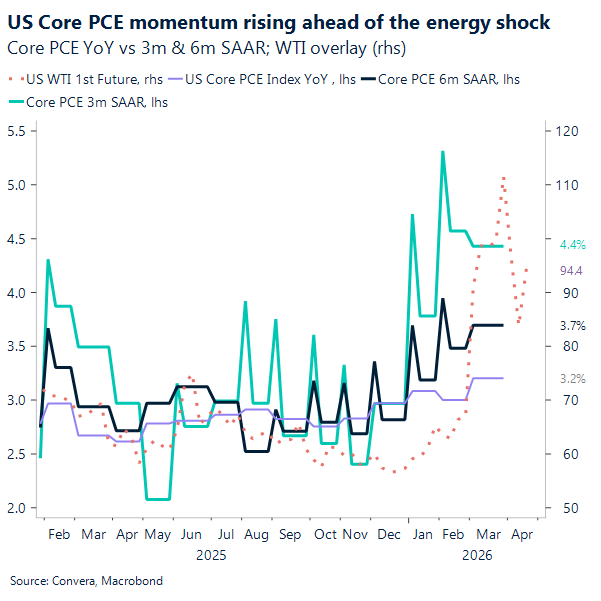

USD: Sticky inflation challenges Fed’s path

Yesterday’s economic data highlights a growing tension within the war-impacted economy. Core PCE has reached its highest level since late 2023, driven by energy costs that are quickly spreading to other sectors. Simultaneously, jobless claims dropped to their lowest point since 1969. This combination of stubborn inflation and a resilient labor market makes it difficult for the Fed to justify rate cuts. Consequently, the hawkish stance recently adopted by several Fed officials appears increasingly justified by the numbers.

The growth story reveals a sharp divide between different sectors of the economy. While first-quarter GDP bounced to 2.0%, massive AI investments are fueling a surge in business spending. However, middle-income households are feeling the squeeze of high gas prices, leading to a visible decline in consumer outlays. Government spending currently helps offset a widening trade deficit, but the private sector is clearly decelerating. If oil prices remain at these levels, the resulting demand destruction could push future growth below long-term trends.

We have entered a regime defined by volatility rather than clear trends. The US economy continues to outperform Europe, creating a significant divergence in global policy expectations. Investors should expect the Fed to hold rates steady even as other central banks restart their hiking cycles. This environment likely favors a strategic rotation into quality tech and international equities. In FX, despite triple-digit oil prices, the US Dollar Index remains soft as markets temporarily overlook the lasting impact of sustained energy costs.

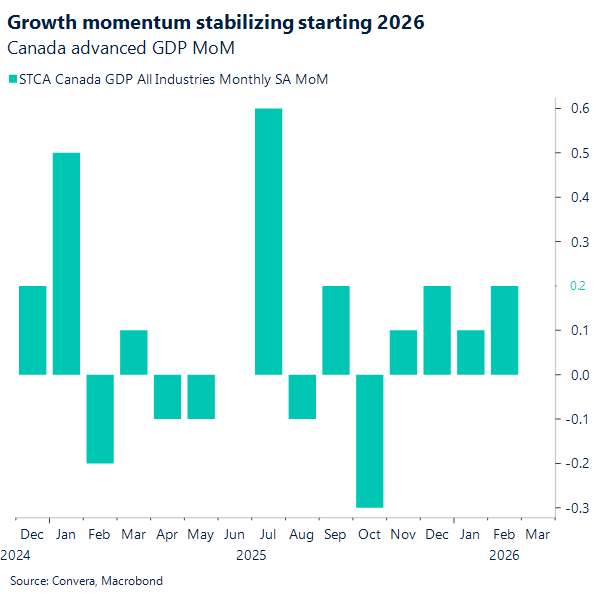

CAD: Growth momentum stabilizes starting 2026

Real gross domestic product (GDP) in Canada grew by 0.2% in February, showing decent economic activity early in 2026. Goods-producing industries drove this growth with a 0.4% gain. Specifically, the manufacturing sector jumped 1.8%, marking its best monthly performance since January 2023. Strong rebounds in auto assembly and machinery production fueled this surge as Ontario plants ramped up. Furthermore, easing supply chain bottlenecks helped wholesale trade return to growth. At the same time, transportation and warehousing advanced 1.2% due to strong freight movement. Mining and oil extraction also posted steady gains. Ultimately, these broad increases easily offset localized weaknesses in the public sector and an Olympics-related dip in spectator sports.

Despite a flat preliminary estimate for March, February’s momentum sets up the Canadian economy for a strong first quarter. In fact, annualized growth is tracking at 1.7%. This figure comfortably beats the Bank of Canada’s (BoC) 1.5% forecast and suggests solid productivity gains against a backdrop of slowing population growth. However, the energy shock stemming from geopolitical conflicts is complicating this positive outlook. The BoC now faces a difficult monetary policy tug-of-war. On one hand, higher oil prices squeeze consumer purchasing power and act as a drag on the broader economy. On the other hand, triple-digit oil prices introduce serious upside risks to inflation. Consequently, the central bank will likely keep the policy rate anchored for an extended period, though persistent energy costs could eventually force them to hike rates.

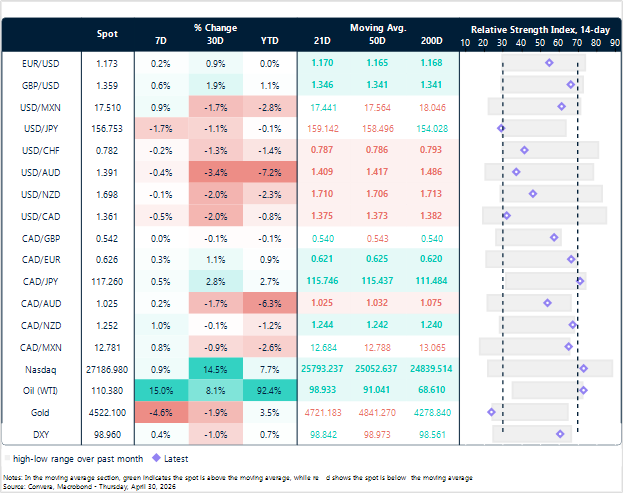

Interestingly, this macro backdrop is not the main driver behind the Canadian dollar’s recent gains. Instead, the slide of USD/CAD toward the 1.36 level is primarily a US dollar story. As markets price in less extreme geopolitical outcomes, the greenback is slowly shedding its safe-haven conflict premium. Domestically, the Loonie lacks a strong secondary engine to pull the pair meaningfully closer to its fair value. February’s growth merely met market expectations, and sluggish CUSMA renegotiations continue to act as an overhead risk premium. Because the BoC’s current path is already priced in, the CAD remains vulnerable to US headline risks. Therefore, the currency pair will likely maintain a choppy bias around the 1.36 mark as we approach the next employment report.

MXN: Mexico growth slows as Peso wobbles

Mexico started the year on a softer footing, and the first quarter GDP report made that clear. Output rose only 0.1% year over year, missing expectations and coming in well below what policymakers had been penciling in. The details matter because they point to an economy running below potential, with a wider negative output gap than the central bank expected. Services were the main support on the year, but the quarter told a weaker story as services fell 0.6% and signaled that household consumption is losing momentum after doing much of the heavy lifting last year.

That softer demand picture also fits with the pressure coming from US tariffs and lingering trade uncertainty. Industry dipped 0.2% on the quarter and the trend still looks downward, even if public investment is no longer collapsing like it did last year. Agriculture also pulled back again, adding to the overall drag. Even so, the baseline is not a deep downturn, just a bumpy patch. A modest rebound in the second quarter still looks reasonable, but risks remain tilted to the downside, and the Middle East conflict adds another headwind through global risk sentiment even if the direct impact on Mexico is limited.

Those macro dynamics help explain the peso’s recent path. The Mexican peso still benefited from carry earlier in April and outperformed several peers, but it softened late in the month as geopolitical tensions boosted oil prices and kept the US dollar firm on a slightly more hawkish Fed tone. USD MXN pushed up toward 17.5 by end April, marking the weakest peso level in about three weeks. At the same time, Mexico inflation eased with headline drifting down to 4.53% in the first half of April and core easing to 4.27%, which reinforced expectations for a more dovish Bank of Mexico. Put together, softer growth and cooler inflation make a rate cut at the May meeting more likely, and that policy repricing has been an added weight on MXN even as the broader trend remains relatively constructive.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

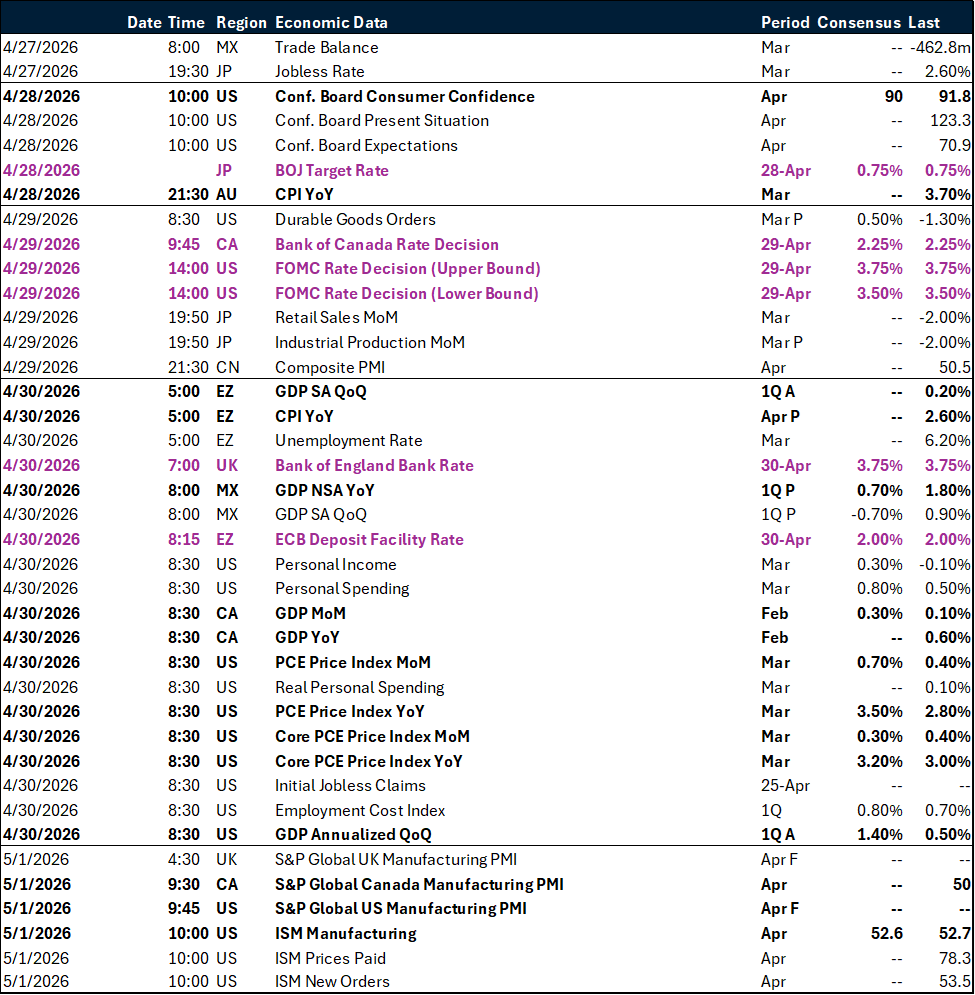

Key global risk events

Calendar: April 27 – May 01

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.