USD: From tactical noise to structural strength

The US dollar narrative through May has transitioned from headline‑driven volatility to a more structurally anchored bullish bias, and the latest developments reinforce that shift.

Early in the month, the dollar traded largely as a function of geopolitics, rising on escalation via oil and haven demand, and falling on de‑escalation hopes. That binary framing has since broken down. Markets are now reassessing the assumption that a peace deal is inherently USD‑negative. Instead, outcomes increasingly skew toward dollar resilience in either scenario: escalation supports the USD through safe‑haven flows and higher energy prices, while de‑escalation reinforces US growth outperformance and rate differentials.

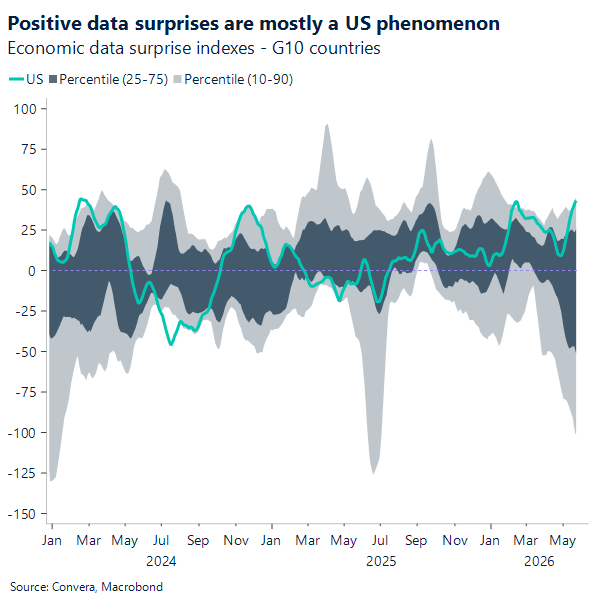

That evolution is now being validated by the data. The Citi US Economic Surprise Index is pushing toward new one-year highs, underlining persistent economic momentum, while inflation remains elevated, amplified by ongoing energy uncertainty. US real yields have risen around 40bp since the conflict began, and rate volatility has picked up, signalling tighter financial conditions and a more entrenched “higher‑for‑longer” regime.

At the same time, markets remain caught in a fragile equilibrium. Investors are increasingly tolerant of geopolitical noise, including recent US strikes on Iranian boats trying to place mines, as long as a path to a deal remains plausible. However, that tolerance looks conditional. Bond market volatility is rising, and any further move in yields risks spilling into equities, where resilience has so far held.

Crucially, this backdrop raises the bar for sustained USD weakness. Whether through inflation persistence, relative growth strength, or renewed risk aversion, the prevailing macro mix continues to favour the dollar. The narrative has shifted decisively: from a reactive, oil‑driven currency to one underpinned by structural macro advantages, with peace no longer a clear bearish catalyst.

EUR: Hormuz uncertainty caps EUR/USD

EUR/USD remains hostage to conflicting developments in the Middle East – a build-up of de-escalation momentum over the weekend and on Monday, as US officials hailed progress on a peace deal, was followed by renewed US-Israeli strikes overnight. EUR/USD has pared yesterday’s gains driven by peace optimism, capped below the 1.1650 mark, as it awaits clarity on what the renewed strikes mean for ongoing talks over an interim deal.

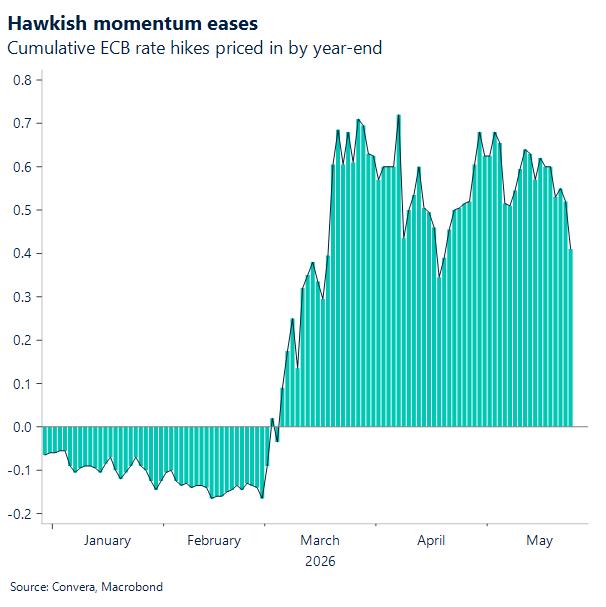

Meanwhile, the euro has lost a fair bit of support from rates. At the end of April, markets had priced in the most aggressive tightening bias for the ECB, with around 85bp expected by year-end. That has now declined to roughly 55bp. Whether June delivers a “risk management” hike to pre-empt stronger price pressures remains to be seen. However, it is becoming clearer that the euro may struggle to benefit significantly, as weakening macro conditions argue otherwise. At the same time, if the geopolitical stalemate persists into June, it is likely to continue overshadowing rate dynamics, keeping their influence on FX secondary.

Looking ahead to the week, focus will be on Germany’s labour market report and May CPI, as the ECB approaches its June meeting with conflicting signals. Beyond that, the eurozone calendar is relatively quiet. In the US, attention will turn to Personal Consumption Expenditures (PCE), the Fed’s preferred inflation gauge, which feeds directly into GDP calculations.

We continue to see downside risks for EUR/USD in a scenario where no meaningful progress emerges from Hormuz.

CAD: Yield differential pushes USD/CAD higher

USD/CAD’s move higher since mid-May has been a clean expression of widening relative-rate support for the dollar. Hotter US inflation data helped push markets back toward a higher-for-longer Fed view, while Canada entered the move with little fresh macro momentum strong enough to offset the softer labour backdrop. That left the pair trading less on idiosyncratic noise and more on the simple fact that US yields were moving higher, faster, and with more conviction.

The US–Canada 2-year yield differential has widened to roughly 120bp, its widest level since July 2025, and USD/CAD has climbed alongside it toward the upper end of its recent range. That is exactly what a relative-momentum market should look like: the US retains the yield advantage, Canada lacks a sufficiently strong domestic impulse to push back, and the Loonie remains vulnerable while that imbalance holds. Unless US yields roll over decisively or Canada delivers a materially stronger domestic surprise, the bias in USD/CAD still looks skewed toward further upside.

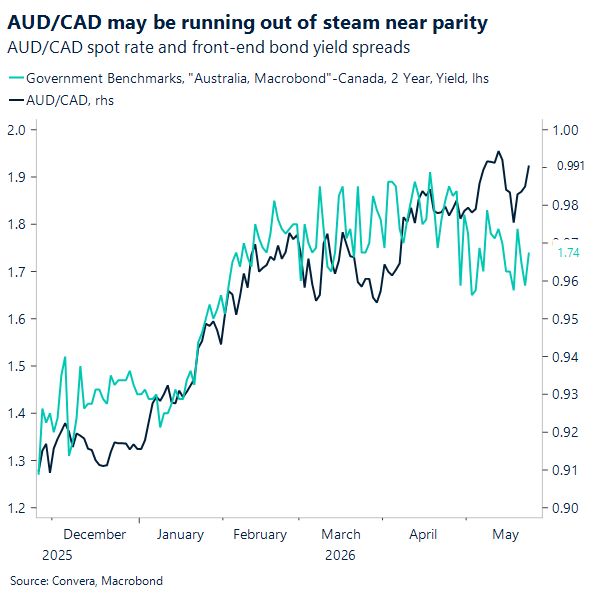

A similar story has been playing out in AUD/CAD, where the Aussie’s status as one of the top-performing G10 currencies year-to-date, combined with persistent CAD softness, has pushed the cross toward parity and up to fresh five-year highs. As the chart shows, AUD/CAD has continued to grind higher even as the Australia–Canada 2-year yield spread has stopped widening and, more recently, narrowed from its April highs. The divergence suggests that the spot has been running ahead of relative front-end rate support, which could make the cross more vulnerable to consolidation near parity ahead of key CPI data in Australia this Wednesday and Canada’s Q1 GDP print on Friday.

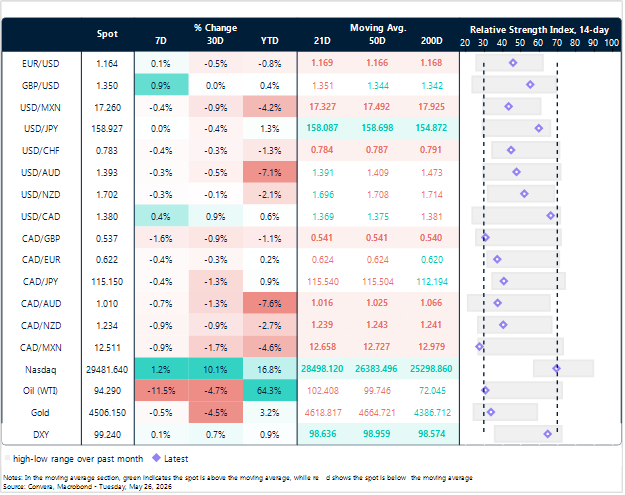

Market snapshot

Table: Currency trends, trading ranges & technical indicators

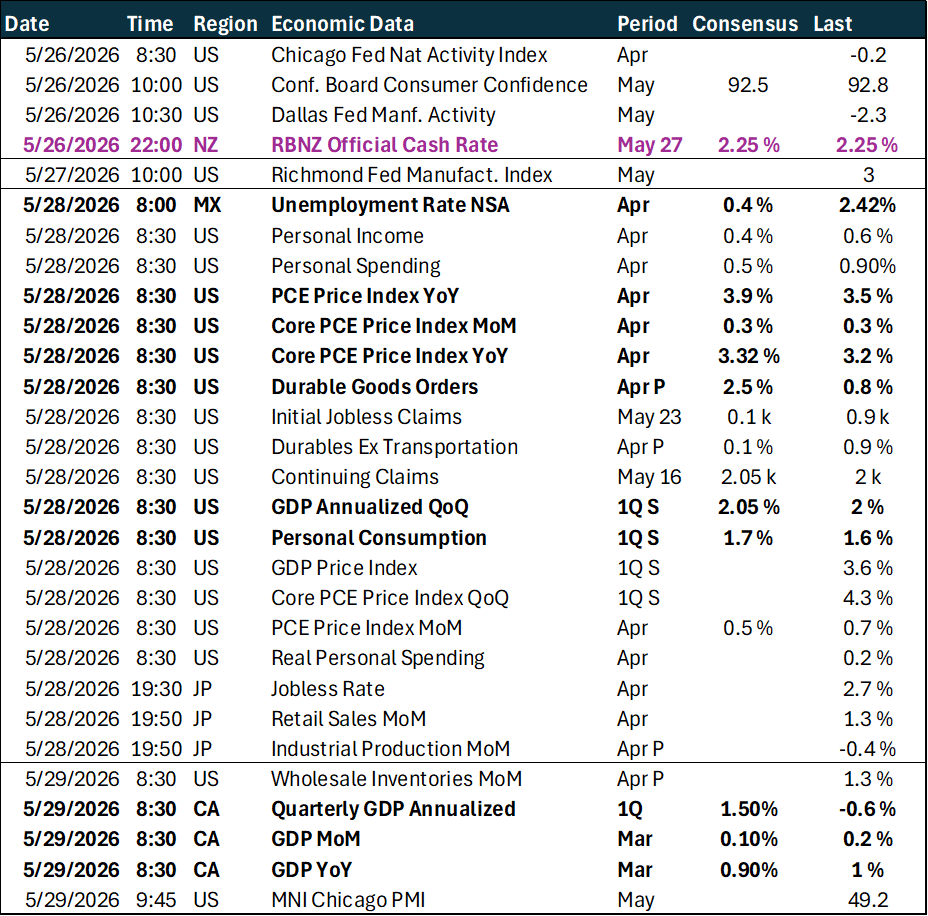

Key global risk events

Calendar: May 25 – 29

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.