Investors are looking back at the week with positive feelings. The rise of US initial jobless claims to an 8-month high was enough to give equities benchmarks a boost and dampen demand for the dollar.

DXY edged out a marginally positive week due to the dollar’s strength versus the yen. The pound remained flat despite the BoE’s dovish undertone and the euro rose for a fourth consecutive week versus the Greenback to hit the $1.0780 level.

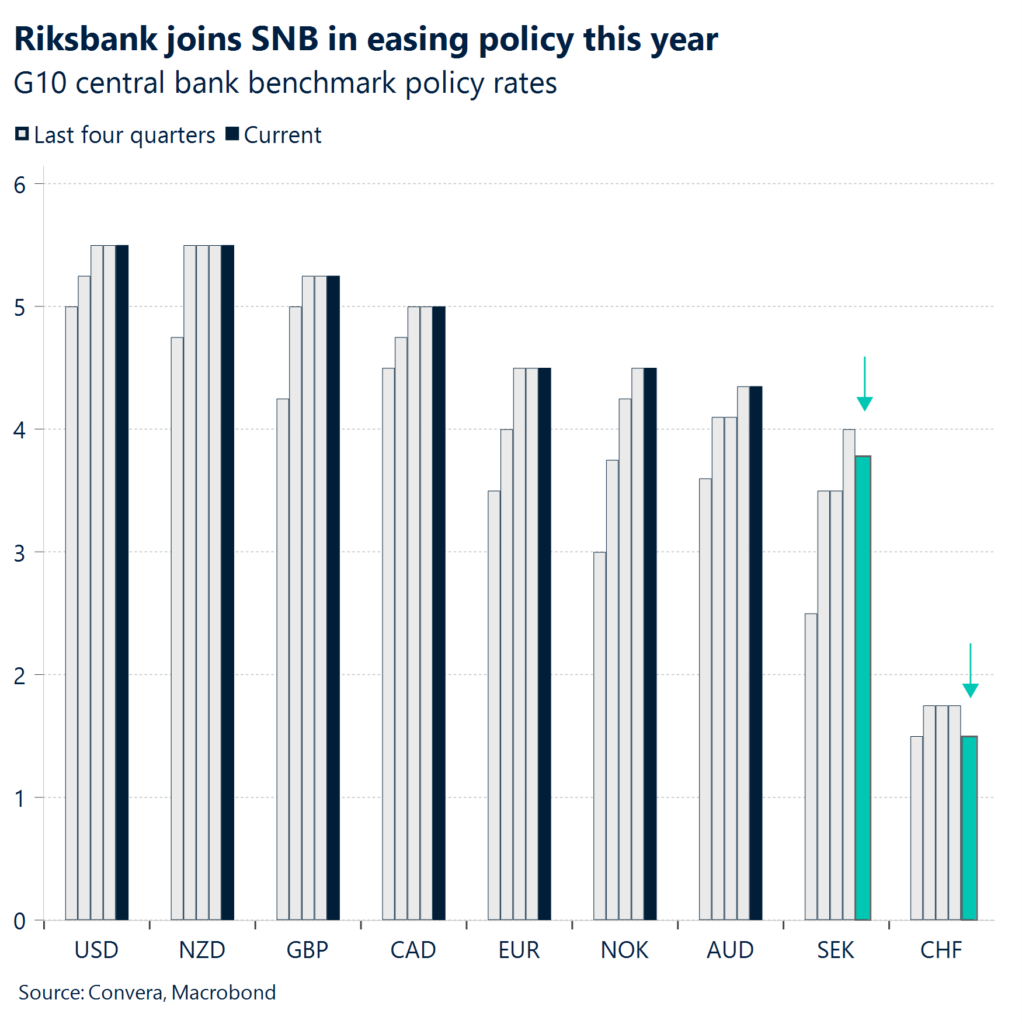

The Swiss Central Bank started off the European dominated G10 easing cycle in Q1 with Sweden’s Riksbank following up with a 25-basis point cut this week. Policy makers are cautiously trying to support their respective economies.

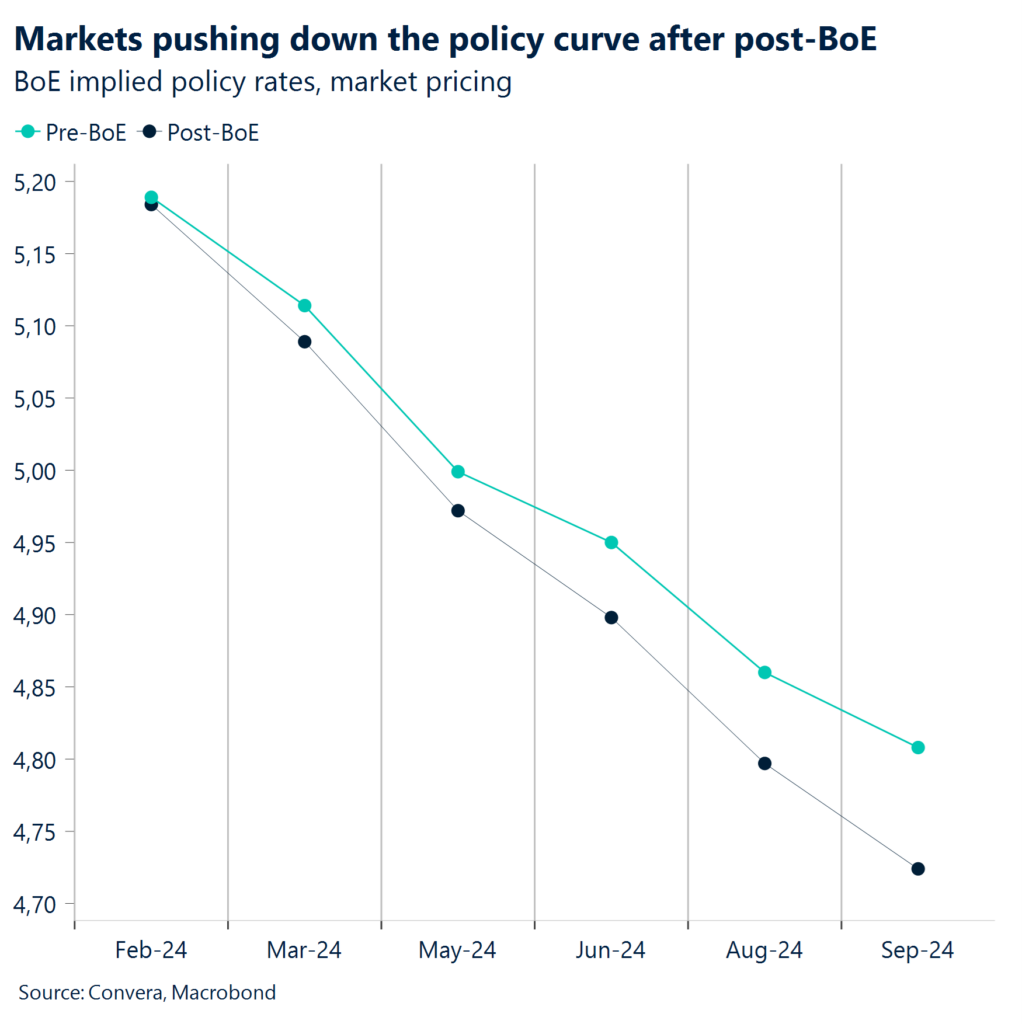

As expected, the Bank of England (BoE) left interest rates unchanged at 5.25%. Still, policy makers are edging closer towards a rate cut while keeping options open amid the volatile nature of macroeconomic data and upside surprises as of late.

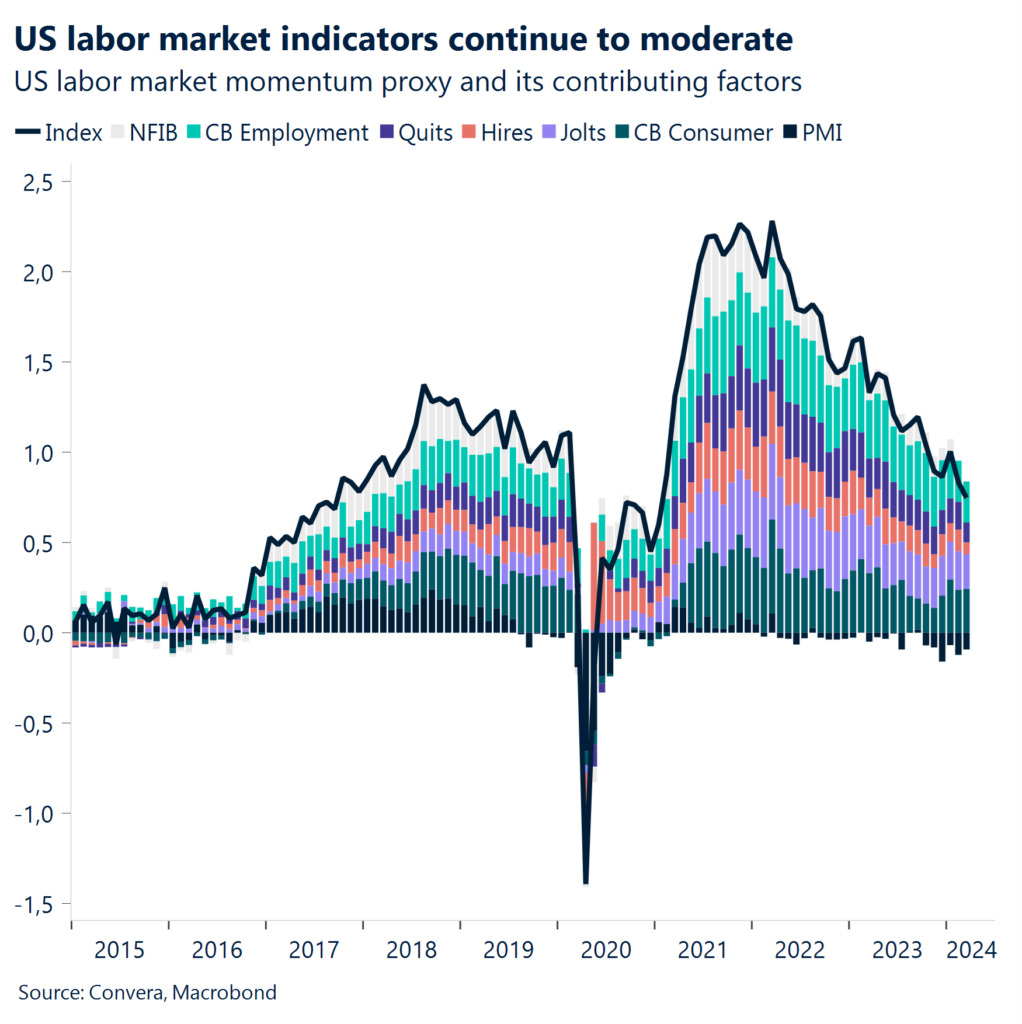

The latest string of data disappointments from the purchasing manager indicators and small business confidence falling to an 11-year low to job growth starting to moderate have thrown the US exceptionalism theme into question.

March retail sales in the Eurozone jumped by 0.8% m/m, above expectations, in what was the sharpest monthly increase in the past 18 months. Producer prices fell by 0.4% in March, in line with consensus, marking a 5th consecutive monthly decline.

The upcoming week could paint a complex picture of an US economy that is experiencing high inflation and a continued divergence of soft vs. hard data.

Global Macro

Risk-on prevails as central banks cut rates

Rising equity markets. Investors are looking back at the week with positive feelings despite the lackluster open on Monday being shaped by British and Japanese investors on holiday. China came back from a 5-day break seemingly refreshed with investors pouring into equities, with the CSI 300 securing its fourth weekly rise in a row. European and US stock benchmarks followed suit as the S&P500 pushed higher for a third week while the Stoxx 600 reached a new record high. A strong earnings season and investors bringing back some of the policy easing bets priced out (Fed, BoE) during the last couple of weeks have given investors the green light to switch into a risk-on mode.

The doves are in Europe. The Swiss Central Bank started off the European dominated G10 easing cycle in Q1 with the Swedish Riksbank following up with a 25-basis point cut this week. Policy makers are cautiously trying to support their respective economies, which have suffered from benchmark rates at decade-highs. However, price pressures remain far from tamed as inflation in Sweden still sits above the European median at around 4%. Inflation is clearly moving in the right direction and has come down a lot over the course of 2023. Nonetheless, elevated price growth in the US, delayed rate cuts from the Federal Reserve and the potential uptick in goods inflation in later parts of 2024 could become a problem for European central bankers eager to ease policy.

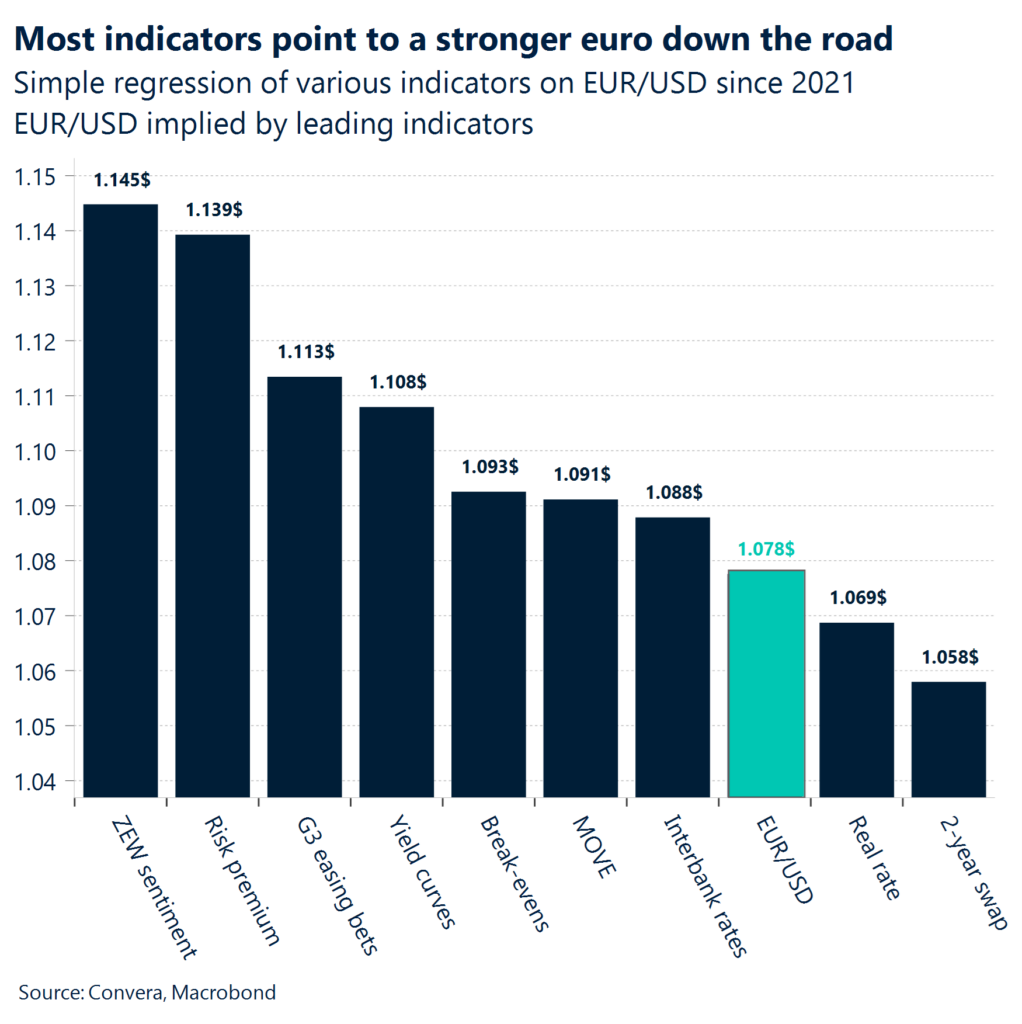

Pricing EUR/USD. The recent string of disappointing US macro data and an improving growth outlook in Europe have lifted EUR/USD from a 5-month low at around the $1.06 level in April to the top $1.07 area. Implied volatility on most tenors remains depressed and suggests range bound movement of the currency pair. Still, it is important to recognize that most leading macro and market indicators highlight an improving outlook for the common currency. While not a guarantee for a rising exchange rate, we see an asymmetric risk profile benefiting the upside over the next 9-12 months.

Deep Dive

Gauging US recession risks

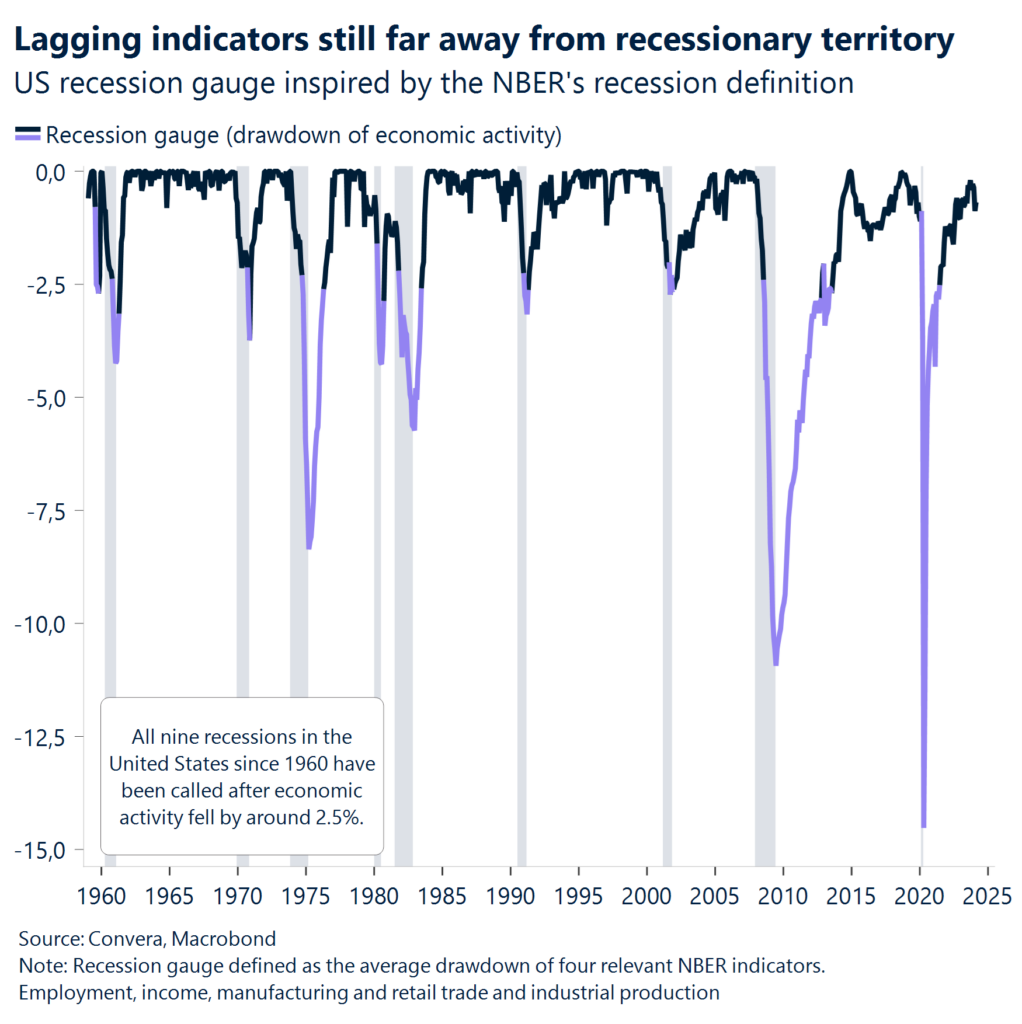

The US economy has clearly been in a league of its own in the post-pandemic era as extraordinary stimulus packages on both the fiscal and monetary sides boosted households balance sheets. The first quarter of the year has underlined the exceptional position of the US economy compared to its peers with inflation and employment data surprising to the upside. Lagging data that is relevant for the National Bureau of Economic Research to make a call on whether the US has entered a recession remained resilient over the past quarters. An average drawdown of 2.5% on employment, personal income, manufacturing and retail trade and industrial production has historically been needed for the NBER to call a recession. We are far from it.

Still, the latest string of data disappointments from the purchasing manager indicators and small business confidence falling to an 11-year low to job growth starting to moderate have thrown the US exceptionalism theme into question.

We have recently proposed two macro theses that are starting to unfold, and which might complicate the picture for the Fed going into the second half of the year. First, the global inflationary impulse and the goods side of inflation have bottomed and are on the rise again. Second, the US labor market and economic growth are more likely to surprise to the downside. This poses a conundrum for the Fed, that is complicated by the upcoming presidential election in November. Q2 inflation misses and further moderation in job and wage growth might sway policy makers to cut rates in July.

However, an early pivot and pipeline price pressures might anchor inflation above the 2% target in 2025. The incoming data will be crucial to gauge how much of the goods inflation uptick will be combatted with by falling wage growth and if the weakness in soft data points translates into deteriorating hard data.

Regional outlook: US & UK

Fed too hawkish, BoE too dovish?

Hawkishness at the wrong time? Comments from several Fed policymakers this week have been suggesting rates will stay elevated for some more time. It’s no surprise given the upside surprise in all inflation readings last quarter and the strength of US economy eroding expectations for how deeply the Fed will be able to cut rates this year. But the economic backdrop appears to be moderating with soft data, like PMIs, disappointing relative to expectations at a fast rate and the overall economic data surprise index trailing at 2022 lows. Moreover, further signs of a cooling labor market are starting to fan hopes of rate cuts once again, spurring a risk on rally with US benchmark equity indices up almost 2% this week.

Coming closer to a cut. As expected, the Bank of England (BoE) left interest rates unchanged at 5.25%. Dave Ramsden joined Swati Dhingra in calling for a cut, thus shifting the vote split to 7-2 from 8-1 previously. During the presser, Bailey stated a June rate cut is ‘neither ruled out, nor fait accompli’ and the bank remains data dependent with two more inflation readings between now and then to digest. The BoE continues to emphasise the UK’s inflation outlook as quite different to the US as it downgraded its 2-year inflation forecast to 1.9% from 2.3% previously.

The bottom line: the BoE is edging ever closer towards a rate cut but is keeping its options open amid the volatile nature of macroeconomic data and upside surprises as of late. At the same time, the Fed is reigniting its hawkishness against the backdrop of solid Q1 hard data. However, leading indicators and labor market momentum are dropping. The upcoming CPI prints for both regions will be crucial to determine which central bank cuts when.

Regional outlook: Eurozone

Confirming recovery thesis

Eurozone PMIs revised higher. Eurozone composite PMI was revised higher to 51.7, up from an expected 51.4, following an upward revision in the services sector PMI and taking the headline index to an 11-month high.

Consumer spending recovers. March retail sales in the Eurozone jumped by 0.8% m/m, above expectations, in what was the sharpest monthly increase in the past 18 months. On yearly terms, retail sales rose by 0.7%, pointing to the first growth since September 2022. The report signals recovering consumer demand and aligns with other economic data releases pointing to the bloc’s economic recovery.

German manufacturing continues to struggle. German industrial production declined by 0.4% m/m in March, admittedly less than the market consensus of a 0.6% m/m drop but marking the first contraction so far this year. The less volatile 3m/3m comparison showed that production was 0.1% higher from January to March 2024 than in the previous three months. On an annual basis, industrial output fell 3.3% y/y in March, softer than the prior 5.3% y/y slump.

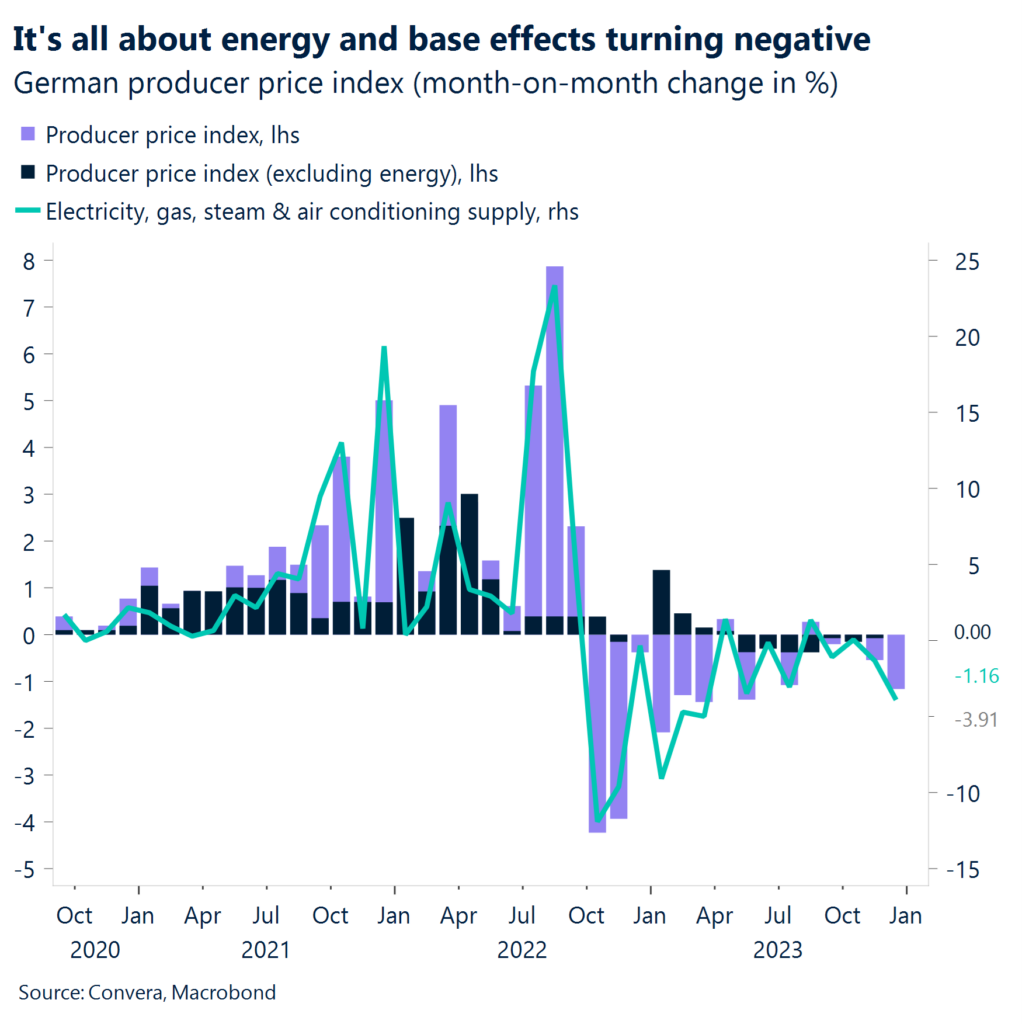

Energy and base effects drive producer disinflation. Eurozone producer prices fell by 0.4% m/m in March, in line with consensus, marking a 5th consecutive monthly decline, driven by a continued drop in energy costs. Excluding energy, producer prices rose 0.2% m/m and declined by 7.8% when compared on a yearly basis.

Week ahead

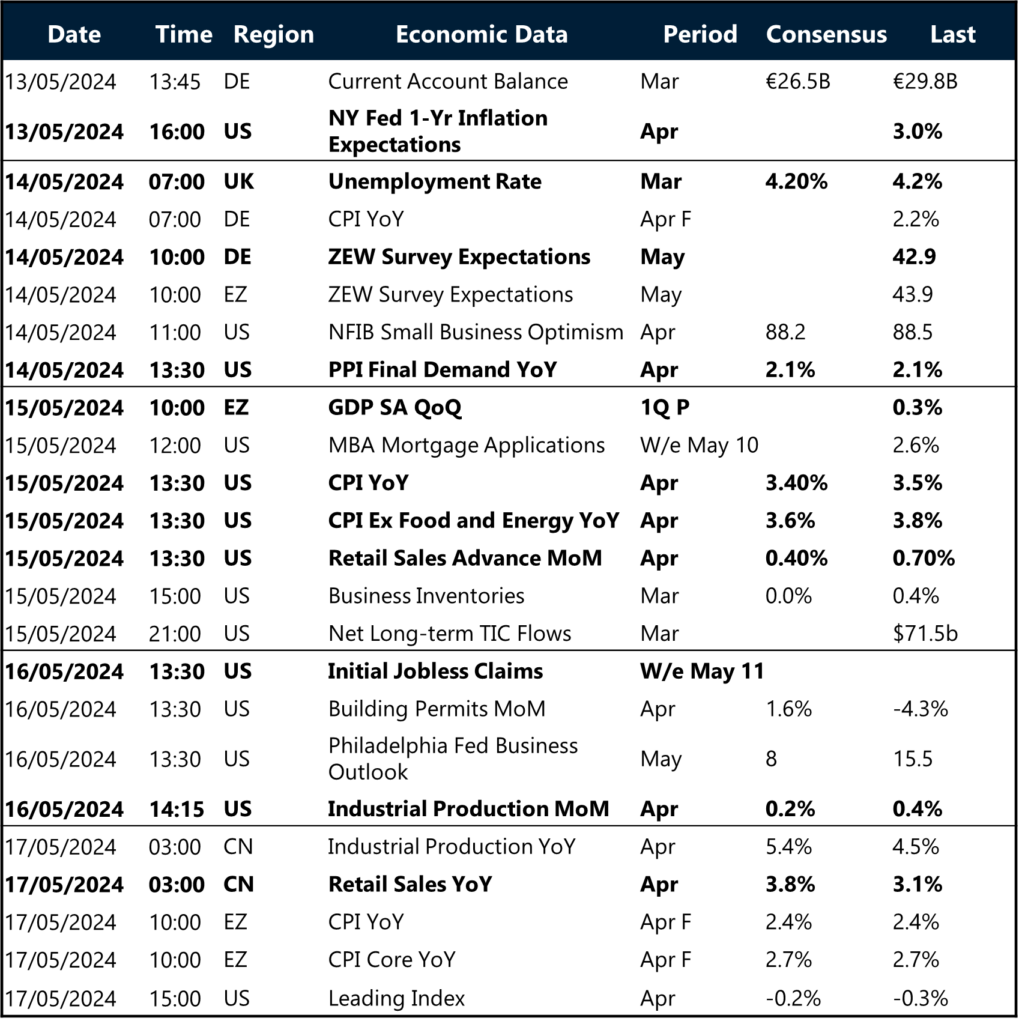

US inflation (CPI) will make or break the week

No news was good news. The lack of market moving headlines and data releases this week have been interpreted as good news for risk assets. The G3 central bank meetings are behind us and with the US jobs report having been published two weeks ago, focus shifts once again to inflation data. The rise of initial jobless claims to an 8-month high in the US was enough to give equities a boost and dampen demand for the dollar.

CPI could test risk-on rally. The upcoming week could paint a complex picture of the US economy that is experiencing high inflation and a continued divergence of soft vs. hard data. Both core and headline inflation are expected to have risen by 0.3% m/m in April with retail sales coming in at 0.4%.

Don’t forget PPI. The producer price index has proved market moving as well in recent times, especially in weeks where the print was combined with other second-tier data to create a certain narrative. With Fed speak recently having shifted to a more hawkish undertone, policy makers could feel vindicated by such strong data and continue pushing the higher for longer narrative.

Small businesses are suffering. At the same time, small business sentiment is expected to have dropped further in April, after reaching an 11-year low the month prior. Jobless claims, industrial production and the leading index will be closely watched as well.

FX Views

Pro-cyclicals push higher

USD Dented by soft jobs data. The dollar’s asymmetric reaction function remains evident as investors buy into the slower US labor growth narrative. The dollar index is around 1.2% below its 2024 high achieved in late April after weaker jobs data of late, but continues to hold above the 105 handle, with decent support found at its 100-week moving average just below. The buck’s high yield appeal remains supportive too, because despite the sharp drop in US yields from 6-month highs, this has eased concerns over diverging monetary policy trends, leading to a decline in cross-market volatility. In this sort of an environment, it seems likely that the USD will remain relatively resilient given the yield advantage on offer vs. most G10s, though the prospects of a broad-based rally seem relatively remote given further Fed hikes are now off the table. Upcoming consumer and producer inflation data will be crucial in providing further clarity on the policy path though, with market pricing for Fed cuts in 2024 having stabilised around 45bps. A downside surprise could be the nail in the coffin to spur a mass unwind of the overstretched dollar long position.

EUR Bounded in a triangle formation. The euro remained largely range bound in a $1.073 – $1.080 span against the US dollar given a lack of top tier market moving data and decisive trading. 1-week realised volatility trended below its longer-term averages, while the implied volatility over the same tenure does not offer meaningful evidence of a shift in the near-term. The pair continues to closely track government bond yield differentials, with both DE-US 2-year and 10-year yield spreads narrowing to 1-month lows favouring the euro. In terms of option market sentiment, 1-week 25-delta risk reversal skew briefly flipped in favour of euro calls for the first time since the beginning of March amid investor concerns on the back of last week’s NFPs. However, the latest sentiment positioning has turned more neutral since. EUR/USD is set to post a fourth consecutive increase when measured on the basis of weekly closing prices, but technicals point to a range bound environment and signal the pair may be running out of steam. Further dollar weakness is a necessary requirement for the euro to break higher above the $1.08 level, given the strong technical resistance barriers ahead.

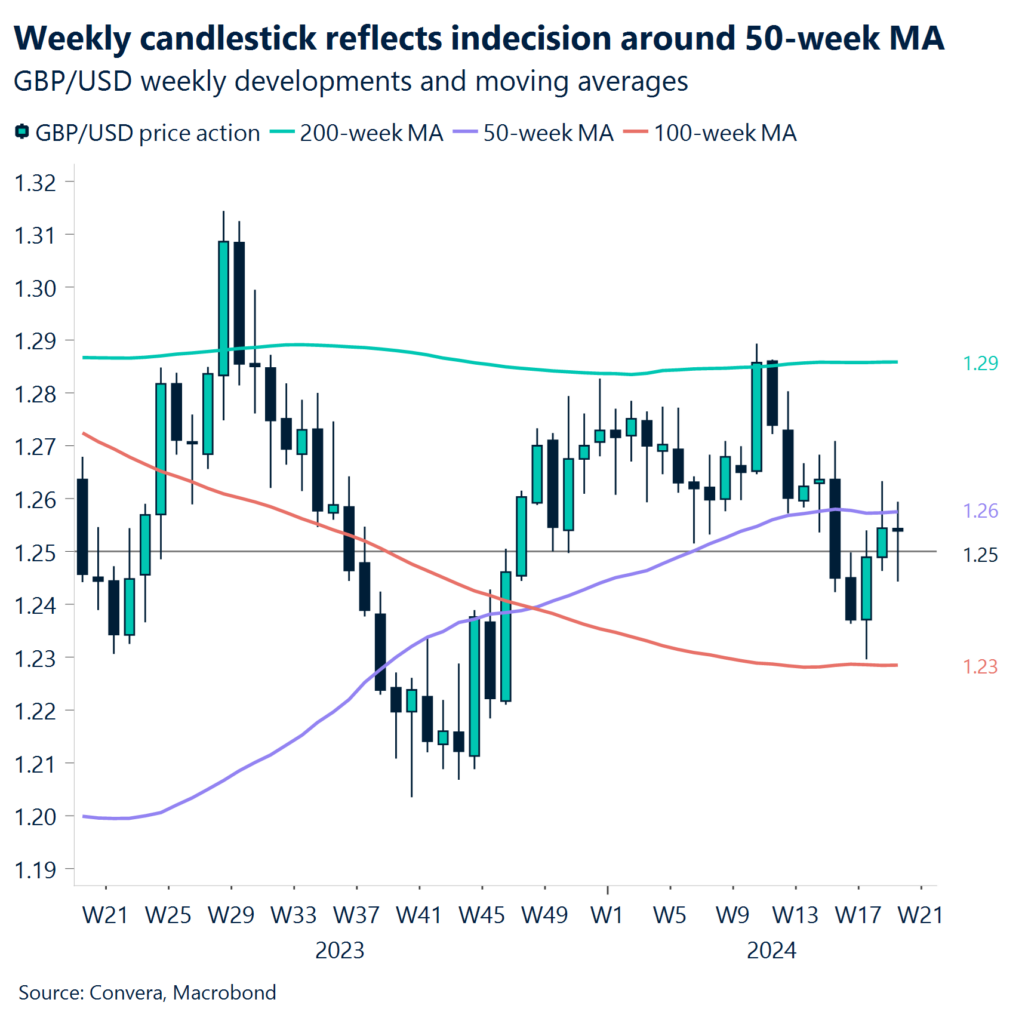

GBP Erases BoE losses after upbeat GDP. Sterling has appreciated against just 25% of its global peers so far this month. Weighing on the pound has been the rising odds of a June rate cut in the UK, which jumped to 56% after the BoE struck a dovish tone at its May meeting, with a 7-2 vote split, a tweak in the guidance and a push back against market pricing. However, stronger than expected Q1 UK GDP results offered the pound some support, as the probability of a June cut fell back below 40%. The yield on the UK’s 2-year Gilt, a good measure of near-term policy rate expectations, has retreated to its lowest level in a month, but amid overall G3 easing bets increasing of late, the pro-cyclical pound remains supported in this risk-on climate. Despite falling to a fresh 1-week low, GBP/USD continues to gravitate towards its 200-day moving average at $1.2541 though short-term upside is capped by its 50-week MA. The weekly candlestick chart reflects indecision as well, as market participants await a slew of key inflation prints from both the US and UK over the next couple of weeks to determine policy paths. Although the latest GDP data will give the BoE food for thought, if we see a big enough downside surprise in UK services inflation, the odds of a June cut will spike higher and sterling risks sliding back towards its 2024 low of $1.23 against the dollar whilst potentially testing €1.15 against the euro.

CHF Tainted by risk rally. The Swiss franc’s momentum against its global peers has increased over the last few months, after appreciating against just 14% of 50 selected peers in February to above 40% so far in May. However, recent dovish repricing of global rate expectations have wounded the franc’s attempted recovery with EUR/CHF holding firm above 0.97, just 1% below its 1-year highs. The yield on the 10-year Swiss bond declined to below the 0.7% level, reaching nearly a fresh monthly low, tracking a global fall in bond yields and putting further pressure on the low-yielding franc as USD/CHF remains suspended above 0.9, almost 8% higher year-to-date. Meanwhile, recent data showed FX reserves held by the Swiss National Bank increased for a fifth straight month and to the highest level in nearly one year in a sign that the SNB has moved away from purposely strengthening the swissy. Markets are pricing at least two more 25bps rate cuts by the SNB before year-end which could further weigh on the franc’s value.

CNY Steady service sector activity underpins Yuan. China’s Caixin/S&P Global Services PMI for April met expectations at 52.5, following a slight dip from the previous reading of 52.7. Despite the marginal decline, the report suggests a robust resurgence in demand, with notable upticks in new orders and export business. Buoyed by improved external market conditions and a rise in inbound tourism, the service sector exhibits resilience. Business confidence remains elevated, reflecting optimism for future growth. While no immediate policy shifts are anticipated, moderate adjustments in the exchange rate are forecasted, driven by evolving currency dynamics and external pressures. Technically, CNY maintains stale amid steady economic data, but slight possibility of minor adjustments to the 7.35-7.40 range in the near term. Market attention turns to upcoming data releases, including CPI, PPI, industrial production, and the unemployment rate.

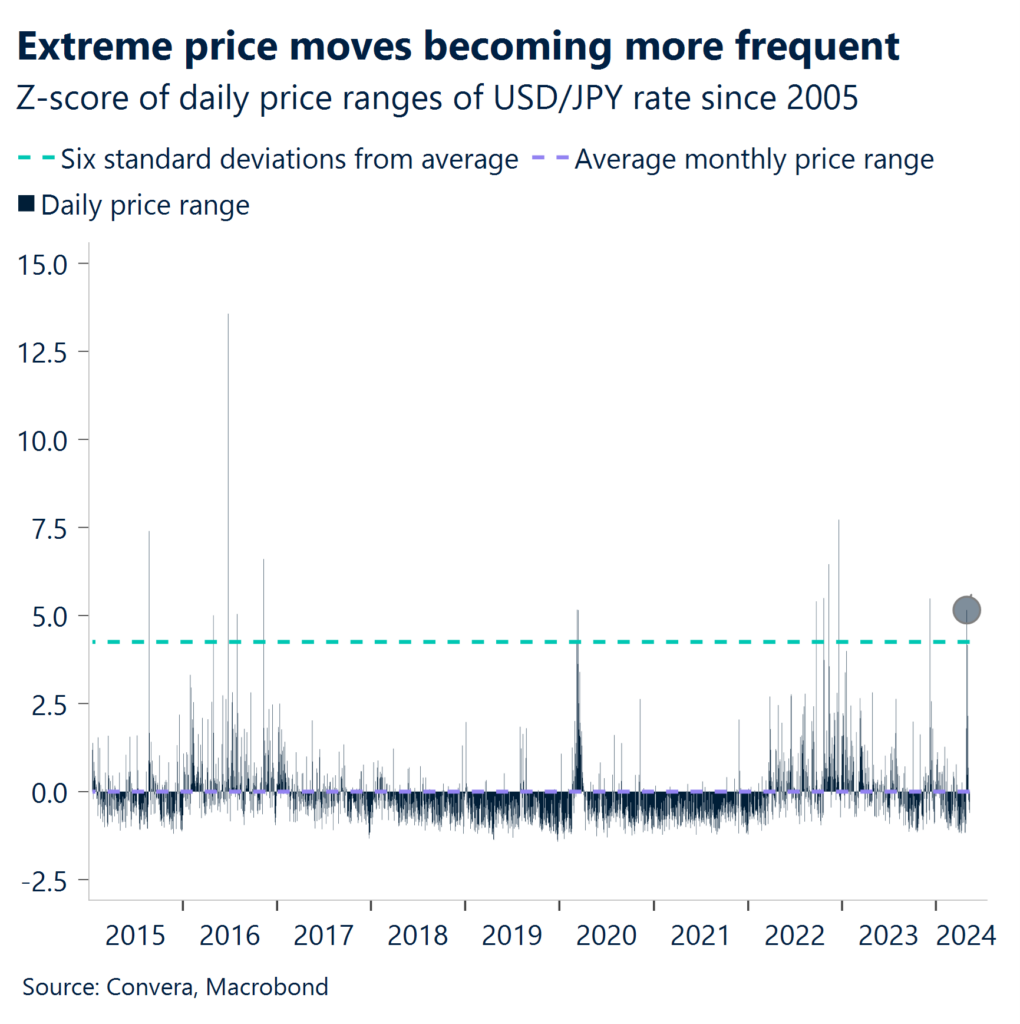

JPY BoJ signals vigilance amid Yen volatility. Bank of Japan (BoJ) Governor Kazuo Ueda hinted at potential policy adjustments in response to yen weakness influencing inflation dynamics. Ueda emphasized the need for vigilance, particularly regarding the impact of currency fluctuations on import costs and consumer demand. USD/JPY retreated to test crucial support levels following its rejection from resistance zones. Technically, USD/JPY undergoes corrective movement, testing key short-term support at 150.265-151.945 after encountering resistance at 158.24-160.33. Focus remains on key economic indicators such as GDP and industrial production for further insights into Japan’s economic trajectory. Ueda’s remarks underscore the central bank’s readiness to act should currency volatility threaten price stability, shaping market expectations amidst ongoing uncertainty. The chart shows extreme price movements are becoming more common recently amid Yen volatility.

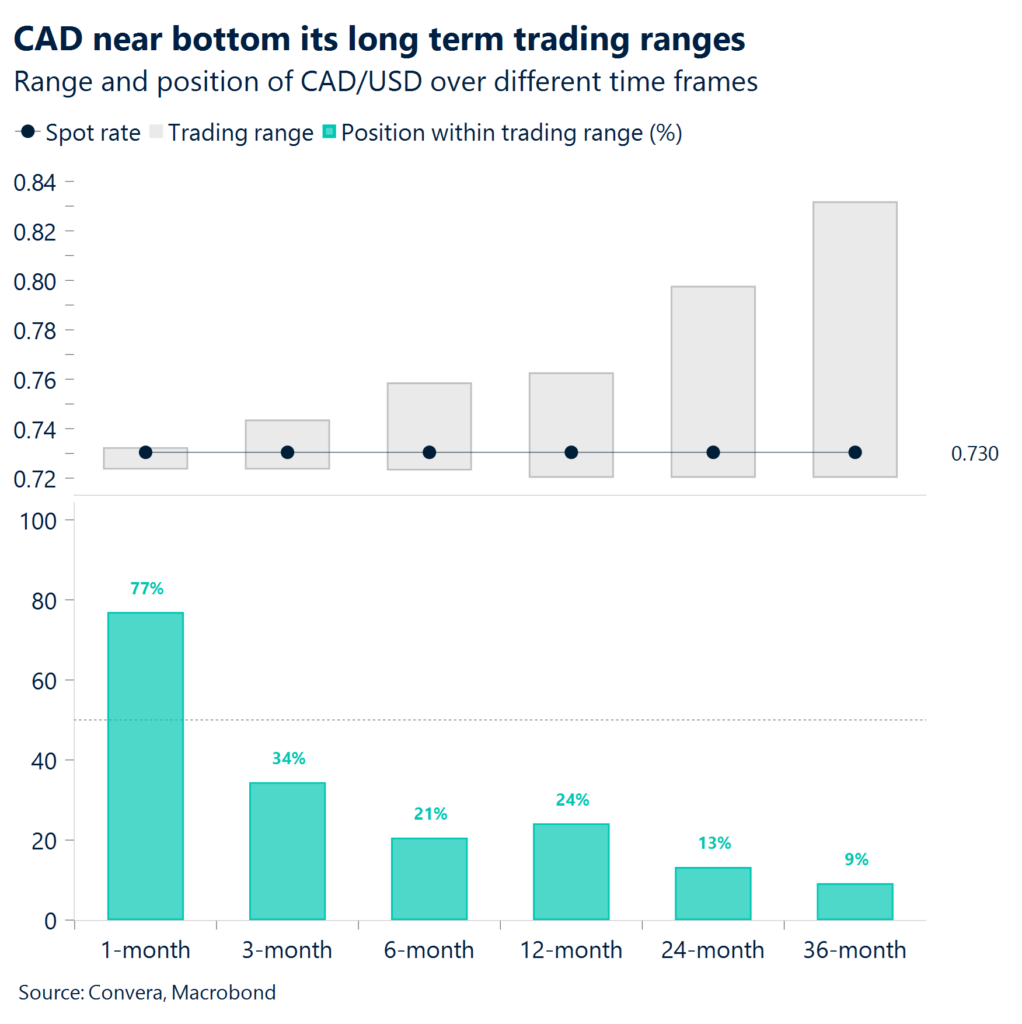

CAD Rescued by softening US data. The Canadia dollar continues to struggle for direction as data cadence slows. Mid-week the US-CA 10-year yield spread widened to a near 3-week high of 87.4bps amid hawkish remarks from Fed officials fuelling the belief that although Fed rate cuts could be delayed, the BoC will still cut rates in June, with USD/CAD touching a 1-week high as a consequence. However, emerging cracks in the US exceptionalist narrative cooled US dollar demand, and USD/CAD pulled back below the $1.37 handle by the end of the week. With realised and implied volatility trending lower and 1-month 25-delta risk reversals largely unchanged, USD/CAD remains broadly range bound between $1.3650 – $1.3750. Looking at technicals, USD/CAD is supported by the 35-day SMA at $1.3660, the level below which CAD has not been able to breach since Mar 20.

AUD RBA maintains status quo, market eyes future moves. The Australian dollar faced selling pressure after the Reserve Bank of Australia (RBA) stood pat on monetary policy, keeping the cash rate at 4.35% as widely anticipated. Notably, the RBA refrained from indicating a clear direction regarding potential rate adjustments, disappointing those anticipating hawkish signals. While acknowledging a gradual easing of inflation, the central bank remains cautious, emphasizing the uncertainty surrounding the optimal path for interest rates. Technically, AUD/USD rallies towards upper resistance levels, converging around the 0.664-0.667 range, reflecting heightened market indecision amid the absence of explicit policy cues. Looking ahead, market focus shifts to key economic indicators such as NAB business confidence, the wage price index, and the unemployment rate.