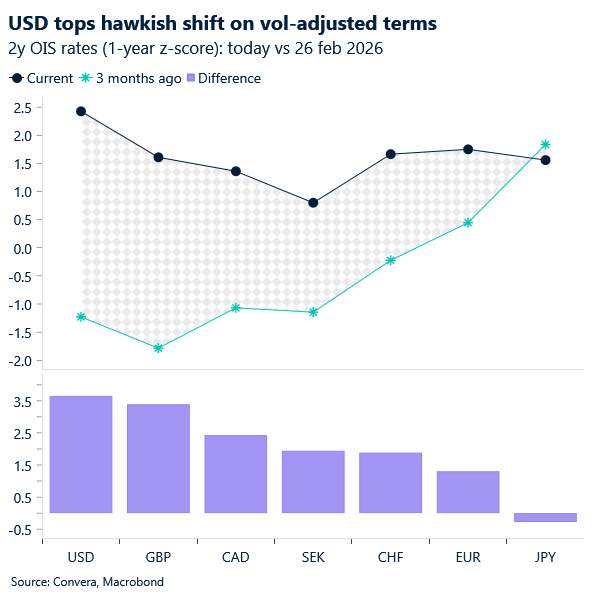

USD: Dollar range-bound as narratives struggle to advance

The Dollar Index – the DXY – has failed to reclaim the 99.400 mark since mid-May, as markets appear increasingly willing to look through bouts of re-escalation – Monday night’s US-Israeli strikes being the latest example – while continuing to cling to the de-escalation story. Meanwhile, the US dollar is becoming more responsive to the growth and rates narrative. This week’s bull steepening – with the front end of the curve falling more than the long end – following some unwinding of Friday’s sharpest Fed hawkish repricing since early 2025, may have contributed to the greenback’s paralysed posture.

That said, the move still feels more positioning-driven than fundamentally warranted. While markets are leaning on the de-escalation narrative, a more sustained unwind likely requires more concrete progress on peace. This is especially true as markets increasingly shift their focus to the macro and policy implications of the conflict, which makes any unwind in the dollar/Treasuries dynamic inherently stickier in the near term. It is useful reminder that both the April CPI and PPI reports came in above expectations, and that markets priced in one full 25bp rate hike on Friday. Against this backdrop, we struggle to see the DXY breaking decisively below the 98 handle just yet.

A more forceful bullish impulse also appears unlikely in the near term either, given the lingering de-escalation narrative, coupled with the still relatively homogeneous “tough talk” from G10 central banks that masks a more dovish-leaning macro backdrop (see eurozone).

Instead, more subdued DXY price action in the lower 99 range appears more likely, as markets await more tangible progress from the de-escalation narrative.

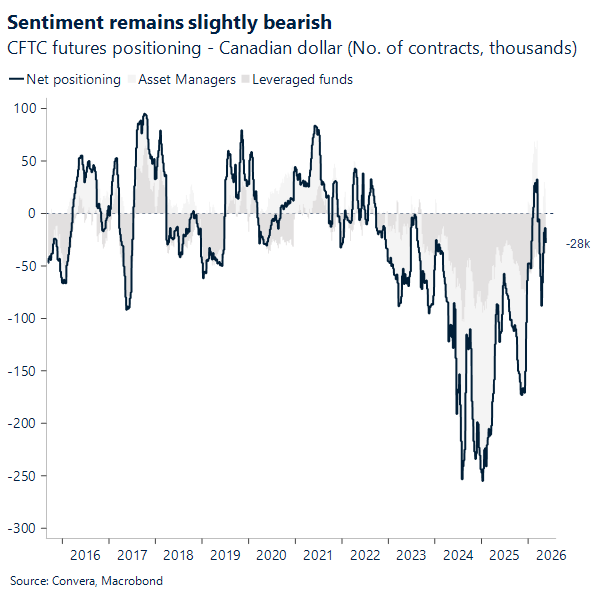

CAD: Stays on the defensive

The Canadian dollar still looks fragile, with the short end of the rates market doing most of the work against it. The US–Canada 2-year government yield spread is now sitting around 129bp in favour of the US based on the latest official benchmarks, keeping the carry backdrop tilted toward USD demand and leaving USD/CAD supported near the top of its recent range. That widening has been reinforced by a familiar policy mix: hotter US inflation has kept markets leaning toward a “higher-for-longer” Fed, while Canada’s latest inflation mix was softer beneath the surface, with core inflation easing to 2.1% in April even as headline CPI rose on energy. In other words, Canada has not yet delivered the kind of domestic macro surprise needed to offset the US yield advantage, and as long as that relative-rate imbalance holds, the Loonie remains vulnerable.

The other problem for CAD is that one of its recent supports may be fading. Canada’s trade balance swung back to a C$1.8bn surplus in March, but that improvement was driven heavily by a rebound in gold shipments and energy exports, with goods exports up 8.5% m/m, metal and non-metallic mineral exports up 24.0%, and energy exports up 15.6%. That is constructive at the headline level, but the details matter: much of the strength came through nominal prices rather than stronger real export momentum, with official data showing export volumes actually edged lower in March. Since then, both oil and gold have come off their recent highs, which reduces the terms-of-trade support that helped the Loonie stabilize earlier in the month and makes March’s trade bounce harder to extrapolate forward.

There is also some domestic noise in the background that does not help sentiment. Alberta is now heading toward an October 19, 2026 non-binding referendum question on whether the province should begin the constitutional path toward a future binding separation vote, and while that is not yet a core macro driver, it does inject an additional layer of political risk premium into CAD at the margin. That matters more because broader positioning is not offering much of a cushion: sentiment still slightly bearish, with net CAD futures positioning around -28k contracts, and the latest CFTC data remain consistent with that picture, showing leveraged funds net short CAD while asset managers are only modestly net long. Taken together, a wide front-end rate gap, softer oil and gold, Alberta headline risk, the still-cautious futures positioning and the CUSMA deal review just around the corner, the balance of risks continues to argue for a Canadian dollar that stays defensively biased in the near term.

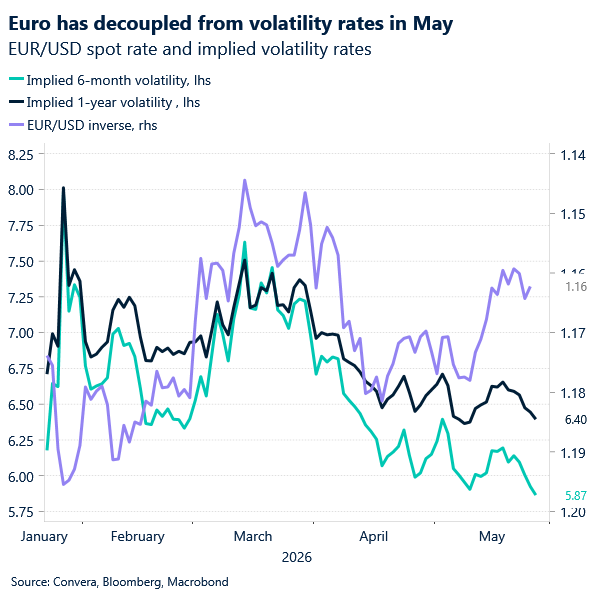

EUR: Losing carry in a low-vol world

EUR/USD continues to trade in a narrow 1.16–1.18 range, with price action increasingly subdued as FX volatility grinds lower. Despite ongoing uncertainty surrounding the Middle East, markets have become notably desensitised to conflicting headlines, with geopolitical developments generating diminishing marginal impact on the currency pair.

This low‑volatility backdrop has important implications for positioning. In an environment where directional conviction is limited, carry considerations tend to dominate, and here the euro is losing ground. While the single currency briefly benefited from a relatively attractive rate profile earlier in the spring, that support has eroded. Market pricing for ECB tightening has been scaled back meaningfully, with expectations falling from around 85bp at end‑April to closer to 55bp currently.

At the same time, the macro picture has softened. Euro‑area data surprises have deteriorated sharply relative to the US, reinforcing a widening growth and policy divergence. Real yield differentials have moved back in the dollar’s favour, and underlying economic momentum remains more resilient in the US than in the eurozone.

What is notable, however, is that EUR/USD has yet to fully reflect this shift. The dominant pro‑risk market narrative – characterised by firm equities and compressed volatility -continues to suppress broader dollar strength, allowing the euro to hold its ground despite weaker fundamentals. This creates a growing disconnect. Rates and growth differentials point to euro downside, but the risk‑supportive environment is preventing a more decisive move.

For now, EUR/USD remains range‑bound. But as carry regains importance and macro divergence persists, the balance of risks is gradually tilting lower, even if the adjustment remains slow in a compressed volatility regime.

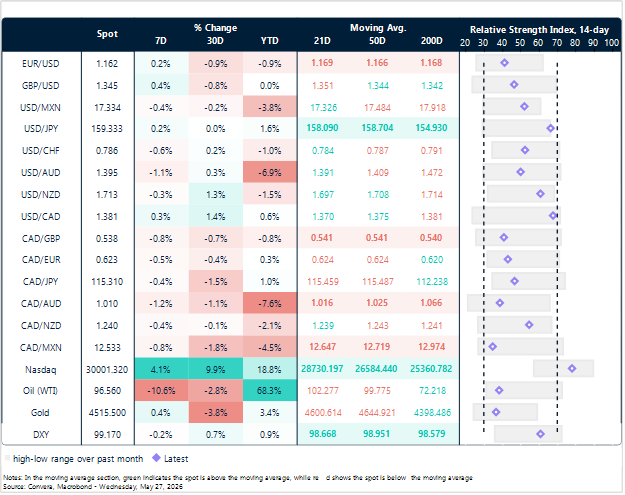

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

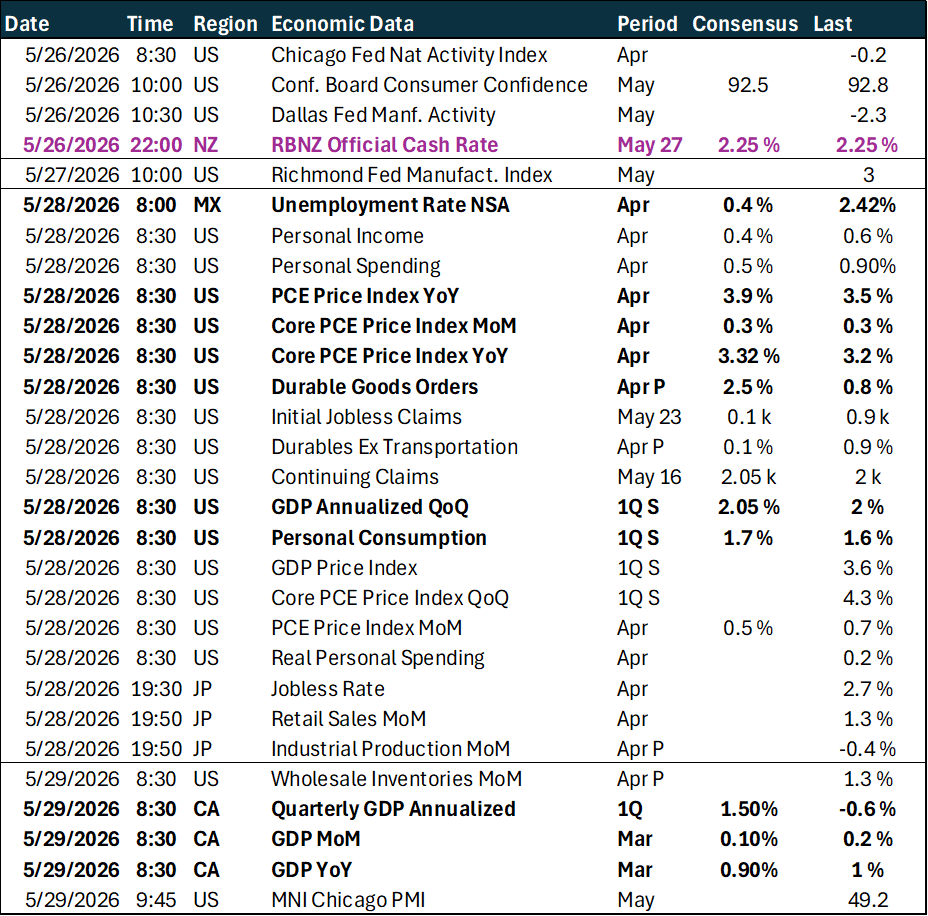

Calendar: May 25 – 29

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.