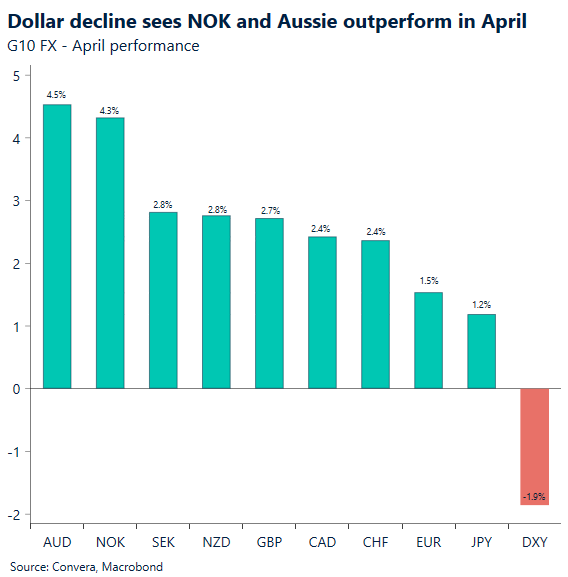

USD at post‑war lows

The US dollar started the new week on the back foot, with the Australian dollar leading gains early in Monday trading. Oil fell and US stockmarket futures gained after US president Donald Trump rejected a peace offer and said the US would escort commercial shipping through the Strait of Hormuz, adding a fresh geopolitical layer to already fragile markets.

Last week delivered a string of central‑bank hold decisions, but the overall tone was more hawkish than the unchanged policy settings suggested. The Fed, ECB, BoE and BoJ all kept rates steady, while warning that higher energy prices are complicating the inflation outlook and pushing the balance of risks closer to further tightening than easing.

Powell’s final meeting as Fed chair added to the drama. The decision split 8–4, the most divided Fed vote since 1992, before a theatrical sign‑off in which Powell confirmed he intends to remain on the Board as a governor while the Fed’s renovation saga continues. Meanwhile, the dollar was further destabilised by a sharp yen move, with suspected Japanese intervention after USD/JPY traded above 160.70 sending the pair abruptly lower and weighing on the greenback more broadly.

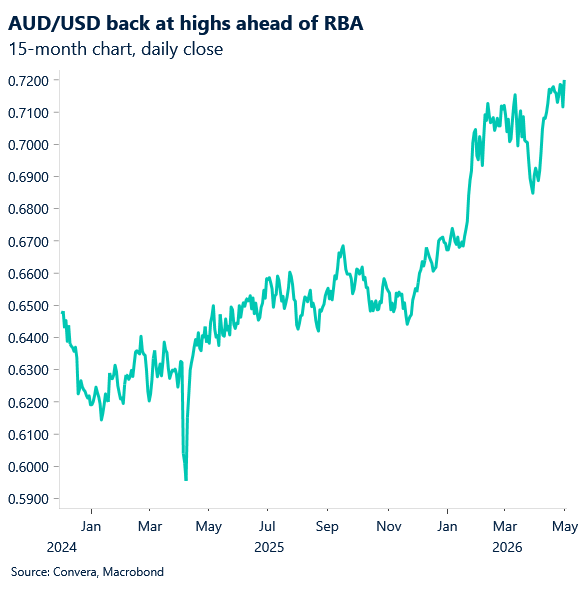

AUD/USD at four‑year highs

AUD/USD climbed to its strongest levels in four years as the weaker US dollar combined with steady domestic fundamentals. The focus now turns to Tuesday’s Reserve Bank of Australia meeting, where expectations remain finely balanced.

Australian inflation data released last week came in slightly softer than expected. Headline inflation eased to 4.6 percent against forecasts of 4.8 percent, while trimmed mean inflation held at 3.3 percent, broadly matching expectations. In response, market pricing for an RBA rate hike edged lower, with the implied probability slipping from around 80 percent to the mid‑70s, though markets still see a meaningful chance of further policy tightening.

For now, AUD/USD remains in an uptrend with next topside targets to 0.7245 and 0.7275.

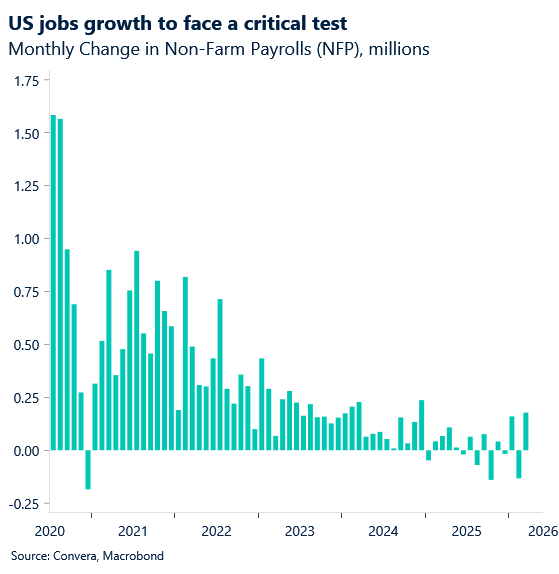

US jobs key on the economic front

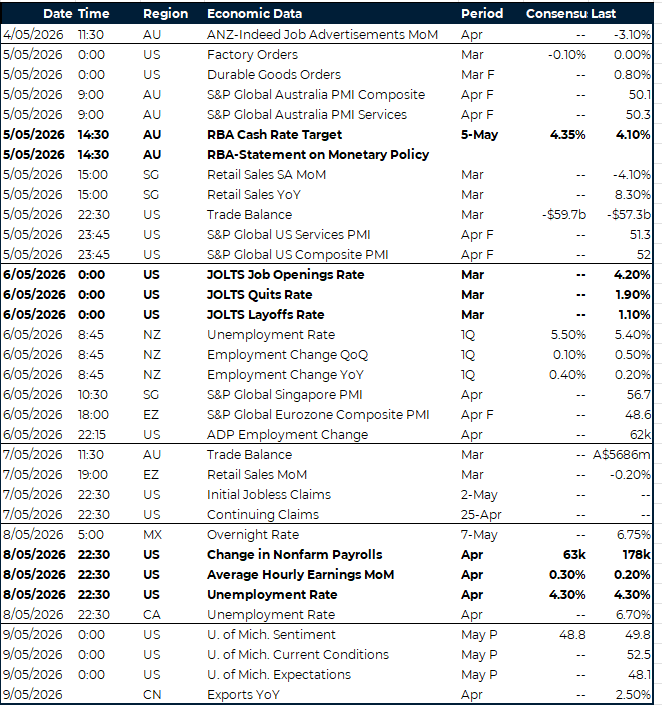

The US economy dominates the week ahead, with markets focused squarely on labour‑market data. The employment picture is under the spotlight after weekly jobless claims fell to their lowest level since 1969, reinforcing the view that labour conditions remain tight despite signs of broader economic cooling.

A full run of jobs data is scheduled, with JOLTS job openings due on Tuesday, ADP employment on Wednesday and the all‑important non‑farm payrolls report on Friday. For NFPs, the market is looking for 60,000 new jobs after the previous month’s 178,000 gain, while the unemployment rate is expected to remain unchanged at 4.3 percent.

Elsewhere, it is a relatively quiet week. Europe sees final manufacturing PMIs on Monday, final services PMIs on Wednesday and retail sales on Thursday, while the UK calendar includes construction PMI on Thursday and a key speech from Bank of England governor Andrew Bailey.

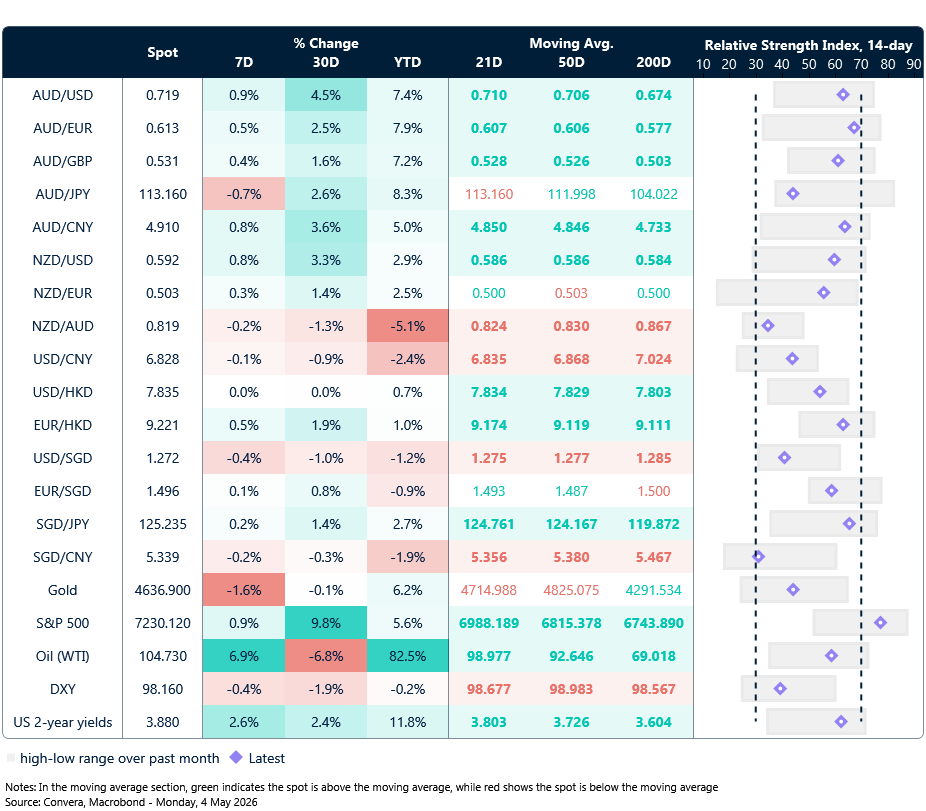

Aussie at highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 4 – 9 May

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.