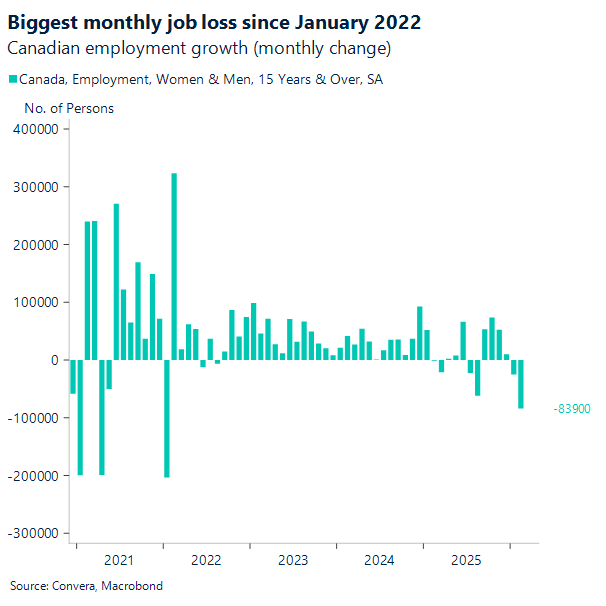

CAD: Steepest job loss since 2022

The latest report reveals a staggering loss of 84,000 jobs, a figure that drastically missed the surveyed expectation of a 10,000-job gain. This is the steepest monthly job loss since January 2022. This contraction was fueled by a massive decline of 108,400 full-time positions, which a modest increase of 24,500 part-time roles could not offset. Consequently, the national unemployment rate climbed to 6.7%. The CAD has moved up from 1.366 to 1.37 as the conflict drags on, and the latest employment report doesn’t help for a Lower loonie case once a conflict premium is removed; for now, oil dictates and helps cushion the macro softness. This geopolitical support remains the primary shield for the Canadian dollar, even as the domestic labor market shows significant signs of distress.

Beyond the headline numbers, the internal dynamics of the report highlight a broadening weakness across various sectors and provinces. The private sector bore the brunt of the downturn with 73,000 lost positions, while regional data showed a sharp 57,000-job decline in Quebec and a 20,000-job drop in British Columbia. Despite this overall softening, average hourly wages for permanent employees unexpectedly surged to 4.2%, well above the 3.2% forecast. This persistent wage pressure creates a challenging environment for the Bank of Canada, as it must weigh inflationary labor costs against a rapidly deteriorating employment landscape. Furthermore, the participation rate dipped to 64.9%, suggesting that the labor force is shrinking just as the employment rate falls to its lowest levels in months.

The demographic breakdown of the report underscores a particularly harsh reality for younger and racialized Canadians. Youth unemployment rose sharply to 14.1% in February, but the disparities among specific groups are even more pronounced. For instance, the unemployment rate for Black youth reached a staggering 23.2%, while Chinese and South Asian youth faced rates of 17.4% and 13.0%, respectively. These figures stand in stark contrast to the 11.2% rate for non-racialized youth, illustrating a stratified labor market where certain groups are disproportionately affected by the current macro softness. As long-term unemployment remains elevated, these structural vulnerabilities will likely persist, leaving the Canadian economy and the loonie highly exposed once the temporary support of high oil prices and conflict-driven premiums inevitably fades.

US macro data: DXY hits peaks despite weak data

The recent influx of US economic data presents a cooling narrative, even if the headline inflation figures suggest a measure of price stability. While the January PCE price index landed essentially in line with expectations at 2.8% year-over-year, the broader suite of indicators suggests a sharper internal slowdown than many anticipated. Most notably, the second revision for 4Q GDP growth plummeted to a mere 0.7%, arriving far below the 1.4% consensus as consumption, capex, and net exports were all adjusted lower. This significant “whiff” in growth, compounded by stagnant durable goods orders, provides substantial ammunition for Fed doves who argue that the domestic economy is finally buckling under the weight of restrictive policy.

Despite these clear signs of domestic fatigue, the US Dollar Index (DXY) has surged to its highest level since last November, firmly reclaiming and surpassing the 100 barrier. Under normal conditions, such a broad miss in GDP and manufacturing data would trigger a sharp retreat in the greenback as traders move to price in a more accommodative Federal Reserve. However, the current currency strength is being fueled by geopolitical pressures rather than internal economic vigor. The escalating situation in Iran and the subsequent volatility in the energy markets have maintained a firm floor under the dollar. Consequently, investors are prioritizing the greenback’s role as a safe haven, allowing it to maintain its momentum even as the underlying economic data begins to sour.

Moving forward, the market remains caught in a high-stakes tug-of-war between lackluster domestic fundamentals and a precarious global risk environment. While the weak January data may temporarily cap the DXY’s upward trajectory by curbing aggressive interest rate expectations, the “conflict premium” remains a potent force that is difficult to ignore. Some optimists might still argue for a first-quarter snapback to justify these elevated dollar levels, yet the broad-based downward revisions in spending and shipments suggest the path ahead is fraught with more friction than previously estimated. Ultimately, until the energy market stabilizes or the tensions in the Middle East cool, the dollar’s dominance will likely persist.

No relief

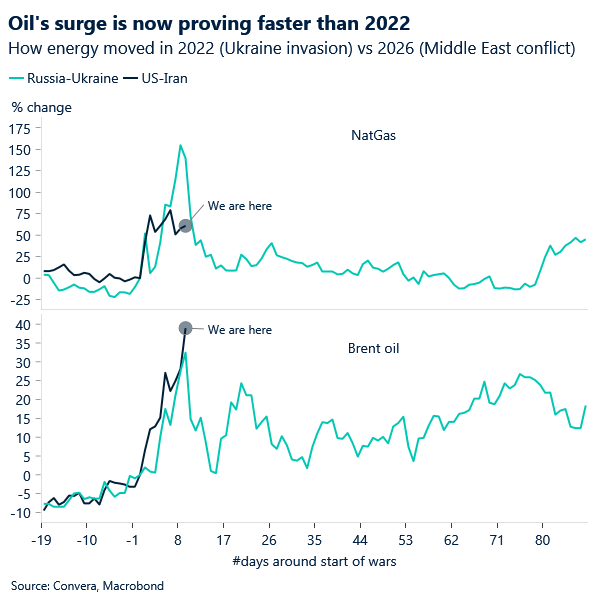

Markets have been whipsawed by conflicting US signals over the likely duration of the conflict — one day hinting at rapid de‑escalation, the next warning of a prolonged campaign — leaving risk appetite fragile and volatility deeply embedded in the headlines. The latest escalation – Iran’s new supreme leader pledged to keep the Strait of Hormuz effectively shut, with US President Trump also striking a defiant tone.

The reported mining of the Strait of Hormuz is also unnerving investors. This is a material threat to an energy system already running a structural shortfall, thus crude oil closed above $100 for the first time since 2022 yesterday.

The IEA’s coordinated release of 400 million barrels briefly steadied nerves earlier in the week, but it’s a band‑aid on a far larger wound: some 18 million barrels a day, nearly a fifth of global supply, should be flowing through Hormuz. Ultimately, the only variable that really matters now is duration — how long the disruption lasts and how deeply it impairs physical energy flows. That’s why terms of trade has snapped back into the FX driving seat, dictating currency performance far more forcefully than rate expectations or traditional macro signals.

Oxford Economics warns that if global oil prices were to average around $140 per barrel for even two months, the combination of tighter financial conditions, renewed supply‑chain stress and a deterioration in business and consumer sentiment would be enough to tip parts of the global economy into a mild recession.

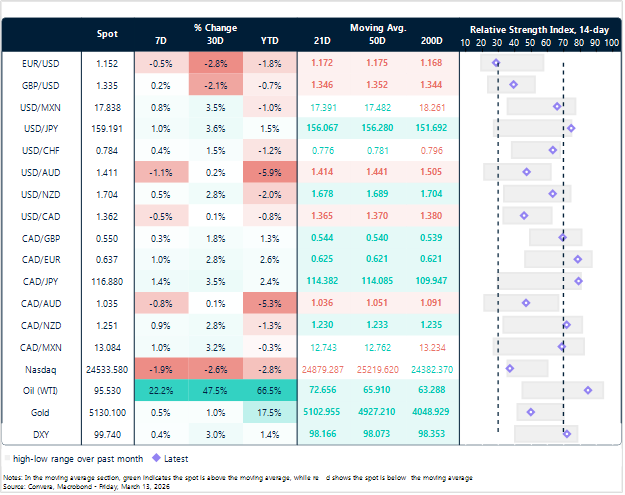

Market snapshot

Table: Currency trends, trading ranges & technical indicators

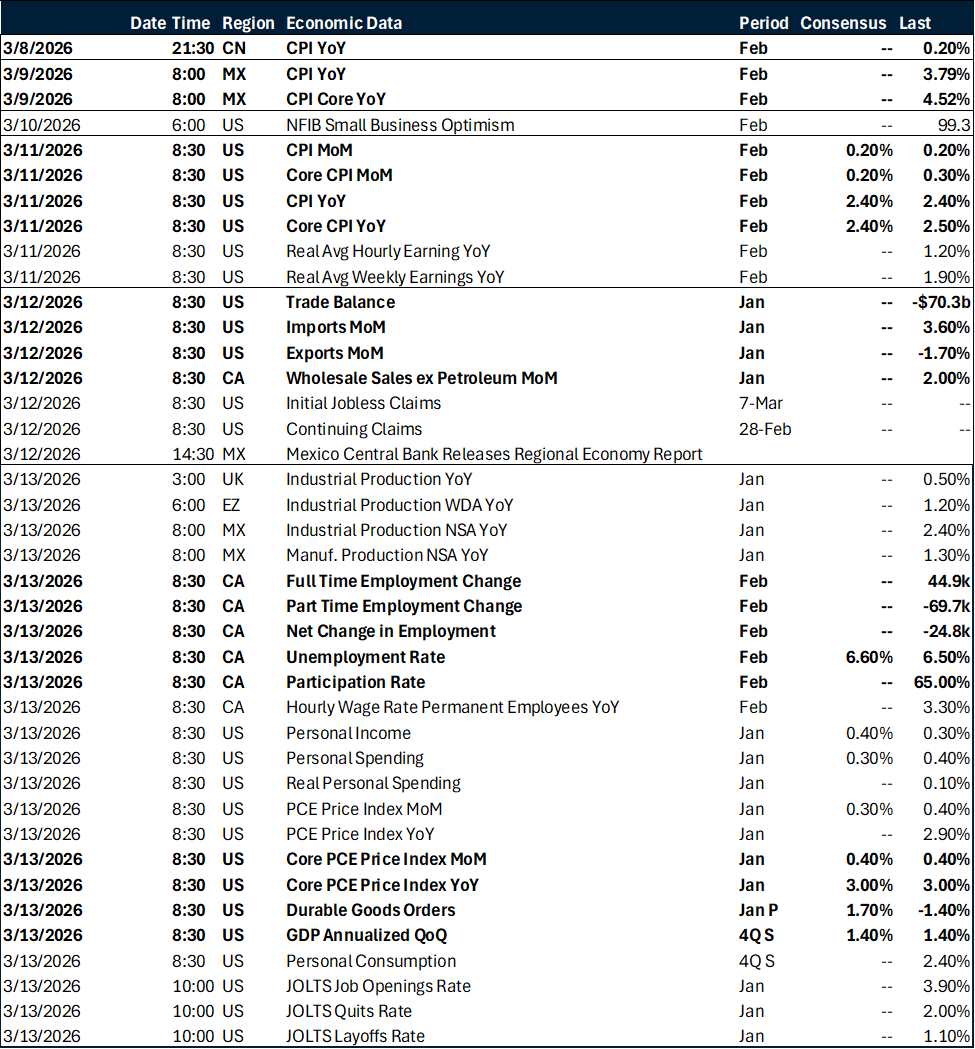

Key global risk events

Calendar: March 9 – 13

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.