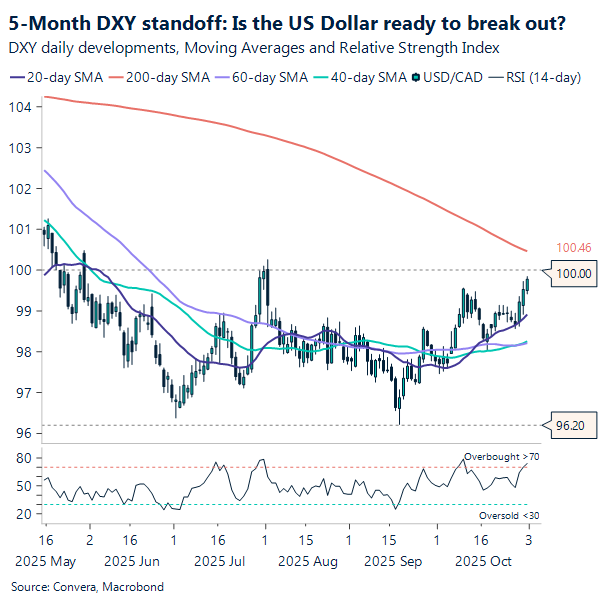

USD: Dollar gains in October as markets weigh Fed’s ‘two and done’ path

The dollar’s recent resilience is difficult to ignore. Despite back-to-back rate cuts by the Federal Reserve in September and October, many market participants had expected this to trigger a more pronounced weakening of the USD. Yet, the DXY has remained range-bound, consolidating since late May, a sign that the dollar’s underlying support remains intact. In October, the US DXY index was up 2%, its first monthly gain since July.

Since August, we’ve argued that the threshold for sustained dollar weakness has risen. This year’s depreciation was driven more by currency hedging and portfolio repositioning than by a broad-based divestment from US assets. While many still lean toward further dollar softness into year-end, several factors complicate that narrative. These include the resilience of US economic growth (Atlanta Fed’s nowcast model points to a healthy 3.9% Q3 growth), the structural support from persistent fiscal deficits, a cautious Fed, and a market that has already priced in much of the anticipated easing. As a result, the dollar’s trajectory is increasingly tied to actual economic outcomes rather than speculative expectations of dovish policy.

Monetary policy remains in a bit of a holding pattern. While another rate cut seems increasingly probable, the lack of September’s Non-Farm Payroll data has left FOMC officials hesitant to make firm commitments. There’s a general sense that the labor market is losing momentum, but without concrete figures, policymakers are understandably taking a cautious approach. In fact, last Friday, two Fed officials publicly opposed the recent rate cut, citing persistent inflation concerns. Kansas City Fed President Jeff Schmid, who voted to hold rates steady, stated: “By my assessment, the labor market is largely in balance, the economy shows continued momentum, and inflation remains too high.”

Complicating matters further is the ongoing government shutdown, now nearing a historic milestone. It’s approaching the longest in US history (35 days), and its continuation has disrupted key economic data releases. In the absence of official labor statistics, market participants will turn to alternative indicators this week, including Wednesday’s ADP employment report. While PMI and ISM data will also be released, their market impact is expected to be limited.

In this context, the dollar’s resilience could extend into November. If alternative labor market data shows signs of strength, it may further bolster the USD, especially as speculation around the Fed’s next move intensifies. But can this resilience translate into a breakout from this five-month sideways trend? Could the news of a government shutdown resolution trigger it? The long-awaited payroll data from the past two months? Or perhaps a dose of bad news from global peers? Fresh data this week may not provide enough of a catalyst, and dollar bulls might need to remain patient. Technically, the charts point to a test of the five-month upper band, but a strong breakout above 100 may still require a more compelling fundamental driver. With the government shutdown potentially becoming the longest on record, the interplay between fiscal uncertainty and monetary policy expectations will be key in shaping the dollar’s near-term trajectory.

GBP: Sterling on shacky grounds

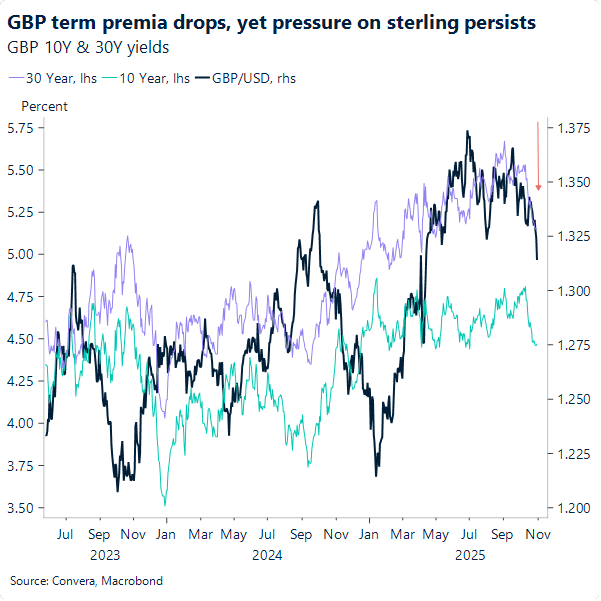

Sterling enters the week on fragile footing ahead of Thursday’s BoE meeting. Markets are pricing in just 7bps of easing for this week and 17bps by year-end – leaving room for dovish surprises, especially after September’s softer inflation print gave policymakers more room to pivot amid a persistently soft labour market and stagnant growth.

Technically, GBP/USD looks increasingly vulnerable. The 1.30 level – unseen since April – is now in play, with the pair having broken below its 200-day moving average for the first time since sterling’s H1 rally against the dollar. The setup leaves the pair unanchored, emboldening bears to engage more forcefully.

Looking into December, the Budget may offer a brief reprieve if fiscal discipline is perceived as credible – recent declines in long-term yields suggest rising expectations of restrictive policy manoeuvres. But the underlying “fix-the-fiscal-hole” policy mix – whether tax hikes or spending restraint – will likely reinforce the need for further BoE easing to support growth. That’s a structurally bearish setup for sterling, whichever bearish force ultimately dominates.

CAD: Federal budget set to be released tomorrow

Last Friday, Statistics Canada released the GDP figures for the month of August. Canada’s real GDP declined by 0.3%, erasing most of July’s gains due to widespread weakness across goods and services sectors. The goods sector shrank 0.6%, its fifth drop this year, while services slipped 0.1% for the first time in six months. Transportation and warehousing fell 1.7%, with air transportation plunging 4.6% amid a strike by 10,000 flight attendants, and pipeline transportation also declined due to reduced natural gas exports to the U.S. Wholesale trade dropped 1.2%, led by steep declines in motor vehicle and food wholesalers, while utilities contracted 2.3%—its lowest since May 2018—due to drought-affected hydroelectric output. Manufacturing fell 0.5%, though retail trade rose 0.9% thanks to gains in vehicle, clothing, and sporting goods sales. Preliminary data suggests GDP edged up 0.1% in September, indicating a modest 0.1% growth for Q3, with official figures due November 28.

These latest GDP figures underscore the fragility of Canada’s economic momentum heading into the final quarter of the year. While September’s advance estimate points to a modest uptick, the broader picture remains clouded by sectoral volatility and external pressures. Looking ahead, risks remain elevated, particularly around future U.S. trade actions and the upcoming CUSMA review. By declaring 2.25% the “just right” level, the Bank of Canada has signaled a clear pivot from monetary stimulus toward the pressing need for structural reform. As Governor Macklem emphasized last week, Canada’s challenges extend beyond a cyclical slowdown, demanding long-term adjustments. The productivity theme is expected to take center stage in November as fiscal policy enters the spotlight with federal budget discussions. The Federal budget is expected to be released tomorrow. With a minority government in power, the outcome of those talks remains uncertain, and could even set the stage for a federal election if consensus proves elusive.

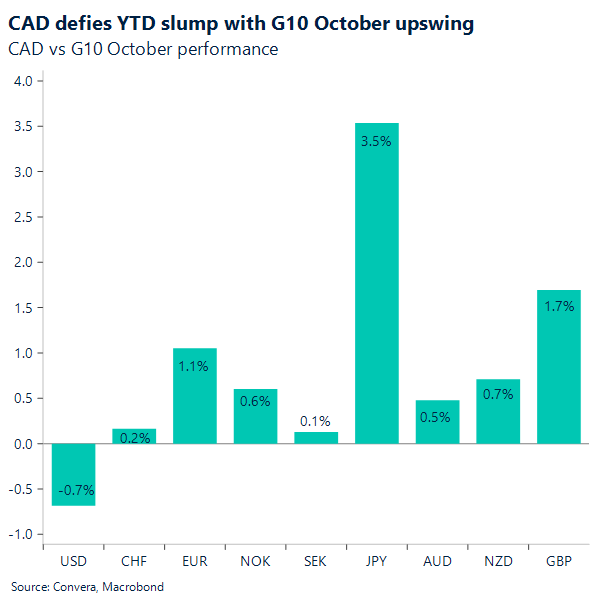

In FX, a similar setup unfolded month-end to the September double-header between the Bank of Canada and the Fed. Back then, a dovish BoC and a hawkish Fed press conference pushed USD/CAD above 1.40. This time, USD/CAD dipped below 1.39 following the BoC’s expected rate cut, as markets weighed the end of Canada’s easing cycle against a Fed that still has room to normalize in upcoming meetings. However, Powell’s signal that the December meeting isn’t locked for another cut led markets to reprice the odds of a ‘two and through’ scenario, sending USD/CAD as high as 1.401. With the latest GDP figure, the USD/CAD has pushed higher to 1.404. The 1.408 level marks a critical short-term resistance for USD/CAD, representing the pair’s highest trade in October and its peak since April. If demand for the U.S. Dollar holds and US labor data doesn’t point to weakness, the Loonie will remain under pressure. In Canada, beyond the federal budget discussions, this week’s employment report is expected to reinforce the central bank’s view of a slowing economy and soft labor market.

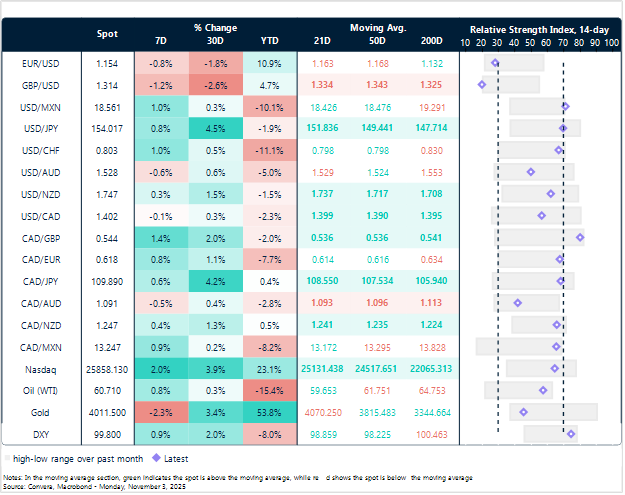

US Dollar broad-based recovery looks stretched across G10 pairs

Table: Currency trends, trading ranges and technical indicators

Key global risk events

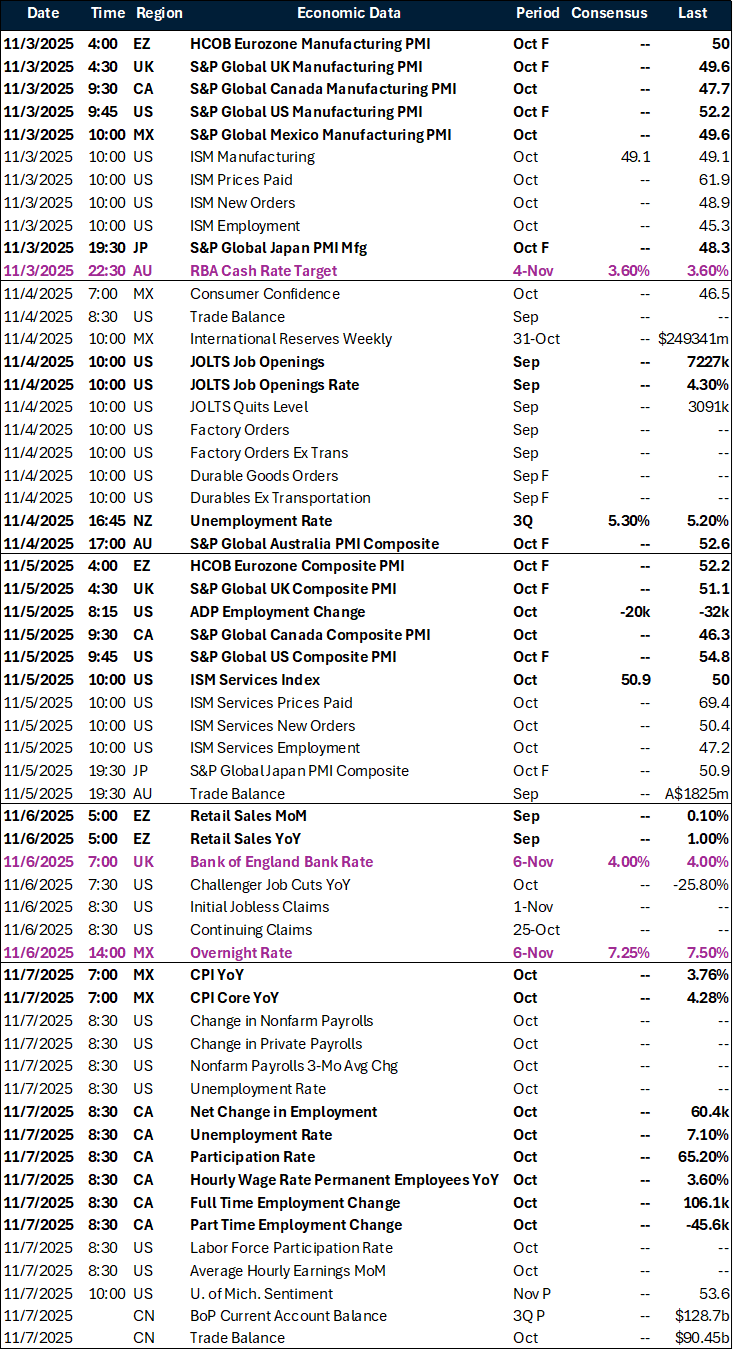

Calendar: November 3-7

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.