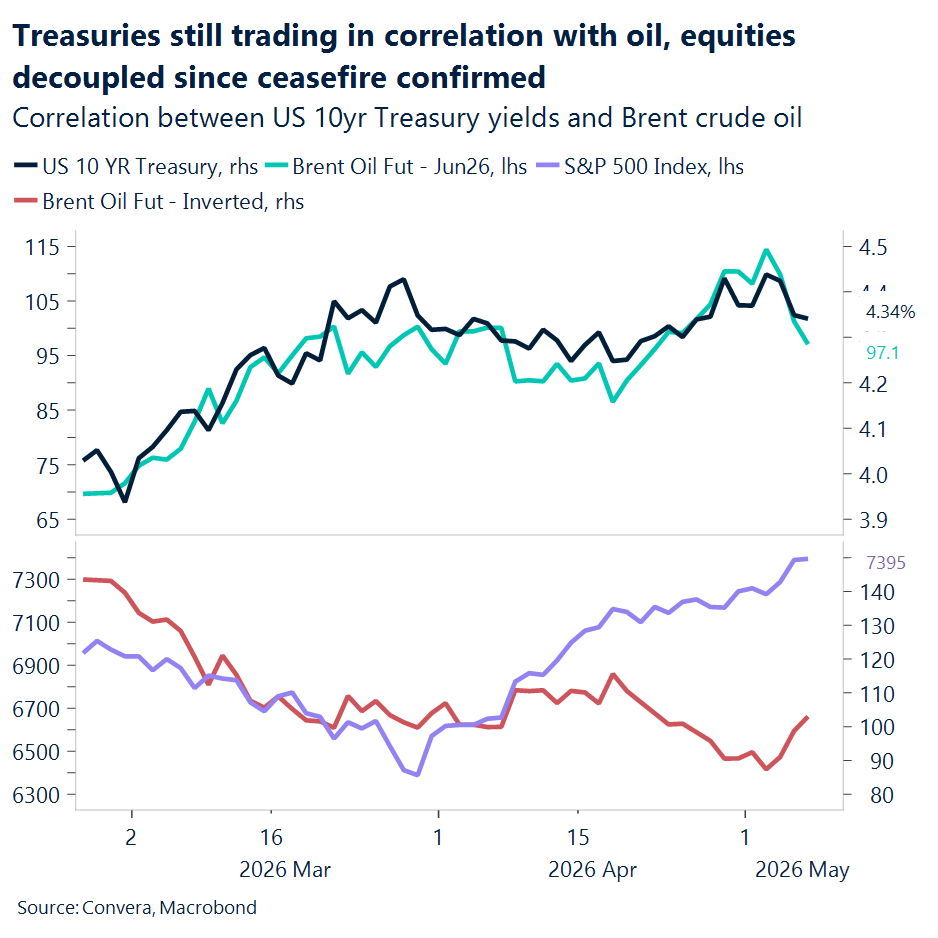

USD: Oil anchors rates, dollar stays range bound

Markets are still trying to price a return to “normal,” but the cross‑asset message remains uneven. Equities have been more willing to look through recent headlines, while rates have stayed more sensitive, with the 10‑year still taking cues from oil. That split matters, because it keeps energy and geopolitics doing more of the macro work, even as broader risk sentiment appears calmer.

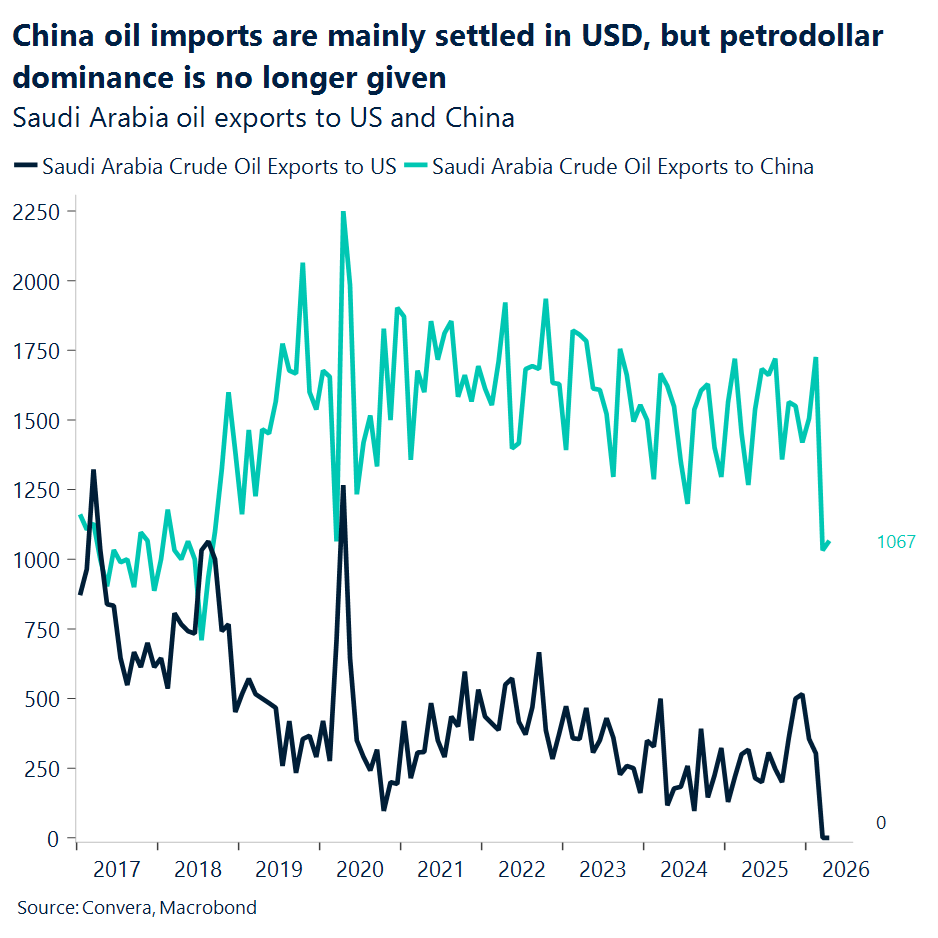

The physical oil story continues to reinforce that backdrop. Saudi crude exports to China have consistently dwarfed shipments to the US, with China typically taking four to six times more volume over recent years. That gap has widened again in early 2026: flows to the US dropped to zero in March and April, while China still absorbed roughly 1.1 mb/d in April, despite a pullback from February highs. It’s a reminder that marginal oil demand remains firmly Asia‑centric, even as overall volumes soften.

That helps explain why the yuan‑oil narrative keeps resurfacing, without yet delivering a regime shift. There is a clear economic logic to settling some China‑facing oil trade in RMB, but the broader system still runs through the dollar. Liquidity, financial depth, and security guarantees all remain USD‑centric, leaving any meaningful move away from dollar settlement more theoretical than practical for now. Talk has accelerated, but the petrodollar has not been displaced.

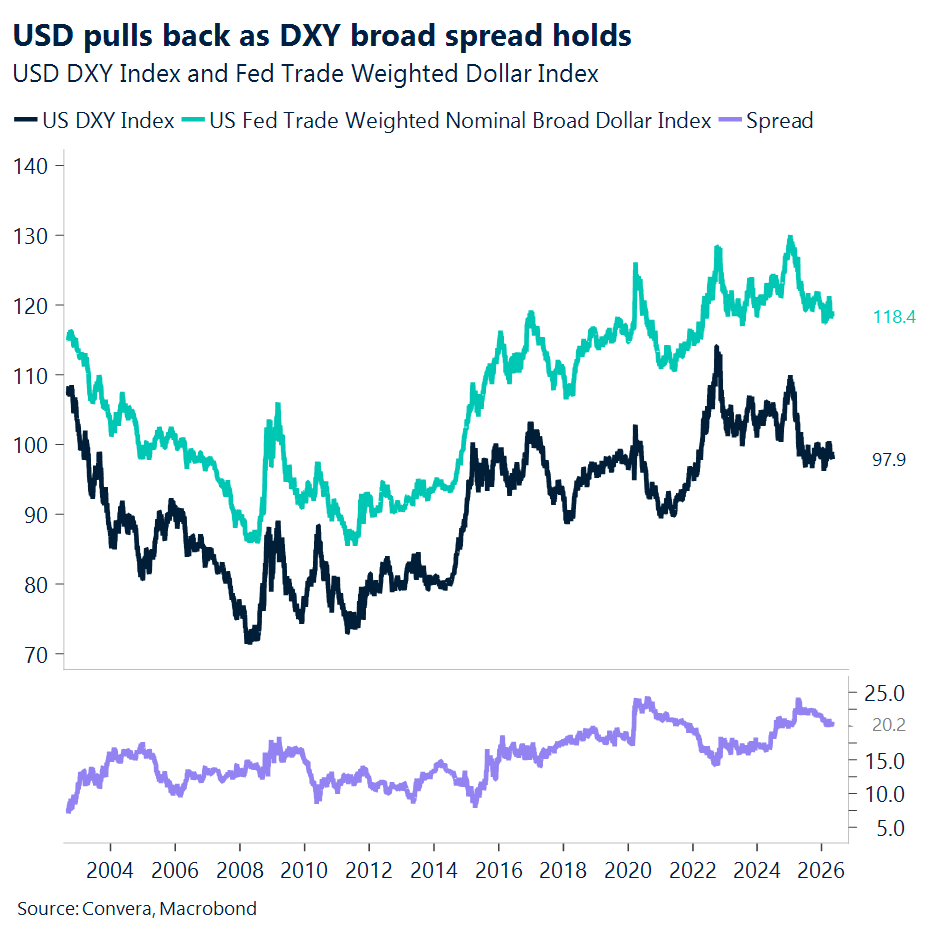

Where the signal sharpens is in the behavior of the dollar itself. Since the ceasefire was confirmed, the USD has slipped about 2%, leaving it modestly lower on the year and still comfortably inside its roughly 11‑month trading range. The key point is not the pullback, but its limits. Even as headline dollar strength has faded, the spread between DXY and the Fed’s broad trade‑weighted dollar has remained slightly elevated, suggesting that USD pressure has eased in the majors without fully unwinding across the broader FX complex.

That mix fits cleanly with the macro backdrop. This week’s US data points to decent, if unspectacular, growth rather than a slowdown, while higher energy prices add a renewed inflation tint. Together, that combination argues against a sustained dollar breakdown. The short‑term impulse has shifted toward modest USD softness as geopolitical stress ebbs, but the medium‑term forces still favour a dollar that stays boxed in, with moves driven by risk pulses rather than a clean new trend.

GBP: Sell‑off on hold?

Sterling has traded relatively calmly into today’s open, despite UK local elections expected to deliver a bruising defeat for the Labour government. Polling stations have closed, with Nigel Farage’s Reform UK racking up sweeping gains in the first counts. That said, a full picture of the results might not come into focus until later today. We are watching GBP/EUR in particular, as the pair has typically been the clearest expression of sterling’s political risk premium.

With the pound widely expected to sell off on the outcome, it is instructive to assess the factors that may temper politically driven bearishness, or at least postpone it. To start, the conflict in the Middle East may have bolstered Starmer’s standing marginally, or at least dampened near‑term calls for his removal given the uncertain geopolitical backdrop. In turn, sterling appears to have lost some of its sensitivity to political drama. The Peter Mandelson scandal is a great case in point, sterling showed to be hypersensitive to it earlier in February to grow indifferent as the issue resurfaced on multiple occasions following the outbreak of the conflict.

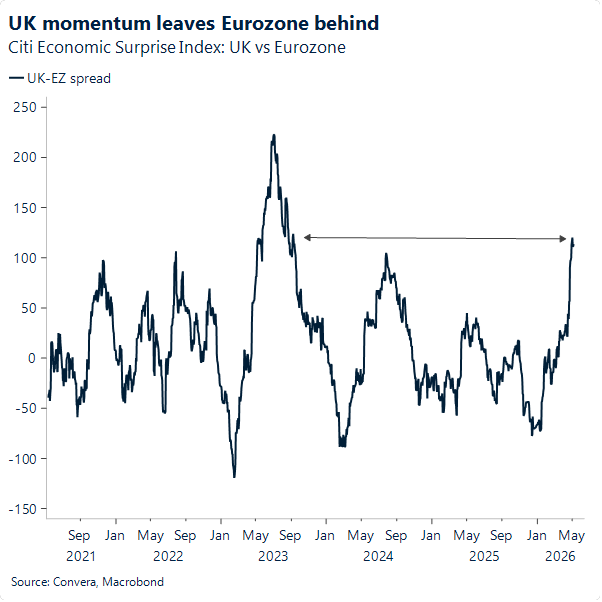

The macro backdrop also plays a role. UK data have surprised to the upside so far this year. With investors focused on the adverse economic implications of the conflict, stronger‑than‑expected domestic momentum has helped offset some of that anxiety. This stands in contrast to the eurozone, which has underperformed on the economic front in 2026. Setting aside political noise, this divergence in growth dynamics may have helped shape the credibility of central banks’ hawkish leanings and, in turn, support for their respective currencies. Should the diverging paths widen further into the year, we see this backdrop as continuing to offer support for the pound.

In addition, in an environment where volatility has eased as markets cling to a de‑escalation narrative in the Middle East, sterling’s carry appeal compares favourably to that of the euro. All things considered, adopting a sustained bearish view on sterling solely on the basis of a largely priced‑in negative election outcome appears unwarranted for now. This backdrop would not however preclude a bearish knee-jerk reaction.

More pronounced downside risks instead lie in the extent to which a poor election result triggers further internal backlash within the party in the months ahead, and how Starmer responds. To this, a deterioration in the macro backdrop – failing to match the strong start to 2026 – would then amplify softer political sentiment and weigh on sterling more forcefully.

EUR: Capped by uncertainty

The euro’s advance against the dollar remains constrained by lingering geopolitical uncertainty, even as de‑escalation hopes resurface intermittently. Confidence in a US–Iran peace outcome remains fragile following fresh US strikes near the Strait of Hormuz, which Washington described as defensive and non‑escalatory. While markets have been willing to fade immediate escalation risks, the persistence of military activity has been enough to cap euro upside and keep risk appetite tentative.

Trade policy has added another layer of uncertainty. President Trump’s decision to set a July 4 deadline for the EU to ratify a trade agreement — alongside renewed tariff threats — has introduced a separate macro risk just as Europe grapples with energy‑driven headwinds. These cross‑currents have limited EUR/USD follow‑through, even as the euro outperformed other European G10 peers yesterday amid a partial unwinding of oil‑related risk premia.

More broadly, the dollar remains supported by relative macro performance. The US economy continues to outperform a eurozone that was already underwhelming this year, and rate differentials have begun to tilt back in USD’s favour. This morning’s German industrial production data reinforces the widening US–euro area divergence. Output fell 0.7% m/m in March, with February revised lower, leaving production in Q1 more than 1% below Q4 2025 levels. The figures underline how German industry is struggling to generate momentum just as the Middle East conflict begins to weigh on energy costs, confidence and investment.

For markets, this strengthens the case that Europe is absorbing the shock less successfully than the US, increasing the risk of downward revisions to first‑quarter growth. In FX terms, softer hard data limits how far relative rate expectations can tilt in the euro’s favour, particularly as questions grow around the ECB’s willingness to tighten into a weakening activity backdrop. For now, EUR/USD appears set to hold above 1.17 this week, but upside toward 1.18 remains conditional on further de‑escalation, whilst 1.20 is growing less likely given growth divergence.

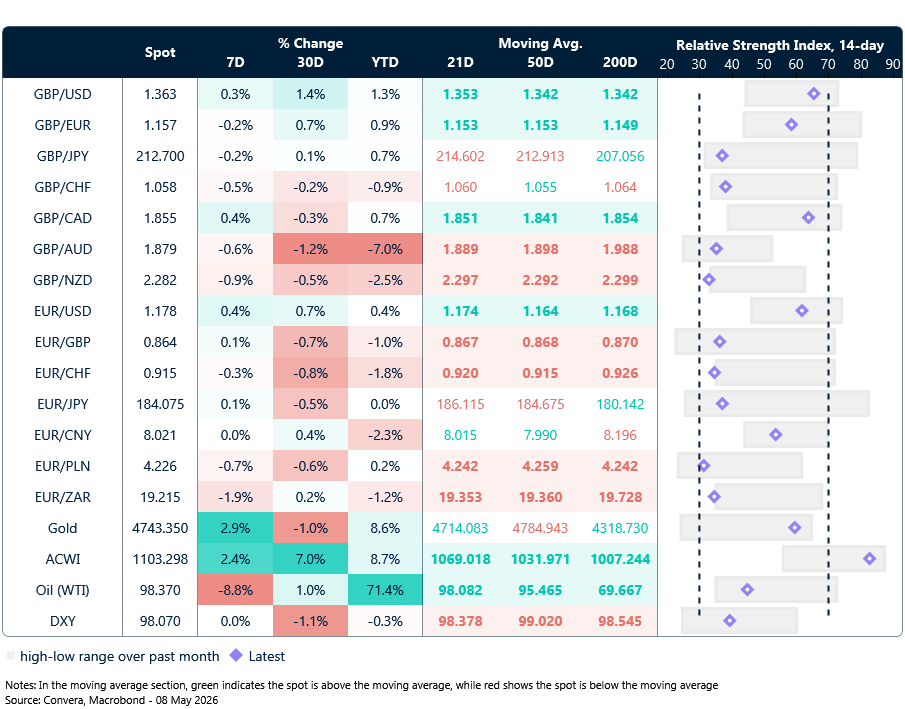

Market snapshot

Table: Currency trends, trading ranges & technical indicators

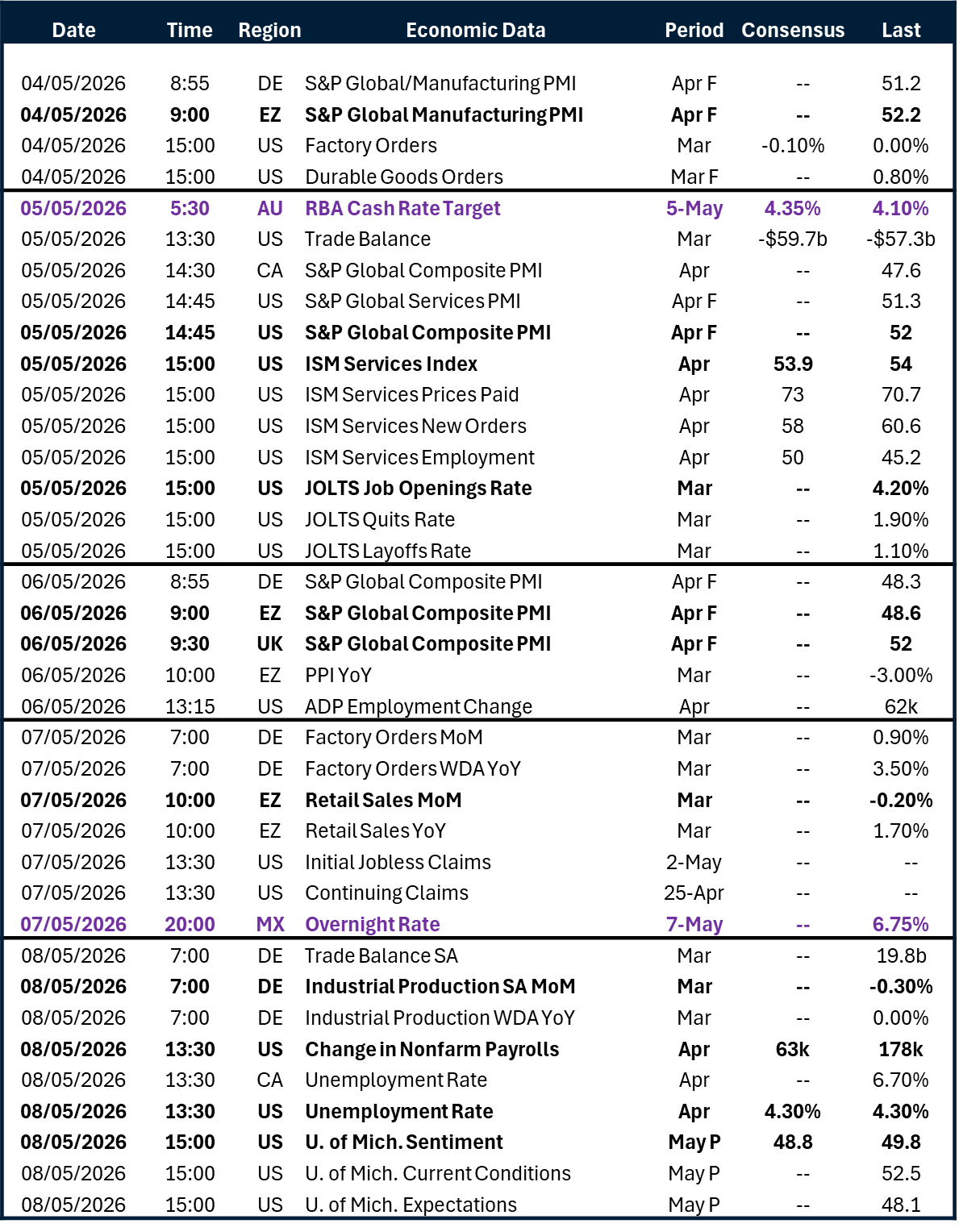

Key global risk events

Calendar: May 04-08

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.