- Global macro is once again in the driver’s seat when it comes to financial markets and risk sentiment. Chinese stimulus, geopolitical tensions and a back and forth in pricing for the Fed, ECB and BoE are complicating the overall picture.

- Sentiment turned sour this week as the Iranian missile attacks on Israel fueled geopolitical angst over a broadening of the conflict, leading commodity prices to rise by the most since early 2023. Equities declined, while the US dollar gained.

- Investors have pared back their easing bets for the Fed, while increasing their expectations for rate cuts from the BoE and ECB. It seems investors had gone too far in pricing in the divergence between the Fed vs. RoW in recent weeks.

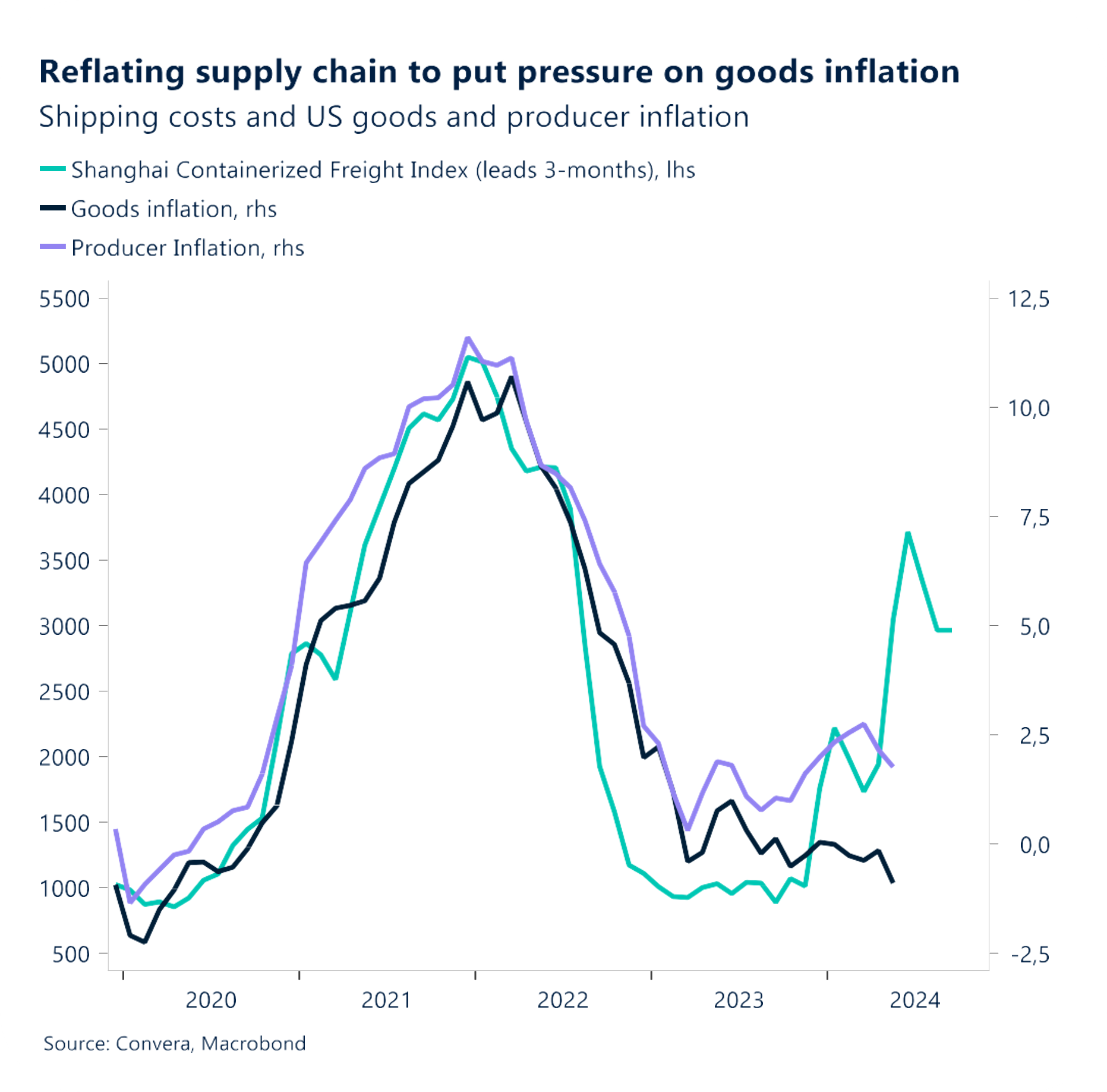

- Inflation is expected to show a continued easing next week. However, the recent dockworker strikes, geopolitical tensions creating commodity headwinds and Chinese stimulus could push goods inflation higher again going into 2025.

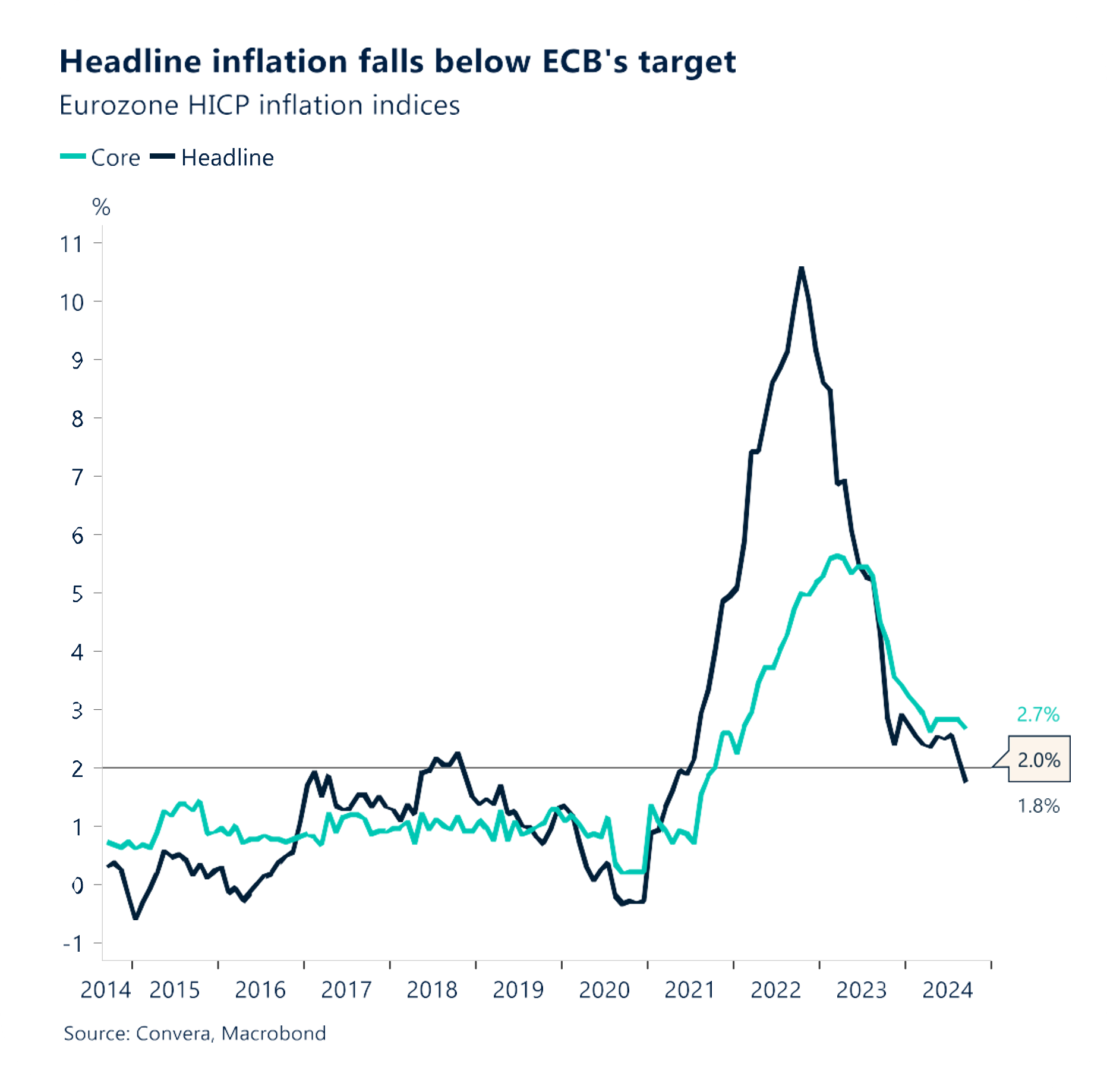

- European consumer prices slowed below the ECB’s 2% target for the first time since 2021, rising by 1.8% year-on-year in September, down from 2.2% the previous month, largely due to a sharp drop in energy costs.

- The US dollar index jumped to its highest in six weeks and is on course for its best week in six months, surging against GBP, EUR, JPY and CHF as central banks around the world appear set to out-dove the Fed.

Global Macro

Global factors complicate the Fed’s job

Chinas stimulus overshadowed. This week’s rebound of the US dollar has created an interesting backdrop going into the inflation print on Wednesday. The efforts from Beijing to stop the equity rout and slowdown in economic momentum have been received quite positively by investors. However, geopolitical tensions and falling rate cutting bets in the US have dampened risk appetite. Fed Chair Jerome Powell’s slightly hawkish tone, coupled with some strong US data has fuelled the rotation into the Greenback.

Rising supply chain risks. Supporting this shift is arguably the dockers strike in the US too, the first such strike since 1977, which has shut down around half of America’s ocean shipping. The longer this persists, the more disruptive it will be, presenting an inflationary risk. Meanwhile, the conflict in the Middle East, causing energy prices to rally, might also prove inflationary if the situation escalates further. Thus, the current skepticism over aggressive Fed rate cuts seems warranted right now, and this is one reason why the US dollar’s rebound could extend in the short term.

Geopolitical focus. A spike in geopolitical risks triggered a surge in safe haven demand. Gold, bonds and the USD, JPY and CHF all rallied, whilst equities and risk-sensitive currencies, like GBP, tumbled. The VIX index, Wall Street’s so-called fear gauge, jumped back above its long-term average, hitting a key level that usually indicates more volatility ahead. Another sign of anxiety that is closely watched by traders is the VVIX – the expected volatility of expected volatility – because this has remained above its long-term average for several months now.

Regional outlook: United States

Stronger growth, less cuts?

Services remain strong. The US’s economic exceptionalism is fuelling the dollar’s gains – with the ISM services PMI rising at its fastest pace since February 2023. However, the dollar’s longer-term trajectory still looks lower amidst the global easing cycle. Despite data this week leading to traders paring back their Fed cutting bets, the odds of the US central bank cutting interest rates by another half-point in November remains around 65%.

ADP, JOLTS rebound. For now, monetary policy by the Federal Reserve largely hinges on the direction of the labour market. Hence, after the rosier job openings figures on Tuesday, followed by Wednesday’s ADP beat, markets have scale back slightly Fed easing expectations by year-end. Less than 65 basis points of cuts are priced in compared to 80bps last week.

Geopolitics comes to the fore. US manufacturing activity shrank in September for a sixth month, reflecting weak orders and declining employment. The prices-paid index fell 5.7 points, the most since May 2023, to 48.3, the first time this year that the gauge has indicated decreasing overall costs. The survey was conducted before a strike at East and Gulf coast ports though, the first in nearly 50 years, and this could potentially push up shipping costs and import prices in the future. Hence with oil prices surging higher and supply chain disruption concerns mounting, inflation worries might start remerging soon.

Regional outlook: Eurozone

Disinflation prompts ECB to reconsider easing pace

Inflation drops below 2%. Consumer prices slowed below the ECB’s 2% target for the first time since 2021, rising by 1.8% year-on-year in September, down from 2.2% the previous month, largely due to a sharp drop in energy costs. Energy prices continued to decline, and inflation slowed for services (4% versus 4.1%), although prices for food, alcohol, and tobacco rose slightly. Core inflation also eased to 2.7%, down from 2.8%. Despite this cooling, the ECB expects inflation to rise again in the latter part of 2024 as the sharp falls in energy prices fall out of the annual comparison.

Investors and ECB sentiment shifting to an October cut. The recent downside miss relative to the ECB’s inflation target has led investors to increase rate cut expectations. With an October rate cut almost fully priced in (23 basis points), market participants are now extending rate cut bets further along the curve. with a rate cut now priced in for every ECB decision until May 2025. The implied terminal rate has fallen below 1.65%, hitting a multi-month low. ECB President Christine Lagarde acknowledged that service prices are easing and core inflation is on a downward trend, a marked shift from the hawkish sentiment a few weeks’ ago.

Investors displeased with Barnier’s fiscal plans. French PM Michel Barnier delayed the target to bring the country’s budget deficit within the EU’s 3% limit by two years, to allow more time to address public finances. He also announced targeted tax hikes to plug the budget deficit, which this year could expand beyond 6%. The market reacted negatively to this announcement, with the yield on French 10-year bonds rising from the week low of 2.78%. The CAC 40 fell 1% on the day, though this was also influenced by headlines concerning an imminent Iranian attack on Israel. Consequently, the 10-year OAT-Bund spread widened by 4 basis points, reaching 78 basis points, near June highs.

Focus: Commodities

China stimulus, Middle East tensions drive gains

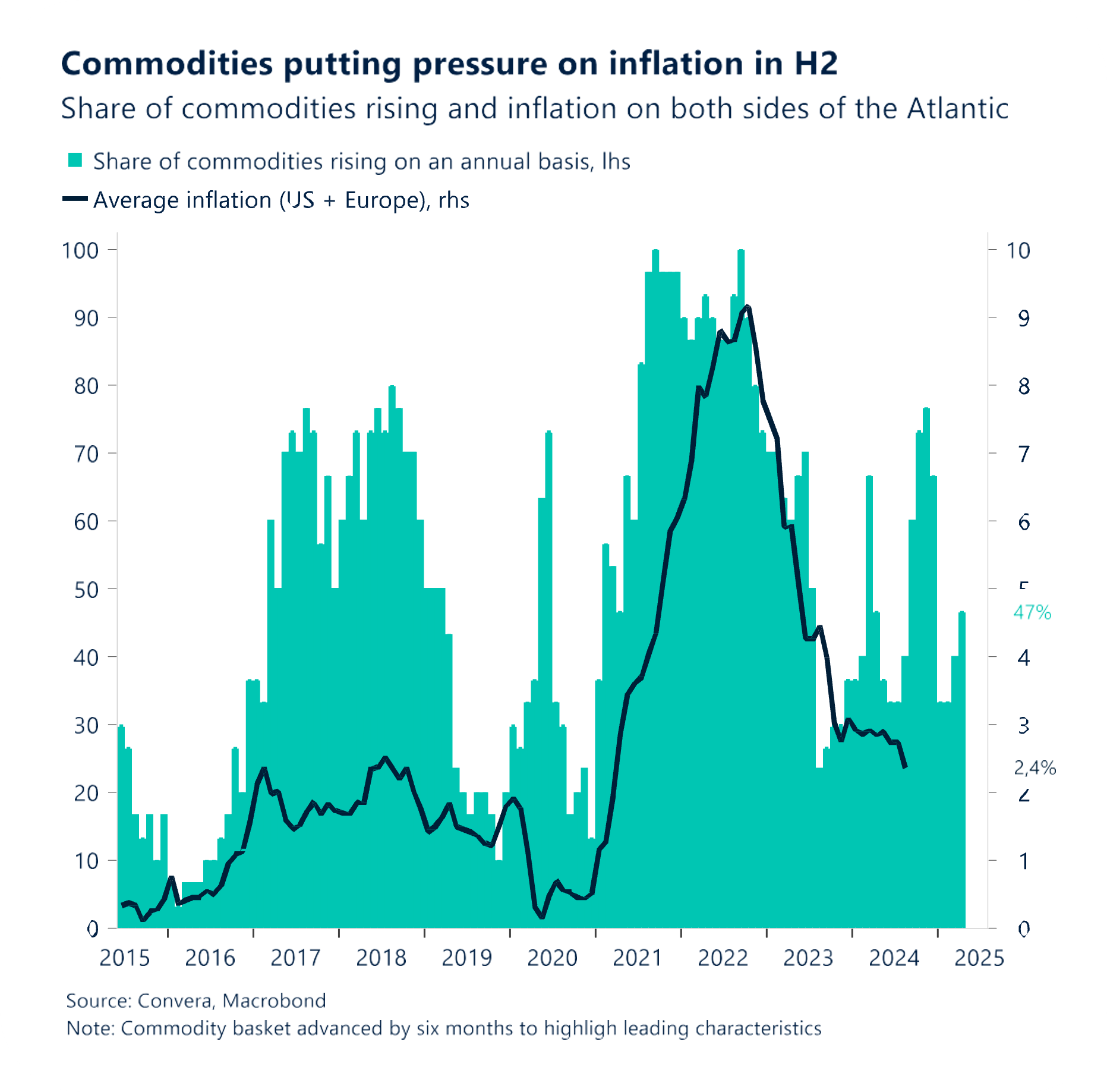

October surge in commodities. While October has only just started, the initial move in commodities is so far unmatched since the huge rally seen after Russia’s invasion of Ukraine in February 2022. Again, geopolitical tensions have been the driver, with WTI crude up almost 10% in the first few days of October after an escalation of encounters between Israel and Iran.

China goes big. Away from energy, industrial metals also saw a massive rally, most notably with iron ore up 22% from its September lows after a series of stimulus measures from Chinese authorities. Commodity market sentiment was boosted by a sequence of moves from Chinese authorities including changes to the Reserve Ratio Requirement (RRR) and cuts to the benchmark medium-term lending facility. The Chinese government also announced new support to the housing market driving further gains.

Aussie, CAD supported. The move in commodities means that while key commodity currencies like the Australian and Canadian dollars have fallen over the week, their losses have been contained versus other major FX markets. For example, while the euro has fallen 2.0% and the GBP fallen 2.5% from recent highs versus the greenback, the Aussie and CAD are down just over 1.0% from their recent highs against the USD. That said, both currencies remain vulnerable to a broader, risk-based sell-off – and their commodity exposure might provide only limited support.

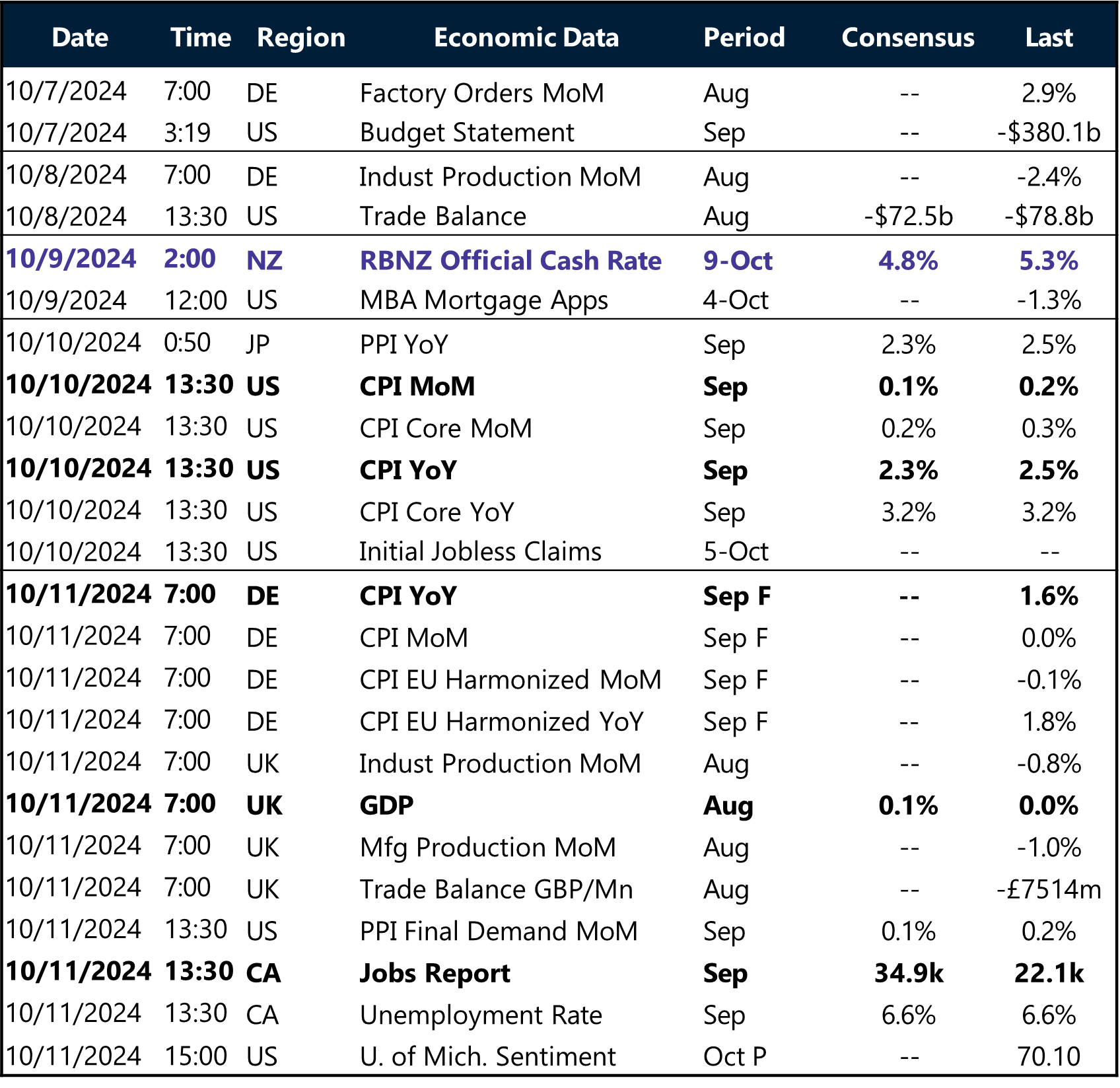

Week ahead

All eyes on US inflation

Nothing in the way of 50. The last two inflation prints in the US set the stage for the Fed to cut rates by 50 basis points as the FOMC was able to switch its focus to the slowing labor market. Consumer prices grew by just 20 basis points in August and July. September could see another risk-positive print of 0.1%, which could push the annual inflation rate from 2.5% to 2.3%. This would bring inflation closer to the Fed’s target and would leave another 50 basis point cut on the table.

Internal disagreement. At the same time, the upcoming Fed minutes from the last meeting will be closely read, as it featured the first dissent from a Fed Governor in almost 20 years. The discussions will reveal to what extent Jerome Powell had to fight to create an almost unanimous decision.

Canadian jobs. One week after the US released its labor market report for September, it is now Canada’s turn. Hiring is expected to inch higher by around 25 thousand. This doesn’t guarantee a fall in the unemployment rate as the pace of the labor force growth continued to accelerate. This could push the jobless rate to 7% going into 2025.

China’s credit. China is set to release some important data points on the monetary front just after Beijing announced pro-growth stimulus measures to boost the economy. Aggregate financing data could show how stronger government funding offset the continued weakness in private-sector credit growth. This data set will be important going forward to gauge how the stimulus is flowing into credit demand and then the real economy via industrial production and retail sales.

FX Views

Dollar rides risk-off wave

USD Sharp reversal thanks to several tailwinds. The US dollar index jumped to its highest in six weeks and is on course for its best week in six months, surging against GBP, EUR, JPY and CHF as central banks around the world appear set to out-dove the Fed. The dollar has a few tailwinds. Its safe haven allure amidst rising tensions in the Middle East kick-started its rebound. Ongoing US exceptionalism with stronger-than-expected US data prompted a hawkish Powell. Rising US Treasury yields as traders pare back Fed rate cutting bets. At the same time, speculation of more easing in Europe were twinned with hesitation at further tightening in Japan. Thus, the US rate disadvantage has narrowed, the gap between 6- and 3-month swap rates in USD versus other major peers has shrunk, and this is boosting the dollar’s yield appeal. In the short term, driven by weakness in other major currencies and haven demand, the dollar’s bullish momentum should continue. Indeed, FX options traders are the most bullish for the USD since July.

EUR Downside risks mount. The escalation in the Middle East has temporarily overshadowed macro developments in FX markets at the start of Q4. The euro was swept up in the risk-off sentiment, dropping over 1% in the past week and testing the $1.10 level, which has held as strong support since mid-August. However, the euro’s bearish trend was already in motion before geopolitical tensions rose, as investors woke up to weakening Eurozone fundamentals and a softer inflation report, which led to a dovish repricing of the ECB’s October meeting expectations. The 2-year US-DE yield spread widened to 160bps, up from September lows of 136bps, further pressuring the euro. French politics also remains a headwind, with 10-year OAT-Bund spreads nearing June highs as concerns about France’s fiscal position resurface ahead of Fitch’s credit review on 11 October. Over the past week, EUR/USD has erased its year-to-date gains, and with lingering US election risks, the outlook for the euro remains skewed to the downside.

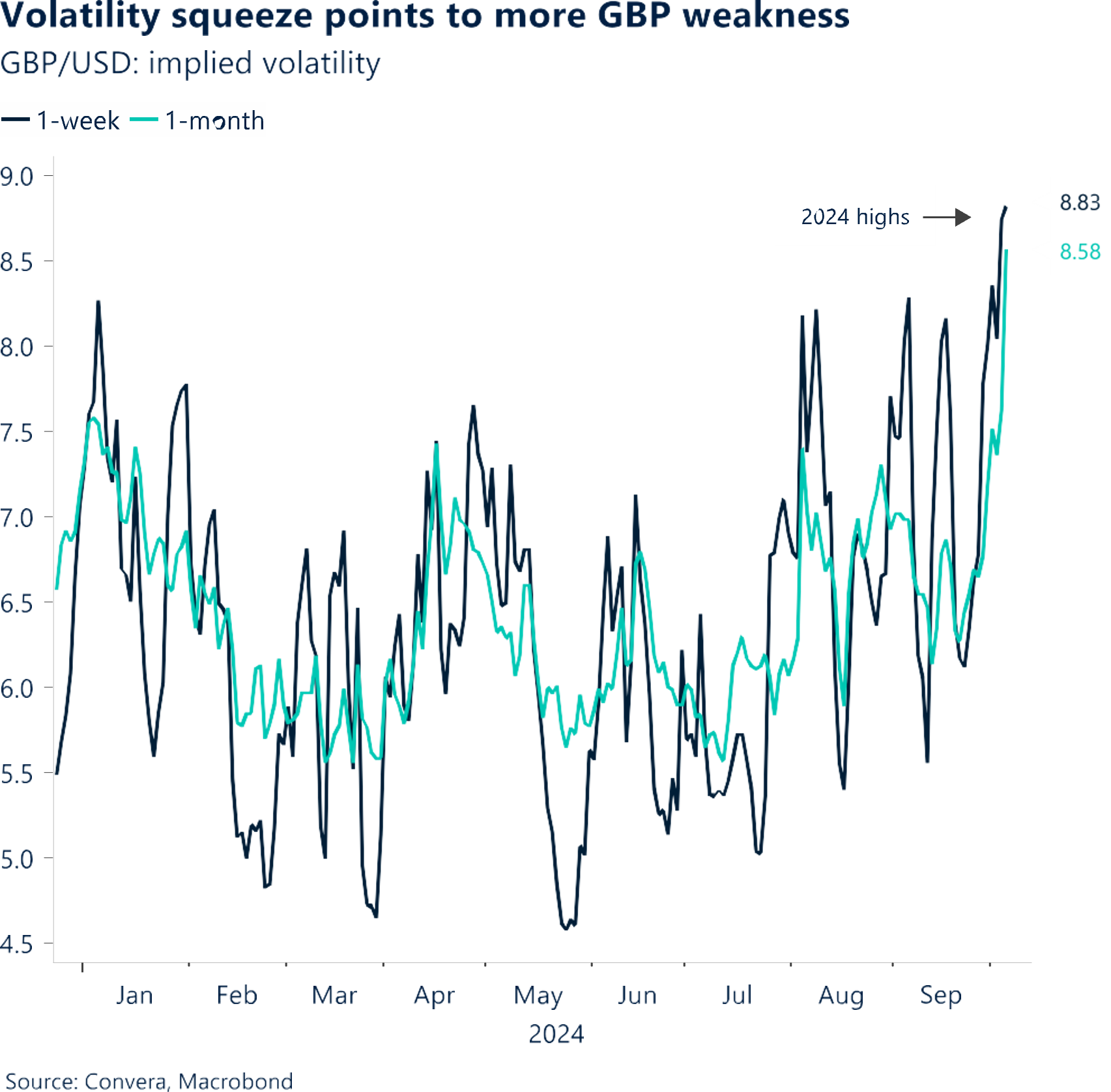

GBP Worst week in over a year. The pound is on track for its worst week since July 2023, hit by the trifecta of risk aversion, solid US data and dovish BoE comments of late. The knock-out blow to GBP/USD was BoE Governor Bailey suggesting a more aggressive approach to rate cuts if inflation continues to improve. Money markets moved to fully price a 25bps cut in November and a 70% chance of a another in December, up from about 40% on Wednesday. We’ve been vocal about the disconnect between BoE pricing and its peers, and saw a dovish recalibration being the biggest risk to sterling’s outlook. The pound slumped more than 1% against both the dollar and the euro in the wake of Bailey’s comments, with GBP/EUR recording its worst day since 2022. With bullish GBP bets overcrowded, the risk is that the pound falls more dramatically if these bets are unwound. Options sentiment in GBP has already reached the most bearish level since mid-August and implied volatility on 1-week and 1-month tenors are at their highest this year as traders scramble to hedge risks. For the pound to pick itself up, several factors need to align, including positive surprises in UK economic data and a de-escalation of tensions in the Middle East.

CHF Surprising lack of safe haven demand. The Swiss franc fell to a 3-week low versus the US dollar this week, erasing the previous week’s gains. Despite tensions in the Mideast flaring, safe haven demand for the franc was contained, and traders favoured the USD. Even EUR/CHF quickly reversed course from 3-week lows despite dismal data from Europe and increased ECB easing bets. We’ve been warning of a weaker franc for several weeks due to it being overvalued against the euro and dollar. Indeed, the new Swiss National Bank (SNB) chief stated this week that although rate cuts are their favoured instrument to weaken the franc, the SNB will not exclude being active in the FX market. So far in 2024, the SNB has refrained from influencing the franc, with data showing it only bought FX worth 103 million francs in Q2, after similarly insignificant purchases of 281 million francs the previous quarter. However, the franc’s resilience over Q3, hampering the country’s exports while inflation is at target, might be a reason to see more FX intervention going into Q4, especially with the risk of CHF attracting safe haven demand amidst rising geopolitical risks.

CNY Chinese market reopening: A critical juncture. On October 8, the local stock market in China will reopen, providing an indication as to whether the recent strong upward trend should continue. With little impact on international commerce, the current stimulus package from China is largely benefiting Chinese assets, particularly in light of the probable decline in US demand. Three reflationary tailwinds for EM assets—a dovish Fed, the end of US exceptionalism, and falling oil prices—coincide with China’s stimulus. Notwithstanding a robust 4Q seasonality, the current events are definitely encouraging for Asian regional currencies. CNY surges to 17-month peak following the stimulus. Following USDCNH’s slight rebound, the bullish potential grew stronger and is currently almost finished with a falling wedge shape—a bullish pattern. Key support line is at 7.00 handle, with next key resistance at 7.20. Future economic disclosures, especially those regarding the FX reserves, should be closely monitored by traders.

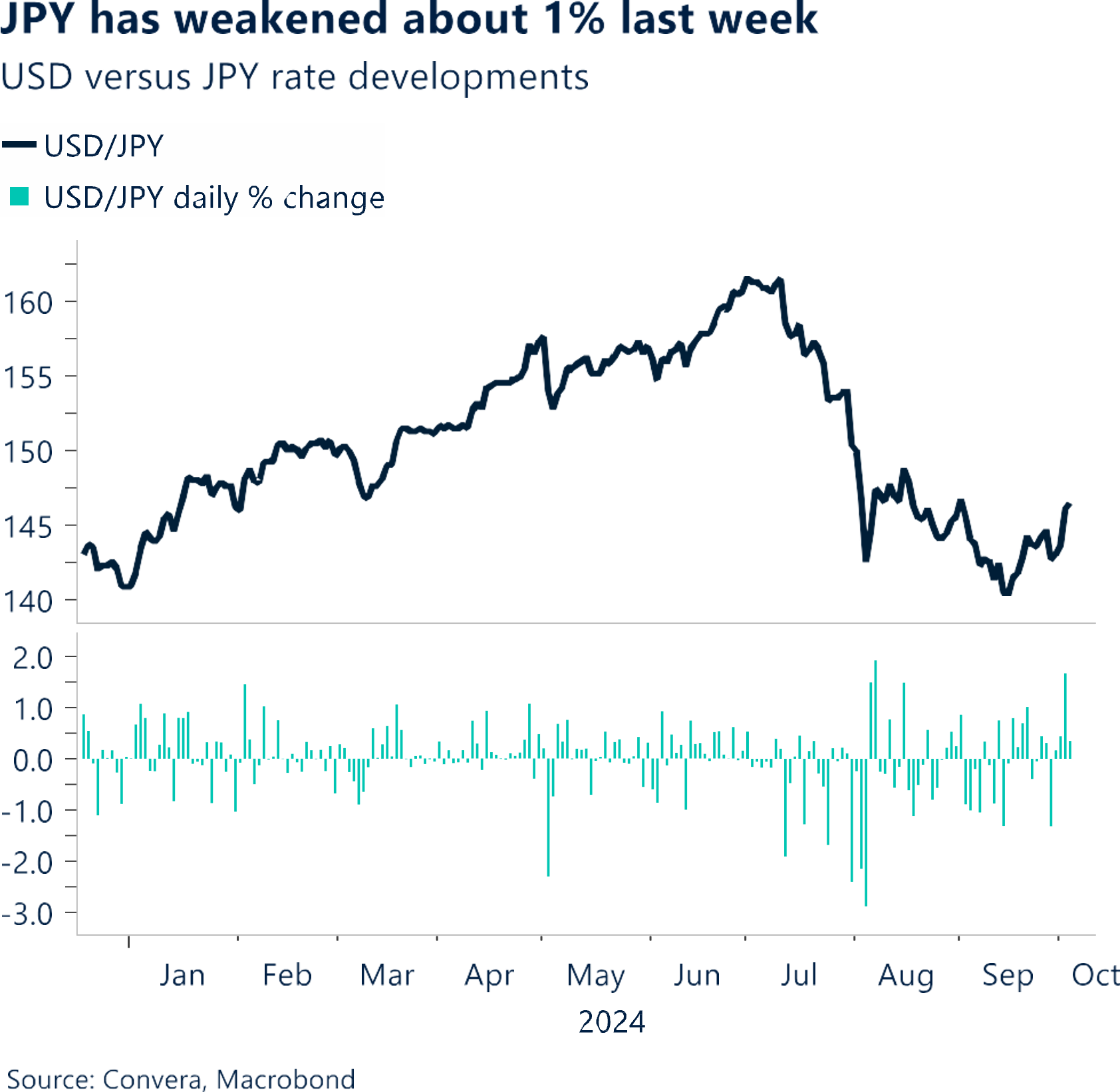

JPY Japanese services sector: Growth momentum questions. Despite the fact that activity was over the crucial 50 level that divides expansion from contraction for the third consecutive month, the September au Jibun Bank PMI services in Japan fell to 53.1 from 53.9 flash and 53.7 in August. Separately, Noguchi, a board member of BoJ, emphasized the need of maintaining easy financial conditions and stated that it would take time for Japanese consumers to change their perception of inflation. He reaffirmed how crucial it is to consider market opinions when formulating policy and stated that the BoJ is not in a rush to shrink the balance sheet. JPY has weakened about 1% last week, and price action suggests further Yen weakening (See chart). Note USD/JPY Year-To-Date performance is still positive gain +3.7%, after correcting from 38-year high of 161.69 on July 3rd 2024. A clearly defined range is maintained by USD/JPY, with significant resistance at 150 and important support levels at 140. Traders need to keep an eye on PPIs, current accounts, and impending household expenditure.

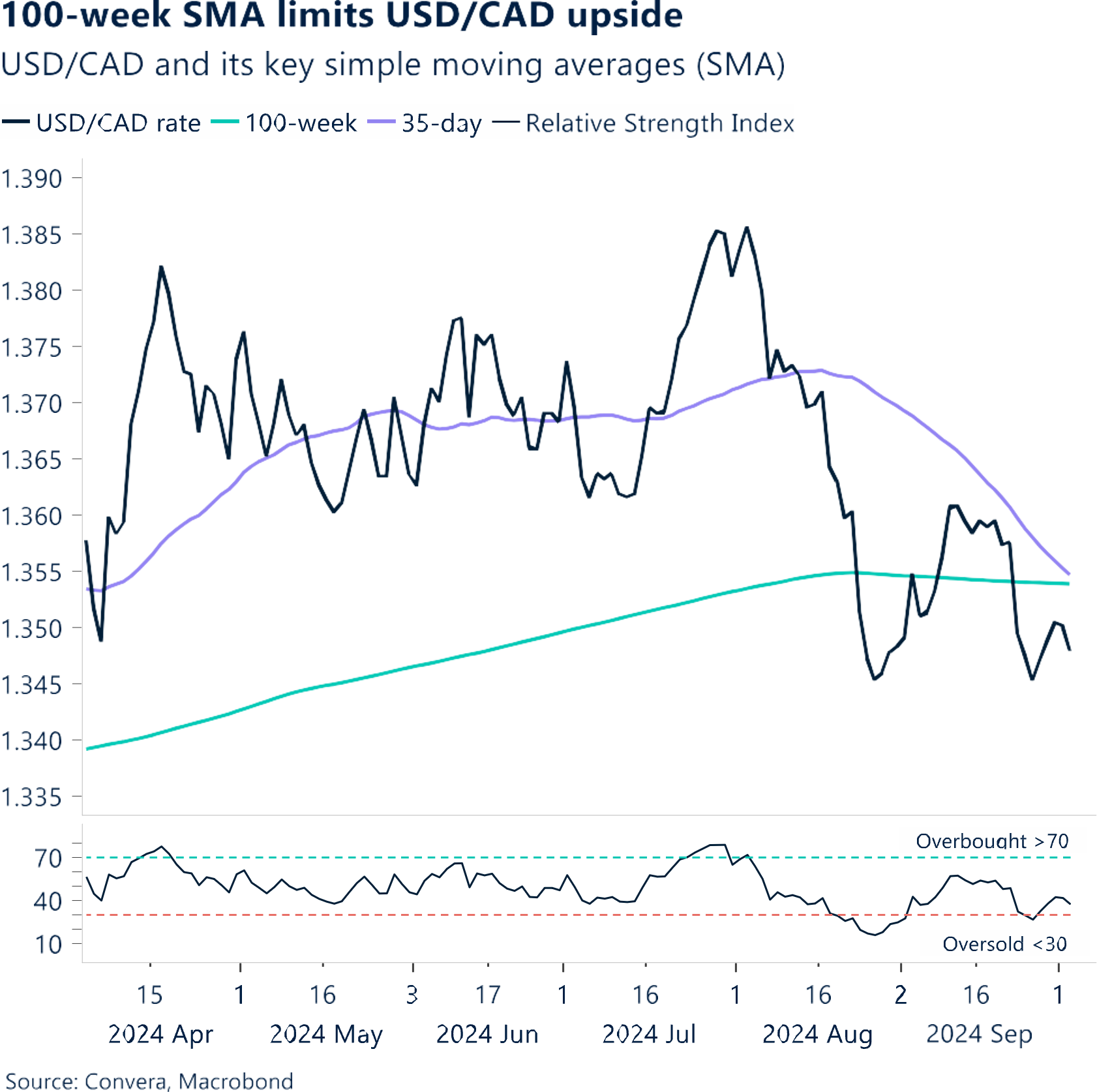

CAD Limited range amid competing narratives. Despite weakening at the start to Q4, the Canadian dollar outperformed within the G10 currency group, driven by competing narratives. Rising tensions between Israel and Iran boosted WTI crude oil prices by over 8% this week, providing support for the loonie through the commodity channel. However, the currency’s gains were curtailed as attention shifted back to macro developments, particularly following less dovish remarks from Fed Chair Jerome Powell. This scaled back expectations of imminent Fed rate cuts, contrasted against bets of faster BoC easing, eroded CAD’s earlier strength. Additionally, the upcoming US election could bolster the US dollar amid heightened risk-off sentiment. Technically, USD/CAD is trading near its 100-week SMA at $1.3537, which may help limit volatility in the pair, despite the downside risks to CAD.

AUD Australian service sector shows signs of cooling. From 50.6 flash and 52.5 in August, the September Judo Bank PMI services in Australia fell to 50.5 as new business growth stalled and export weakness persisted. The economy has not yet benefited from tax cuts and other household stimulus programs put in place at the beginning of the fiscal year. From 51.7 in August, the composite PMI fell into contraction to 49.6 now. The rise in AUD/USD continues to the range highs of 0.68-0.6901 in March 2023–September 2024. Now, the goal for bulls is to stay above 0.68, with the 0.6900 acting as the next resistance. In the grand scheme of things, a persistent range breakout may signal a significant change in the medium- to longer-term tone, particularly if it is bolstered by an ongoing pro-cyclical trend in world markets. Investors want to keep an eye on Westpac’s consumer sentiment and NAB’s business confidence.

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.