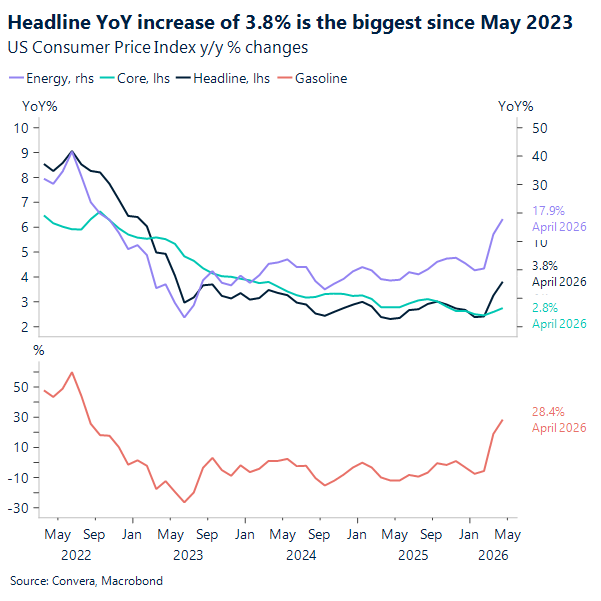

USD: April inflation heat tests market calm

Markets are taking the hotter-than-expected inflation data in stride this morning. While the US dollar edged up slightly and two-year Treasury yields climbed, the overall reaction remained relatively muted. Traders seem to be holding their breath because there is still one more inflation report due before the next Federal Reserve meeting in June. Even with Brent and WTI crude prices stuck in triple digits, the immediate needle for investors has not moved significantly yet.

The real surprise lies beneath the surface in the core inflation figures. Core CPI, which excludes volatile food and energy costs, rose 0.4% for the month and 2.8% annually. Both of these metrics topped economist estimates and represent the largest yearly jump since last September. This upward trend is particularly concerning because it follows a notable rise in March. Consequently, these sticky core numbers provide a fresh headache for Fed officials aiming for price stability.

Much of the monthly heat came from the energy sector, which accounted for over 40% of the total increase. Gasoline prices surged over 5% in April alone, pushing the headline annual inflation rate to a significant 3.8%. Although shelter and food costs also climbed, the energy index’s 17.9% annual spike remains the dominant factor. It will be a challenging transition for Kevin Warsh when he takes the Fed reins, as he must manage stubborn inflation while oil prices remain pegged at $100.

EUR: Fatigue sets in near 1.18

The euro is showing increasing signs of fatigue as repeated attempts to break above 1.18 against the dollar continue to fail. Each ceasefire‑related headline out of the Middle East has pushed EUR/USD toward that level, but rallies have faded quickly. While the pair remains above its key daily moving averages, short‑term momentum is rolling over, and a sustained close below the 200‑day moving average near 1.1680 would raise the risk of a deeper unwind.

Positioning still matters. Long‑USD exposure remains large enough to be trimmed on de‑escalation news, but each false dawn diminishes that support. More importantly, even a genuine peace agreement would not automatically generate a new euro‑positive impulse. The ECB has yet to act, rate differentials still favour the dollar, and the EU‑US trade agreement remains unresolved. In other words, peace may remove a headwind, but it does not create a durable tailwind.

If markets refocus on policy fundamentals, the picture becomes more challenging. Three ECB hikes are already priced for this year, leaving limited room for euro‑positive surprise, while tightening driven by stagflation risks is not a clean FX positive. By contrast, any repricing is more likely to come from the USD side via shifts in Fed expectations or haven demand.

Against that backdrop, today’s ZEW surveys at 10:00 BST will be watched closely. The last release in April delivered a sharp deterioration in both German and Eurozone sentiment and coincided with EUR/USD slipping from the 1.18 area, reinforcing the view that euro resilience was sentiment‑driven rather than data‑backed. With conviction already thinning, another weak print would again pose asymmetric downside risks.

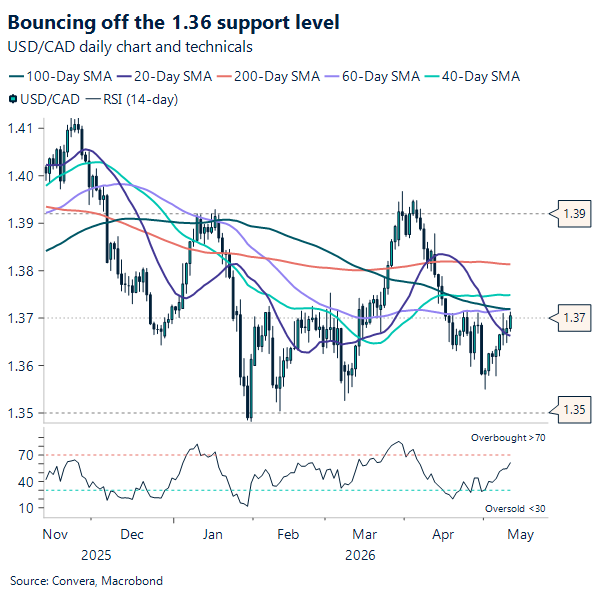

CAD: Bouncing off the 1.36 support level

After the weaker than expected labour read from last Friday, the USD/CAD bounced from its weekly low near 1.355 to around 1.371, a move that suggests the market initially leaned into the “softer Canada” narrative and priced a bit more caution on the policy outlook. Even so, the rebound also hints at two-way risk from here, because steady wage growth can keep inflation concerns alive while the rise in unemployment argues for patience. For traders and corporates, that combination often translates into choppier ranges and more sensitivity to each incremental data point, especially as markets weigh whether the Bank of Canada can stay restrictive or needs to turn more supportive.

The CAD is still a “USD giving back premium” story. USD/CAD is trading around 1.37, has broken above the 20-day moving average and sits below the 50/100/200-day moving averages, which keeps the near-term technical bias pointed lower for the pair, after a sequence of lower highs since late March. The first line in the sand is 1.3600, then the more meaningful support zone near 1.3520–1.3500; a clean break there would open room for a deeper extension. On the topside, rebounds should run into supply around 1.3680, then 1.3720–1.3730, with the 200-day near 1.3815 still the bigger trend filter, so unless USD/CAD can reclaim the mid-1.37s on a closing basis, the setup favors choppy-to-lower trade into the next week.

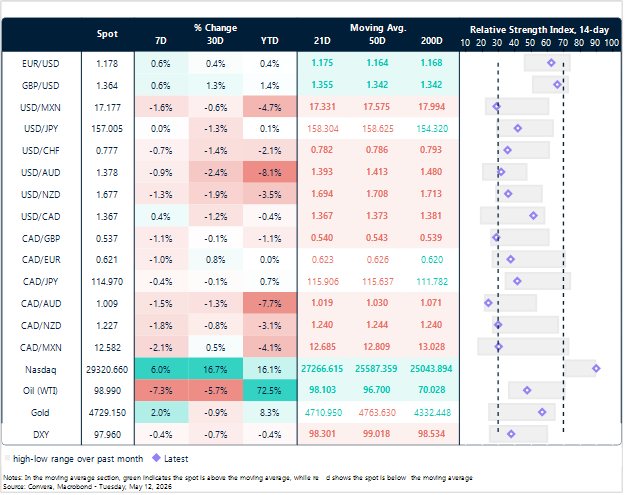

Market snapshot

Table: Currency trends, trading ranges & technical indicators

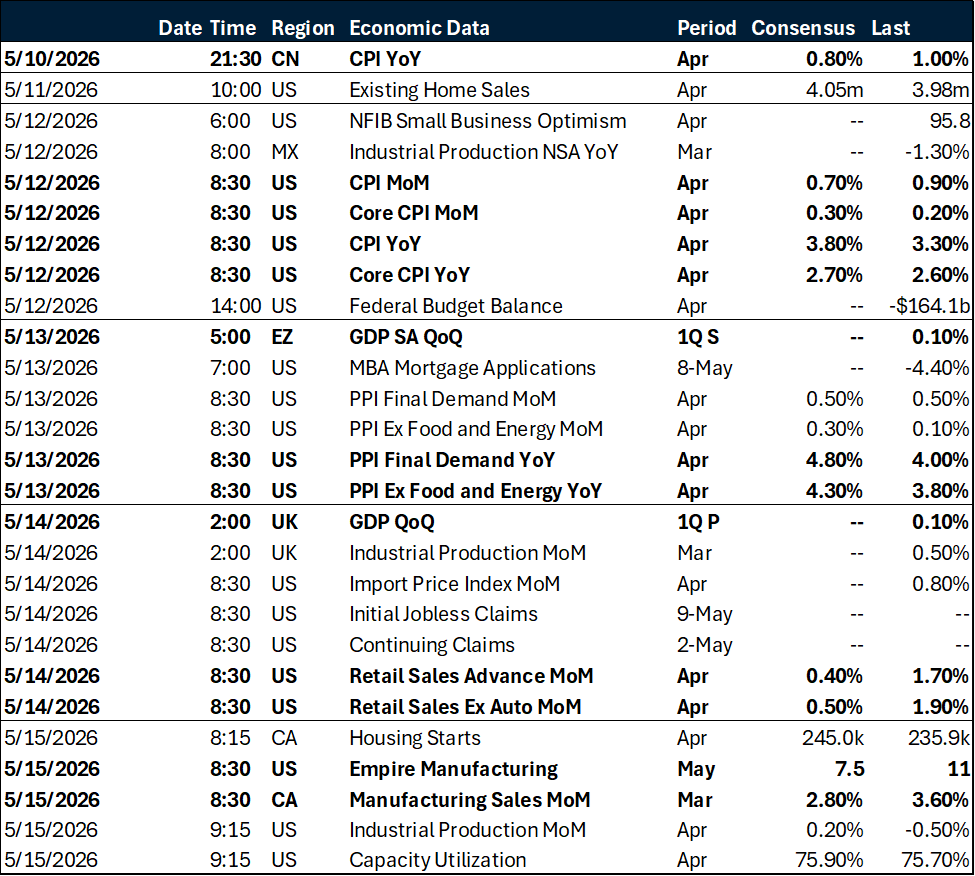

Key global risk events

Calendar: May 11 – 15

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.