USD: Limited peace progress, focus on inflation

The US dollar has started the week on firmer footing, supported by a renewed rise in energy prices after hopes for a near‑term Middle East peace deal faded. Brent and WTI both jumped around 3% as progress toward an agreement stalled, reversing last week’s optimism that a breakthrough could be secured ahead of President Trump’s visit to China later this week. Trump dismissed Iran’s latest proposal as “totally unacceptable”, while reports suggested the administration is reviewing options ranging from a resumption of military operations to renewed plans to escort commercial shipping through the Strait of Hormuz.

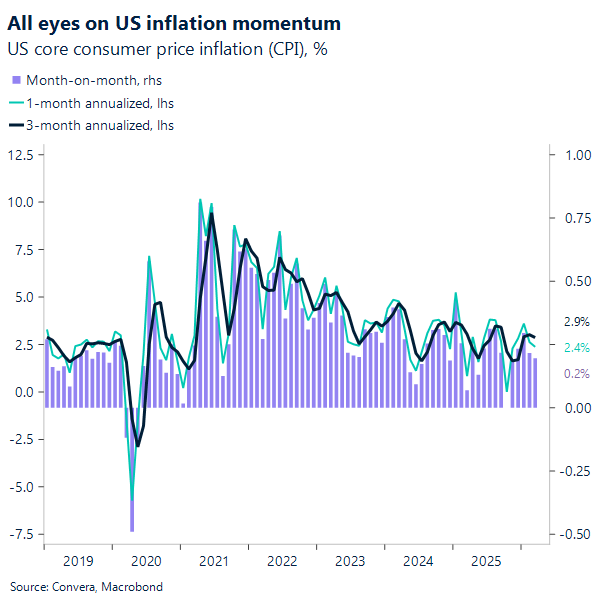

Absent meaningful behind‑the‑scenes pressure, most plausibly from China, markets are increasingly pricing a prolonged impasse. That points to higher oil prices and renewed global inflation pressure, placing the focus squarely on today’s US CPI release. Headline inflation is expected to accelerate to 0.6% m/m and 3.7% y/y, with core prices also forecast to firm. Any upside surprise would likely push Fed rate expectations higher and support the dollar via the yield channel.

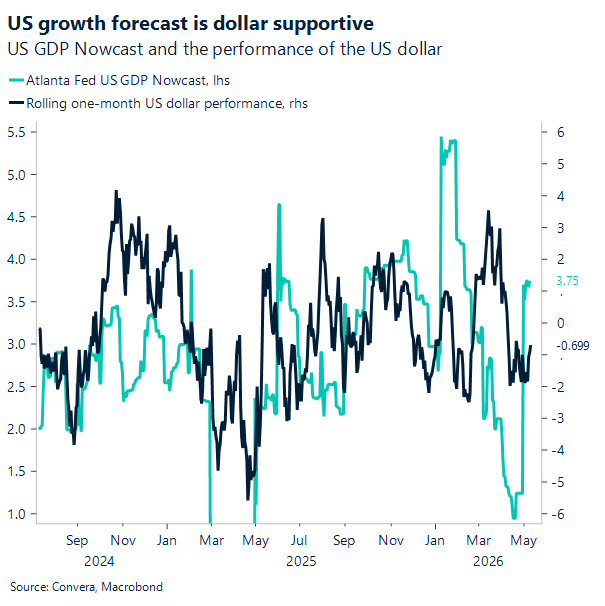

Still, the scope for sustained USD upside remains uncertain. Since the conflict began, FX has been trading through three competing lenses — oil, rates and risk, and resilient risk appetite continues to cap dollar gains. Global equities remain near record highs and volatility is anchored close to long‑run averages, limiting demand for defensive dollar positioning even as energy prices rise. For now, that has kept the USD confined to relatively narrow ranges against many peers.

That balance may not hold indefinitely. The US is likely to absorb less growth damage from higher commodity prices than most major economies, many of which are net energy importers. While markets remain focused on the inflationary impact of higher oil, the growth consequences may be underappreciated – and those dynamics are ultimately more supportive for the dollar, both fundamentally and as a relative haven.

EUR: Fatigue sets in near 1.18

The euro is showing increasing signs of fatigue as repeated attempts to break above 1.18 against the dollar continue to fail. Each ceasefire‑related headline out of the Middle East has pushed EUR/USD toward that level, but rallies have faded quickly. While the pair remains above its key daily moving averages, short‑term momentum is rolling over, and a sustained close below the 200‑day moving average near 1.1680 would raise the risk of a deeper unwind.

Positioning still matters. Long‑USD exposure remains large enough to be trimmed on de‑escalation news, but each false dawn diminishes that support. More importantly, even a genuine peace agreement would not automatically generate a new euro‑positive impulse. The ECB has yet to act, rate differentials still favour the dollar, and the EU‑US trade agreement remains unresolved. In other words, peace may remove a headwind, but it does not create a durable tailwind.

If markets refocus on policy fundamentals, the picture becomes more challenging. Three ECB hikes are already priced for this year, leaving limited room for euro‑positive surprise, while tightening driven by stagflation risks is not a clean FX positive. By contrast, any repricing is more likely to come from the USD side via shifts in Fed expectations or haven demand.

Against that backdrop, today’s ZEW surveys at 10:00 BST will be watched closely. The last release in April delivered a sharp deterioration in both German and Eurozone sentiment and coincided with EUR/USD slipping from the 1.18 area, reinforcing the view that euro resilience was sentiment‑driven rather than data‑backed. With conviction already thinning, another weak print would again pose asymmetric downside risks.

GBP: Markets look through short-term political jitters

Prime Minister Keir Starmer’s speech following Labour’s poor local election results was largely unimpressive from a market perspective, with attention instead focused on the broader geopolitical backdrop – particularly the fallout from failed US‑Iran peace efforts. That said, markets were not expecting much from the speech to begin with. Instead, the greater focus has been on how imminent a leadership challenge might be in the wake of the electoral setback. Some pressure grew on UK assets this morning, with bonds falling and the pound declining, as a mounting number of Labour Party politicians called on the leader to step down following the elections. Yet we doubt these moves will be sustained.

Chief among them was MP Catherine West, who had threatened to trigger an immediate leadership challenge before deciding to step down, instead calling on Starmer to set a timetable for his departure, along with other MPs.

Still, this degree of political fragility is something investors have grown accustomed to, raising the bar for any sustained market reaction to political noise alone. West’s move was also seen as largely strategic – designed to stir internal debate and potentially draw out stronger leadership contenders. For now, however, no clear alternative has emerged. And against an already fragile geopolitical backdrop, potential challengers may be reluctant to step forward. These dynamics – familiarity with political uncertainty and a degree of skepticism – help explain why sterling has, overall, been quite indifferent.

We believe the peak of pressure on Starmer – embodied by West’s threat – has likely passed for now, suggesting sterling may refocus on the macro backdrop, as well as the broader geopolitical environment. The former may itself have taken on a more political dimension: should the upbeat momentum seen so far this year persist in the months ahead – with tomorrow’s Q1 GDP release a key test – it would provide further reason to keep worst-case scenarios for both Starmer and the pound off the table for now.

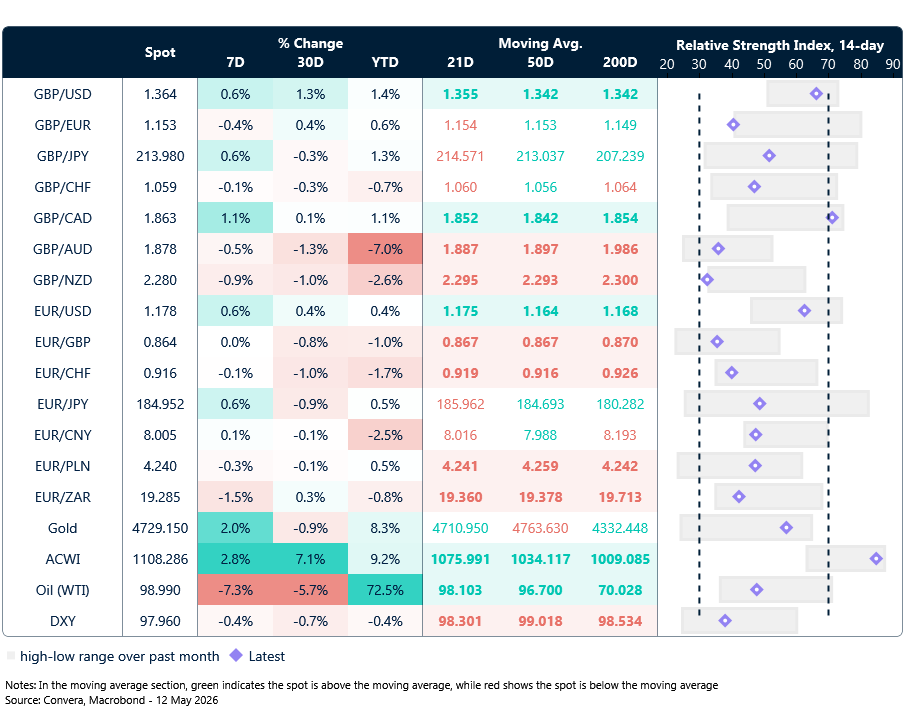

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

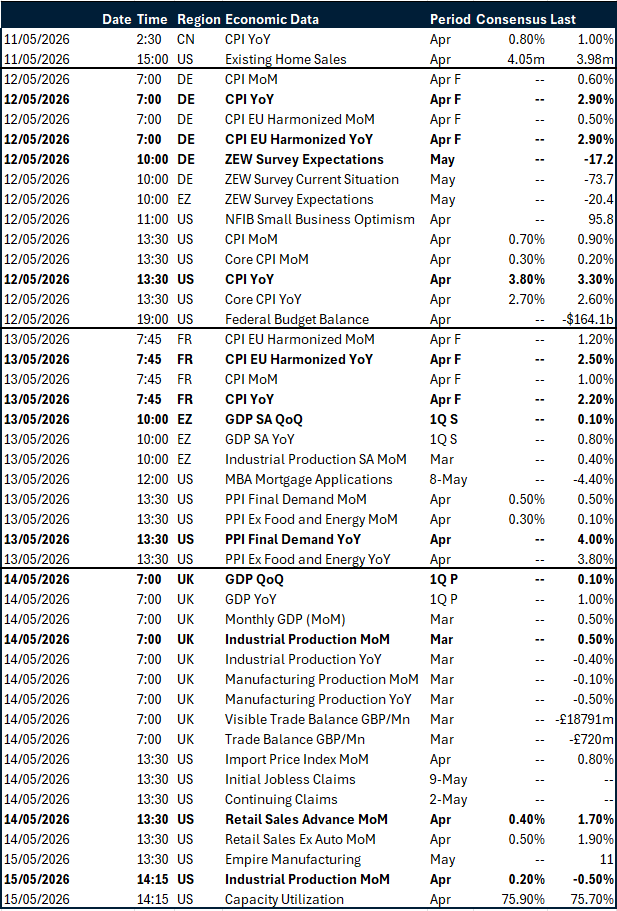

Calendar: May 11-15

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.