USD: Soft jobs and strong services keep dollar bid

The latest ADP data signals stabilization in the U.S. labor market after two months of decline, though underlying details point to continued softening in demand. Private-sector payrolls rose by a modest 42,000, reversing the prior month’s downward revision. While any gain is welcome, this increase was entirely driven by large firms. In contrast, employment at small businesses fell for the fifth time in six months. This divergence suggests that while major companies may be selectively expanding, the broader economy, often powered by smaller firms, is still pulling back on hiring. Meanwhile, high-profile layoffs at Amazon, Starbucks, and Target continue to stoke concerns about the labor market’s overall health.

To properly assess the 42,000 gain, one must consider the structural recalibration of the labor market, as analyzed by the Federal Reserve Bank of Dallas. The “break-even employment” rate, the pace of job growth needed to absorb new labor and keep unemployment steady, has collapsed. Driven by reversed immigration flows and cyclical shifts in labor force participation, this threshold has fallen from a peak of 250,000 in 2023 to around 30,000 by mid-2025. In this context, what once seemed alarmingly low now reflects equilibrium, suggesting the 42,000 figure is not weakness, but balance.

Complementing the labor data, the ISM Services Index showed a strong rebound in non-manufacturing activity, expanding at its fastest pace in eight months. This surge was fueled by a sharp rise in demand, with New Orders jumping to 56.2 and Business Activity climbing to 54.3. These forward-looking indicators signal resilient consumer and business demand. Given that services comprise the largest share of the U.S. economy, recession fears may be premature despite soft payrolls.

However, this strength comes with an inflationary sting. The demand rebound pushed the Prices Paid index to a three-year high of 70, highlighting ongoing challenges for monetary policy. The services report also echoed labor stabilization, with its employment index rising to a five-month high of 48.2, still contracting, but at a slower pace. Taken together, modest labor gains consistent with a rebalanced market, surging demand, and persistent service-sector inflation have reduced the likelihood of another rate cut this year. The U.S. dollar remains firmly bid, trading at its highest level since late May and testing key resistance at the 200-day SMA, a technical level closely watched in FX markets.

Beyond the data, investor attention is turning to the U.S. Supreme Court hearings on the legality of certain administration-imposed tariffs, a development that could carry significant implications for trade policy and market sentiment.

As mentioned this past Monday, the data this week may not provide enough of a catalyst, and dollar bulls might need to remain patient. Technically, a strong breakout above its 200-day SMA may still require a more compelling fundamental driver. With the government shutdown becoming the longest on record, the interplay between fiscal uncertainty, the future of trade policy and monetary policy expectations will be key in shaping the dollar’s near-term trajectory.

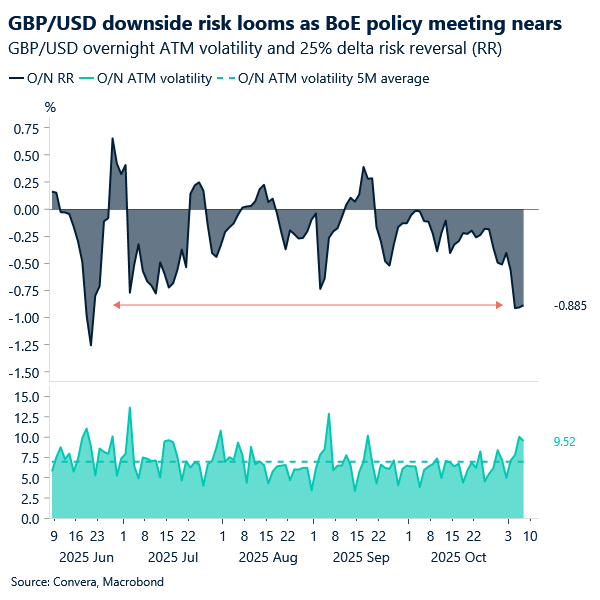

GBP: Easing ahead but not fully priced

While only 9 basis points of a quarter-point cut are priced in, today’s BoE meeting may reawaken dovish sentiment. A softening labour market – now coupled with inflation that eased in September – and reassuring signals from Reeves, alongside media leaks hinting at restrictive fiscal measures that are reducing pressure the long end of the curve, could point to more easing than markets currently anticipate. Hawks, by contrast, may prefer to wait for the full budget picture before recalibrating the easing path, leaning more toward a December cut. By then, markets are pricing in 16 basis points of easing.

For sterling, a more pronounced dovish tilt today would hinge on remarks that inflation has eased, as the labour market’s softness has already been well telegraphed. Should such remarks emerge, expect further depreciation. On the inflation front, policymakers have yet to coalesce around the lower-than-expected September print, leaving room for more directional impetus to be embedded in the policy path.

GBP/USD, which had held above 1.3020, now risks breaching that level – and even slipping below 1.30. The pair sits at 7-month lows and its price action has clearly adopted a more bearish tone as the November budget nears.

Sterling remains technically oversold, with the Relative Strength Index (RSI) entrenched below 30. Yet fresh dovish signals from the BoE today could validate further downside, keeping momentum stretched and positioning skewed.

EUR: A pause in the pressure

The euro broke a five-day losing streak against the US dollar yesterday, attempting to hold the $1.15 level as global risk sentiment showed tentative signs of stabilisation. This modest improvement follows a stretch of heightened risk aversion that had reignited demand for the dollar’s safe haven qualities.

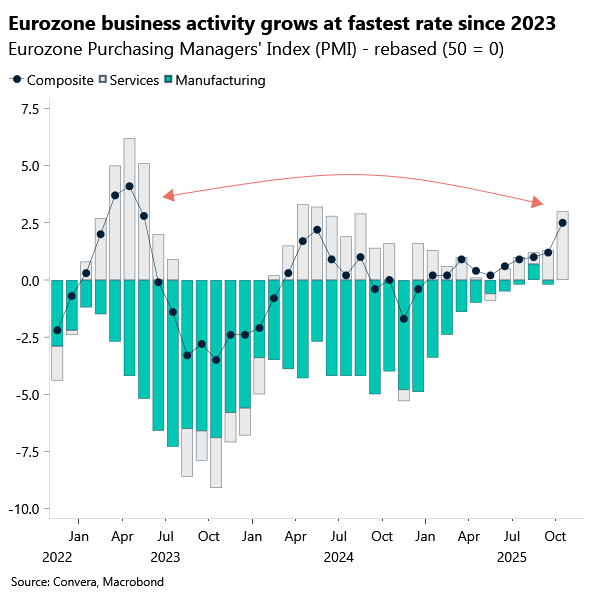

Beyond sentiment, domestic data offered partial support. Revised PMI data surprised to the upside, surpassing both the flash estimate of 52.2 and September’s 51.2 print. This marks the strongest pace of expansion since May 2023, pointing to a meaningful rebound from the sluggish momentum that defined much of 2025. Services activity accelerated sharply, while manufacturing posted only marginal gains. The improvement was demand-led, with new business inflows rising at the fastest rate in two and a half years.

Meanwhile, data this morning showed industrial production rose by 1.3% m/m in September, partially reversing the steep August decline of -3.7%. The data points to tentative signs of life, but improvements over the coming months are likely to remain modest and rooted in low base effects. In short, this is a cyclical bounce – not a turning point.

Aside from the domestic news – with US macro data flows stalled by the ongoing government shutdown, the euro lacks its most potent bullish driver: soft US fundamentals. In the absence of fresh downside catalysts for the dollar, EUR/USD remains vulnerable to renewed selling pressure, despite the valuation gap of roughly two cents versus our fair value estimate.

GBP/USD sits in oversold territory

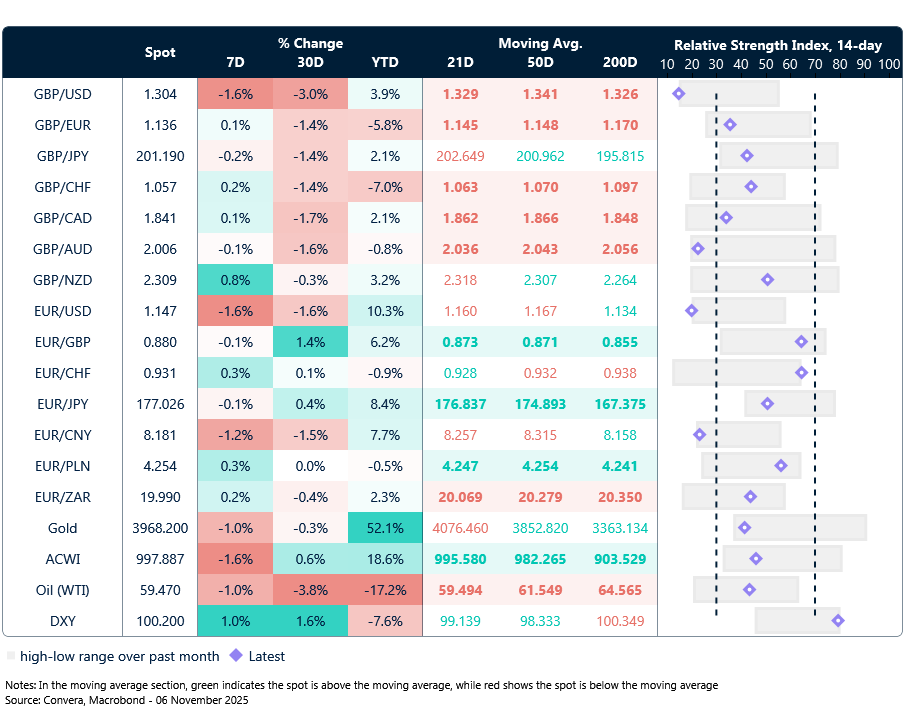

Table: Currency trends, trading ranges and technical indicators

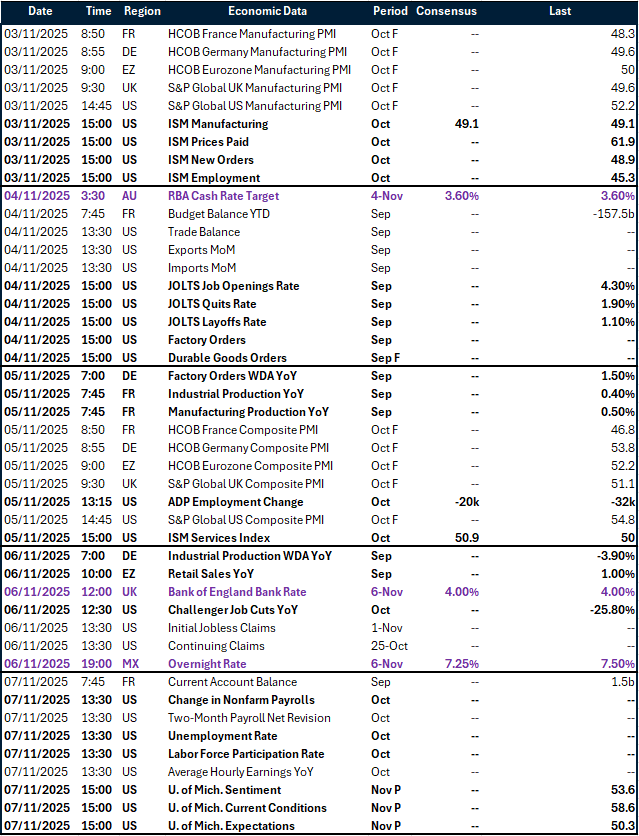

Key global risk events

Calendar: November 3-7

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.