Dollar ends week slightly lower on softer Fed pricing

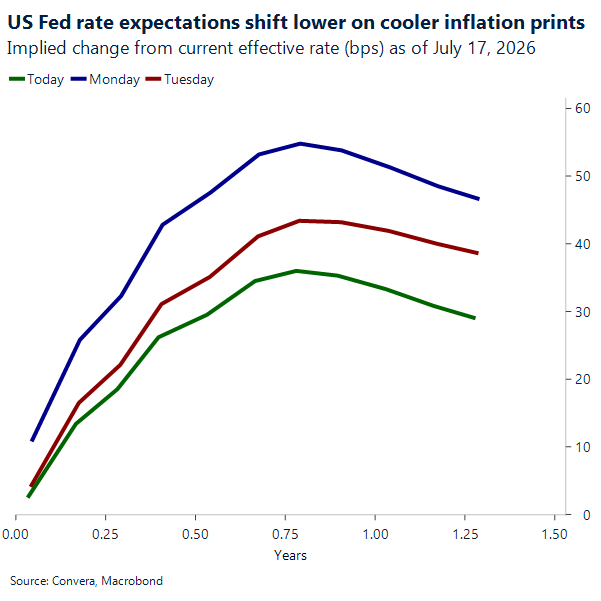

The US Dollar is ending lower the week after CPI and PPI both came in softer than expected, pushing markets to scale back near-term Fed hike risk. Headline CPI fell 0.4% in June, while PPI followed with a 0.3% monthly decline against expectations for a flat reading. Final-demand PPI slowed to 5.5% year over year, below the 6.2% consensus, while core PPI excluding food, energy and trade rose just 0.1% on the month. One print doesn’t make a trend, but two softer inflation reports have made it harder for markets to keep pricing a more hawkish Fed path.

Fed rate expectations have moved lower across the curve compared with earlier in the week, as cooler inflation reduced the urgency for additional tightening. Still, markets have not been given a clean green light to price early easing. Fed Chairman Kevin Warsh has pushed back against any “mission accomplished” reading of the inflation data, reminding investors that inflation remains above the Fed’s 2% target. That has helped Treasury yields pare some of their early week declines and kept the Dollar from breaking down more decisively.

For the Dollar, the week’s data shifted the short-term balance lower without fully changing the broader backdrop. Softer inflation and lower front-end yields reduce the appeal of chasing the Dollar on rate support. At the same time, stronger retail sales and Warsh’s cautious tone suggest the Fed can stay on hold. Markets have repriced July-end meeting, easing fears of near-term Fed risk. The Dollar remains vulnerable if inflation keeps surprising lower, but the bar for a deeper selloff remains higher.

The main short-term risk now sits outside the data calendar. Middle East tensions have pushed oil prices higher again, with reports that Iran may pressure the Houthis to disrupt Red Sea oil routes if the US expands strikes. A renewed energy shock could revive inflation concerns and make markets more careful about leaning too dovish on the Fed. Risk aversion in equities could also put a defensive bid back under the Dollar, especially if investors rotate toward safety. For now, softer inflation is weighing on the greenback, but geopolitics and Fed caution should limit how far that move can run.

USD/CAD rally loses momentum

USD/CAD has lost momentum as softer US inflation has taken some heat out of the Dollar. Weaker CPI and PPI prints eased the recent rise in US yields and reduced near-term Fed hike pressure, pulling the pair back toward 1.4050 after a sharp run higher. The move looks more like a repricing of near-term Fed risk than a full reversal in the broader Dollar backdrop. Firmer oil prices have also helped the loonie at the margin, but the US rates story remains the main driver for USD/CAD.

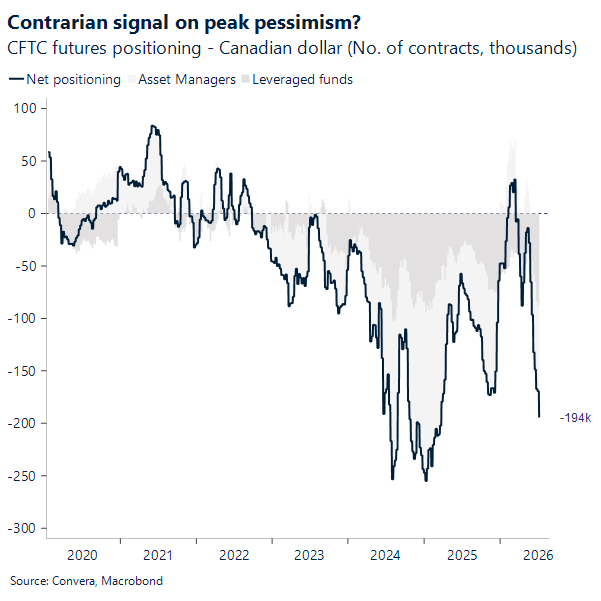

Canada’s domestic backdrop has also stopped deteriorating. The Bank of Canada held rates at 2.25%, as expected, and pointed to signs of improvement, with growth picking up and inflation expected to cool gradually after its recent spike. Manufacturing sales added another firmer data point, rising 1.3% m/m to a record C$78.1bn in May, beating expectations and extending the recovery in factory activity. Still, positioning remains a risk, with net Canadian-dollar exposure near -194k contracts, showing that sentiment toward CAD is still heavily stretched.

The daily chart shows USD/CAD pulling back from its June highs and trading near 1.4050. The pair has slipped below the 20-day moving average at 1.416, confirming that upside pressure has eased, though spot remains above the 50-day near 1.397 and the 100-day and 200-day near 1.3850. The next key test is the 1.4000–1.3978 zone. A break below that area would likely need more follow-through from the US disinflation story and another leg lower in US yields.

Next week’s Canadian data could help shape the next move. June CPI lands Monday, with markets looking for inflation to ease to 3.1% y/y from 3.2%. Retail sales follow Thursday and will offer a cleaner read on household demand. For now, USD/CAD remains caught between a softer US inflation impulse, a steadier Canadian backdrop and still-wide yield differentials.

Carry support meets growing complacency

After the pound rose more than 1% against the US dollar on Wednesday, its largest daily gain since March, GBP/USD has slipped back below 1.35 and remains under modest pressure. The move reflects a deterioration in risk sentiment as geopolitical tensions re-emerge. With the US-Iran conflict still simmering and President Trump stepping up criticism of China, investors are becoming more cautious, allowing traditional risk-off dynamics to regain influence over FX markets.

Sterling has nevertheless enjoyed a supportive backdrop in recent weeks. Reduced UK fiscal concerns following expectations of a Shabana Mahmood appointment as Chancellor, stronger-than-expected UK data and, most importantly, an exceptionally benign volatility environment have all worked in the pound’s favour. Carry trades have benefited from low FX volatility and the hawkish Bank of England pricing makes sterling one of the more attractive high-yielding currencies in the G10.

However, there are signs that a considerable amount of good news is already reflected in sterling. Three-month sterling volatility has fallen to around 6%, a level that appears complacent given Andy Burnham’s imminent arrival in Downing Street and the unresolved fiscal questions facing any new administration. While investors are increasingly comfortable that the next government may prove more fiscally disciplined than initially feared, the UK’s structural fiscal challenges have not disappeared.

Against the euro, the pound has also pulled back from more than one-year highs. We flagged the overbought conditions earlier this week, but we’re also conscious that GBP/EUR looks stretched relative to front-end rate differentials, suggesting upside may become harder to sustain from current levels.

Overall, sterling appears supported by carry and positioning dynamics but increasingly vulnerable to any pickup in volatility, geopolitical risks or renewed scrutiny of the UK’s fiscal trajectory. Next week brings a dense UK data calendar, including labour market figures, inflation, retail sales and flash PMIs, which should provide a timely test of whether the recent improvement in sentiment towards UK assets can be justified by underlying fundamentals.

Market snapshot

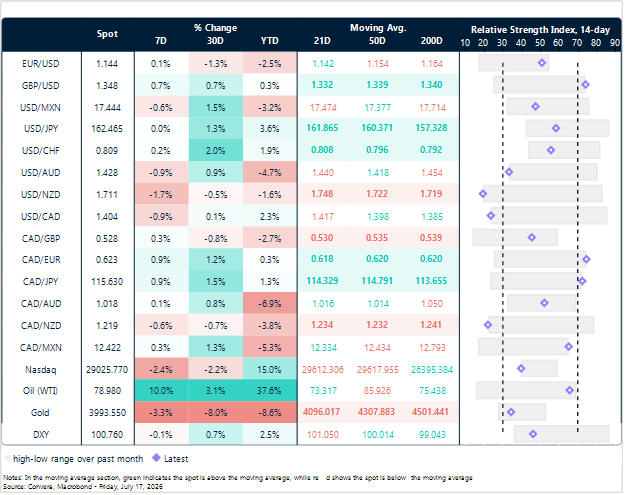

Table: Currency trends, trading ranges & technical indicators

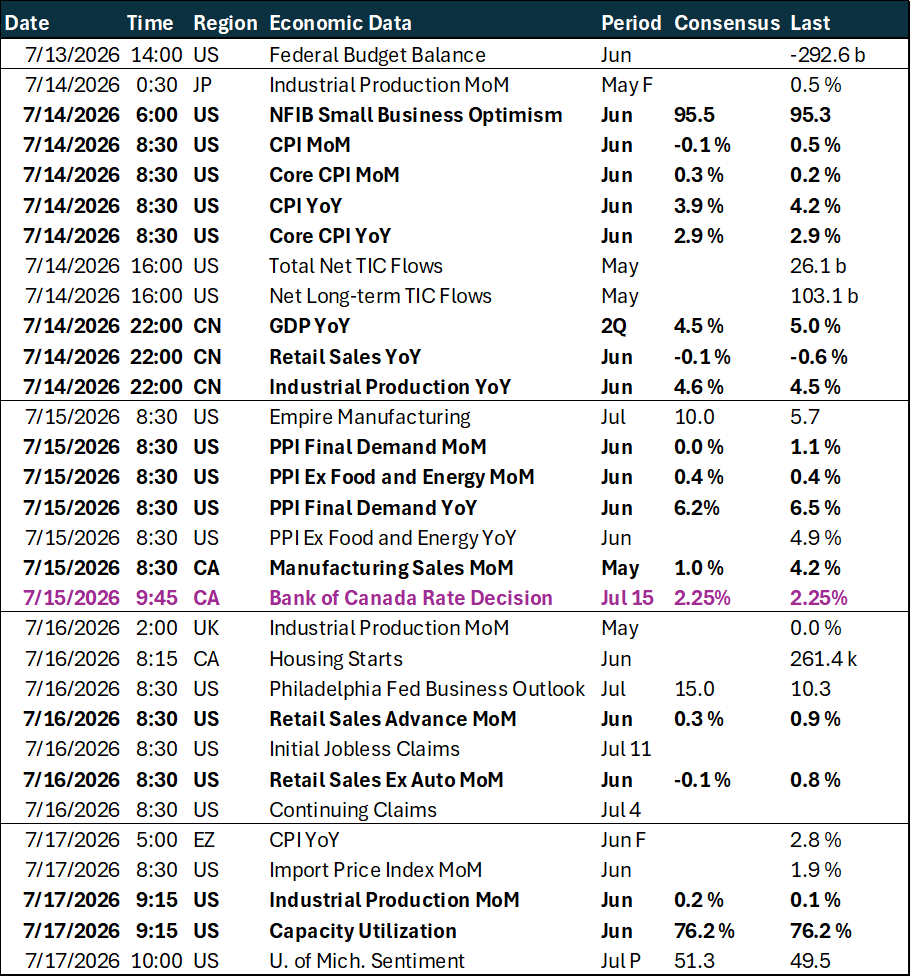

Key global risk events

Calendar: July 13 – 17

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.