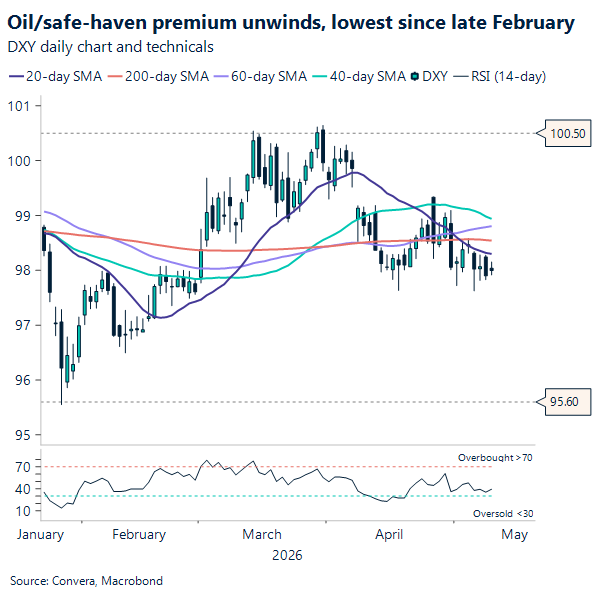

USD: Oil anchors rates, dollar stays range bound

While markets are still struggling to price in a return to “normal,” the cross-asset message remains uneven. Equities, however, have been looking past recent headlines, fueled by a Q1 2026 earnings season that has been, in a word, robust. As of early May, with nearly 90% of S&P 500 companies having reported, this season is shaping up to be the strongest since the post-pandemic boom of 2021. Corporate America has largely brushed off the “geopolitical fog,” delivering a blended earnings growth rate between 27.7% and 28.2%, the highest since Q4 2021. This strength is broad-based: approximately 84% of companies have surpassed EPS estimates, comfortably exceeding the five-year average of 78%. Furthermore, the top line remains healthy, with revenue climbing roughly 11.3% year-over-year and 80% of firms beating sales expectations.

Meanwhile, rates have stayed more sensitive, with the 10‑year still taking cues from oil. The split matters, because it keeps energy and geopolitics doing more of the macro work, even as broader risk sentiment appears calmer. Starting the week, Oil is higher after US President Donald Trump said Iran’s response to the US peace plan was “totally unacceptable.” Both Brent crude and WTI jumped about 3.0% on the news, with the WTI trading again closer to $100 a barrel.

On the macro side, last Friday, the US jobs report came in stronger than expected. April nonfarm payrolls rose 115,000 versus 65,000 expected. Under the hood, the message is a bit more mixed than the headline suggests. The household survey shows the labor force shrank and employment fell there, so the unemployment rate held at 4.3% partly because people exited the labor market, not a great growth signal. Same “low hiring, low firing” regime that has been in place since late last year, as softer wage growth on the month and a broader pattern of cooling job gains over the past three months remain in the picture. Still, this mix makes it hard to justify a meaningful easing story, and it likely keeps the Fed’s attention on upside inflation risks, while the June statement could even dial back the easing bias if conditions hold.

For the US Dollar, the report lands as a supportive input, even if the day-to-day drivers are still dominated by geopolitics and policy optics. Since the ceasefire was confirmed, the USD has slipped about 2%, leaving it modestly lower on the year and still comfortably inside its roughly 11‑month trading range. The greenback remains tightly linked to the Iran conflict and the ebb and flow of any conflict premium, while intermittent pressure also comes from Japan, where the market stays alert to the risk of BoJ-related intervention dynamics. What the data does do is make the next leg lower in the Dollar harder to sustain, because it reinforces the idea that the Fed cannot comfortably keep cutting in an environment where the labor market looks stable and inflation risks feel one-sided. In other words, unless energy prices and the Middle East backdrop change the calculus in a big way, the bar for sustained Dollar weakness looks higher, as the more dovish scenarios get pushed further out.

What’s happening in markets this week?

This week opens with a cloud of political speculation in the UK regarding Keir Starmer’s leadership and its potential impact on UK bond market stability. On Tuesday, focus shifts to US CPI inflation report alongside the start of the highly anticipated China-US Summit. While leaders discuss trade and technology, the focus moves on to Wednesday on the Congressional vote for Kevin Warsh to lead the Federal Reserve. Simultaneously, market participants will closely monitor negotiations on Wednesday to reopen the Strait of Hormuz, as any progress there could finally ease the persistent supply-side shocks currently driving global prices higher.

Turning to the end of the week, Thursday highlights include the US PPI release and a final wave of corporate earnings guidance that will reveal how manufacturers are handling rising input costs. This data helps bridge the gap to Friday, when a flurry of international reports, including UK GDP and Eurozone industrial production, will test the resilience of advanced economies. Furthermore, Friday’s updates on Chinese and Indian inflation will provide the final pieces for global demand projections.

CAD: Loonie finds support at 1.36

After the weaker than expected labour read from last Friday, the USD/CAD bounced from its weekly low near 1.355 to around 1.371, a move that suggests the market initially leaned into the “softer Canada” narrative and priced a bit more caution on the policy outlook. Even so, the rebound also hints at two-way risk from here, because steady wage growth can keep inflation concerns alive while the rise in unemployment argues for patience. For traders and corporates, that combination often translates into choppier ranges and more sensitivity to each incremental data point, especially as markets weigh whether the Bank of Canada can stay restrictive or needs to turn more supportive.

The CAD is still a “USD giving back premium” story. USD/CAD is trading around 1.367 starting the week, sitting below the 20/50/100/200-day moving averages, which keeps the near-term technical bias pointed lower for the pair, after a sequence of lower highs since late March. The first line in the sand is 1.3600, then the more meaningful support zone near 1.3520–1.3500; a clean break there would open room for a deeper extension. On the topside, rebounds should run into supply around 1.3680, then 1.3720–1.3730, with the 200-day near 1.3815 still the bigger trend filter, so unless USD/CAD can reclaim the mid-1.37s on a closing basis, the setup favors choppy-to-lower trade into the next week.

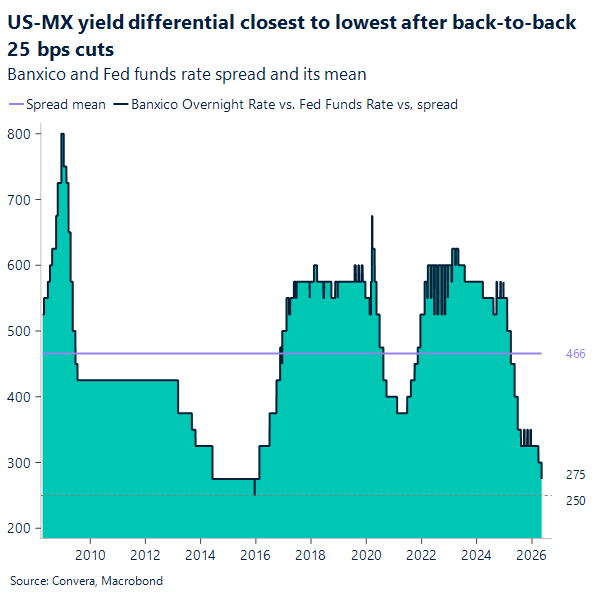

MXN: Banxico signals endgame, Peso carry holds

Banxico delivered a second straight 25bp cut, taking the overnight interbank target rate down to 6.50% effective May 8, but the split vote made the decision feel more cautious than dovish. Three board members supported the move, while two preferred to hold, which is a clear sign that the easing window is narrowing. Inflation helped justify the cut, because April headline slowed to 4.45% and core eased to 4.26%. Still, both measures remain above the 3% target midpoint, and Banxico continues to highlight upside risks to the inflation path. At the same time, the growth story has weakened, with the bank pointing to a contraction in 1Q26 that implies more slack and less demand pressure.

Even more important for markets, the statement read like a “final cut” rather than an invitation to keep moving lower. Banxico explicitly framed this step as concluding the easing cycle that began in March 2024, and it signaled that maintaining the reference rate at current levels should be appropriate from here. That message matters because it reduces the odds that investors will price a long string of additional cuts. It also reflects a tighter risk balance: Banxico revised headline inflation forecasts higher for 2Q–3Q26 due to expected non-core pressures, and it kept the balance of risks tilted to the upside. In plain terms, policy is now being described as restrictive enough, especially given the mix of exchange-rate considerations, soft activity, and the degree of existing monetary restraint.

For USD/MXN, the cut mechanically narrows Mexico’s carry advantage, but the “likely done” guidance should help cap follow-through upside in the pair by limiting expectations for further spread compression. In the near term, a lower policy rate can trim support for the peso at the margin, yet the bigger driver for sustained MXN weakness is usually the market’s belief that more cuts are coming. Banxico’s pause signal pushes back against that narrative, and the statement’s explicit reference to the exchange rate, along with the note that the peso has appreciated since the prior decision, reads like a reminder that officials do not want to over-ease and trigger instability. As a result, USD/MXN rallies tied only to “Banxico still cutting” may struggle to extend, while risk sentiment and oil prices remain key short-term swing factors as the peso finds it difficult to break below its 2026 low near 17.08, keeping year-to-date gains around 4%.

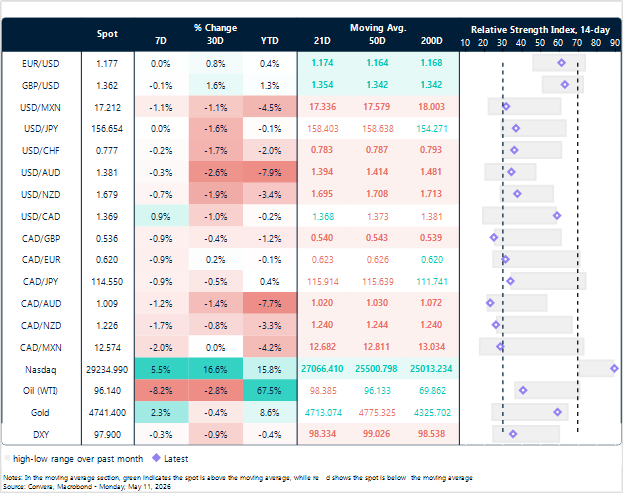

Market snapshot

Table: Currency trends, trading ranges & technical indicators

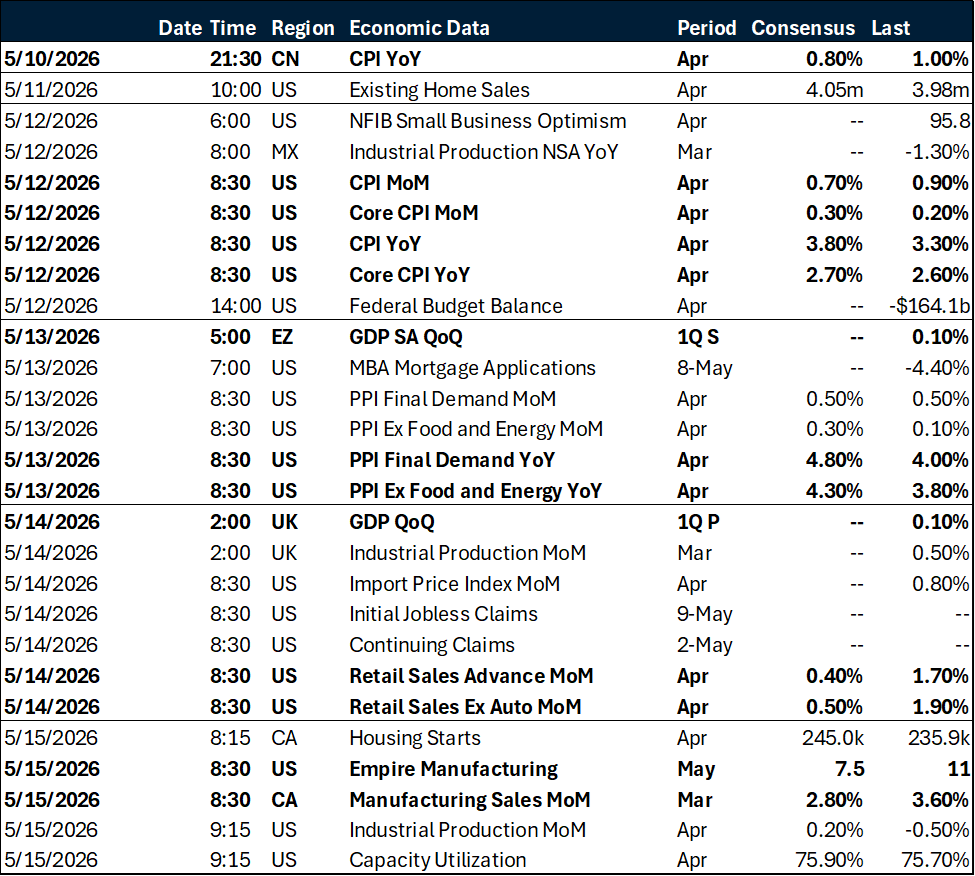

Key global risk events

Calendar: May 11 – 15

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.