USD: Lower yields, lower dollar, despite mixed signals

Recent de-escalation efforts are keeping a firm lid on the US dollar. The US dollar index is down 1.5% this week despite mixed signals from the Middle East. Markets reacted to Israeli Prime Minister Benjamin Netanyahu’s announcement of an agreement to begin direct talks with Lebanon. However, hours later the Prime Minister confirmed that there is no ceasefire in Lebanon, and Israel will continue to strike Hezbollah.

This geopolitical optimism has spilled into broader market sentiment. Over the past week, the VIX fear index dropped sharply from 30 to 20, reflecting a clear easing in investor anxiety. Major US equity indexes have recovered to near flat for the year, while the two-year Treasury yield has fallen 12 basis points as markets reprice near‑term risk.

US economic data adds to the mixed picture. Fourth-quarter GDP was revised down to an annualized 0.5%, below the prior 0.7%, highlighting how momentum faded late in 2025 despite strong signals entering 2026. The labor market is also showing continued signs of cooling, with initial jobless claims rising to 219,000, above expectations. Meanwhile, personal income unexpectedly fell 0.1% in February, even as consumer spending grew at a slightly slower pace.

Taken together, these crosscurrents leave the Federal Reserve in an increasingly uncomfortable position, which aligns with the Fed’s minutes released this week. Policymakers are balancing persistent inflation risks against the possibility that global tensions weigh on labor markets. Core PCE inflation holding at 3.0% year over year reinforces concerns that price pressures remain sticky. With growth slowing and inflation risks heightened by potential energy disruptions, the Fed’s policy flexibility continues to narrow.

The combination of softer data and easing geopolitics creates an unusual market dynamic. Falling yields and a weaker dollar are providing equities breathing room, fueling the current relief rally.

Still, a sustained FX mean-reversion trend depends on factors deeper than the next headline. The outlook hinges on whether the truce proves to be a durable off-ramp and if the physical oil and shipping systems actually normalize.

EUR: Euro rides fragile optimism and hawkish tailwinds

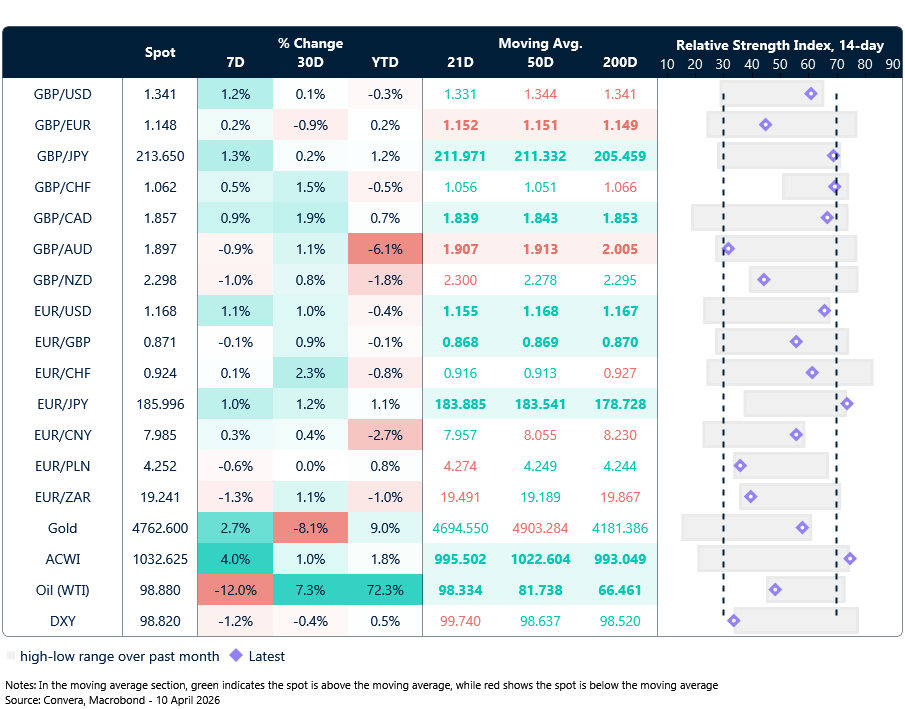

EUR/USD spent yesterday testing a cluster of flat long‑term moving averages just below the 1.17 line, closing just barely above them by the end. Near‑zero slopes on these gauges point to directionless underlying momentum, yet the pair’s persistence in challenging them signals growing confidence among euro buyers. EUR/USD has now closed higher for four consecutive sessions since April 6, reflecting a more assertive bullish posture as de‑escalation hopes build.

Despite a still‑fragile truce – with Israel’s continued military operations in Lebanon now a key point of contention – markets appear to believe the broader trajectory is toward de‑escalation. Strikes have fallen sharply since the ceasefire announcements, and both sides look more open to diplomacy than they were just days ago.

Against this backdrop of cautious optimism, the euro is enjoying a bit of a honeymoon: the ceasefire has improved risk sentiment, the diplomatic channel remains intact, and the ECB still looks comparatively hawkish versus the Fed. Even so, markets may lose patience quickly if they are not met with clearer conditions attached to the ceasefire and tangible progress toward something more durable.

We remain skeptical of a more confident foothold in the 1.17 area this week, given the still‑high uncertainty on the ceasefire front. The US also releases March CPI today, with a sizeable jump expected – and any knee‑jerk hawkish reaction on the US side is likely to keep EUR/USD upside capped.

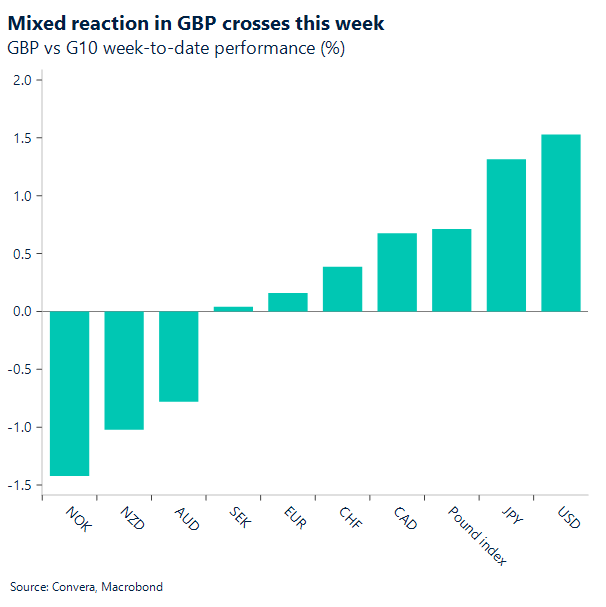

GBP: Sterling’s diverging paths

Sterling is on track for its second‑largest weekly gain of the year versus the dollar. GBP/USD has rebounded sharply, reclaiming the 1.34 handle after briefly slipping below 1.32 earlier in the week. The pound has also firmed modestly against the euro, edging back toward 1.15, while posting a 1.5% rise versus the yen and underperforming the Antipodeans by around 1%.

The moves reflect a burst of ceasefire‑driven optimism as markets unwind defensive USD positioning. But the underlying environment remains low‑visibility. Energy prices are still elevated, and the ceasefire’s practical impact is limited so far: only ten ships have passed through the Strait of Hormuz since the announcement — none of them fuel carriers. For the UK, one of Europe’s most gas‑dependent economies, this keeps the inflation risk premium alive. Options markets reflect this, with GBP volatility demand exceeding EUR, signalling traders see sterling as more exposed.

Political risk is also re‑entering the narrative. With the May election approaching, investors are wary that a Labour government could lean into more expansive fiscal commitments. Any perception of looser, less sustainable spending would likely unsettle gilts, steepen the long end of the curve and weigh on sterling via the sentiment channel.

In short, sterling’s conflict‑driven resilience against the euro looks increasingly vulnerable, with the cross shifting toward a more fragile, growth‑sensitive dynamic. Against the dollar, however, the technical picture is more constructive: GBP/USD still has scope for further gains if risk sentiment holds and key resistance levels give way.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

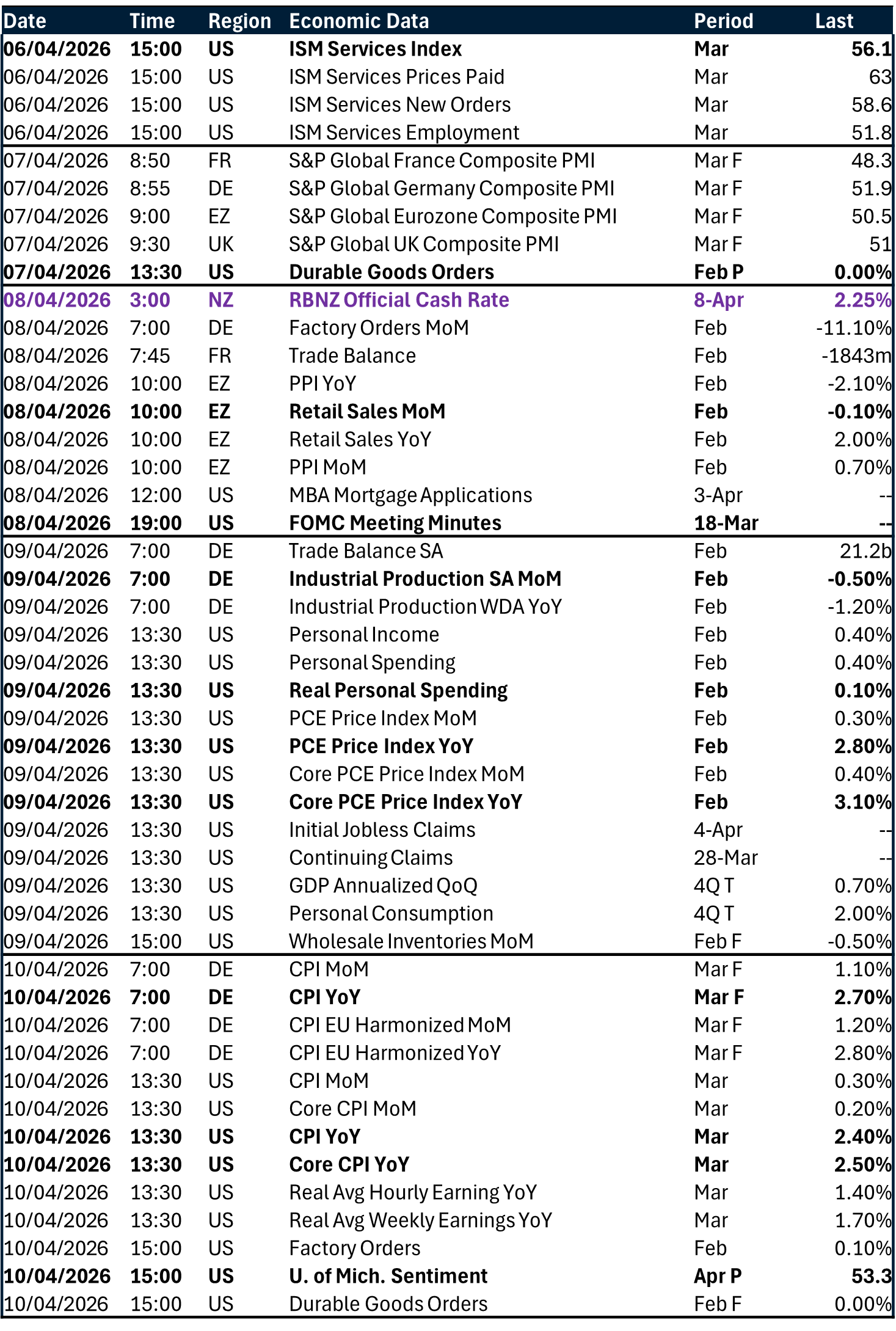

Key global risk events

Calendar: April 06-10

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.