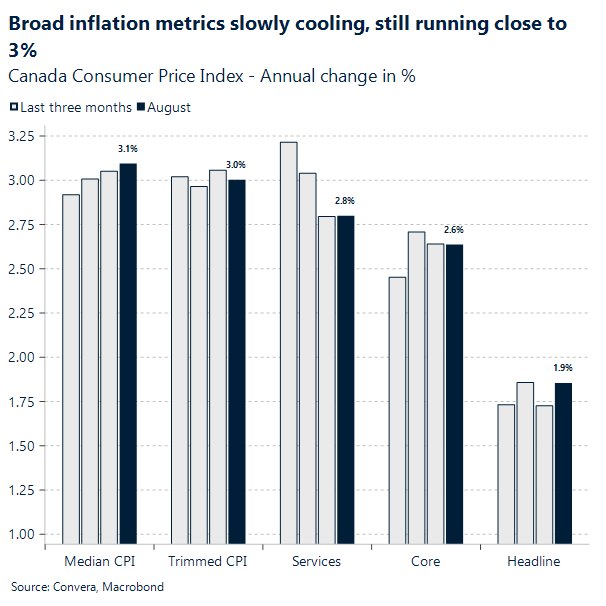

CAD: Inflation mostly in line with expectations, solidifies the case for a rate cut

The August Canadian CPI data paints a mixed but ultimately dovish picture for the Bank of Canada. While the headline inflation rate saw an increase to 1.9% year-over-year, it still came in below the market expectation of 2.0%. This acceleration was primarily driven by a less steep decline in gasoline prices compared to the previous month, rather than broad-based inflationary pressures. The month-over-month CPI actually fell by 0.1%, missing the flat expectation and indicating a slight deflationary movement in the short term. This suggests that the underlying inflationary pressures are moderating, and the headline number is largely an effect of volatile energy prices.

Further analysis of the report’s components reveals a more nuanced economic landscape. The core CPI, which excludes volatile gasoline prices, saw its growth slow slightly to 2.4% after three consecutive months at 2.5%. This reinforces the notion that the core inflationary trend is cooling. While some categories, such as meat and cellular services, saw faster price increases, these were partially offset by price declines in fresh fruit and travel tours. The data, taken as a whole, suggests that inflation is not spiraling out of control and may be on a downward trajectory, giving the Bank of Canada room to consider a more accommodative monetary policy.

This softer-than-expected inflation data has significantly increased the likelihood of a rate cut by the Bank of Canada in tomorrow’s meeting, with market sentiment now pricing in a 90% chance of a cut. In response to this, and on the back of broader U.S. dollar weakness, the USD/CAD exchange rate is trading at 1.376.

USD: Dollar and yields drift lower

Following July’s softer U.S. jobs report, markets have embraced a more upbeat global investment narrative – equities continue to push record highs, and FX carry trades remain in demand (helped further by easing volatility). Investors appear at ease with a 125–150bp Fed easing cycle unfolding without clear signs of recession. The consensus view for further dollar weakness into year-end looks reasonable. However, the cyclical and Fed-driven leg lower in the dollar could face scrutiny later this year if U.S. growth surprises to the upside – a scenario with historical precedent.

The US dollar index has slipped to an almost 2-month trough tracking Treasury yields lower as markets brace for Wednesday’s Fed decision. A 25bp rate cut is fully priced in, with a slim chance of a larger 50bp move following recent signs of labor market cooling. Investors will focus on the Fed’s updated macro projections – especially the rate path – with expectations leaning toward continued easing through year-end.

The vote split will also be closely watched, as a three-way division among FOMC members hasn’t occurred since 2019. Traders are also eyeing whether Stephen Miran’s confirmation as Fed governor will come in time to influence this week’s meeting.

Beyond the Fed decision, key U.S. data releases this week include Tuesday’s August retail sales and Thursday’s jobless claims and July TIC flows. Last week’s spike in claims briefly pressured the dollar, and the TIC data will be closely watched for signs that foreign investors may be moving from hedging to outright selling U.S. assets.

MXN: Super peso on a roll

The Mexican peso, living up to its “super peso” moniker, has hit a new high for 2025. Trading at 18.3 yesterday, a level not seen since July 2024, the currency has been a standout performer. It has added 2% to its impressive 13% year-to-date gains, solidifying its position as a outperformer in Latam and Emerging Market currencies. The most remarkable surge has occurred since “Liberation Day”, with roughly two-thirds of that appreciation, a staggering 8%, happening in just three months. This exceptional resilience is the result of several powerful drivers, including its high-carry attractiveness, a stable macro environment that appeals to global investors, and a broader global appetite for Emerging Market local assets, all of which have solidified its position as a top-performing currency. Overall, the backdrop for risk, along with Fed easing, should also allow the Peso to continue outperforming, beyond our call of 18.5 as a short-term floor. Beyond this, the narrowing of rate differentials with the U.S., shouldn’t be a worry for Banxico as the Fed is poised to cut rates this Wednesday.

CAD: Navigating conflicting signals

The upcoming central bank meetings present a complex dilemma for the CAD as both the Bank of Canada (BoC) and the U.S. Federal Reserve (Fed) are widely expected to cut interest rates. The market’s interpretation of the tone and forward guidance of these cuts will be the primary driver of the USD/CAD.

The BoC faces a consequential decision in its upcoming rate announcement, as it weighs the need to support a weakening economy against the imperative to contain persistent inflationary pressures. Recent data underscores a clear deceleration in economic activity, with GDP contracting by 1.6% in Q2 and early indicators pointing to continued softness in Q3. Labor market conditions have deteriorated, with over 100,000 jobs lost in July and August and the unemployment rate climbing to 7.1%. External risks, including a slowing U.S. economy further compound domestic fragility. The Canadian economy is still navigating the aftermath of trade disruptions, and a rate cut could provide a much-needed boost, particularly given the lagged nature of policy transmission.

However, the case for maintaining the current policy rate remains robust, and it is this side of the argument that creates the BoC’s predicament. The bank is deeply concerned about inflation, which remains a key risk (although latest inflation report has slightly moved down). It needs clearer evidence that price pressures are easing before it can confidently lower rates without risking a surge in inflation. Wage growth continues to exceed the Bank’s inflation target, raising concerns about cost-push inflation. The rise in unemployment may be partially attributable to demographic shifts, such as the influx of temporary residents, which are beyond the scope of monetary policy. Moreover, final domestic demand expanded by 3.4% in Q2, and consumption rose by 4.5%, indicating underlying resilience in interest-sensitive sectors. These figures suggest that headline GDP weakness may overstate the degree of economic slack, and that inflationary risks remain material. The uncertain fiscal outlook and the fact that the full impact of previous rate cuts has yet to be realized further complicate the decision.

In light of these considerations, the BoC will carefully calibrate its response. Whether it opts to hold or ease, the bank’s credibility will hinge on its ability to communicate a coherent strategy that reflects both the complexity of the moment and the limitations of its policy tools.

But then, what does this all mean for the Canadian Dollar?

This is where the Fed comes in, Fed’s own signals. Here’s how the interplay between the two central banks could affect the CAD:

Scenario 1: BoC “Dovish” Cut vs. Fed “Hawkish” Cut

• BoC Action: The BoC cuts its policy rate and the statement and press conference are “dovish,” signaling a clear path for further easing. The bank’s communication would emphasize the need to support the Canadian economy and would suggest that this is the beginning of a broader easing cycle.

• Fed Action: The Fed also cuts its policy rate, as expected. However, the tone is interpreted as a “hawkish cut.” This would be a surprise to the market, which has priced in a series of Fed cuts. This “hawkish cut” would mean the Fed downplays the need for further cuts and emphasizes that they are not committing to a full-blown easing cycle.

• CAD Outlook: This is a bearish scenario for the Canadian dollar. Both central banks are cutting, but the BoC’s dovish tone makes the CAD relatively less attractive. The Fed’s hawkish cut makes the USD strengthen as it suggests the U.S. is not on a sustained path of monetary easing. The USD/CAD pair would likely move upward, potentially rising toward or above 1.383.

Scenario 2: BoC “Hawkish” Cut vs. Fed “Dovish” Cut

• BoC Action: The BoC cuts its policy rate, but the statement is surprisingly “hawkish.” The BoC would likely emphasize the persistent inflation pressures and the resilience of the Canadian economy, suggesting that this cut is a one-off measure and that the bank is prepared to pause.

• Fed Action: The Fed cuts its policy rate, and the statement is “dovish.” The Fed would stress the need to support the U.S. economy and signal a clear commitment to a full easing cycle.

• CAD Outlook: This would be a very bullish scenario for the Canadian dollar. The BoC’s hawkish cut would be a positive surprise for the CAD, as it suggests less room for further easing in Canada. This would be coupled with the Fed’s dovish cut, which would soften the USD. The USD/CAD pair would likely move sharply downward, potentially breaking below 1.37, as the interest rate differential narrows in favor of the CAD.

The two scenarios where both central banks deliver “dovish” cuts or “hawkish” cuts are unlikely to trigger a definitive breakout for the USD/CAD. Instead, they will most likely keep the pair confined to its recent summer trading range. The real question is whether this Wednesday’s confluence of central bank decisions will provide the necessary catalyst for a significant directional move beyond that range. The answer lies not in the rate cuts, which are largely priced in, but in the narrative and the forward guidance. Time will tell if the communication from either the Bank of Canada or the Federal Reserve is strong enough to finally break the summer-long impasse.

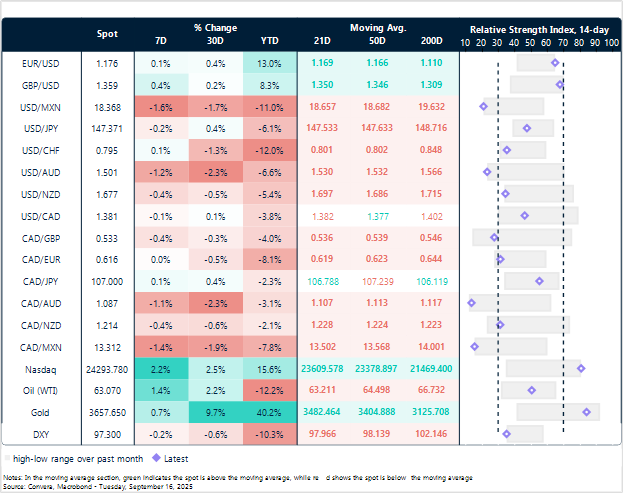

Broad based dollar weakness

Table: Currency trends, trading ranges and technical indicators

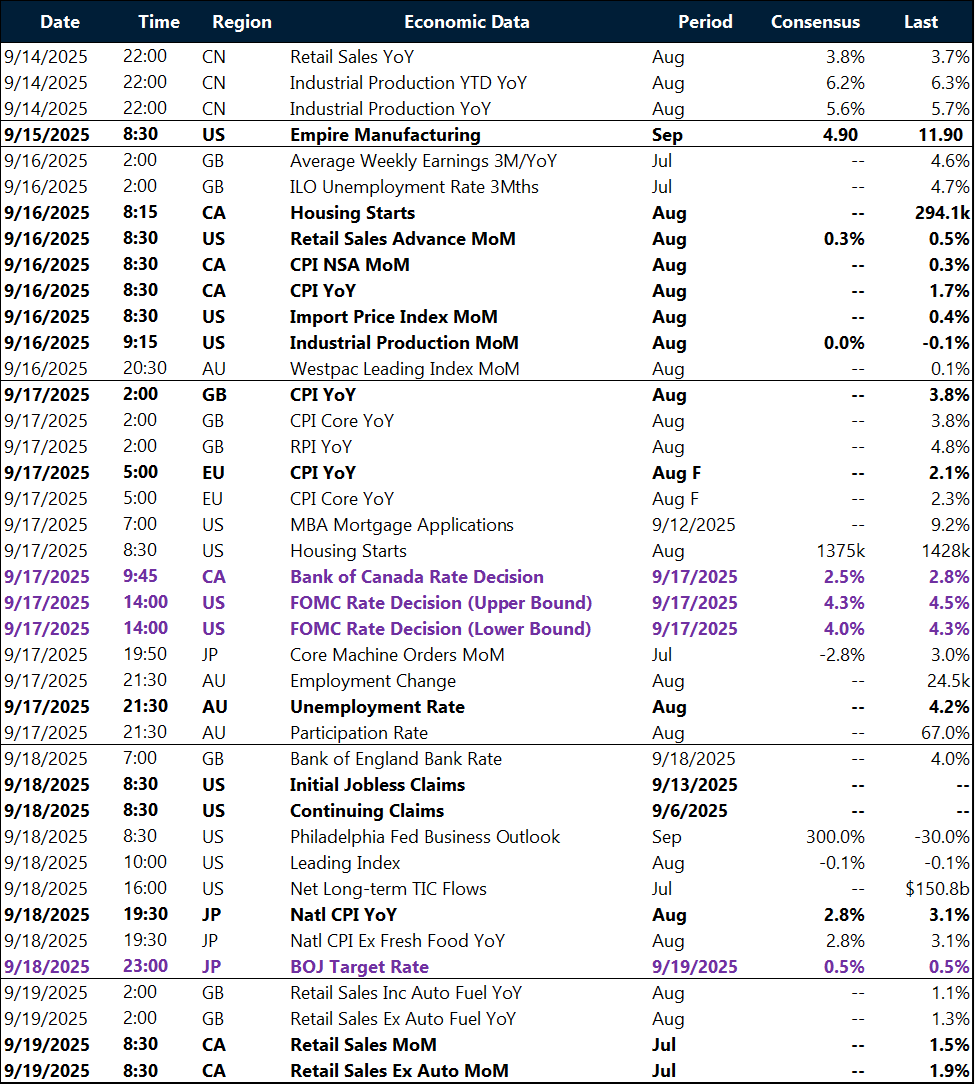

Key global risk events

Calendar: September 15-19

All times are in EST.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.