The last big week of the year has come to an end with the G3 central banks all deciding not to raise interest rates. However, the Fed’s dovish pivot was enough for markets to continue pricing in aggressive policy easing for 2024, which has led financial markets into full-on risk-on mode. We see two potential risks to this “Goldilocks” scenario, which has seen equities rise to near record highs.

A truly historic Fed meeting. Markets came into the week pricing in significant policy easing from the G3 central banks for next year and it seemed that investors were ready to push back against policy makers expected rhetoric of holding rates higher for longer. However, to the surprise of everyone, investors didn’t need to push back. The Federal Reserve forecast three rate cuts for 2024 and emphasized the progress on the fight against inflation — enough to continue the “everything rally” that started back in November. To highlight how large the deviation of the actual versus the expected FOMC decision and press conference really was, we can look at the post-meeting movements in financial markets. The real US 5-year yield fell by more than 40 basis points, recording its third-largest two-day fall since at least 2005 with cross-asset performance (fixed income, FX and equities) tracked by Bloomberg having its best Fed day since 2009. And while the ECB and BoE did push back against market pricing as expected, it did little to nothing to change investors’ minds about lower rates in the future. Both the Nasdaq and S&P 500 came close to touching record levels, following in the footsteps of the German equity benchmark achieving that feat earlier this week. US equities are on track to rise for the seventh consecutive week, recording their best winning streak since 2017. Markets seem to be priced for a Goldilocks scenario, in which the US economy avoids a recession but weakens enough for the Fed to cut rates by 125-150 basis points next year. The biggest risks going into 2024 will be on the extremes: (1) US economy weakens more than expected or (2) inflation stays above 2% and reaccelerates in the second half of next year.

Global Macro

Last week’s major events

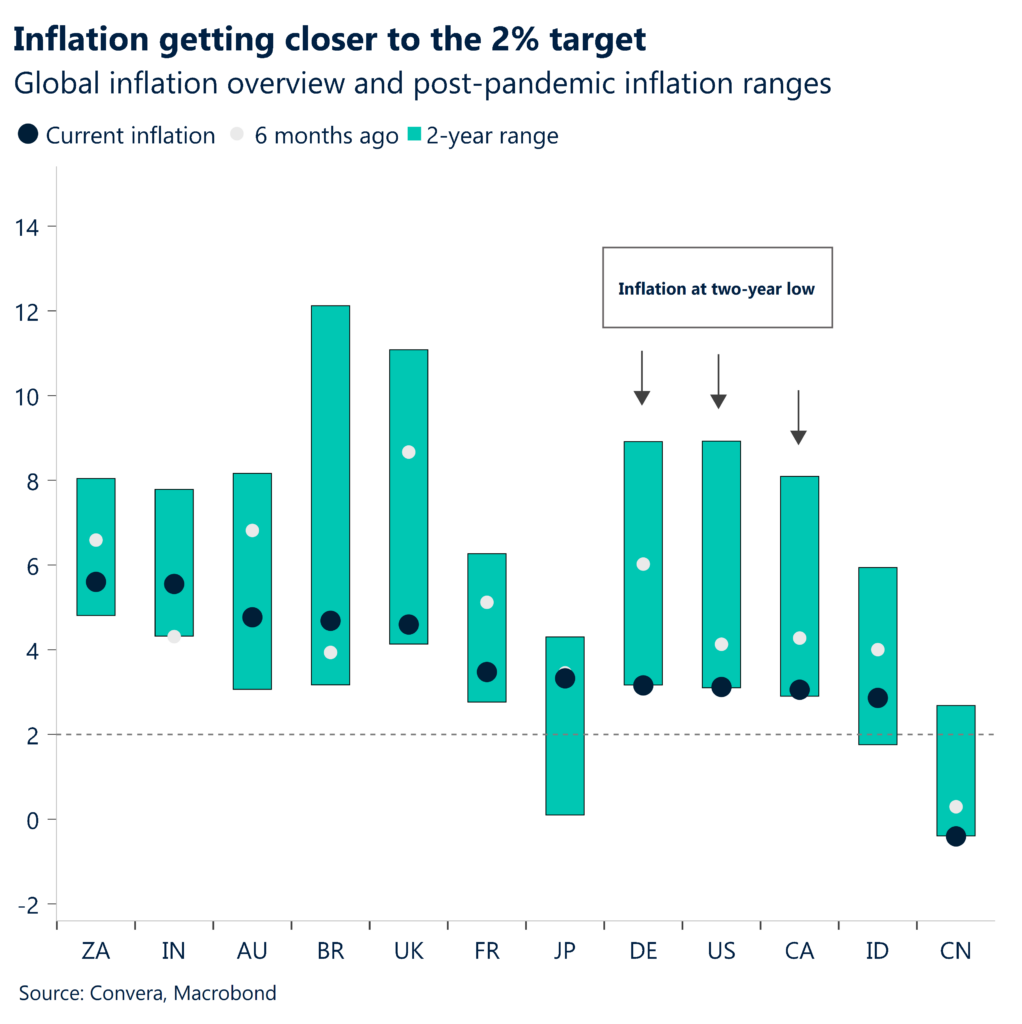

US inflation slowed in November. US inflation came in slightly above consensus, rising by 10 basis points instead of remaining unchanged on the month. Thanks to base effects, however, the yearly rate continued its slow but steady descent in November, falling from 3.2% to 3.1%. Underlying (core) inflation remained sticky at 4%, still twice above the Fed’s target. Still, the report itself won’t be a game changer for policy makers as it came in largely as expected.

But risk of inflation bottoming above 2%. The same cannot be said about US small business optimism falling to a 6-month low. The NFIB barometer pushed lower for the fourth-consecutive month, coming in at 90.6. Looking at the most important two sub-indicators, expected employment and price growth both picked up significantly in recent months to levels that would not be compatible with inflation and wages falling back to their respective 2% and 3% targets. The Atlanta Fed revised up its US GDP Nowcast for Q4 from 1.2% to 2.2%, following a stronger than expected retail sales rise of 0.3% vs. the expected 0.1% decline.

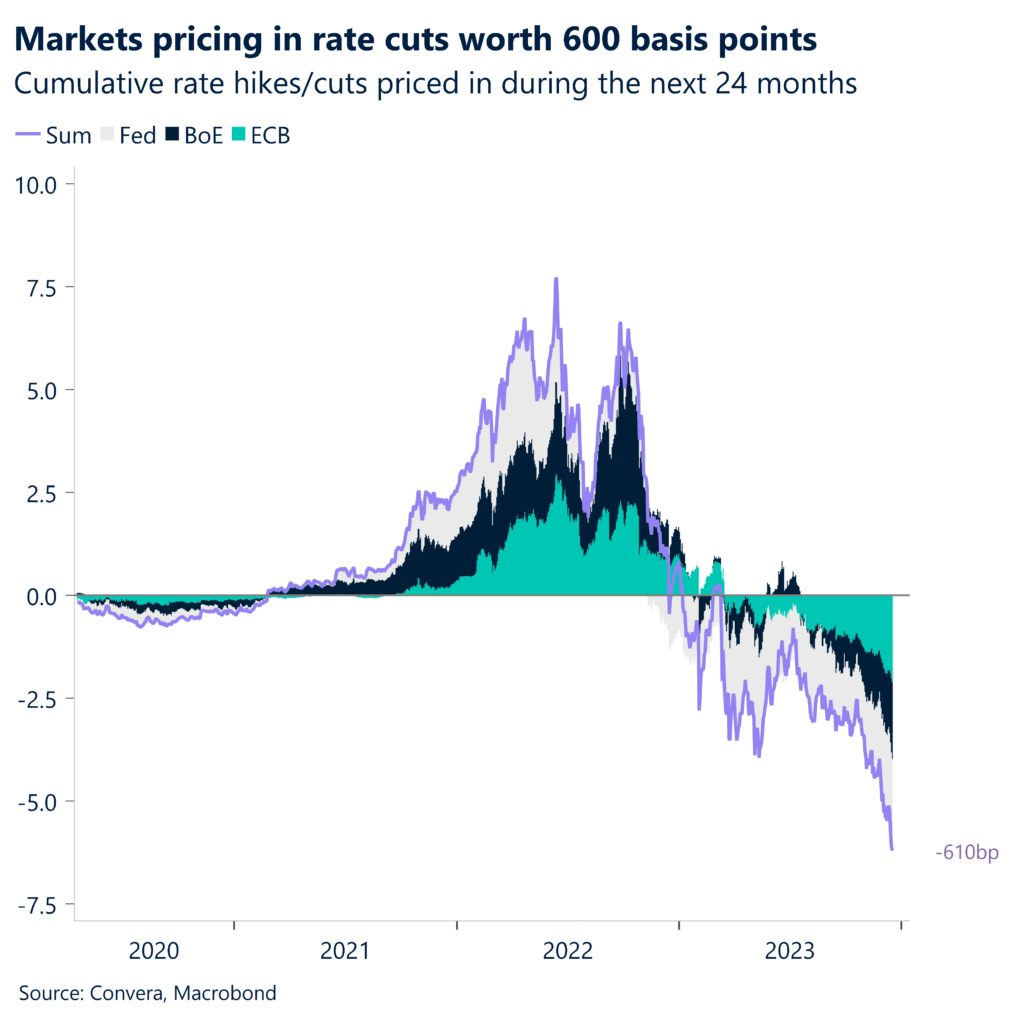

Fed still gave investors the green light. The Federal Reserve’s most aggressive tightening cycle in four decades is officially over. The US central bank left policy rates unchanged at 22-year highs for a third consecutive time, cementing the narrative of peak interest rates and igniting a global cross-asset rally and FX capital allocation away from the dollar. The closely watched dot-plot showed the Fed’s intention of cutting interest rates three times next year. In combination with Chair Jerome Powell not pushing back against the recent easing of financial conditions and emphasizing the positive development on the inflation front and easing labor market conditions, markets took that as a nod to continue pricing in more policy easing in 2024.

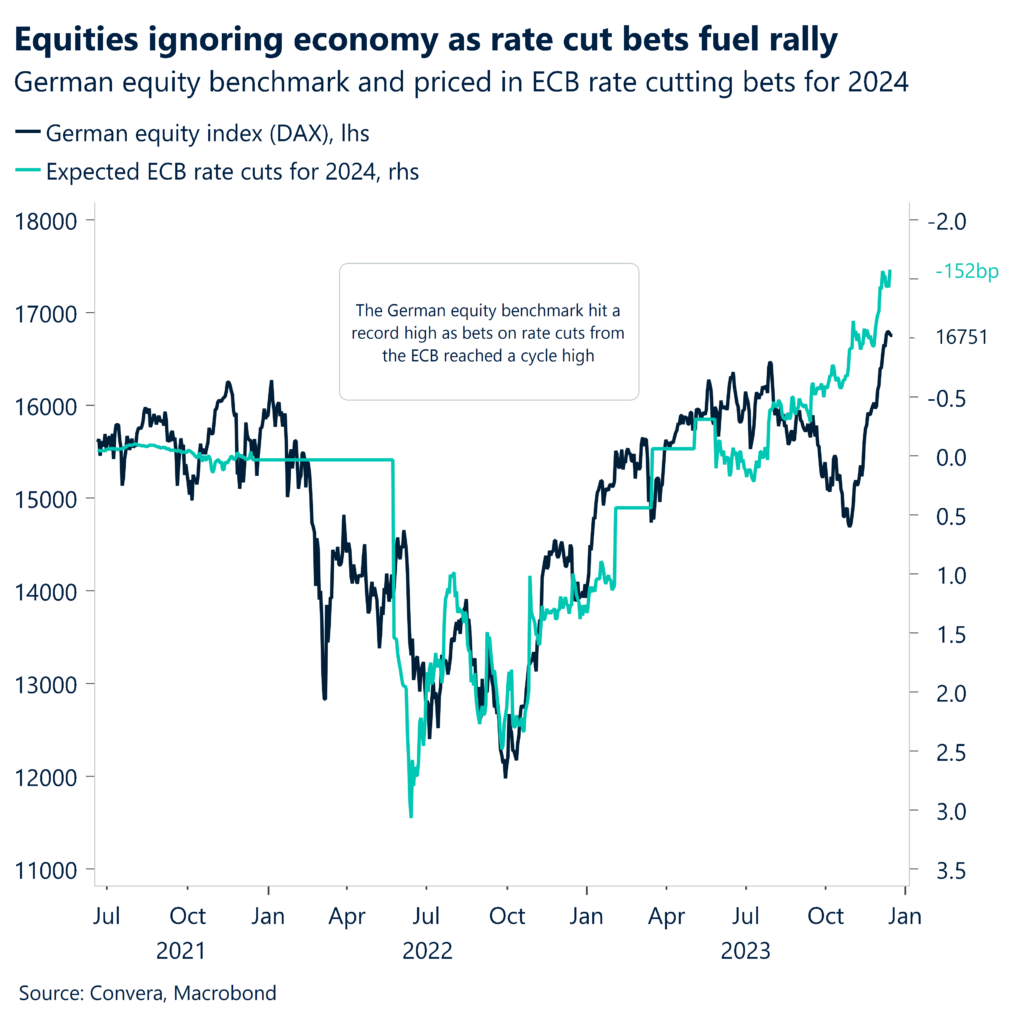

Sentiment is on the rise. German investor morale improved for the second consecutive month and surprised investors to the upside. The ZEW economic sentiment indicator climbed to 12.8 in December reaching a new high since March 2023. Despite an ongoing fiscal budget crisis, economic expectations have once again slightly improved, as more respondents expect interest rate cuts by the European Central Bank (ECB) in H1 2024.

But it’s not a clear-cut recovery. Overall optimism remained depressed going into December, which is highlighted by Friday’s PMI surveys. German manufacturing activity rose for a fifth consecutive month but remained in negative (recessionary) territory. At the same time, the weaker services sector (48.4 vs. 49.6) dragged down the composite PMI deeper into contraction (46.7 vs. 47.8). The worries over the recovery gained traction after the employment barometer fell for a second consecutive month as companies scaled back capacity. Higher unemployment rates have become our base case for the region going into 2024.

But the Eurozone is still expected to fall into recession. A recent Bloomberg survey revealed that the Eurozone is expected to suffer its first recession since the pandemic, in line with our consensus. The weakness ought to be led by Germany as Europe’s largest economy struggles to emerge from its manufacturing downturn while battling a fiscal budget crisis and weak global demand. The survey contrasts with the European Commission forecasts from earlier last month, which foresees the block returning to growth in Q4.

Markets are not believing the ECB. The European Central Bank (ECB) kept its deposit rate at a record high of 4% for the second consecutive meeting as widely anticipated. The euro rallied, adding further gains from an already favourable session on the back of a dovish FOMC meeting. Policymakers have also pledged to maintain rates at sufficiently restrictive levels for as long as necessary, confirming that no rate cut discussions took place with the new projections showing inflation above 2% in December 2024. However, markets continue to price in rate cuts worth 150 basis points throughout next year.

UK wage data starting to fall. This week’s ONS data release showed British wages excluding bonuses rose by 7.3% in the three months leading up to the end of October, compared with the same period last year. Wage growth was below economists’ expectations for a 7.4% increase and is now 0.6% below its multi-decade high reached in August. The unemployment rate, using the new adjusted experimental method, remained unchanged at 4.2% for the fifth consecutive months. However, claimant count change increase for the third month in a row to 16,000 in November, setting a new five month high. Around half of UK industries are now experiencing job cuts, based on the data from the ONS on the number of people receiving paid renumeration.

UK economy contracted in Q3. The last data patch for the third quarter has finally been released and it showed the UK economy falling more than expected in October. Economic activity unexpectedly contracted by 0.3% and more than the 0.1% decline economists had expected. Disappointment was the broad theme of the report published this morning. A weak industrial sector and falling domestic demand have pushed down the Gross Domestic Product, which has now been almost flat since the beginning of 2022. Industrial and manufacturing production fell by 0.8% and 1.1% on the month, both coming in weaker than expected.

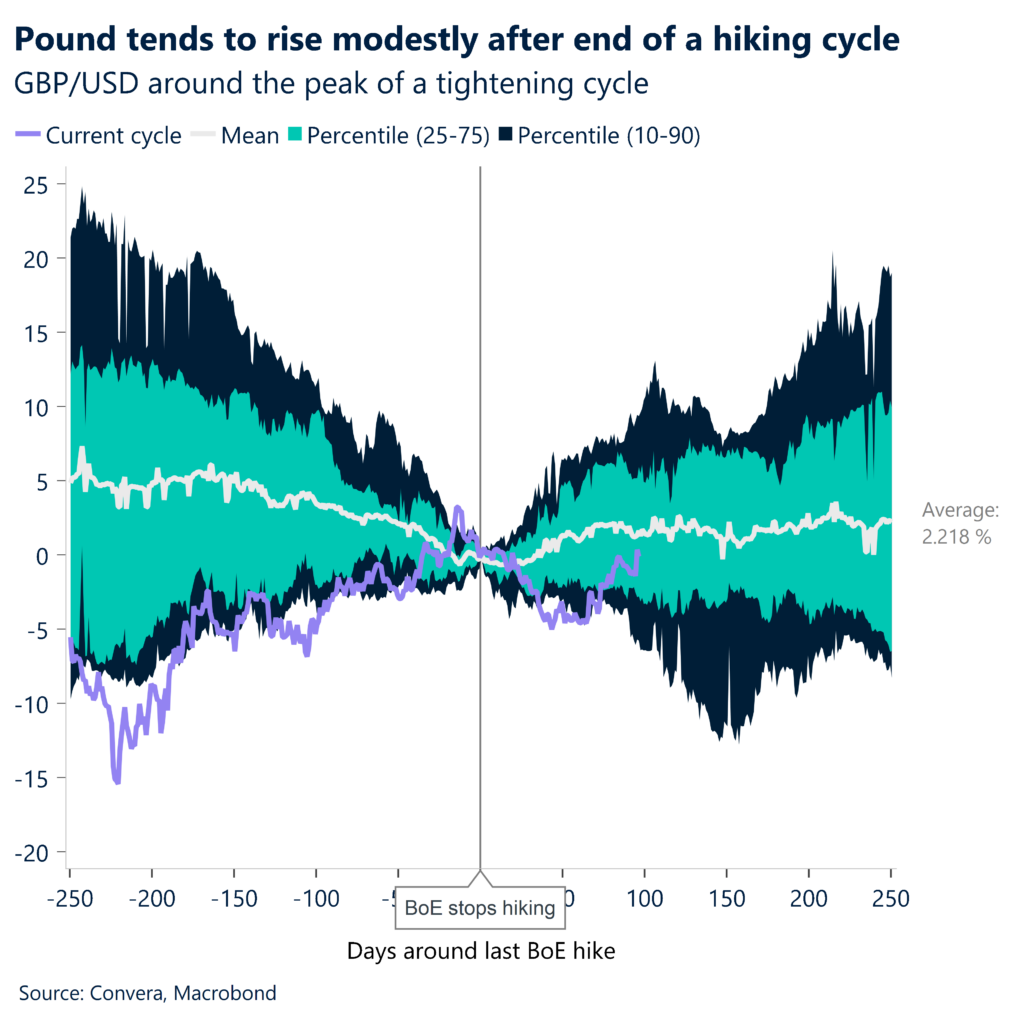

BoE delivers a hawkish hold. The Bank of England left policy rates unchanged at 5.25% and pushed back against rate-cut speculation. The Monetary Policy Committee voted 6:3 to keep rates at 15-year highs of 5.25% with Governor Andrew Bailey emphasizing the need to continue the fight against inflation. Given still high wage and core inflation rates, the BoE has looked past recent weakness in economic data. Especially, the last two weeks have confirmed a slowing economy with the UK contracting in October and seeing claimant numbers rise. However, policy makers wanted to send a signal that they are in a different camp than the US central bank with three members of the MPC voting to hike interest rates by 25 basis points. And while markets continue to price in significant easing from the BoE due to the Fed opening the flood gates to excessive rate cuts pricing on Wednesday, the pushback has been enough for the pound to benefit.

Global Macro

The view ahead

Inflation reports follow central bank decisions. Following the last central bank meetings of the year, investors will have one last week in December to digest before the holiday season begins. Sentiment data in Germany and the US will come into focus. However, the overall narrative of the week will be driven by inflation data, which will be released in Canada, the Eurozone, UK, US and Japan. This will be the first test for both investors, who have committed themselves to pricing in aggressive policy easing from central banks for 2024, and central banks, which have largely pushed back against the extent to which they might be willing to lower interest rates. Tuesday’s Bank of Japan decision will also be closely watched, as markets assess how likely policy makers are to tweak their monetary policy.

The 7-day look ahead.

Monday (18.12) – Ifo business climate

Tuesday (19.12) – Bank of Japan, Canadian inflation, Eurozone inflation (final)

Wednesday (20.12) – UK inflation, German and US consumer confidence

Thursday (21.12) – US GDP, US initial jobless claims, US Leading Index

Friday (22.12) – Japanese inflation, US PCE inflation

All dates GMT

FX Views

G10 FX appreciating vs. USD without exception

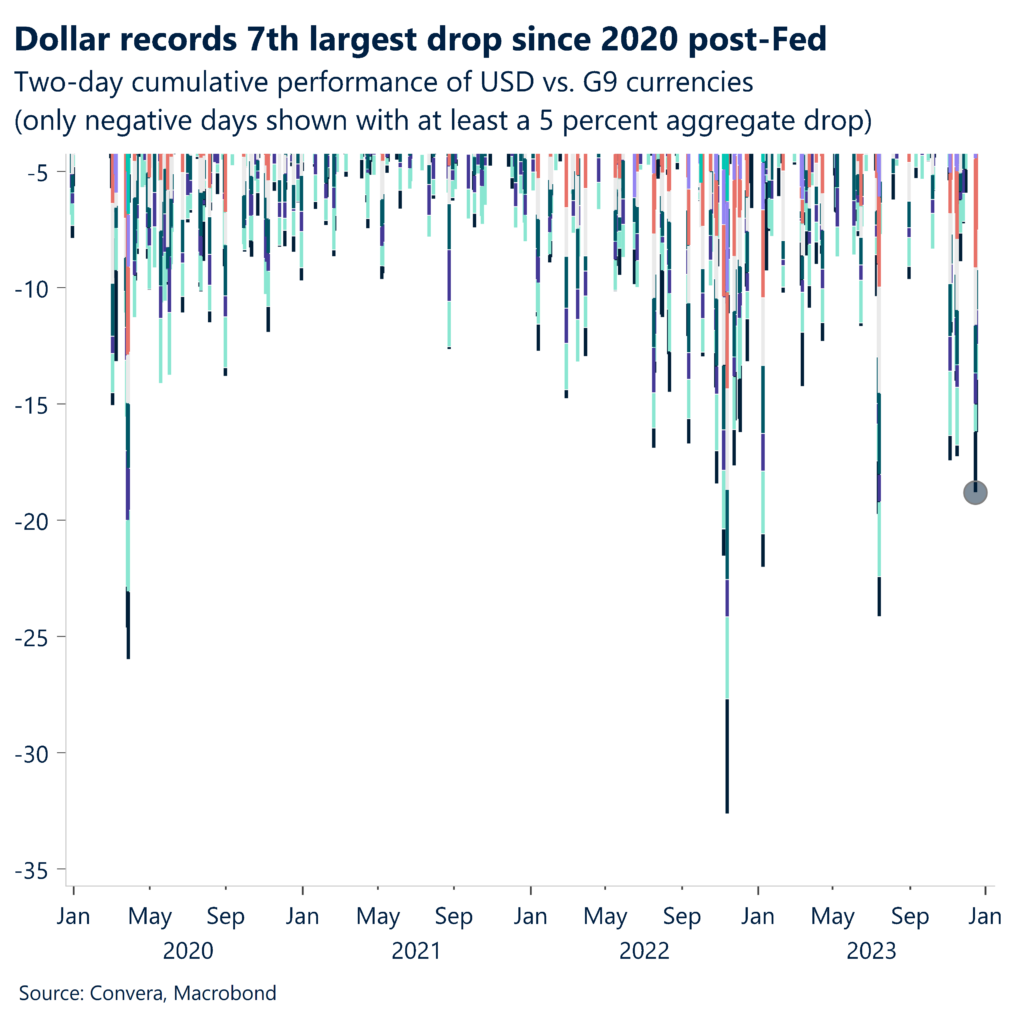

USD Collateral damage from the dovish pivot. Markets are currently pricing in an incredible six rate cuts from the Fed for 2024, starting in March, resulting in the dollar’s worst post-Fed performance since 2009. In fact, the greenback has fallen against every currency in the G9 basket and has recorded its seventh worst two-day aggregate fall since the pandemic. DXY is now trading around the 102 mark and 5% below its October peak. That said, the US economy continued to outperform its peers over the last week, with retail sales beating expectations and inflation falling less than expected. However, the gravitational pull from the Fed has proven difficult for FX traders to ignore. Momentum is dominating the narrative right now and the greenback will need an upside surprise on the inflation front next week to establish a bottom going into years end.

EUR ECB pushes back. The euro rallied to a fresh 2-week high against the US dollar following a dovish Fed hold and hit the $1.10 mark as Lagarde delivered a surprisingly hawkish pushback. The ECB kept its deposit rate at 4% for the second consecutive meeting but announced its intention to fully discontinue PEPP program by the end of 2024. This will put all policy tools into a tightening mode. The newly updated central bank forecasts for inflation and real GDP growth were downgraded for 2024 and 2025, skewing risks for early policy easing. Investors have priced out March rate cuts but continue to expect around 150bps worth of cuts over the course of next year despite ECB’s best efforts to convince otherwise. The euro is on track to gain over 1.7% against the US dollar this week, the third best weekly performance of the year. However, the current pricing for EUR/USD looks stretched, so we will be expected to see pullback over the course of next week. The pair could find support at 21-day SMA around $1.0880 level in the short term with more available at the 100-day SMA at $1.0809.

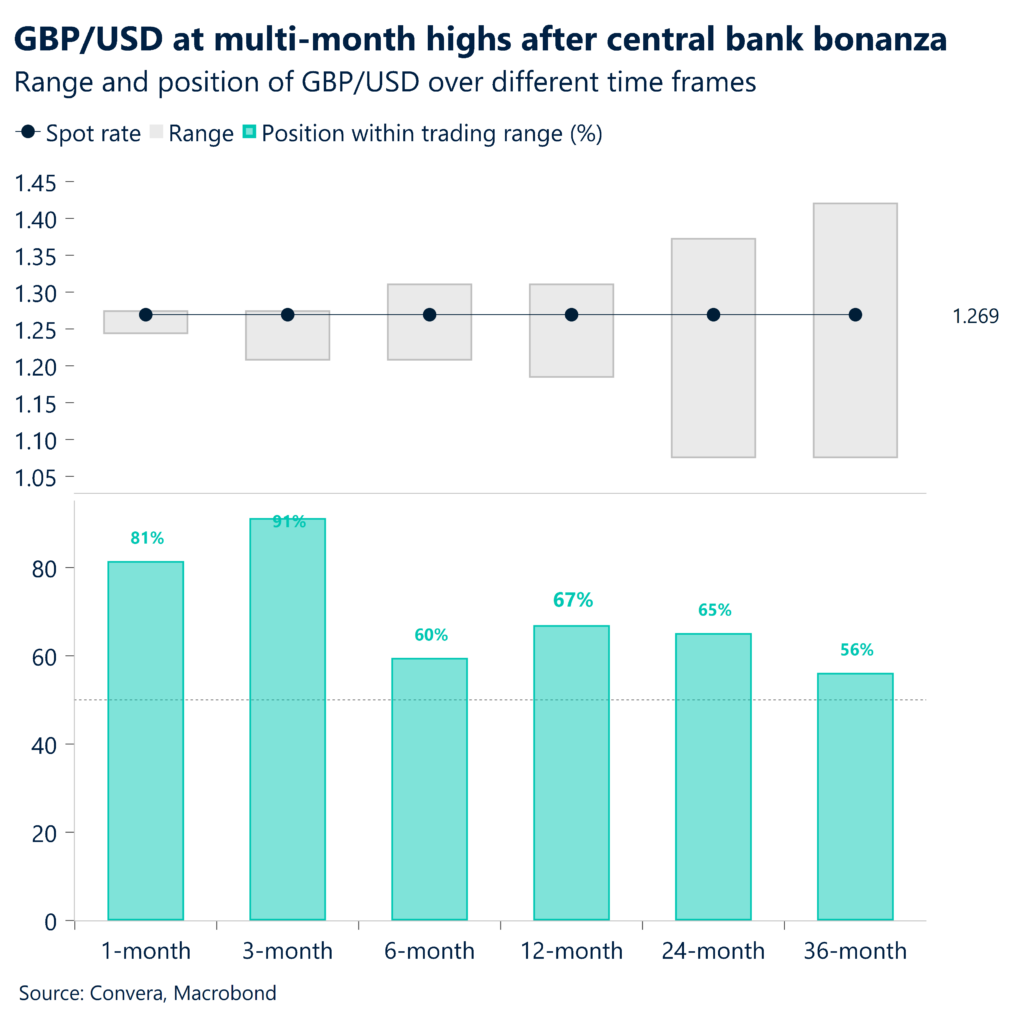

GBP Remarkable recovery after hawkish BoE. Broad US dollar weakness and a hawkish BoE hold saw cable appreciate past the $1.27 handle and touch a fresh 3-month high. The MPC voted to keep rates at 15-year highs of 5.25% with Governor Bailey emphasizing the need to continue the fight against inflation. BoE sent a clear signal that it is not following in Fed’s footsteps, despite a contraction in GDP growth in October, as wage and core inflation rates continue to run high. And while markets are continuing to price in four rate cuts from the BoE, the pushback was enough for the pound to benefit in the near term. Looking ahead as technical indicators point to an overvalued pricing, we expect the GBP/USD rally to run out of steam and retrace from multi-month highs. Cable faces resistance at 200-week SMA at $1.2840, capping any further short-term gains. Meanwhile, support can be found at 14-day SMA at $1.2636 level as investors continue to digest the news and assess the longer-term implications of central bank decisions.

CHF SNB calls end to hikes. The Swiss franc was mostly lower over the last week as the Swiss National Bank signalled an end to its rate-hiking cycle. Following the decision, SNB President Thomas Jordan said: “Price stability is already ensured given our newest inflation forecast.” Notably, headline annual inflation in Switzerland has fallen to 1.4% – down from a peak of 3.5% in mid-2022 – meaning the SNB has less reason to keep policy restrictive. The SNB sees Swiss inflation at 1.9% at the end of 2024. The EURCHF climbed sharply from major support at 0.9400. This level – the lowest since the 2015 “flash crash” – is seen as a key psychological level for the SNB. A move below this level might trigger intervention. While lower in most markets, the CHF gained versus the US dollar – in line with most other currencies – as the greenback fell after the Federal Reserve policy decision. The USDCHF fell to four-month lows and remains in a clear downtrend with both 100- and 200-day moving averages pointing lower. Support is seen at 0.8620 and 0.8550. We’ve got a quiet week ahead with trade balance due on Tuesday and the SNB Bulletin due Wednesday.

CAD 2 ½ – month high on sustained USD selling. USD/CAD plummeted to a near three-month low below the $1.3400 level as the FOMC delivered a dovish tilt and gave markets the clearest signal yet that its aggressive hiking campaign is finished. The dovish Fed, along with the risk-on mood shown by an extension of the rally in the global equity markets continue to weigh heavily on the greenback. Meanwhile, crude oil prices are on track for the first weekly rise in two months spurred on by a bullish forecast from the IEA for oil demand for 2024, acting as a tailwind for the loonie. USD/CAD is on track to record its 2nd largest weekly depreciation of the year and is over 3.5% below its recent 13-month high. Going forward, there is scope for further weakening in the near-term. If the pair breaks past the September low of $1.3377, this opens the door for the April bottom of $1.3300. However, in the short-term, momentum indicators are pointing to overstretched conditions – the USD/CAD might gain over the coming weeks.

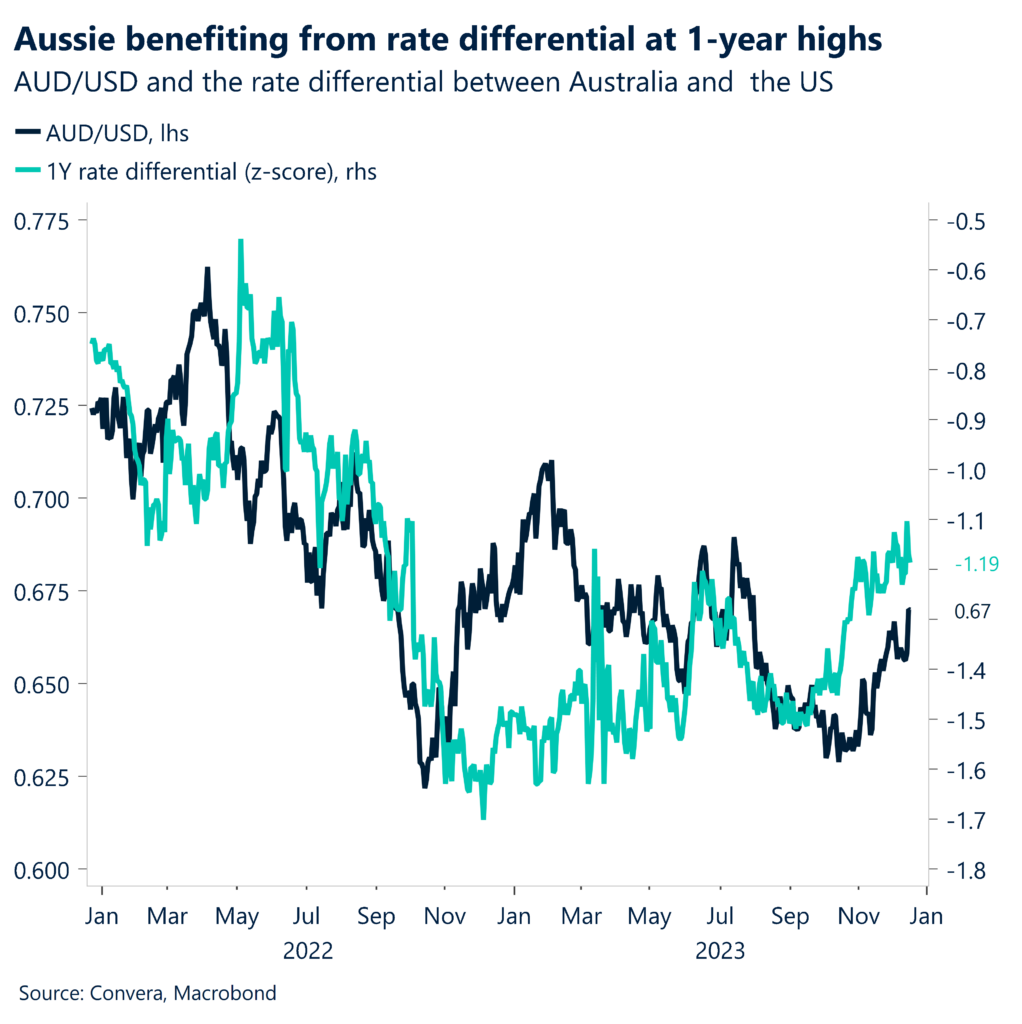

AUD Employment surge and fiscal strength in focus. The AUD has recorded a weekly gain of 1.5%, yet it still lags behind the year-to-date (YTD) performance with a decrease of 1.7% against the dollar. Despite this, the AUD is currently positioned above its 21-day EMA and 100-day EMA due to improved risk sentiment following the Federal Reserve’s pause. The Westpac consumer confidence index concluded 2023 as its second-worst year, reflecting negative sentiment amid rising rates, despite a minor December uptick. Concurrently, the National Australia Bank’s business confidence indicator plummeted to -9 in November, the lowest since 2012, potentially indicating increased caution among companies for 2023 investments and hiring. However, November’s employment report surprised positively with a significant surge in job growth and labor participation. Fitch Ratings highlighted Australia’s strong fiscal position relative to peers. Nevertheless, with consumer sentiment struggling and global headwinds prevailing, the RBA may need to consider rate cuts in 2024 to sustain growth . From a technical perspective, the AUD/USD remains in a long-term downtrend – since Q1 2021 – and it remains possible to retest the 4Q23 low of 0.6269 and the 4Q22 low of 0.6170 before concluding this bear market. Key data to watch next week includes housing credit, private sector credit, and the MI leading index.

CNY Stronger, despite retail sales dip and property sector challenges. The yuan continues to fluctuate around 7.11 per dollar. Over the last week, the USDCNY fell 0.6%, in line with the medium-term trend – the USDCNY is below both the 100- and 200-day moving averages in a sign of weakness for the pair Over the longer term, the CNY has struggled, with the USD/CNY’s YTD performance of +3.09%. The People’s Bank of China (PBoC) maintained its medium-term lending facility rates, while November’s data showed mixed trends. Retail sales growth disappointed at 10.1% y/y, reflecting ongoing consumer weakness amid falling incomes and deflationary pressures. However, industrial production surpassed estimates, likely due to front-loaded stimulus and easier base effects. Property investment continued to decline, down 9.4% y/y in Jan-Nov, with home prices still decreasing despite partial easing by local governments. All eyes will be on foreign investment and PBoC loan prime rate next week. Support seen around 7.10.

JPY BoJ policy in focus. While USD/JPY fell around 1.5% last week, it’s crucial to highlight its robust year-to-date (YTD) performance, which stands at an impressive 8.3% gain. The latest Tankan survey, indicating firms’ inflation views exceeding 2% through 2025, has fueled speculation that the Bank of Japan may finally normalize ultra-loose settings. However, December’s flash PMI revealed manufacturing contracting quicker on soft demand, with input cost growth accelerating further. The services gauge improved slightly to 52 in December from 50.8 in November, while the composite PMI experienced a small expansion to 50.4 in December from 49.6 in November. Despite upbeat Tankan big manufacturer sentiment, real sector uncertainty persists, limiting the BOJ’s ability to adjust crisis-era policy support presently. While future yen appreciation is now more likely because the Fed has paused, the unclear timing for BoJ action keeps USD/JPY rangebound for now. From a technical standpoint, the 50% retrace of 2021 — the 127.25 January 2023 low — and the 125.86 June 2015 top, serve as longer-term support levels. Core focus for next week include the BoJ Monetary Policy Statement and rate decision, trade balance, and national CPI.