USD: No panic, no dollar surge

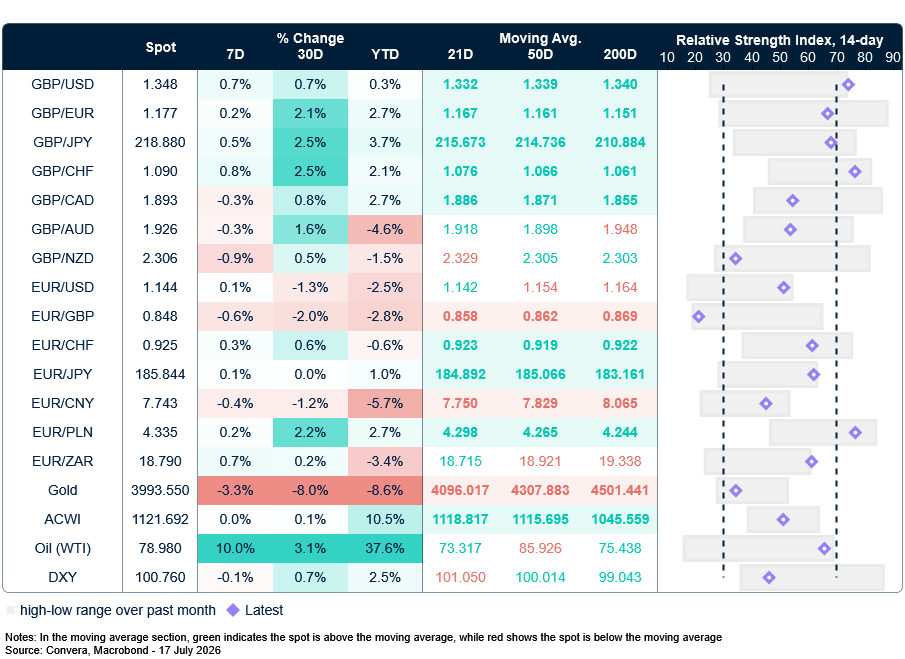

The US dollar Index has been drifting lower since its 24 June high of 101.800, with the move gathering pace following a series of softer-than-expected inflation prints. DXY has now broken below its 21-day moving average near 101.000, although the broader trend remains constructive relative to the lows seen in early May. Support around 100.20/10 remains a key area to watch.

Despite the US and Iran showing no intention of pausing hostilities in the region, markets have so far refrained from entering full panic mode. The VIX index remains relatively subdued compared with the levels reached in March and June, limiting the extent to which safe-haven demand has flowed into the greenback.

Meanwhile, a hawkish Fed undertone continues to simmer. Markets remain priced for one additional rate hike this year, while Kevin Warsh has cautioned against placing too much weight on individual inflation prints when assessing the broader inflation outlook.

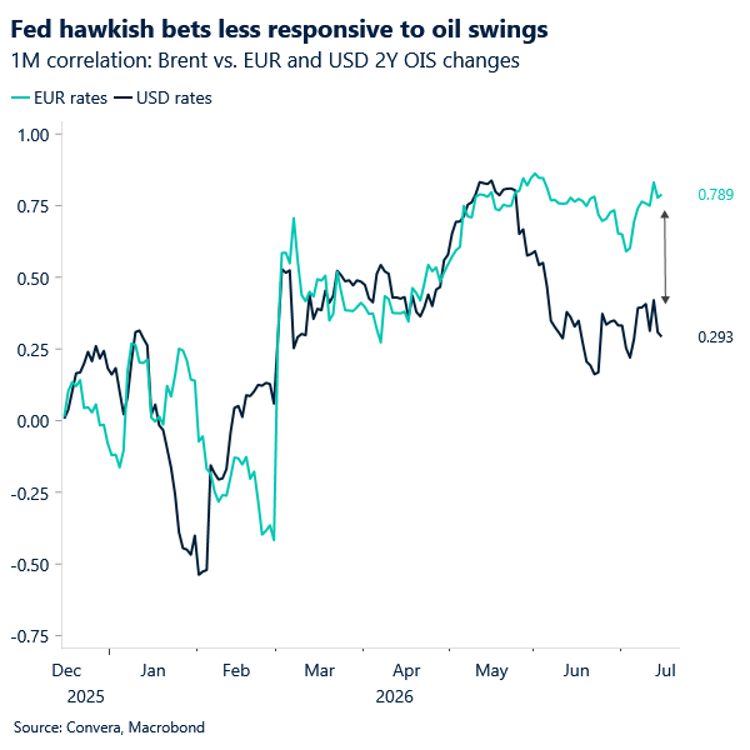

At the same time, a hawkish repricing “catch-up” in other G10 rate markets following the latest geopolitical re-escalation, particularly in EUR rates, also helped temper bullish momentum in the dollar. These markets continue to display greater sensitivity to oil price swings, reflecting both their higher exposure to imported energy inflation and a softer underlying macro backdrop. With domestic growth offering less justification for a sustained hawkish stance, fluctuations in energy prices play a larger role in shaping rate expectations, amplifying both dovish repricing when oil falls and hawkish repricing when it rises.

With the Fed entering its communications blackout period this Saturday and little hawkish impetus from Warsh, Fed-related support for the dollar is likely to remain limited in the coming days. Absent a more prolonged escalation in the Middle East, we expect DXY to trade largely directionless within the 100-101 range ahead of the 29 July Fed meeting.

EUR: A delicate balance for the common currency

We doubt EUR/USD will develop much directional conviction in the coming days, with both the ECB and Fed entering their communications blackout periods. The main downside risk stems from a further rise in oil prices driven by the US-Iran standoff, which would worsen the eurozone’s terms of trade by increasing the cost of energy imports relative to export prices.

The bigger downside amplifier, however, is risk sentiment. So far, market anxiety has remained surprisingly contained despite the latest geopolitical re-escalation. As we’ve noted before, the euro tends to exhibit greater risk sensitivity when geopolitical tensions flare, as investors become increasingly mindful of growth risks linked to Europe’s still-fresh memory of the 2022 energy shock.

Over the next couple of weeks, the euro is likely to walk a fine line. Elevated oil prices could help maintain a hawkish floor under ECB expectations and lend support to the currency. At the same time, a broader shift into risk-off positioning would likely outweigh that support and erode the euro’s appeal.

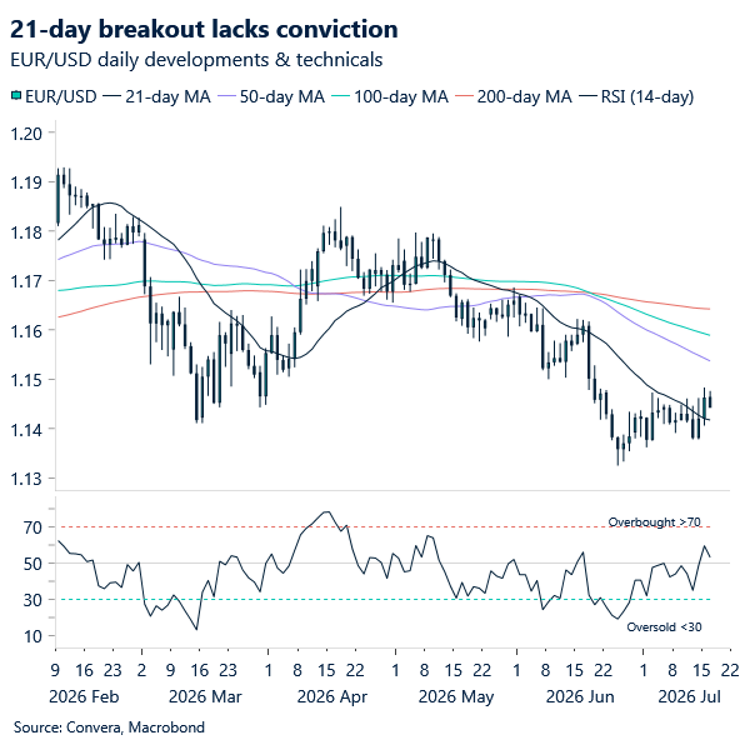

Absent a more prolonged geopolitical escalation, consolidation around the 1.14 handle appears the most likely outcome ahead of the month-end slate of central bank meetings.

GBP: Carry support meets growing complacency

After the pound rose more than 1% against the US dollar on Wednesday, its largest daily gain since March, GBP/USD has slipped back below 1.35 and remains under modest pressure. The move reflects a deterioration in risk sentiment as geopolitical tensions re-emerge. With the US-Iran conflict still simmering and President Trump stepping up criticism of China, investors are becoming more cautious, allowing traditional risk-off dynamics to regain influence over FX markets.

Sterling has nevertheless enjoyed a supportive backdrop in recent weeks. Reduced UK fiscal concerns following expectations of a Shabana Mahmood appointment as Chancellor, stronger-than-expected UK data and, most importantly, an exceptionally benign volatility environment have all worked in the pound’s favour. Carry trades have benefited from low FX volatility and the hawkish Bank of England pricing makes sterling one of the more attractive high-yielding currencies in the G10.

However, there are signs that a considerable amount of good news is already reflected in sterling. Three-month sterling volatility has fallen to around 6%, a level that appears complacent given Andy Burnham’s imminent arrival in Downing Street and the unresolved fiscal questions facing any new administration. While investors are increasingly comfortable that the next government may prove more fiscally disciplined than initially feared, the UK’s structural fiscal challenges have not disappeared.

Against the euro, the pound has also pulled back from more than one-year highs. We flagged the overbought conditions earlier this week, but we’re also conscious that GBP/EUR looks stretched relative to front-end rate differentials, suggesting upside may become harder to sustain from current levels.

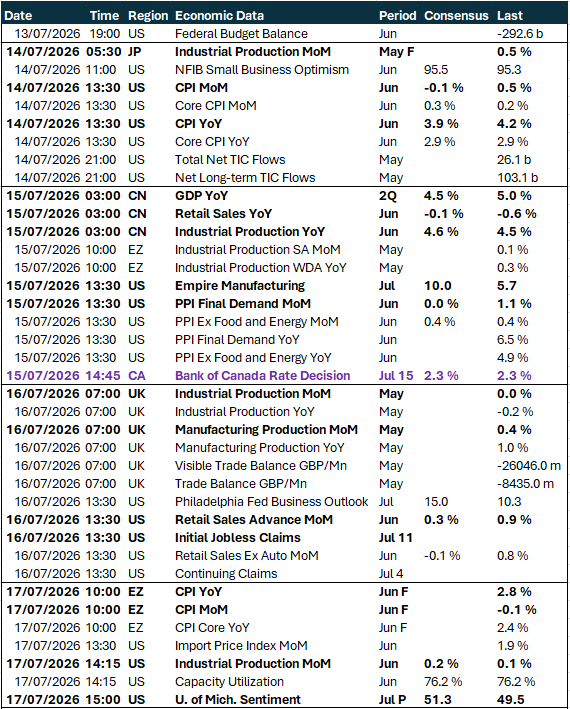

Overall, sterling appears supported by carry and positioning dynamics but increasingly vulnerable to any pickup in volatility, geopolitical risks or renewed scrutiny of the UK’s fiscal trajectory. Next week brings a dense UK data calendar, including labour market figures, inflation, retail sales and flash PMIs, which should provide a timely test of whether the recent improvement in sentiment towards UK assets can be justified by underlying fundamentals.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: July 13-17

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.