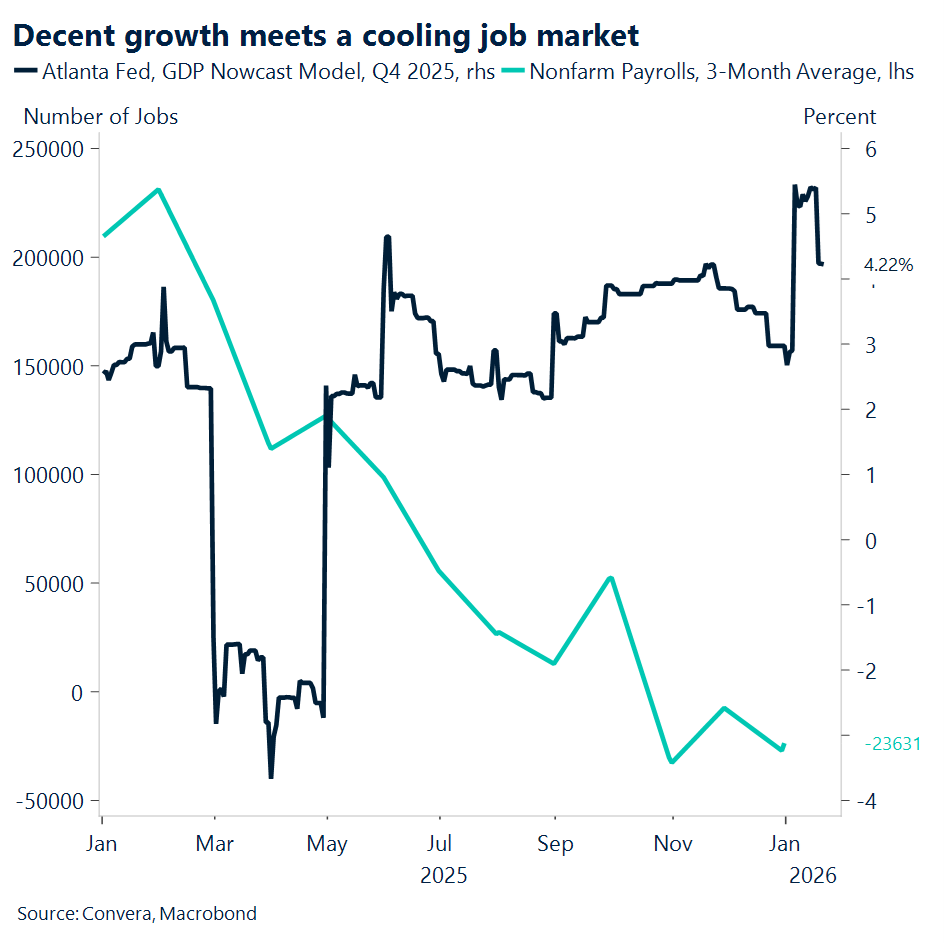

The macro data are sending mixed signals that challenge prior convictions about the cycle, but the pattern is consistent with a K shaped economy. Services and manufacturing both show stabilization to start the year, with the January ISM Services PMI holding at 53.8 and the ISM Manufacturing PMI rising to 52.6, the latter’s first expansionary reading in a year. At the same time labor demand looks softer, as private payrolls rose by only 22,000 in January and job openings slipped to about 6.5 million in December. That divergence aligns with a K shaped backdrop in which high income consumption and continued investment in artificial intelligence sustain demand and productivity while trade exposed and middle income segments face tighter hiring and tariff related price pressures, themes Fed officials have flagged in recent communications.

Against that backdrop San Francisco Fed President Mary Daly has emphasized labor market risks even as she supported the Federal Open Market Committee’s decision on (Jan 28) to hold the policy rate at 3.50 to 3.75 percent. In last week remarks she said she could have made a case for easing a little more and kept the door open to additional cuts if hiring weakens, which is directionally consistent with our view that last week’s job readings do not materially change the policy path and that the committee will put more weight on near term inflation data. That stance also fits with a committee that cut three times last year and then paused in January to reassess, a sequence that leaves incoming prices data as the swing factor for the next move.

Vice Chair Philip Jefferson has articulated the same bridge from growth resilience to policy patience. Last week he described himself as cautiously optimistic that disinflation will resume as tariff pass through fades and productivity remains firm, and he said the current stance is broadly within the neutral range with a bias to wait for clearer evidence before easing again. That framing matches our baseline that inflation prints will dominate the near term reaction function while officials acknowledge that tariffs, sticky goods prices, and a gradually softer labor market have complicated the last leg of disinflation.

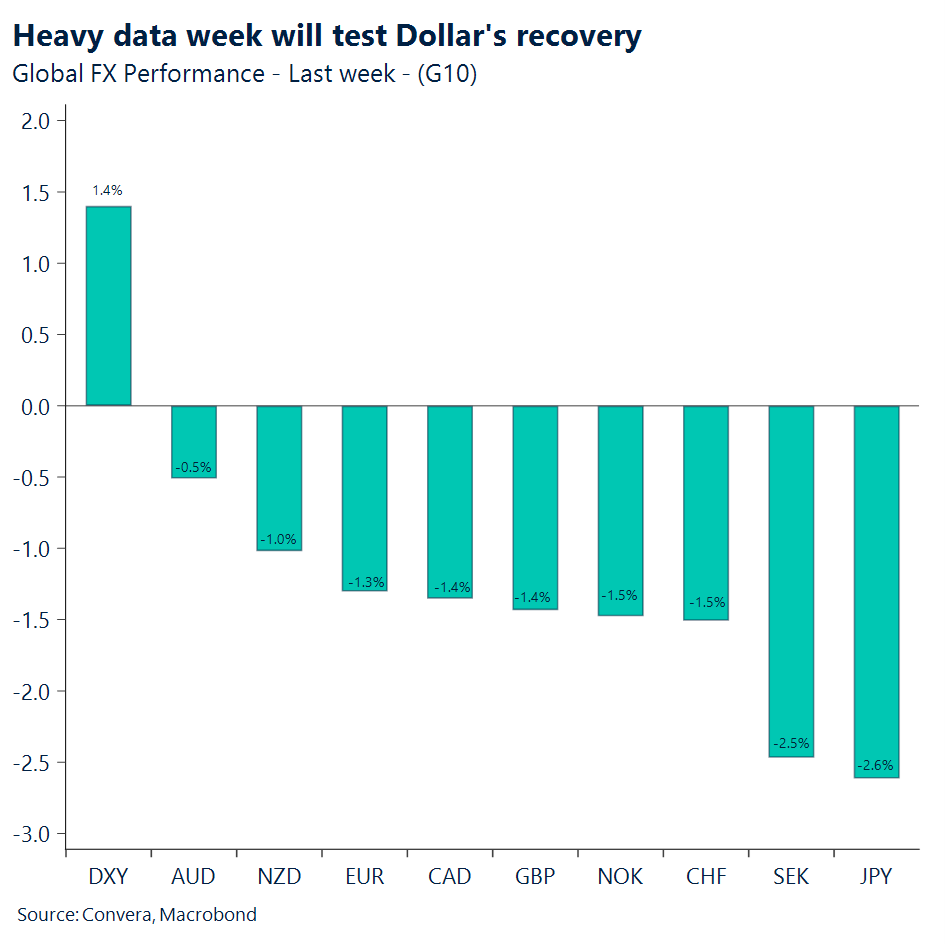

The heavy data week ahead is going to test last week’s Dollar recovery, with the Dollar Index hovering near a two-week high. The three market moving releases arrive in quick succession: retail sales on (Tue, Feb 10), NFP on (Wed, Feb 11), and the January CPI on (Fri, Feb 13). January CPI often runs firm because price lists reset and seasonal factors can under adjust, and several desks are flagging an unusual early year rise in core goods prices in online data. The Bureau of Labor Statistics will also publish annual benchmark revisions alongside the (Feb 11) jobs report, following advance guidance that marked down the twelve months through March 2025 by about 911,000, which raises the risk that several 2025 payroll months turn negative after re benchmarking. In all, we do not think the latest JOLTS estimates shift the policy outlook. Our base case remains that the FOMC focuses on the next inflation prints and, provided price pressures ease, delivers 25bp cuts in (June) and (December), while monitors subsequent labor reports for any deterioration in conditions.

EUR: Jobs test to steer EUR/USD

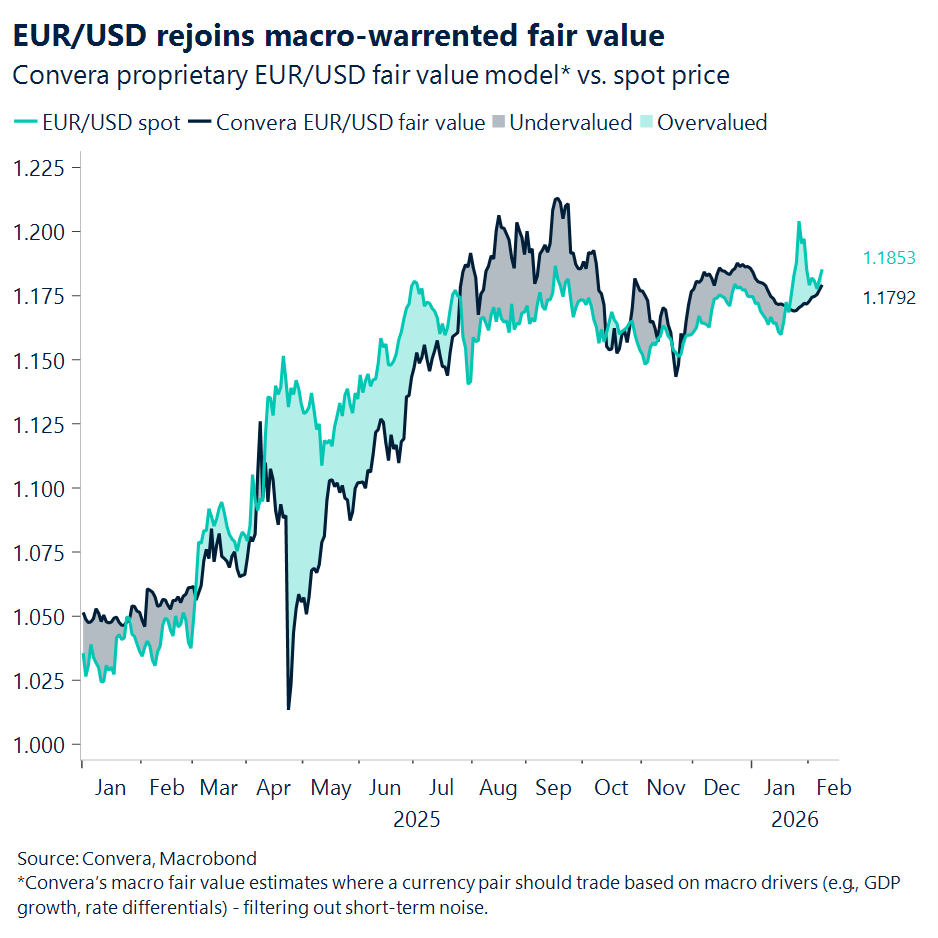

EUR/USD slipped about 0.3% into the weekly close as the market unwound the sentiment‑heavy euro bid built during the recent USD selloff, but paired some losses on Friday as the US macro story failed to gain traction in support of the greenback. The pair is now trading much closer to its fair value zone, which has drifted toward the upper 1.17 area. Meanwhile, overnight reports that Chinese regulators advised financial institutions to rein in their holdings of US Treasuries on market volatility concerns helped keep the pair sentimentally inflated into the week’s start, hovering in the 1.18 area.

The fair value anchor nudged higher through the week, helped by a US data flow that failed to deliver a decisive macro signal. Labour indicators softened again, keeping the broader picture uneven and limiting euro downside beyond a technical clean‑out. With US fundamentals still muddled, EUR/USD remains gravitationally pulled toward 1.18 until US jobs and inflation prints this week offer clearer direction.

On policy, the ECB held steady as expected. Lagarde’s neutral tone reinforced the idea that eurozone resilience – and limited concern about currency‑driven disinflation – keeps the policy stance firmly in wait‑and‑see mode. That restored neutrality shifts the spotlight back to the US side of the rate differential, just as the FOMC’s recent labour‑market optimism faces a reality check.

This backdrop will be quite instructive this week in delineating short‑term EUR/USD price action, with the US jobs report set to either challenge or validate the FOMC’s more upbeat labour market outlook, triggering a more pronounced repricing of near‑term policy expectations in turn. An above‑consensus result would likely pull the pair back below 1.18 as rate differentials re‑widen in favour of the greenback. That said, with markets having priced in a hawkish baseline from this month’s Fed policy meeting, any softer‑than‑expected major US data release in the coming weeks could carry a heavier bullish impact on EUR/USD.

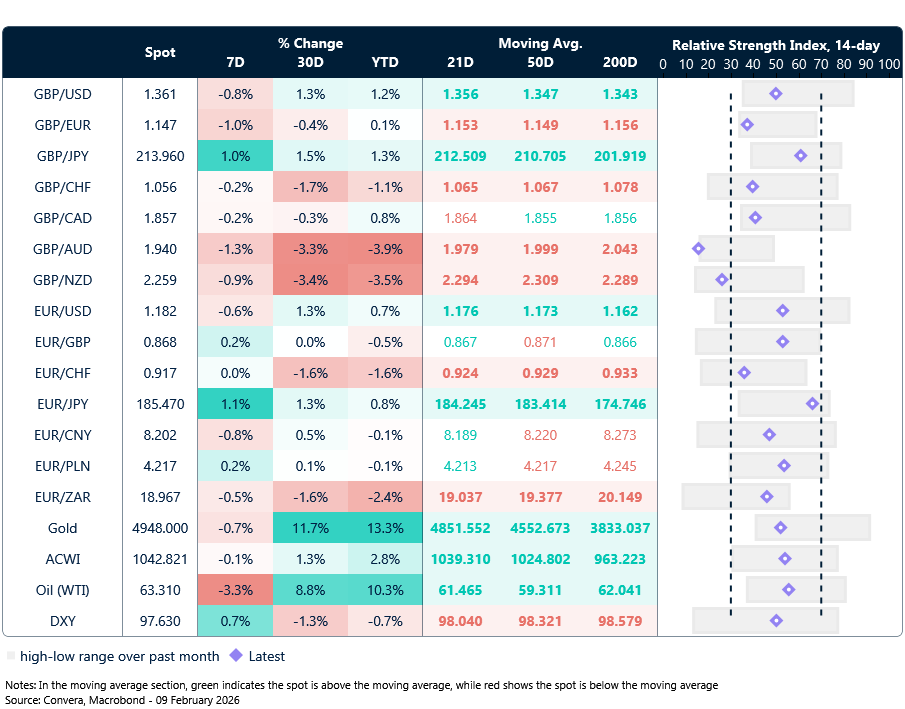

Market snapshot

Table: Currency trends, trading ranges & technical indicators

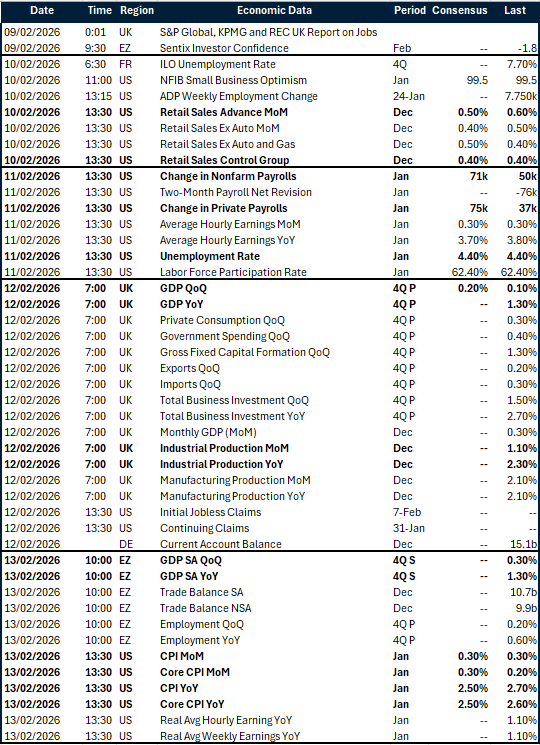

Key global risk events

Calendar: February 9-13

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.